You might also like

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- Paystub 3Document1 pagePaystub 3J RequenaNo ratings yet

- Sap Fi Step by Step Configuration GuideDocument77 pagesSap Fi Step by Step Configuration GuideShine Kaippilly100% (1)

- Tax Invoice For: Your Telstra BillDocument8 pagesTax Invoice For: Your Telstra BillmaryannemooreNo ratings yet

- BIR Ruling No. 206-90Document2 pagesBIR Ruling No. 206-90Raiya Angela100% (2)

- Tax Declaration Form 2021 22Document4 pagesTax Declaration Form 2021 22Kasiviswanathan ChinnathambiNo ratings yet

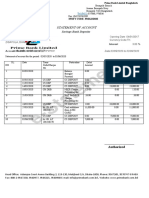

- Prime Bank LTDDocument1 pagePrime Bank LTDfgfdghfNo ratings yet

- HRA - House Rent Allowance - Exemption Rules & Tax DeductionsDocument4 pagesHRA - House Rent Allowance - Exemption Rules & Tax DeductionsKrishna SwainNo ratings yet

- Income Tax Ready Reckoner 2011-12Document28 pagesIncome Tax Ready Reckoner 2011-12kpksscribdNo ratings yet

- 5.1.5 Income Tax DeductionDocument7 pages5.1.5 Income Tax DeductionCommon ManNo ratings yet

- Investment Proof Submission Guidelines, FY 203-24Document16 pagesInvestment Proof Submission Guidelines, FY 203-24asanimamathaNo ratings yet

- Unit III - The Payment of Bonus Act, 1965 - Labour LawsDocument13 pagesUnit III - The Payment of Bonus Act, 1965 - Labour Lawspatelia kevalNo ratings yet

- Taxation Theory QuestionsDocument7 pagesTaxation Theory QuestionsPrince kumarNo ratings yet

- Assignment of Economic and Business Legislature: Submitted To-Submitted byDocument7 pagesAssignment of Economic and Business Legislature: Submitted To-Submitted byMohit SahniNo ratings yet

- Handbook To Investment DeclarationDocument17 pagesHandbook To Investment DeclarationMourya ChigurupatiNo ratings yet

- Deductions On Section 80CDocument12 pagesDeductions On Section 80CViraja GuruNo ratings yet

- Investment Types and Guidlines FY 2022 23Document39 pagesInvestment Types and Guidlines FY 2022 23Jyoshna NookalaNo ratings yet

- Declaration Form 12BB 2022 23Document4 pagesDeclaration Form 12BB 2022 23S S PradheepanNo ratings yet

- Individual-Txation-FY-2018-19-with - JJDocument64 pagesIndividual-Txation-FY-2018-19-with - JJCOMPLETE ACADEMYNo ratings yet

- Othguide For Act Invt Proof Submission - FY 2021-22 - Guide For Act Invt Proof Submission - FY 2021-22Document19 pagesOthguide For Act Invt Proof Submission - FY 2021-22 - Guide For Act Invt Proof Submission - FY 2021-22Dhruv JainNo ratings yet

- ItfjfygjDocument3 pagesItfjfygjKrishna GNo ratings yet

- Net Income How To Calculate Net Income in Income TaxDocument34 pagesNet Income How To Calculate Net Income in Income TaxSeetha SenthilNo ratings yet

- Law of TaxationDocument13 pagesLaw of TaxationRameshNadarNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Chapter 12 TaxdeductionsDocument16 pagesChapter 12 TaxdeductionsRiya SharmaNo ratings yet

- Basic Concepts of TaxationDocument5 pagesBasic Concepts of TaxationMaya SharmaNo ratings yet

- 7th Term - Legal Frameworks of ConstructionDocument79 pages7th Term - Legal Frameworks of ConstructionShreedharNo ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- 4 Chapter VI-ADocument11 pages4 Chapter VI-AVENKATESWARLUMCOMNo ratings yet

- IT Assignment 2Document7 pagesIT Assignment 2Srinivasulu Reddy PNo ratings yet

- TDSDocument2 pagesTDSNarayan NarayanNo ratings yet

- PO SavingsDocument8 pagesPO Savingsamrish_ydsNo ratings yet

- Tax Rebate Claim Form-2019Document2 pagesTax Rebate Claim Form-2019Muhammad Hanif SuchwaniNo ratings yet

- DeductionsDocument7 pagesDeductionsAnurag BishtNo ratings yet

- Notes To Investment Proof SubmissionDocument10 pagesNotes To Investment Proof Submissiongopikiran6No ratings yet

- Tax Saving InstrumentsDocument19 pagesTax Saving Instrumentsharry.anjh3613No ratings yet

- Notes To Investment Proof SubmissionDocument10 pagesNotes To Investment Proof SubmissionVinayak DhotreNo ratings yet

- Income Tax Section 80Document19 pagesIncome Tax Section 80DEV HUGENNo ratings yet

- Assignment On Income From House PropertyDocument17 pagesAssignment On Income From House PropertySandeep ChawdaNo ratings yet

- Salaries PresentationDocument21 pagesSalaries PresentationDipika PandaNo ratings yet

- Dena Niwas Housing Loan: (To Be Reset at The End of Every 3 Years)Document24 pagesDena Niwas Housing Loan: (To Be Reset at The End of Every 3 Years)asdNo ratings yet

- Avoidance & EvasionDocument34 pagesAvoidance & EvasionHarshita RanjanNo ratings yet

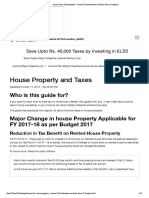

- Income From House Property - Income Tax Deductions On Home Loans & PropertyDocument13 pagesIncome From House Property - Income Tax Deductions On Home Loans & Propertyrajesh_bNo ratings yet

- Question and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofDocument6 pagesQuestion and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofAnamika VatsaNo ratings yet

- Tax Planning For Salaried Employees - Taxguru - inDocument5 pagesTax Planning For Salaried Employees - Taxguru - invthreefriendsNo ratings yet

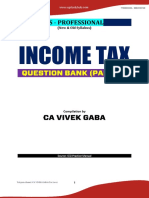

- Cs Professional Income Tax Question Bank Part - 1 For Dec 21 & June 22Document64 pagesCs Professional Income Tax Question Bank Part - 1 For Dec 21 & June 22pande anujNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- Up To Rs. 2,50,000: Taxable Income Tax RateDocument13 pagesUp To Rs. 2,50,000: Taxable Income Tax RateRashi ViRdiNo ratings yet

- Investment Declaration ManualDocument10 pagesInvestment Declaration ManualAbhinav VivekNo ratings yet

- Principles of Taxation M. Khalid Petiwala: Income From PropertyDocument8 pagesPrinciples of Taxation M. Khalid Petiwala: Income From PropertyosamaNo ratings yet

- Handbook - Tax Planning Level 1Document22 pagesHandbook - Tax Planning Level 1Prem SagarNo ratings yet

- Handbook - Tax Planning Level 2Document30 pagesHandbook - Tax Planning Level 2Malli Arjun staff guitar zgkNo ratings yet

- Sri Lanka PAYE Income Tax TablesDocument14 pagesSri Lanka PAYE Income Tax Tableskahatadeniya0% (1)

- Income Tax RulesDocument4 pagesIncome Tax RulesvenkatanagachandraNo ratings yet

- Unit 4 Return FillingDocument71 pagesUnit 4 Return FillingAnshu kumarNo ratings yet

- Income Tax India Basic DetailsDocument28 pagesIncome Tax India Basic DetailsrupaparaNo ratings yet

- Investment PlanDocument1 pageInvestment PlanNitin AgarwalNo ratings yet

- Income Tax Calculations On Salaries and Other Income For The Assessment Year 2024Document20 pagesIncome Tax Calculations On Salaries and Other Income For The Assessment Year 2024ManoharanR Rajamanikam0% (1)

- TAX ON INTEREST INCOME: Interest On Saving Bank Account: Tax, 80TTA, ITRDocument4 pagesTAX ON INTEREST INCOME: Interest On Saving Bank Account: Tax, 80TTA, ITRcmlcbhtidNo ratings yet

- 14 Tax-Saving Investment Options Beyond Section 80C LimitDocument12 pages14 Tax-Saving Investment Options Beyond Section 80C Limitsintus2u83No ratings yet

- CONT .: (15 Minutes Extra Time Will Be Given Due To Slow Internet or Electricity Issues)Document4 pagesCONT .: (15 Minutes Extra Time Will Be Given Due To Slow Internet or Electricity Issues)ALEEM MANSOORNo ratings yet

- Investment Declaration Form For The Financial Year 2014 - 15Document7 pagesInvestment Declaration Form For The Financial Year 2014 - 15devanyaNo ratings yet

- Jigar Bonus ActDocument2 pagesJigar Bonus ActJigar PatelNo ratings yet

- Assignment Budget and Accounting Entries Questions PDFDocument4 pagesAssignment Budget and Accounting Entries Questions PDFNah HamzaNo ratings yet

- Salary Statement: Employee No. Exchange RateDocument1 pageSalary Statement: Employee No. Exchange RateSapana MallaNo ratings yet

- Invoice: Atria Convergence Technologies Limited, Due Date: 10/0 5/2021Document3 pagesInvoice: Atria Convergence Technologies Limited, Due Date: 10/0 5/2021Kirti Kumar YeldiNo ratings yet

- National Teachers College: Student Registration FormDocument1 pageNational Teachers College: Student Registration FormVal RenonNo ratings yet

- Mitsubishi FiltersDocument1 pageMitsubishi Filterscodin82147No ratings yet

- Ug Special TermDocument40 pagesUg Special TermRegina SamsonNo ratings yet

- O: +1 410-737-8677 F: +1 410-737-8688 3610 Commerce Drive - Suite 817 Baltimore, MD 21227 USADocument14 pagesO: +1 410-737-8677 F: +1 410-737-8688 3610 Commerce Drive - Suite 817 Baltimore, MD 21227 USASiddiq KhanNo ratings yet

- Computing Pay For Work Done On: Below Are The Steps On Computing Employee's SalaryDocument20 pagesComputing Pay For Work Done On: Below Are The Steps On Computing Employee's Salaryburn lastNo ratings yet

- NK Gok Otc ReceiptjDocument16 pagesNK Gok Otc ReceiptjThyagamurthy MVNo ratings yet

- Chapter - 1 Computation of Tax LiabilityDocument6 pagesChapter - 1 Computation of Tax LiabilityNitin RajNo ratings yet

- VAT - Module 1 - General Principles To Zero-RatedDocument57 pagesVAT - Module 1 - General Principles To Zero-RatedReyan RohNo ratings yet

- Sales Invoice: MD Mehedi HasanDocument1 pageSales Invoice: MD Mehedi HasanDerrick MoeelleNo ratings yet

- Credit Card Reconciliation - Brianna Daguio 1Document9 pagesCredit Card Reconciliation - Brianna Daguio 1api-507868036No ratings yet

- Bangalore UniversityDocument2 pagesBangalore UniversityAtul KashyapNo ratings yet

- Presentation On Clubbing of Income Under Income TaxDocument11 pagesPresentation On Clubbing of Income Under Income TaxCA Arpit Gupta100% (2)

- 27 - Hotel Specialist Tagaytay Inc. v..20210505-11-1fg6pgfDocument23 pages27 - Hotel Specialist Tagaytay Inc. v..20210505-11-1fg6pgfPio Vincent BuencaminoNo ratings yet

- A. P. (DIR Series) Circular No.109 Dated June 11, 2013 A.P. (DIR Series) Circular No.17 Dated November 16, 2010Document5 pagesA. P. (DIR Series) Circular No.109 Dated June 11, 2013 A.P. (DIR Series) Circular No.17 Dated November 16, 2010vikalp123123No ratings yet

- Treasury Rules Vol-II PDFDocument300 pagesTreasury Rules Vol-II PDFAneela TabassumNo ratings yet

- Statement June and JulyDocument2 pagesStatement June and JulyGregory Scarpa SnrNo ratings yet

- "Statement of Management'S Responsibilty For Annual Income Tax Return'Document2 pages"Statement of Management'S Responsibilty For Annual Income Tax Return'mikel bautistaNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSunil KumarNo ratings yet

- New Microsoft Word DocumentDocument5 pagesNew Microsoft Word DocumentAdil HassanNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Rintu DasNo ratings yet

- 49-Filipinas Life Assurance v. CIR G.R. No. L-21258 October 31, 1967Document13 pages49-Filipinas Life Assurance v. CIR G.R. No. L-21258 October 31, 1967Jopan SJNo ratings yet