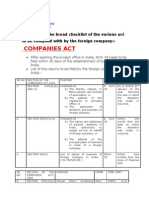

Rules of Merger - Demeerger

Rules of Merger - Demeerger

You might also like

- Stock Audit ReportDocument8 pagesStock Audit ReportkeeranNo ratings yet

- Form 10FDocument2 pagesForm 10FRajeev AttriNo ratings yet

- SMEDA Partnership DeedDocument6 pagesSMEDA Partnership DeedArshed MehmoodNo ratings yet

- Form CHG-1-16032017 Signe Cfil CDocument6 pagesForm CHG-1-16032017 Signe Cfil CsunjuNo ratings yet

- WPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveDocument29 pagesWPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveFahim Khan0% (1)

- Checklist-Companies Act 1956Document34 pagesChecklist-Companies Act 1956Divya PoojariNo ratings yet

- Law 50 Imp. QuestionsDocument51 pagesLaw 50 Imp. QuestionsMayakuntla NeeladriNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document3 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- Deductions From Gross Total IncomeDocument91 pagesDeductions From Gross Total Incomeheena4647No ratings yet

- Section 195 and Form 15CBDocument53 pagesSection 195 and Form 15CBVALTIM09No ratings yet

- Supplemental Agreement On Admission Cum Retirement ofDocument3 pagesSupplemental Agreement On Admission Cum Retirement ofGITIKA ARORANo ratings yet

- Sbec Summary NotesDocument107 pagesSbec Summary NotesShobhit ShuklaNo ratings yet

- Stock StatementDocument5 pagesStock StatementPraveen S. VastradNo ratings yet

- E Nomination PDFDocument2 pagesE Nomination PDFSagar RajputNo ratings yet

- Abstract Under Karnataka Shops and Commercial Establishment Rules, 1963Document2 pagesAbstract Under Karnataka Shops and Commercial Establishment Rules, 1963AsokNo ratings yet

- Format of Audit Report of A Private Limited Company With CARO & IFC - Taxguru - inDocument11 pagesFormat of Audit Report of A Private Limited Company With CARO & IFC - Taxguru - inSwetha SNo ratings yet

- Presentation On Corporate Level StragegiesDocument12 pagesPresentation On Corporate Level StragegiesVaibhav SinghNo ratings yet

- By-Law No. 1Document9 pagesBy-Law No. 1sspecoreNo ratings yet

- Research of Epfo ApprovalDocument1 pageResearch of Epfo ApprovalKbg GangadharNo ratings yet

- CS Executive Tax Laws Suggested Answers-1Document21 pagesCS Executive Tax Laws Suggested Answers-1nehaNo ratings yet

- Maharajkumar Gopal Saran Narain Singh v. CITDocument3 pagesMaharajkumar Gopal Saran Narain Singh v. CITRonit KumarNo ratings yet

- CHECKLIST FOR CONVERSION OF Partnership Firm IN PRIVATE LIMITED CoDocument4 pagesCHECKLIST FOR CONVERSION OF Partnership Firm IN PRIVATE LIMITED CoRavindra PoojaryNo ratings yet

- Form No. SH-3 Register of Sweat Equity SharesDocument1 pageForm No. SH-3 Register of Sweat Equity SharesGaurav Kumar SharmaNo ratings yet

- Mandatory Compliance Checklist For Private Limited CompanyDocument6 pagesMandatory Compliance Checklist For Private Limited CompanyParas03No ratings yet

- FIN - 005 Fixed Assets PolicyDocument20 pagesFIN - 005 Fixed Assets PolicykhanjaaliNo ratings yet

- Format Due DiligenceDocument48 pagesFormat Due DiligenceUmeshNo ratings yet

- Partnership Authority Letter For DSA AgreementDocument3 pagesPartnership Authority Letter For DSA AgreementTeam BLLNo ratings yet

- Factories Act 1948 Annual Leave With Wages SpecialDocument15 pagesFactories Act 1948 Annual Leave With Wages SpecialNishant RanjanNo ratings yet

- Final RFP UpssclDocument58 pagesFinal RFP Upssclbikashsingh01No ratings yet

- Shalimar Research15July2013Document34 pagesShalimar Research15July2013equityanalystinvestor100% (1)

- Covering Letter For CLRA - HYR ReturnDocument1 pageCovering Letter For CLRA - HYR ReturnShiva kantNo ratings yet

- Form No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarDocument9 pagesForm No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarHardik KalariaNo ratings yet

- Regulation of The Share Transfer AgentDocument15 pagesRegulation of The Share Transfer AgentAmrutha GayathriNo ratings yet

- Coppergate Educare Costing Theory NotesDocument106 pagesCoppergate Educare Costing Theory Notespratikjai100% (1)

- Lodr PPT - TtaDocument9 pagesLodr PPT - Ttatarun motianiNo ratings yet

- Statutory Checklist-Tds OthersDocument15 pagesStatutory Checklist-Tds OthersGaurav KumarNo ratings yet

- Tax Implications of Amalgamations / Mergers / Demergers / Slump SalesDocument54 pagesTax Implications of Amalgamations / Mergers / Demergers / Slump Salesvvikram756667% (3)

- E-Nomination Facility by Epfo On Unified Member PortalDocument10 pagesE-Nomination Facility by Epfo On Unified Member PortalUpasana Talapady100% (2)

- Dsa Invoice - Points To Remember: Don'tsDocument3 pagesDsa Invoice - Points To Remember: Don'tsMadhan Kumar BobbalaNo ratings yet

- This Draft of Deed of Partnership': Lawyer atDocument4 pagesThis Draft of Deed of Partnership': Lawyer atTANUNo ratings yet

- Agenda For First Board Meeting Before AGM of Private Limited CompaniesDocument15 pagesAgenda For First Board Meeting Before AGM of Private Limited Companieshetalsangoi0% (1)

- 51 Checklist Buy BackDocument3 pages51 Checklist Buy BackvrkesavanNo ratings yet

- Director's RemunerationDocument3 pagesDirector's Remunerationzxchua3No ratings yet

- Corporate Disclosure and Investor ProtectionDocument26 pagesCorporate Disclosure and Investor ProtectionMatharu Knowlittle100% (1)

- Regulation by SEBI, Takeover CodeDocument28 pagesRegulation by SEBI, Takeover CodemonuNo ratings yet

- Esic Form 37Document1 pageEsic Form 37Umesh C0% (2)

- Form No 3CDDocument8 pagesForm No 3CDSURANA1973No ratings yet

- The The The The The: Published by AuthorityDocument92 pagesThe The The The The: Published by Authorityrahulchow2No ratings yet

- CA Final Audit Sample MCQs by ICAIDocument53 pagesCA Final Audit Sample MCQs by ICAIAditya HalderNo ratings yet

- Foreign Company To Run Business in IndiaDocument3 pagesForeign Company To Run Business in Indiagaurav singhNo ratings yet

- SURVEYOR PPT FOR REGISTRATIONDocument32 pagesSURVEYOR PPT FOR REGISTRATIONNIKHIL KASAT100% (1)

- Partnership Act, 2020 (1964) : AmendmentsDocument22 pagesPartnership Act, 2020 (1964) : Amendmentsvivek yadav100% (1)

- Company LawDocument76 pagesCompany LawtoabhishekpalNo ratings yet

- Presentation On Compromise ArrangementDocument75 pagesPresentation On Compromise ArrangementPalakVermaNo ratings yet

- Companies Applicability Chart by Darshan KhareDocument6 pagesCompanies Applicability Chart by Darshan KharePavan KumarNo ratings yet

- CA Inter (QB) - Chapter 4Document123 pagesCA Inter (QB) - Chapter 4Siddhi ShahNo ratings yet

- Tax Audit ReportDocument28 pagesTax Audit Reportsmith sethisNo ratings yet

- Company Act, 2013Document22 pagesCompany Act, 2013CHARAK RAYNo ratings yet

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorFrom EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo ratings yet

- Actions Required Under CA 2013Document5 pagesActions Required Under CA 2013ranjusanjuNo ratings yet

- PRTC - RFBT First PreboardDocument15 pagesPRTC - RFBT First PreboardMae Anne De VeraNo ratings yet

- Business Organisations and AgencyDocument250 pagesBusiness Organisations and Agencyalexops5No ratings yet

- Law On ParcorDocument5 pagesLaw On ParcorPhebegail ImmotnaNo ratings yet

- Yujuico v. QuiambaoDocument25 pagesYujuico v. QuiambaoAlthea Angela GarciaNo ratings yet

- Mara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Document6 pagesMara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Serenity CarlyeNo ratings yet

- AFAR FinalMockBoard BDocument11 pagesAFAR FinalMockBoard BCattleyaNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document24 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija Talipan100% (1)

- Final AgreementDocument2 pagesFinal Agreementnicole quistoyNo ratings yet

- Analysis of FinancialDocument207 pagesAnalysis of FinancialShane Aileen AngelesNo ratings yet

- Relation of Partner To Third PartiesDocument7 pagesRelation of Partner To Third PartiesMuhammad ShehzadNo ratings yet

- D' Amore FruitiesDocument65 pagesD' Amore FruitiesJannah DatualiNo ratings yet

- SM Chap 9Document41 pagesSM Chap 9Debora BongNo ratings yet

- Partnership Formula Definition and ExamplesDocument6 pagesPartnership Formula Definition and ExamplesBhjjkkNo ratings yet

- Digest - Wolfgang Aurbach Vs Sanitary WaresDocument1 pageDigest - Wolfgang Aurbach Vs Sanitary WaresremraseNo ratings yet

- De Operating AgreementDocument59 pagesDe Operating AgreementAyan RoyNo ratings yet

- Partnership Unit2Document28 pagesPartnership Unit2Sergio RamosNo ratings yet

- (Reviewer) Law On Agency (UP 2014 Ed.)Document20 pages(Reviewer) Law On Agency (UP 2014 Ed.)Carl Joshua Dayrit100% (2)

- Transport AgreementDocument2 pagesTransport Agreementreimart sarmientoNo ratings yet

- Scal Membership Application FormDocument4 pagesScal Membership Application Formsuresh6265No ratings yet

- Feasibility in Ergonomics AutosavedDocument63 pagesFeasibility in Ergonomics AutosavedMichael AsinguaNo ratings yet

- JKL Q1Document3 pagesJKL Q1praveenNo ratings yet

- Classification of PropertyDocument15 pagesClassification of PropertyAYUSHI TYAGINo ratings yet

- TaxationDocument33 pagesTaxationlordaiztrand100% (1)

- Dissolution and Winding UpDocument8 pagesDissolution and Winding UpregenNo ratings yet

- Commercial Law ReviewerDocument33 pagesCommercial Law ReviewerFrancis PunoNo ratings yet

- Oil Rigs SAS Department: Contract For Works & Services at Oil Rig SitesDocument36 pagesOil Rigs SAS Department: Contract For Works & Services at Oil Rig SitesChinmaya SreekaranNo ratings yet

- LLPCollegeDocument25 pagesLLPCollegeKeshavNo ratings yet

- Construction Management Anna University NotesDocument131 pagesConstruction Management Anna University NotesOnline AdoroNo ratings yet

- Dissolution and Winding Up of Partnership Under The Partnership ActDocument9 pagesDissolution and Winding Up of Partnership Under The Partnership ActAnkita BalNo ratings yet

You might also like

- Stock Audit ReportDocument8 pagesStock Audit ReportkeeranNo ratings yet

- Form 10FDocument2 pagesForm 10FRajeev AttriNo ratings yet

- SMEDA Partnership DeedDocument6 pagesSMEDA Partnership DeedArshed MehmoodNo ratings yet

- Form CHG-1-16032017 Signe Cfil CDocument6 pagesForm CHG-1-16032017 Signe Cfil CsunjuNo ratings yet

- WPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveDocument29 pagesWPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveFahim Khan0% (1)

- Checklist-Companies Act 1956Document34 pagesChecklist-Companies Act 1956Divya PoojariNo ratings yet

- Law 50 Imp. QuestionsDocument51 pagesLaw 50 Imp. QuestionsMayakuntla NeeladriNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document3 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- Deductions From Gross Total IncomeDocument91 pagesDeductions From Gross Total Incomeheena4647No ratings yet

- Section 195 and Form 15CBDocument53 pagesSection 195 and Form 15CBVALTIM09No ratings yet

- Supplemental Agreement On Admission Cum Retirement ofDocument3 pagesSupplemental Agreement On Admission Cum Retirement ofGITIKA ARORANo ratings yet

- Sbec Summary NotesDocument107 pagesSbec Summary NotesShobhit ShuklaNo ratings yet

- Stock StatementDocument5 pagesStock StatementPraveen S. VastradNo ratings yet

- E Nomination PDFDocument2 pagesE Nomination PDFSagar RajputNo ratings yet

- Abstract Under Karnataka Shops and Commercial Establishment Rules, 1963Document2 pagesAbstract Under Karnataka Shops and Commercial Establishment Rules, 1963AsokNo ratings yet

- Format of Audit Report of A Private Limited Company With CARO & IFC - Taxguru - inDocument11 pagesFormat of Audit Report of A Private Limited Company With CARO & IFC - Taxguru - inSwetha SNo ratings yet

- Presentation On Corporate Level StragegiesDocument12 pagesPresentation On Corporate Level StragegiesVaibhav SinghNo ratings yet

- By-Law No. 1Document9 pagesBy-Law No. 1sspecoreNo ratings yet

- Research of Epfo ApprovalDocument1 pageResearch of Epfo ApprovalKbg GangadharNo ratings yet

- CS Executive Tax Laws Suggested Answers-1Document21 pagesCS Executive Tax Laws Suggested Answers-1nehaNo ratings yet

- Maharajkumar Gopal Saran Narain Singh v. CITDocument3 pagesMaharajkumar Gopal Saran Narain Singh v. CITRonit KumarNo ratings yet

- CHECKLIST FOR CONVERSION OF Partnership Firm IN PRIVATE LIMITED CoDocument4 pagesCHECKLIST FOR CONVERSION OF Partnership Firm IN PRIVATE LIMITED CoRavindra PoojaryNo ratings yet

- Form No. SH-3 Register of Sweat Equity SharesDocument1 pageForm No. SH-3 Register of Sweat Equity SharesGaurav Kumar SharmaNo ratings yet

- Mandatory Compliance Checklist For Private Limited CompanyDocument6 pagesMandatory Compliance Checklist For Private Limited CompanyParas03No ratings yet

- FIN - 005 Fixed Assets PolicyDocument20 pagesFIN - 005 Fixed Assets PolicykhanjaaliNo ratings yet

- Format Due DiligenceDocument48 pagesFormat Due DiligenceUmeshNo ratings yet

- Partnership Authority Letter For DSA AgreementDocument3 pagesPartnership Authority Letter For DSA AgreementTeam BLLNo ratings yet

- Factories Act 1948 Annual Leave With Wages SpecialDocument15 pagesFactories Act 1948 Annual Leave With Wages SpecialNishant RanjanNo ratings yet

- Final RFP UpssclDocument58 pagesFinal RFP Upssclbikashsingh01No ratings yet

- Shalimar Research15July2013Document34 pagesShalimar Research15July2013equityanalystinvestor100% (1)

- Covering Letter For CLRA - HYR ReturnDocument1 pageCovering Letter For CLRA - HYR ReturnShiva kantNo ratings yet

- Form No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarDocument9 pagesForm No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarHardik KalariaNo ratings yet

- Regulation of The Share Transfer AgentDocument15 pagesRegulation of The Share Transfer AgentAmrutha GayathriNo ratings yet

- Coppergate Educare Costing Theory NotesDocument106 pagesCoppergate Educare Costing Theory Notespratikjai100% (1)

- Lodr PPT - TtaDocument9 pagesLodr PPT - Ttatarun motianiNo ratings yet

- Statutory Checklist-Tds OthersDocument15 pagesStatutory Checklist-Tds OthersGaurav KumarNo ratings yet

- Tax Implications of Amalgamations / Mergers / Demergers / Slump SalesDocument54 pagesTax Implications of Amalgamations / Mergers / Demergers / Slump Salesvvikram756667% (3)

- E-Nomination Facility by Epfo On Unified Member PortalDocument10 pagesE-Nomination Facility by Epfo On Unified Member PortalUpasana Talapady100% (2)

- Dsa Invoice - Points To Remember: Don'tsDocument3 pagesDsa Invoice - Points To Remember: Don'tsMadhan Kumar BobbalaNo ratings yet

- This Draft of Deed of Partnership': Lawyer atDocument4 pagesThis Draft of Deed of Partnership': Lawyer atTANUNo ratings yet

- Agenda For First Board Meeting Before AGM of Private Limited CompaniesDocument15 pagesAgenda For First Board Meeting Before AGM of Private Limited Companieshetalsangoi0% (1)

- 51 Checklist Buy BackDocument3 pages51 Checklist Buy BackvrkesavanNo ratings yet

- Director's RemunerationDocument3 pagesDirector's Remunerationzxchua3No ratings yet

- Corporate Disclosure and Investor ProtectionDocument26 pagesCorporate Disclosure and Investor ProtectionMatharu Knowlittle100% (1)

- Regulation by SEBI, Takeover CodeDocument28 pagesRegulation by SEBI, Takeover CodemonuNo ratings yet

- Esic Form 37Document1 pageEsic Form 37Umesh C0% (2)

- Form No 3CDDocument8 pagesForm No 3CDSURANA1973No ratings yet

- The The The The The: Published by AuthorityDocument92 pagesThe The The The The: Published by Authorityrahulchow2No ratings yet

- CA Final Audit Sample MCQs by ICAIDocument53 pagesCA Final Audit Sample MCQs by ICAIAditya HalderNo ratings yet

- Foreign Company To Run Business in IndiaDocument3 pagesForeign Company To Run Business in Indiagaurav singhNo ratings yet

- SURVEYOR PPT FOR REGISTRATIONDocument32 pagesSURVEYOR PPT FOR REGISTRATIONNIKHIL KASAT100% (1)

- Partnership Act, 2020 (1964) : AmendmentsDocument22 pagesPartnership Act, 2020 (1964) : Amendmentsvivek yadav100% (1)

- Company LawDocument76 pagesCompany LawtoabhishekpalNo ratings yet

- Presentation On Compromise ArrangementDocument75 pagesPresentation On Compromise ArrangementPalakVermaNo ratings yet

- Companies Applicability Chart by Darshan KhareDocument6 pagesCompanies Applicability Chart by Darshan KharePavan KumarNo ratings yet

- CA Inter (QB) - Chapter 4Document123 pagesCA Inter (QB) - Chapter 4Siddhi ShahNo ratings yet

- Tax Audit ReportDocument28 pagesTax Audit Reportsmith sethisNo ratings yet

- Company Act, 2013Document22 pagesCompany Act, 2013CHARAK RAYNo ratings yet

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorFrom EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo ratings yet

- Actions Required Under CA 2013Document5 pagesActions Required Under CA 2013ranjusanjuNo ratings yet

- PRTC - RFBT First PreboardDocument15 pagesPRTC - RFBT First PreboardMae Anne De VeraNo ratings yet

- Business Organisations and AgencyDocument250 pagesBusiness Organisations and Agencyalexops5No ratings yet

- Law On ParcorDocument5 pagesLaw On ParcorPhebegail ImmotnaNo ratings yet

- Yujuico v. QuiambaoDocument25 pagesYujuico v. QuiambaoAlthea Angela GarciaNo ratings yet

- Mara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Document6 pagesMara, Teri, and Rita Partnership Statement of Partnership Liquidation December 31, 2018Serenity CarlyeNo ratings yet

- AFAR FinalMockBoard BDocument11 pagesAFAR FinalMockBoard BCattleyaNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document24 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija Talipan100% (1)

- Final AgreementDocument2 pagesFinal Agreementnicole quistoyNo ratings yet

- Analysis of FinancialDocument207 pagesAnalysis of FinancialShane Aileen AngelesNo ratings yet

- Relation of Partner To Third PartiesDocument7 pagesRelation of Partner To Third PartiesMuhammad ShehzadNo ratings yet

- D' Amore FruitiesDocument65 pagesD' Amore FruitiesJannah DatualiNo ratings yet

- SM Chap 9Document41 pagesSM Chap 9Debora BongNo ratings yet

- Partnership Formula Definition and ExamplesDocument6 pagesPartnership Formula Definition and ExamplesBhjjkkNo ratings yet

- Digest - Wolfgang Aurbach Vs Sanitary WaresDocument1 pageDigest - Wolfgang Aurbach Vs Sanitary WaresremraseNo ratings yet

- De Operating AgreementDocument59 pagesDe Operating AgreementAyan RoyNo ratings yet

- Partnership Unit2Document28 pagesPartnership Unit2Sergio RamosNo ratings yet

- (Reviewer) Law On Agency (UP 2014 Ed.)Document20 pages(Reviewer) Law On Agency (UP 2014 Ed.)Carl Joshua Dayrit100% (2)

- Transport AgreementDocument2 pagesTransport Agreementreimart sarmientoNo ratings yet

- Scal Membership Application FormDocument4 pagesScal Membership Application Formsuresh6265No ratings yet

- Feasibility in Ergonomics AutosavedDocument63 pagesFeasibility in Ergonomics AutosavedMichael AsinguaNo ratings yet

- JKL Q1Document3 pagesJKL Q1praveenNo ratings yet

- Classification of PropertyDocument15 pagesClassification of PropertyAYUSHI TYAGINo ratings yet

- TaxationDocument33 pagesTaxationlordaiztrand100% (1)

- Dissolution and Winding UpDocument8 pagesDissolution and Winding UpregenNo ratings yet

- Commercial Law ReviewerDocument33 pagesCommercial Law ReviewerFrancis PunoNo ratings yet

- Oil Rigs SAS Department: Contract For Works & Services at Oil Rig SitesDocument36 pagesOil Rigs SAS Department: Contract For Works & Services at Oil Rig SitesChinmaya SreekaranNo ratings yet

- LLPCollegeDocument25 pagesLLPCollegeKeshavNo ratings yet

- Construction Management Anna University NotesDocument131 pagesConstruction Management Anna University NotesOnline AdoroNo ratings yet

- Dissolution and Winding Up of Partnership Under The Partnership ActDocument9 pagesDissolution and Winding Up of Partnership Under The Partnership ActAnkita BalNo ratings yet