You might also like

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Economic Indicators for Southeastern Asia and the Pacific: Input–Output TablesFrom EverandEconomic Indicators for Southeastern Asia and the Pacific: Input–Output TablesNo ratings yet

- Indian Auto Component Industry Performance Review: 2017-18 Growth and ExportsDocument16 pagesIndian Auto Component Industry Performance Review: 2017-18 Growth and Exportsknlpriya05No ratings yet

- Sub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Document39 pagesSub: Investor Presentation On Financial Results For The Quarter and Nine Months Ended 31 December, 2021Dasari PrabodhNo ratings yet

- Jamna Auto Jamna Auto: India I EquitiesDocument16 pagesJamna Auto Jamna Auto: India I Equitiesrishab agarwalNo ratings yet

- Persistent Systems Buy Case Target Price Rs.1025 19.2% UpsideDocument3 pagesPersistent Systems Buy Case Target Price Rs.1025 19.2% UpsideKishor KrNo ratings yet

- 2020 08 06 PH e Mpi PDFDocument8 pages2020 08 06 PH e Mpi PDFJNo ratings yet

- THGL - Proposal - Summary - 16thaug19 - SlidesDocument10 pagesTHGL - Proposal - Summary - 16thaug19 - Slidessaheb167No ratings yet

- Astral delivers 73% revenue growth, 332% PBT growth in Q1Document5 pagesAstral delivers 73% revenue growth, 332% PBT growth in Q1Namrata ShahNo ratings yet

- Boeing Current Market Outlook 2013Document37 pagesBoeing Current Market Outlook 2013VaibhavNo ratings yet

- Zomato's Ride to IPO - Industry Overview, Key Metrics, Valuations and all you need to knowDocument8 pagesZomato's Ride to IPO - Industry Overview, Key Metrics, Valuations and all you need to knowHarish RedquestNo ratings yet

- Hero Motocorp DCF ValuationDocument66 pagesHero Motocorp DCF ValuationPrabhdeep DadyalNo ratings yet

- Arvind Ltd Stock Analysis and ForecastDocument3 pagesArvind Ltd Stock Analysis and ForecastKishor KrNo ratings yet

- Analyst Presentation and Factsheet Q1fy21Document25 pagesAnalyst Presentation and Factsheet Q1fy21Va AniNo ratings yet

- IT Services - Analyst Presentation - Sep15Document15 pagesIT Services - Analyst Presentation - Sep15Nimish NamaNo ratings yet

- Early Stage Investment Report 2019Document9 pagesEarly Stage Investment Report 2019kurt kNo ratings yet

- Maruti Suzuki India LTDDocument40 pagesMaruti Suzuki India LTDnishantNo ratings yet

- Indian Retail Lube MarketDocument12 pagesIndian Retail Lube MarketsudhanshuNo ratings yet

- Tata Motors Q2 FY10 Results Show Recovery Across Automotive SectorsDocument17 pagesTata Motors Q2 FY10 Results Show Recovery Across Automotive Sectorsrayhan7No ratings yet

- KPJ Healthcare Neutral: MalaysiaDocument5 pagesKPJ Healthcare Neutral: MalaysiaArdoni SaharilNo ratings yet

- Kaveri Seeds - June 2021Document10 pagesKaveri Seeds - June 2021gaurav guptaNo ratings yet

- SBICARD Q1FY21 RESULTS SHOW REGULAR SPENDING UPTICK DEFIES LOCKDOWN CHALLENGESDocument4 pagesSBICARD Q1FY21 RESULTS SHOW REGULAR SPENDING UPTICK DEFIES LOCKDOWN CHALLENGESYash devgariaNo ratings yet

- Q1 2020-21 Fact Sheet PDFDocument27 pagesQ1 2020-21 Fact Sheet PDFJose CANo ratings yet

- Avenue Supermarts - REDUCE: Margin Miss Offsets Sales BeatDocument8 pagesAvenue Supermarts - REDUCE: Margin Miss Offsets Sales BeatAshokNo ratings yet

- Team7 FMPhase2 Trent SENIORSDocument75 pagesTeam7 FMPhase2 Trent SENIORSNisarg Rupani100% (1)

- 1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationDocument8 pages1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationJajahinaNo ratings yet

- Auto Components Infographic November 2021Document1 pageAuto Components Infographic November 2021ROOHI SHARMA 19111037No ratings yet

- Indian Healthcare and Pharma Industry Full Report 1624655688Document11 pagesIndian Healthcare and Pharma Industry Full Report 1624655688saurav_kumar_32No ratings yet

- Trent 10 08 2023 IscDocument7 pagesTrent 10 08 2023 Iscaghosh704No ratings yet

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDocument14 pagesWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNo ratings yet

- Himanshu Parihar 211510023747 SocratesDocument7 pagesHimanshu Parihar 211510023747 SocratesHimanshu PariharNo ratings yet

- Calculate CAGR, NPV, IRR and Revenue ProjectionDocument14 pagesCalculate CAGR, NPV, IRR and Revenue ProjectionSamuel WuNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

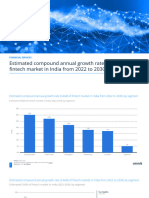

- Statistic - Id1372816 - Estimated Cagr of Fintech Market in India 2022 2030 by SegmentDocument8 pagesStatistic - Id1372816 - Estimated Cagr of Fintech Market in India 2022 2030 by SegmentGuilherme LustosaNo ratings yet

- Parag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyDocument10 pagesParag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyNiravAcharyaNo ratings yet

- 1Q20 Core Earnings in Line With Forecast: Metro Pacific Investments CorporationDocument8 pages1Q20 Core Earnings in Line With Forecast: Metro Pacific Investments CorporationJNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- Balkrishna Industries LTD: Investor Presentation - May 2021Document31 pagesBalkrishna Industries LTD: Investor Presentation - May 2021Kpvs NikhilNo ratings yet

- Secondary Pres On MULDocument23 pagesSecondary Pres On MULnishantNo ratings yet

- 2 Wheelers in A Sweet Spot - Flag Bearer of The Recovery in Automotive SegmentDocument23 pages2 Wheelers in A Sweet Spot - Flag Bearer of The Recovery in Automotive SegmentayushNo ratings yet

- Key Performance Indicators Y/E MarchDocument1 pageKey Performance Indicators Y/E Marchretrov androsNo ratings yet

- Sub: Investor Presentation On The Financial ResultsDocument13 pagesSub: Investor Presentation On The Financial ResultsPabloNo ratings yet

- KPIT Income Statement Analysis and ForecastingDocument13 pagesKPIT Income Statement Analysis and ForecastingAnonymous Fr37v90cqNo ratings yet

- Camposol Real Food For Life: CAMPOSOL Holding LTD Fourth Quarter and Preliminary Full Year 2015 ReportDocument25 pagesCamposol Real Food For Life: CAMPOSOL Holding LTD Fourth Quarter and Preliminary Full Year 2015 Reportkaren ramosNo ratings yet

- IDirect SKFIndia Q2FY20Document10 pagesIDirect SKFIndia Q2FY20praveensingh77No ratings yet

- Radico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020Document23 pagesRadico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020UmangNo ratings yet

- TCS Financial Results: Quarter III FY 2021-22Document25 pagesTCS Financial Results: Quarter III FY 2021-22Arindam MukhopadhyayNo ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- Quarterly Results 2010-11: HCL TechnologiesDocument31 pagesQuarterly Results 2010-11: HCL Technologies13lackhatNo ratings yet

- Q1 - 2023 24 Investor PresentationDocument27 pagesQ1 - 2023 24 Investor PresentationashwinsadvayofficialNo ratings yet

- Q2'10 - Investor Fact SheetDocument2 pagesQ2'10 - Investor Fact Sheet2020technologiesNo ratings yet

- How India Celebrates Report Dec 2021Document21 pagesHow India Celebrates Report Dec 2021Krish PatelNo ratings yet

- Vijaya Diagnostic Centre Limited Q4 & FY22 Investor PresentationDocument37 pagesVijaya Diagnostic Centre Limited Q4 & FY22 Investor PresentationShivang AsharNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- Valuation - Wokmore PDFDocument2 pagesValuation - Wokmore PDFDaemon7No ratings yet

- H123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosDocument30 pagesH123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosNikhilKapoor29No ratings yet

- TVS Motor Company: CMP: INR549 TP: INR548Document12 pagesTVS Motor Company: CMP: INR549 TP: INR548anujonwebNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- Auto Components Infographic December 2023Document1 pageAuto Components Infographic December 2023raghunandhan.cvNo ratings yet

- Highlights of the Growing Indian Auto Ancillary IndustryDocument19 pagesHighlights of the Growing Indian Auto Ancillary IndustryVijayBhasker VeluryNo ratings yet

- MB Cap supplier layout BR08 and BR10Document2 pagesMB Cap supplier layout BR08 and BR10KarthikMeenakshiSundaramNo ratings yet

- DMA-EZCCM-001 Reference Manual PDFDocument50 pagesDMA-EZCCM-001 Reference Manual PDFKarthikMeenakshiSundaramNo ratings yet

- Dataman 50: Reference ManualDocument36 pagesDataman 50: Reference ManualKarthikMeenakshiSundaramNo ratings yet

- Dataman Fixed Mount Readers Reference Manual: 2019 March 22 Revision: 6.1.6.64Document130 pagesDataman Fixed Mount Readers Reference Manual: 2019 March 22 Revision: 6.1.6.64KarthikMeenakshiSundaramNo ratings yet

- Dataman 50: Quick Reference GuideDocument17 pagesDataman 50: Quick Reference GuideKarthikMeenakshiSundaramNo ratings yet

- Control Box Reference GuideDocument5 pagesControl Box Reference GuideKarthikMeenakshiSundaramNo ratings yet

- 2019 ID Guide PDFDocument20 pages2019 ID Guide PDFKarthikMeenakshiSundaramNo ratings yet

- Cognex Machine VisionDocument20 pagesCognex Machine VisionKevanNo ratings yet

- 3D-A1000 Dimensioning System: Fast, Accurate, and Intuitive Dimensioning TechnologyDocument4 pages3D-A1000 Dimensioning System: Fast, Accurate, and Intuitive Dimensioning TechnologyKarthikMeenakshiSundaramNo ratings yet

- 2016 ID GuideDocument16 pages2016 ID GuideKarthikMeenakshiSundaramNo ratings yet

- DM150 Quick ReferenceDocument20 pagesDM150 Quick ReferenceKarthikMeenakshiSundaramNo ratings yet

- Cognex Machine VisionDocument20 pagesCognex Machine VisionKevanNo ratings yet

- 7 Rules For Successful SellingDocument2 pages7 Rules For Successful SellingKarthikMeenakshiSundaramNo ratings yet

- 2015 ID GuideDocument16 pages2015 ID GuideKarthikMeenakshiSundaramNo ratings yet

- IDDocument39 pagesIDKarthikMeenakshiSundaramNo ratings yet

- ACMA-Presentation Press-Conference 2020Document16 pagesACMA-Presentation Press-Conference 2020KarthikMeenakshiSundaramNo ratings yet

- Theory On Variable Frequency DriveDocument39 pagesTheory On Variable Frequency DriveKarthikMeenakshiSundaramNo ratings yet