You might also like

- Slides 5Document41 pagesSlides 5Gonçalo AlmeidaNo ratings yet

- MBA Finance and Financial Management: Bond, Equity and Firm ValuationsDocument52 pagesMBA Finance and Financial Management: Bond, Equity and Firm Valuationsconstruction omanNo ratings yet

- Corp Fin 3Document25 pagesCorp Fin 3Nguyễn GiangNo ratings yet

- SectionE 1Document101 pagesSectionE 1Michael ChanNo ratings yet

- S 8 - Valuation of StocksDocument14 pagesS 8 - Valuation of StocksAninda DuttaNo ratings yet

- Principles of Asset Pricing Unit e LecturesDocument42 pagesPrinciples of Asset Pricing Unit e LecturesgiggalipufNo ratings yet

- Review - Bond & Stock ValuationDocument24 pagesReview - Bond & Stock ValuationkerenkangNo ratings yet

- Investment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsDocument5 pagesInvestment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsNitesh KirarNo ratings yet

- Chapter 5Document59 pagesChapter 5Shrief MohiNo ratings yet

- An Introduction To Security Valuation: Dr. Amir RafiqueDocument34 pagesAn Introduction To Security Valuation: Dr. Amir RafiqueUsman MahmoodNo ratings yet

- CH 09 Bonds & ValuationDocument35 pagesCH 09 Bonds & ValuationtyoshinoNo ratings yet

- Valuation of Bond & EquityDocument30 pagesValuation of Bond & EquityngbopNo ratings yet

- Investments FINA-3720 Ligang Zhong: Lectures 12 & 13 (Chapter 18) Equity Evaluation ModelsDocument46 pagesInvestments FINA-3720 Ligang Zhong: Lectures 12 & 13 (Chapter 18) Equity Evaluation ModelsroBinNo ratings yet

- Corporate Finance - Lecture 3Document40 pagesCorporate Finance - Lecture 3Faraz BodaghiNo ratings yet

- Chapter 6.valuation of SDocument48 pagesChapter 6.valuation of SPark CảiNo ratings yet

- Lecture 3Document28 pagesLecture 3sandhurstalabNo ratings yet

- Chapter 6.VALUATION OF SDocument48 pagesChapter 6.VALUATION OF SChâu Nguyễn thịNo ratings yet

- Chapter 8Document36 pagesChapter 8evan.billonNo ratings yet

- BU7300 Week 3 Cost of EquityDocument25 pagesBU7300 Week 3 Cost of EquityKawther Moh'dNo ratings yet

- Bond ValuationDocument58 pagesBond Valuationpassinet100% (1)

- How to Value Common StocksDocument48 pagesHow to Value Common StocksPrajval Somani100% (2)

- Key Bond Concepts ExplainedDocument21 pagesKey Bond Concepts ExplainedAntonio C S Leitao100% (1)

- Week 5 SlidesDocument37 pagesWeek 5 SlidesKarthik RamanathanNo ratings yet

- Stock Valuation Models and Techniques for Fundamental AnalysisDocument43 pagesStock Valuation Models and Techniques for Fundamental AnalysisAna Paula Yucra de LuNo ratings yet

- Equity Valuation: Learning ObjectivesDocument25 pagesEquity Valuation: Learning Objectivesswastik guptaNo ratings yet

- CH 05 - Bonds, Bond Valuation, and Interest RatesDocument53 pagesCH 05 - Bonds, Bond Valuation, and Interest RatesSyed Mohib HassanNo ratings yet

- Discounted Cash Flow ValuationDocument35 pagesDiscounted Cash Flow ValuationRemonNo ratings yet

- Session 05Document34 pagesSession 05Alvaro Enrique Vargas BenitesNo ratings yet

- Stock ValuationDocument17 pagesStock ValuationbmunirbNo ratings yet

- Chapter 2: Valuation of Stocks and Bonds: 2.1 Time Value of MoneyDocument61 pagesChapter 2: Valuation of Stocks and Bonds: 2.1 Time Value of MoneyDhara dhakadNo ratings yet

- Bond Basics ExplainedDocument43 pagesBond Basics ExplainedNurhastuty WardhanyNo ratings yet

- Equity ValuationDocument36 pagesEquity ValuationANo ratings yet

- S 4,5 - TVM Discounted Cash Flow ValuationDocument23 pagesS 4,5 - TVM Discounted Cash Flow ValuationAninda DuttaNo ratings yet

- Chapter 2Document16 pagesChapter 2Eldar AlizadeNo ratings yet

- FIN3009 Financial Management: Topic 5: Bonds and Bond ValuationDocument72 pagesFIN3009 Financial Management: Topic 5: Bonds and Bond Valuationkc103038No ratings yet

- Chapter 8 - 9 - 11Document99 pagesChapter 8 - 9 - 11Koey TseNo ratings yet

- Cost Capital: by Monika VermaDocument27 pagesCost Capital: by Monika VermabadalgujjarNo ratings yet

- Topic 7-ValuationDocument36 pagesTopic 7-ValuationK60 Nguyễn Ngọc Quế AnhNo ratings yet

- Chapter 3 CLC StudentDocument38 pagesChapter 3 CLC StudentLinh HoangNo ratings yet

- Ch4 Bond SDocument139 pagesCh4 Bond SK60 NGUYỄN THỊ HƯƠNG QUỲNHNo ratings yet

- CH 05 - Bonds, Bond Valuation, and Interest RatesDocument42 pagesCH 05 - Bonds, Bond Valuation, and Interest RatesNoor PervezNo ratings yet

- PresTheme2-Eng-Time Value of MoneyDocument39 pagesPresTheme2-Eng-Time Value of MoneyKristina PekovaNo ratings yet

- Interest Rate Risk and Bond PricesDocument61 pagesInterest Rate Risk and Bond PricesMarwa HassanNo ratings yet

- Ch6 MARA 641Document37 pagesCh6 MARA 641MubeenNo ratings yet

- Chapter 6 StudentDocument30 pagesChapter 6 StudentLinh HoangNo ratings yet

- ch08 Fin202Document54 pagesch08 Fin202Nguyễn Thanh Nhàn K16No ratings yet

- Valuation of Bonds and Shares BD CH 8,9Document42 pagesValuation of Bonds and Shares BD CH 8,9Hien ThuNo ratings yet

- Equity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaDocument51 pagesEquity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaSheeza AshrafNo ratings yet

- MIT15 401F08 Review Mid PDFDocument38 pagesMIT15 401F08 Review Mid PDFGasimovskyNo ratings yet

- Chapter 6 StudentDocument30 pagesChapter 6 Studentmin - radiseNo ratings yet

- Valuation of Bonds, Shares and Financial AssetsDocument12 pagesValuation of Bonds, Shares and Financial AssetsHabibullah SarkerNo ratings yet

- CorperateFinance NumericalIteration03Feb2020Document226 pagesCorperateFinance NumericalIteration03Feb2020JoanneNo ratings yet

- CH 04Document12 pagesCH 04Mai NguyễnNo ratings yet

- Jun 2006 - Qns Mod BDocument13 pagesJun 2006 - Qns Mod BHubbak KhanNo ratings yet

- Corporate FinanceDocument87 pagesCorporate FinanceXiao PoNo ratings yet

- Chapter 18 Equity Valuation Models Lecture Notes PDFDocument11 pagesChapter 18 Equity Valuation Models Lecture Notes PDFcourse shtsNo ratings yet

- ValuationDocument23 pagesValuationBisma KhalidNo ratings yet

- Topic 2 - Time Value of MoneyDocument48 pagesTopic 2 - Time Value of MoneyБота ОмароваNo ratings yet

- Valuation of Securities & Weighted Average Cost of CapitalDocument15 pagesValuation of Securities & Weighted Average Cost of CapitalSyed Abid HussainNo ratings yet

- Sample Cover Letter Requesting Full-Time PositionDocument1 pageSample Cover Letter Requesting Full-Time PositionJuan SanguinetiNo ratings yet

- Cover Letter GuideDocument5 pagesCover Letter GuideSyeha Abdal NasherNo ratings yet

- Reporte Escrito PDFDocument3 pagesReporte Escrito PDFJuan SanguinetiNo ratings yet

- Sample Consulting Analyst Cover LetterDocument1 pageSample Consulting Analyst Cover LetterHaoming ChangNo ratings yet

- COVER LETTER TIPSDocument2 pagesCOVER LETTER TIPSNikhil GobhilNo ratings yet

- Cover Letter Guide (Accessible For Website)Document9 pagesCover Letter Guide (Accessible For Website)IngYassineNo ratings yet

- KKJJHHHGGDocument23 pagesKKJJHHHGGJuan SanguinetiNo ratings yet

- Capital Budgeting: Workshop Questions: Finance & Financial ManagementDocument12 pagesCapital Budgeting: Workshop Questions: Finance & Financial ManagementJuan SanguinetiNo ratings yet

- Sample Cover Letters PDFDocument6 pagesSample Cover Letters PDFbala1307No ratings yet

- Capital Budgeting: Suggested Answers To Workshop Questions Finance & Financial ManagementDocument23 pagesCapital Budgeting: Suggested Answers To Workshop Questions Finance & Financial ManagementJuan SanguinetiNo ratings yet

- Finance& Financial Management Risk, Cost of Capital & Capital BudgetingDocument39 pagesFinance& Financial Management Risk, Cost of Capital & Capital BudgetingJuan SanguinetiNo ratings yet

- Finance & Financial Management Equity FinancingDocument25 pagesFinance & Financial Management Equity FinancingJuan SanguinetiNo ratings yet

- KKJJHHHGGDocument47 pagesKKJJHHHGGJuan SanguinetiNo ratings yet

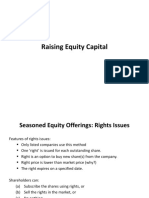

- Raising Equity CapitalDocument9 pagesRaising Equity CapitalJuan SanguinetiNo ratings yet

- Lecture 4 Risk Return PDFDocument33 pagesLecture 4 Risk Return PDFJuan SanguinetiNo ratings yet

- The Time Value of Money: A Pound Today Is More Valuable Than A Pound Tomorrow'Document19 pagesThe Time Value of Money: A Pound Today Is More Valuable Than A Pound Tomorrow'Juan SanguinetiNo ratings yet

- FFM Class Outline 2018 - 2019Document5 pagesFFM Class Outline 2018 - 2019Juan SanguinetiNo ratings yet

- KKJJHHHGGDocument40 pagesKKJJHHHGGJuan SanguinetiNo ratings yet

- Finance & Financial Management Net Present Value & Other Investment RulesDocument43 pagesFinance & Financial Management Net Present Value & Other Investment RulesJuan SanguinetiNo ratings yet

- Strathclyde University Finance & Financial Management Group-Based AssignmentDocument4 pagesStrathclyde University Finance & Financial Management Group-Based AssignmentJuan SanguinetiNo ratings yet

- Lecture 1 Introduction PDFDocument26 pagesLecture 1 Introduction PDFJuan SanguinetiNo ratings yet

- Exam Script 2018 22nd MarchDocument10 pagesExam Script 2018 22nd MarchJuan SanguinetiNo ratings yet

- IB Urban Environments Option G (Latest 2024)Document154 pagesIB Urban Environments Option G (Latest 2024)Pasta SempaNo ratings yet

- Sample BudgetDocument109 pagesSample BudgetAnjannette SantosNo ratings yet

- Chemical EquationsDocument22 pagesChemical EquationsSiti Norasikin MuhyaddinNo ratings yet

- Price List 2014: Valid From 01.04.2014, Prices in Euro, Excluding VAT. Previous Price Lists Will Become InvalidDocument106 pagesPrice List 2014: Valid From 01.04.2014, Prices in Euro, Excluding VAT. Previous Price Lists Will Become InvalidarifNo ratings yet

- NY B17 ATF FDR - 7-24-03 ATF Email and 10-25-01 ATF After Action Report 092Document20 pagesNY B17 ATF FDR - 7-24-03 ATF Email and 10-25-01 ATF After Action Report 0929/11 Document Archive100% (2)

- Government's Role in Public HealthDocument2 pagesGovernment's Role in Public Healthmrskiller patchNo ratings yet

- ChecklistDocument2 pagesChecklistKyra AlesonNo ratings yet

- Etextbook 978 0078025884 Accounting Information Systems 4th EditionDocument61 pagesEtextbook 978 0078025884 Accounting Information Systems 4th Editionmark.dame383100% (48)

- Space Management Guidelines: Brief SummaryDocument17 pagesSpace Management Guidelines: Brief SummaryMOHD JIDINo ratings yet

- Spare Parts Catalog - Scooptram ST1030Document956 pagesSpare Parts Catalog - Scooptram ST1030Elvis RianNo ratings yet

- Numerical Investigation of The Effect of Nappe Non Aeration On Caisson Sliding Force During Tsunami Breakwater Over Topping Using OpenFOAM Akshay PatilDocument73 pagesNumerical Investigation of The Effect of Nappe Non Aeration On Caisson Sliding Force During Tsunami Breakwater Over Topping Using OpenFOAM Akshay PatilSamir BelghoulaNo ratings yet

- Trace Log 20131229152625Document3 pagesTrace Log 20131229152625Razvan PaleaNo ratings yet

- 11 - Surrogate Constraints 1968Document9 pages11 - Surrogate Constraints 1968asistensi pakNo ratings yet

- Amazon removes restricted supplement listing multiple timesDocument12 pagesAmazon removes restricted supplement listing multiple timesMasood Ur RehmanNo ratings yet

- Global Server Load Balancing: Cns 205-5I: Citrix Netscaler 10.5 Essentials and NetworkingDocument37 pagesGlobal Server Load Balancing: Cns 205-5I: Citrix Netscaler 10.5 Essentials and NetworkingsudharaghavanNo ratings yet

- Complete HSE document kit for ISO 14001 & ISO 45001 certificationDocument8 pagesComplete HSE document kit for ISO 14001 & ISO 45001 certificationfaroz khanNo ratings yet

- Crim Cases MidtermsDocument76 pagesCrim Cases MidtermsCoreine Valledor-SarragaNo ratings yet

- Rotating EquipmentDocument3 pagesRotating EquipmentSathish DesignNo ratings yet

- Apollo Experience Report Lunar Module Landing Gear SubsystemDocument60 pagesApollo Experience Report Lunar Module Landing Gear SubsystemBob Andrepont100% (3)

- Younis 2020Document5 pagesYounis 2020nalakathshamil8No ratings yet

- Drive Unit TENH EH 10003, 225, 50/60Hz 400/440V: Qty. Description Specification Material Size DT Doc IdDocument1 pageDrive Unit TENH EH 10003, 225, 50/60Hz 400/440V: Qty. Description Specification Material Size DT Doc IdKarikalan JayNo ratings yet

- Agreement: /ECE/324/Rev.2/Add.127 /ECE/TRANS/505/Rev.2/Add.127Document29 pagesAgreement: /ECE/324/Rev.2/Add.127 /ECE/TRANS/505/Rev.2/Add.127Mina RemonNo ratings yet

- Rapidcure: Corrosion Management Products Rapidcure UwDocument1 pageRapidcure: Corrosion Management Products Rapidcure UwHeramb TrifaleyNo ratings yet

- Anchoring in Bad WeatherDocument2 pagesAnchoring in Bad WeatherDujeKnezevicNo ratings yet

- Tata Consulting Engineers Design Guide For Auxiliary Steam HeaderDocument10 pagesTata Consulting Engineers Design Guide For Auxiliary Steam HeadervijayanmksNo ratings yet

- Certified Elder Law Attorney Middletown NyDocument8 pagesCertified Elder Law Attorney Middletown NymidhudsonlawNo ratings yet

- CIO Executive SummaryDocument8 pagesCIO Executive SummaryResumeBearNo ratings yet

- ED621826Document56 pagesED621826A. MagnoNo ratings yet

- HACCP Plan With Flow Chart-1Document23 pagesHACCP Plan With Flow Chart-1Anonymous aZA07k8TXfNo ratings yet

- Impact On Cocoon Quality Improvement.1Document10 pagesImpact On Cocoon Quality Improvement.1Naveen NtrNo ratings yet