You might also like

- Test Bank For Advertising and Promotion: An Integrated Marketing Communications Perspective, 12th Edition, George Belch Michael BelchDocument28 pagesTest Bank For Advertising and Promotion: An Integrated Marketing Communications Perspective, 12th Edition, George Belch Michael BelchPauline Chavez100% (12)

- PFRS 15 Revenue From Contracts With CustomersDocument7 pagesPFRS 15 Revenue From Contracts With Customerspanda 1100% (2)

- Revenue Recognition Accounting TheoryDocument4 pagesRevenue Recognition Accounting TheorychristoperedwinNo ratings yet

- (AFAR) (S05) - PFRS 15, Installment Sales, and Consignment SalesDocument6 pages(AFAR) (S05) - PFRS 15, Installment Sales, and Consignment SalesPolinar Paul MarbenNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Open Book - The Inside Track To - John C. P. Goldberg - 1Document11 pagesOpen Book - The Inside Track To - John C. P. Goldberg - 1smith smith100% (1)

- Pakistan International School, Riyadh.: Admission Test Guideline For Play Group Nursery KindergartenDocument2 pagesPakistan International School, Riyadh.: Admission Test Guideline For Play Group Nursery KindergartenSikandar KhanNo ratings yet

- Maserati Granturismo Coupe 4 2l 2009 2018 Workshop Manual Wiring DiagramsDocument22 pagesMaserati Granturismo Coupe 4 2l 2009 2018 Workshop Manual Wiring Diagramschristopherwhite251290ywa100% (111)

- Revenue Revisited: The Global Body For Professional AccountantsDocument3 pagesRevenue Revisited: The Global Body For Professional AccountantsPANTUGNo ratings yet

- IFRS 15 Revenue From Contracts With Customers-2Document8 pagesIFRS 15 Revenue From Contracts With Customers-2abbyNo ratings yet

- Revenue Revisited - Part 1 - ACCA GlobalDocument7 pagesRevenue Revisited - Part 1 - ACCA Globalvivsubs18No ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument5 pagesIFRS 15 Revenue From Contracts With CustomersADEYANJU AKEEMNo ratings yet

- Acca Ifrs 15Document19 pagesAcca Ifrs 15Ittihadul islamNo ratings yet

- Week 3 IFRS 15-Revenue From Contracts With CustomersDocument20 pagesWeek 3 IFRS 15-Revenue From Contracts With CustomerskoketsoNo ratings yet

- Impact and Implication of PFRS 15Document7 pagesImpact and Implication of PFRS 15Jethermaine BaybayanNo ratings yet

- Revenue Recognition Under PFRS 15Document14 pagesRevenue Recognition Under PFRS 15Jenver BuenaventuraNo ratings yet

- Module 1 - PDFDocument4 pagesModule 1 - PDFMelanie SamsonaNo ratings yet

- P2 Day 18 IFRS 15 (Tang) Solution PDFDocument5 pagesP2 Day 18 IFRS 15 (Tang) Solution PDFAmanda7No ratings yet

- Ind As 115 Revenue From Contracts With Customers Overview and Impact OnDocument34 pagesInd As 115 Revenue From Contracts With Customers Overview and Impact OnVM educationzNo ratings yet

- 43219A IFRS 15 - GAAP - bd1Document30 pages43219A IFRS 15 - GAAP - bd1DimakatsoNo ratings yet

- PRFS 15Document3 pagesPRFS 15Heneir FloresNo ratings yet

- Implementing PFRS 15: Challenges of An Accounting ChangeDocument3 pagesImplementing PFRS 15: Challenges of An Accounting ChangeNathanielNo ratings yet

- IFRS15 Revenue Recognition GuideDocument4 pagesIFRS15 Revenue Recognition GuideDaniel Nichole MerindoNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument8 pagesIfrs 15: Revenue From Contracts With CustomersAira Nhaira MecateNo ratings yet

- IFRS 15 ImplementationDocument30 pagesIFRS 15 Implementationbalint_renata_1No ratings yet

- Group 6-Psak 72 (Makalah) PDFDocument25 pagesGroup 6-Psak 72 (Makalah) PDFdwi davisNo ratings yet

- PFRS 15 Revenue GuideDocument12 pagesPFRS 15 Revenue GuideEdison Salgado CastigadorNo ratings yet

- Revenue Recognition Ifrs 15 ModelDocument4 pagesRevenue Recognition Ifrs 15 ModelAbdulhameed Babalola0% (1)

- AFAR-06 (Revenue From Contracts With Customers - Other Topics)Document26 pagesAFAR-06 (Revenue From Contracts With Customers - Other Topics)MABI ESPENIDONo ratings yet

- MFRS 15 Implementation Challenges for Construction, Telecom, AutomotiveDocument6 pagesMFRS 15 Implementation Challenges for Construction, Telecom, AutomotiveNik RubiahNo ratings yet

- Chapter 12 Revenue From Contracts With CustomersDocument24 pagesChapter 12 Revenue From Contracts With CustomersJane DizonNo ratings yet

- IFRS-15 Mepov23Document4 pagesIFRS-15 Mepov23Youssef ShabanNo ratings yet

- IFRS 15 Revenue From Contracts With Customers: Are You Ready For The "Big Change?"Document4 pagesIFRS 15 Revenue From Contracts With Customers: Are You Ready For The "Big Change?"Miruna CatalinaNo ratings yet

- PWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018Document12 pagesPWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018sourabhbansal108No ratings yet

- IFRS 15 Revenue from Contracts Customers GuideDocument8 pagesIFRS 15 Revenue from Contracts Customers GuideEmezi Francis ObisikeNo ratings yet

- AFAR-06 (Revenue From Customer Contracts - Other Topics)Document26 pagesAFAR-06 (Revenue From Customer Contracts - Other Topics)mysweet surrenderNo ratings yet

- Ifrs 15Document7 pagesIfrs 15Nauman KhalidNo ratings yet

- Applying IFRS Power-UtilitiesDocument20 pagesApplying IFRS Power-Utilitiesstudentul1986100% (1)

- Ifrs 15: Revenue From Contracts With CustomersDocument4 pagesIfrs 15: Revenue From Contracts With CustomersALMA MORENA100% (2)

- Implementing IFRS 15 Revenue From: Contracts With CustomersDocument24 pagesImplementing IFRS 15 Revenue From: Contracts With Customershui7411No ratings yet

- Problems in Revenue RecognitionDocument4 pagesProblems in Revenue RecognitionNaga Praveen TNo ratings yet

- IFRS 15 - Revenue From Contracts With CustomersDocument5 pagesIFRS 15 - Revenue From Contracts With CustomersAnkur MittalNo ratings yet

- BSA 3101 Topic 3A - Revenue From ContractsDocument14 pagesBSA 3101 Topic 3A - Revenue From ContractsDerek ShepherdNo ratings yet

- CFAS Unit 1 - Module 5.1Document11 pagesCFAS Unit 1 - Module 5.1Ralph Lefrancis DomingoNo ratings yet

- IFRS Industry Insights: Technology SectorDocument3 pagesIFRS Industry Insights: Technology SectorKiranmai GogireddyNo ratings yet

- IFRS 15 Revenue RecognitionDocument18 pagesIFRS 15 Revenue RecognitionHamza JavaidNo ratings yet

- EY Devel80 Revenue May2014Document4 pagesEY Devel80 Revenue May2014Tanjim TanimNo ratings yet

- IFRS Industry Issues IFRS 15 Issue 4Document5 pagesIFRS Industry Issues IFRS 15 Issue 4Rejoice MpofuNo ratings yet

- Technical LineDocument27 pagesTechnical LinemalisevicNo ratings yet

- Accounting Theory - Revenue RecognitionDocument5 pagesAccounting Theory - Revenue RecognitionHeather Hudson100% (1)

- IFRS 15 (IAS) - Revenue From Contracts With CustomersDocument10 pagesIFRS 15 (IAS) - Revenue From Contracts With CustomersAngie MagnayeNo ratings yet

- IFRS 15 - Aerospace Practical Guide Global PDFDocument30 pagesIFRS 15 - Aerospace Practical Guide Global PDFLeoAngeloLarciaNo ratings yet

- IFRS 15 5-Step Model for Revenue RecognitionDocument32 pagesIFRS 15 5-Step Model for Revenue RecognitionMarian MarNo ratings yet

- PFRS 15, MarbellaDocument3 pagesPFRS 15, MarbellaDazzelle BasarteNo ratings yet

- Chapter 6 - Revenue RecognitionDocument7 pagesChapter 6 - Revenue RecognitionGebeyaw BayeNo ratings yet

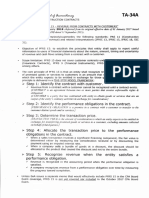

- Toa 34a-3Document1 pageToa 34a-3Arvin Glen BeltranNo ratings yet

- IFRS 15 Summary PDFDocument8 pagesIFRS 15 Summary PDFAshraf ValappilNo ratings yet

- Q30 Egin Part (A) - pg43, pg176 The Need For A Conceptual FrameworkDocument16 pagesQ30 Egin Part (A) - pg43, pg176 The Need For A Conceptual FrameworkLe YenNo ratings yet

- IFRS 15 Revenue RecognitionDocument7 pagesIFRS 15 Revenue RecognitionLumingNo ratings yet

- IFRS Practice Issues Revenue NIIF 15 Sept14Document204 pagesIFRS Practice Issues Revenue NIIF 15 Sept14prof_fids100% (1)

- Updates in FRS IFRS 15Document19 pagesUpdates in FRS IFRS 15Mary Rose MercadoNo ratings yet

- Strategic Economic Relationships: Contracts and Production ProcessesFrom EverandStrategic Economic Relationships: Contracts and Production ProcessesNo ratings yet

- Suspense Accounts and Error CorrectionDocument5 pagesSuspense Accounts and Error CorrectionNozimanga ChiroroNo ratings yet

- The Need For and An Understanding of A Conceptual FrameworkDocument5 pagesThe Need For and An Understanding of A Conceptual FrameworkNozimanga ChiroroNo ratings yet

- What Is A Financial InstrumentDocument7 pagesWhat Is A Financial InstrumentNozimanga ChiroroNo ratings yet

- Research and DevelopmentDocument4 pagesResearch and DevelopmentNozimanga ChiroroNo ratings yet

- IdiomebiDocument180 pagesIdiomebiTea GaguaNo ratings yet

- UCSPDocument31 pagesUCSProseNo ratings yet

- Recap To r7 Sept 25 To 26, 2022Document5 pagesRecap To r7 Sept 25 To 26, 2022john ivanNo ratings yet

- CH 02Document42 pagesCH 02Lê JerryNo ratings yet

- D.03 Fraud QuestionnaireDocument4 pagesD.03 Fraud QuestionnaireChè HadiansyahNo ratings yet

- Quiz BeeDocument19 pagesQuiz BeeJanara WamarNo ratings yet

- Plaintiff-Appellee: Second DivisionDocument14 pagesPlaintiff-Appellee: Second DivisionAurora SolastaNo ratings yet

- NSS Exploring Economics 1 (3 Edition) : Revision NotesDocument4 pagesNSS Exploring Economics 1 (3 Edition) : Revision NotesadrianNo ratings yet

- Rizal and The Chinese ConnectionDocument12 pagesRizal and The Chinese ConnectionLee HoseokNo ratings yet

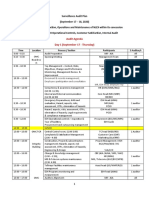

- Surveillance Audit PlanDocument3 pagesSurveillance Audit PlanJessa VillanuevaNo ratings yet

- Template Dco Manual FinalDocument96 pagesTemplate Dco Manual FinalCaitlin Ann AlonzoNo ratings yet

- People v. VergaraDocument2 pagesPeople v. VergaraVoid LessNo ratings yet

- Chapter - IDocument42 pagesChapter - IAbineshwaran SaravananNo ratings yet

- Module 1 - Topic No. 1 - Part4Document10 pagesModule 1 - Topic No. 1 - Part4Limuel MacasaetNo ratings yet

- Apsic Announcement JakartaDocument16 pagesApsic Announcement Jakartaakreditasi rssriwijayaNo ratings yet

- Auditing Theory RA 9298 Auditing Theory RA 9298Document10 pagesAuditing Theory RA 9298 Auditing Theory RA 9298sninaricaNo ratings yet

- Synacomex 2000Document5 pagesSynacomex 2000Giurca RaduNo ratings yet

- Charge Assumption ReportDocument2 pagesCharge Assumption ReportALi MAlikNo ratings yet

- Dwnload Full Cengage Advantage Books Essentials of The Legal Environment Today 5th Edition Miller Solutions Manual PDFDocument36 pagesDwnload Full Cengage Advantage Books Essentials of The Legal Environment Today 5th Edition Miller Solutions Manual PDFmagawumiicav100% (10)

- Tamargo Vs CADocument2 pagesTamargo Vs CAralph_atmosferaNo ratings yet

- SBU - Syllabus in Criminal Law I (Updated For AY 2023-2024) CLEANDocument29 pagesSBU - Syllabus in Criminal Law I (Updated For AY 2023-2024) CLEANCarmela Luchavez AndesNo ratings yet

- دور صندوق النقد الدولي في إدارة أزمة الديون الخارجية للدول العربية خلال الفترة (2008 2015م)Document19 pagesدور صندوق النقد الدولي في إدارة أزمة الديون الخارجية للدول العربية خلال الفترة (2008 2015م)Addam AbdelghaniNo ratings yet

- Module 8Document38 pagesModule 8Dissa Dorothy AnghagNo ratings yet

- Motion For Discovery of An Injury in Fact To Prove Personal JurisdictionDocument13 pagesMotion For Discovery of An Injury in Fact To Prove Personal JurisdictionDavid Dienamik89% (9)

- Session Breakout StrategyDocument2 pagesSession Breakout Strategyvamsi kumarNo ratings yet

- Regulations of The Occupational Health and Safety DepartmentDocument62 pagesRegulations of The Occupational Health and Safety DepartmentCruz CruzNo ratings yet