You might also like

- Auditing ReportDocument5 pagesAuditing ReportFRAULIEN GLINKA FANUGAONo ratings yet

- Psa 120Document14 pagesPsa 120Kimberly LimNo ratings yet

- Requirements FOR PAS 701: Key Audit MattersDocument3 pagesRequirements FOR PAS 701: Key Audit MattersRenella Dane H PinedaNo ratings yet

- Section 2: Audit Plan Overall Audit Strategy (Audit Approach)Document7 pagesSection 2: Audit Plan Overall Audit Strategy (Audit Approach)April ManjaresNo ratings yet

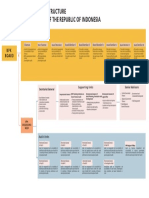

- Organizational Structure The Audit Board of The Republic of IndonesiaDocument1 pageOrganizational Structure The Audit Board of The Republic of IndonesiaFranz rumapeaNo ratings yet

- AUD610 June2016Document9 pagesAUD610 June2016Nurfara ZakariaNo ratings yet

- Introduction To AuditingDocument2 pagesIntroduction To Auditinglied27106No ratings yet

- Audit Report00Document64 pagesAudit Report00tilokiNo ratings yet

- ISO Auditing-2Document25 pagesISO Auditing-2suniljayaNo ratings yet

- Completing The Audit: Chapter ObjectivesDocument9 pagesCompleting The Audit: Chapter ObjectivesEmmaNo ratings yet

- Then Do A Pictionary of The Jobs That You Can See in The PuzzleDocument7 pagesThen Do A Pictionary of The Jobs That You Can See in The PuzzleDayana VegaNo ratings yet

- F-RAI-024 Summary of Internal Auditor Evaluation Rev. 0Document3 pagesF-RAI-024 Summary of Internal Auditor Evaluation Rev. 0welmar urquiaNo ratings yet

- Audit Reports: Learning OutcomesDocument50 pagesAudit Reports: Learning OutcomesParmila RawatNo ratings yet

- Psa 700Document1 pagePsa 700Mary Grace NaragNo ratings yet

- Informe: Evaluación de Comentarios Y Aclaraciones Elaboración AprobaciónDocument8 pagesInforme: Evaluación de Comentarios Y Aclaraciones Elaboración AprobaciónJeyson Fredd CVNo ratings yet

- Internal Quality Audit Report TemplateDocument3 pagesInternal Quality Audit Report TemplateGVS RaoNo ratings yet

- Overview of Audit Process and Pre-Engagement ActivitiesDocument5 pagesOverview of Audit Process and Pre-Engagement ActivitiesJoyce Ann CortezNo ratings yet

- Auditing Notes 4 SWDocument4 pagesAuditing Notes 4 SWDhiraj rahateNo ratings yet

- Adobe Scan May 07, 2021Document22 pagesAdobe Scan May 07, 2021T.Gayatri Devi Guest FacultyNo ratings yet

- SA 700 New Nov 18 Elements of Audit Report (Sections) : Independent Auditor'SDocument1 pageSA 700 New Nov 18 Elements of Audit Report (Sections) : Independent Auditor'SApeksha ChilwalNo ratings yet

- CA Pragati Gupta: Mobile: +91-9718319246Document2 pagesCA Pragati Gupta: Mobile: +91-9718319246The Cultural CommitteeNo ratings yet

- Psa 540 Audit of Accounting EstimatesDocument1 pagePsa 540 Audit of Accounting EstimatesHatake KakashiNo ratings yet

- Audit ReportDocument71 pagesAudit ReportShruth ShahNo ratings yet

- Week 1 - Introduction and Audit FrameworkDocument20 pagesWeek 1 - Introduction and Audit FrameworkGnanapragasam NavaneethanNo ratings yet

- Assessing External Audit Effectiveness: Audit Committee Oversight EssentialsDocument2 pagesAssessing External Audit Effectiveness: Audit Committee Oversight EssentialsWilson FernandoNo ratings yet

- Chapter14 - Auditing IT Controls Part 1 - BSA2ADocument10 pagesChapter14 - Auditing IT Controls Part 1 - BSA2AjejelaNo ratings yet

- Framework of Philippine Standards On AuditingDocument35 pagesFramework of Philippine Standards On AuditingSalmairah Balty AmoreNo ratings yet

- CHAPTER 5 - AudTheoDocument4 pagesCHAPTER 5 - AudTheoVicente, Liza Mae C.No ratings yet

- Chapter 2 - Audit Strategy, Planning and ProgrammingDocument1 pageChapter 2 - Audit Strategy, Planning and Programmingthuzh007No ratings yet

- Audit ReportsDocument72 pagesAudit Reportskaran kapadiaNo ratings yet

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- SA Chart FullDocument37 pagesSA Chart FullJinal SanghviNo ratings yet

- Content Explanation Impact of Various IssuesDocument3 pagesContent Explanation Impact of Various IssuesSyedSumairNo ratings yet

- Module 1 PDFDocument8 pagesModule 1 PDFKez MaxNo ratings yet

- Fundamentals of Auditing FinalDocument4 pagesFundamentals of Auditing FinalLv ValenzonaNo ratings yet

- Standards On Auditing: Presented By: Nikhil Panicker Manaswi Tripathi Moderator: CA. Abhay ChhajedDocument85 pagesStandards On Auditing: Presented By: Nikhil Panicker Manaswi Tripathi Moderator: CA. Abhay Chhajedneelam mishraNo ratings yet

- Audit PlanningDocument2 pagesAudit Planninglied27106No ratings yet

- Chapter 07 - Audit ReportingDocument8 pagesChapter 07 - Audit ReportingDamsaraNo ratings yet

- 62549studentjournal-Jan2021a (1) - RemovedDocument15 pages62549studentjournal-Jan2021a (1) - RemovedTimepass MungfuliNo ratings yet

- Lecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesLecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDenny June CraususNo ratings yet

- IAASB (2015a) - at A Glance. New and Revised Auditor Reporting Standards and Related Conforming AmendmentsDocument12 pagesIAASB (2015a) - at A Glance. New and Revised Auditor Reporting Standards and Related Conforming AmendmentsAndrecarvalho97No ratings yet

- AG Presentation 2nd Annual Board Training 11 June 2021 FinalDocument15 pagesAG Presentation 2nd Annual Board Training 11 June 2021 FinalREJAY89No ratings yet

- 2017-1 Acct7103 01 L-BB PDFDocument7 pages2017-1 Acct7103 01 L-BB PDFStephanie XieNo ratings yet

- PAS 700 and 701 Graphic OrganizerDocument2 pagesPAS 700 and 701 Graphic OrganizerwencyNo ratings yet

- Aud Agile Eng m04 Pnotes Conducting An AuditDocument24 pagesAud Agile Eng m04 Pnotes Conducting An AuditMohamed ElsawyNo ratings yet

- DOH AG III - Accomplishment ReportDocument18 pagesDOH AG III - Accomplishment Reportshane natividadNo ratings yet

- SA Chart 200 330Document14 pagesSA Chart 200 330mohammed farisNo ratings yet

- Ch. 7 - Audit Reports CA Study NotesDocument3 pagesCh. 7 - Audit Reports CA Study NotesUnpredictable TalentNo ratings yet

- This Study Resource Was Shared Via: Chapter 2 - Audit Strategy, Planning and ProgrammingDocument1 pageThis Study Resource Was Shared Via: Chapter 2 - Audit Strategy, Planning and ProgrammingNavneet NandaNo ratings yet

- Auditing Full Version Sir Jaypee Tinipid Version1Document17 pagesAuditing Full Version Sir Jaypee Tinipid Version1Lovely Rose ArpiaNo ratings yet

- In Audit New Auditors Report Insights Infographic Doc NoexpDocument3 pagesIn Audit New Auditors Report Insights Infographic Doc NoexpHitesh ValechaNo ratings yet

- Standalone Financial StatementsDocument39 pagesStandalone Financial StatementsLogan ThakurNo ratings yet

- AT 2.03 Risk Assessment Phase I - B Part 2 PSA320Document33 pagesAT 2.03 Risk Assessment Phase I - B Part 2 PSA320Alyssa MoralesNo ratings yet

- G10349 RG Audit Assurance Alert CAS 701 Key Audit Matters December 2018 PDFDocument16 pagesG10349 RG Audit Assurance Alert CAS 701 Key Audit Matters December 2018 PDFJosephNo ratings yet

- Refreshed Auditors Report January 2018Document8 pagesRefreshed Auditors Report January 2018Shahid MahmudNo ratings yet

- SAMPLE Auditing PDFDocument74 pagesSAMPLE Auditing PDFMiku LendioNo ratings yet

- Assessing External Audit QualityDocument4 pagesAssessing External Audit QualityLarkinNo ratings yet

- Micb 2014 Ifrs enDocument61 pagesMicb 2014 Ifrs enDaniel PetracheNo ratings yet

- MARCH 2013: Presentation of The Auditor-GeneralDocument22 pagesMARCH 2013: Presentation of The Auditor-GeneraljamalNo ratings yet

- THE LAW ON SALES BLOG Case Digest Submitted by ZosaDocument5 pagesTHE LAW ON SALES BLOG Case Digest Submitted by ZosawencyNo ratings yet

- Management Information SystemDocument12 pagesManagement Information SystemregenNo ratings yet

- SAADDocument2 pagesSAADwencyNo ratings yet

- G.R. No. 128759 - Jaromay Laurente Pamaos Law OfficesDocument8 pagesG.R. No. 128759 - Jaromay Laurente Pamaos Law OfficeswencyNo ratings yet

- 2 Needs To AutomateDocument1 page2 Needs To AutomatewencyNo ratings yet

- CindysDocument1 pageCindyswencyNo ratings yet

- G.R. No. 116635 - CONCHITA NOOL ET AL. vs. COURT OF APPEALS EDocument9 pagesG.R. No. 116635 - CONCHITA NOOL ET AL. vs. COURT OF APPEALS EwencyNo ratings yet

- Physician Use of A Computerized Medical Record System During THDocument2 pagesPhysician Use of A Computerized Medical Record System During THwencyNo ratings yet

- Custom Search: Today Is Monday, April 02, 2018Document7 pagesCustom Search: Today Is Monday, April 02, 2018wencyNo ratings yet

- Tomas See Tuazon, Petitioner, vs. Court of Appeals and John Siy LIM, RespondentsDocument9 pagesTomas See Tuazon, Petitioner, vs. Court of Appeals and John Siy LIM, RespondentswencyNo ratings yet

- Aguirre Vs CADocument3 pagesAguirre Vs CAdempe24No ratings yet

- PAS 700 and 701 Graphic OrganizerDocument2 pagesPAS 700 and 701 Graphic OrganizerwencyNo ratings yet

- Conchita Nool and Gaudencio Almojera, Petitioner, vs. Court of Appeals, Anacleto Nool and Emilia Nebre, RespondentsDocument10 pagesConchita Nool and Gaudencio Almojera, Petitioner, vs. Court of Appeals, Anacleto Nool and Emilia Nebre, RespondentswencyNo ratings yet

- Supply AnalysisDocument2 pagesSupply AnalysiswencyNo ratings yet

- PAS 700 and 701 Graphic OrganizerDocument2 pagesPAS 700 and 701 Graphic OrganizerwencyNo ratings yet

- Demand AnalysisDocument2 pagesDemand AnalysiswencyNo ratings yet

- Review Questions - Chapter 9 Internal AuditDocument7 pagesReview Questions - Chapter 9 Internal AudithaleedaNo ratings yet

- Acctg I State Test Review Packet - KEYDocument13 pagesAcctg I State Test Review Packet - KEYMr. Intel0% (1)

- Capital Structure On Bank Performance Report.Document25 pagesCapital Structure On Bank Performance Report.Aniba ButtNo ratings yet

- DTMFIs Minimum Licensing Requirements 2020 FinalDocument21 pagesDTMFIs Minimum Licensing Requirements 2020 FinalLesley munikwaNo ratings yet

- Slaus 570 - Going ConcernDocument22 pagesSlaus 570 - Going ConcernsamaanNo ratings yet

- Tactics For Preventing and Detecting FraudDocument3 pagesTactics For Preventing and Detecting Fraudharikrishna_rsNo ratings yet

- MTM HR Internship ReportDocument73 pagesMTM HR Internship Reportsunny_fzNo ratings yet

- PSQCS, Framework, Psas, Papss, Psres, Psaes, PsrssDocument3 pagesPSQCS, Framework, Psas, Papss, Psres, Psaes, PsrssChristine Joyce FajardoNo ratings yet

- Benoy Mathew Resume-1Document2 pagesBenoy Mathew Resume-1Benoy MathewNo ratings yet

- Board of Directors: Company SecretaryDocument27 pagesBoard of Directors: Company SecretaryVaibhav AgrawalNo ratings yet

- Power of The Bir and Cir-Income Taxation 101-02.23.20Document4 pagesPower of The Bir and Cir-Income Taxation 101-02.23.20Dhierissa LeeNo ratings yet

- Model Constitution For A CharitableDocument14 pagesModel Constitution For A Charitableal mooreNo ratings yet

- General Reform SummaryDocument10 pagesGeneral Reform SummaryRaghu RamNo ratings yet

- Assurance Principles Midterm QuizDocument5 pagesAssurance Principles Midterm Quizjovelyn labordoNo ratings yet

- DISA 3.0 Mod1 Day 1 Quiz 1Document3 pagesDISA 3.0 Mod1 Day 1 Quiz 1Jackson Abraham ThekkekaraNo ratings yet

- 4.1 Enron The Control Environment RatanDocument3 pages4.1 Enron The Control Environment RatanNurul Islam 18352216600% (1)

- Caely Holdings (G14)Document38 pagesCaely Holdings (G14)sharvesh veshNo ratings yet

- FABM-1 - Module 1 - Intro To AccountingDocument13 pagesFABM-1 - Module 1 - Intro To AccountingKJ Jones100% (26)

- Ap RmycDocument16 pagesAp RmycJoseph Bayo BasanNo ratings yet

- Audit Firm SpecializationonEarningandauditquality PDFDocument27 pagesAudit Firm SpecializationonEarningandauditquality PDFBerthelo KuedaNo ratings yet

- ISA 701 MindMapDocument1 pageISA 701 MindMapAli HaiderNo ratings yet

- Exide Report 2010Document72 pagesExide Report 2010AzeembasheerNo ratings yet

- Auditing Quiz - Cash and Cash Equivalents Auditing Quiz - Cash and Cash EquivalentsDocument3 pagesAuditing Quiz - Cash and Cash Equivalents Auditing Quiz - Cash and Cash EquivalentsLawrence YusiNo ratings yet

- Sales Department Flowchart 2Document21 pagesSales Department Flowchart 2nicole bancoroNo ratings yet

- The Energy Conservation Act, 2001 No 52 2001: Ministry of Law, Justice and Company AffairsDocument26 pagesThe Energy Conservation Act, 2001 No 52 2001: Ministry of Law, Justice and Company AffairsMA AhmedNo ratings yet

- Materi Training Risk Champion 2023 v.3 AEIDocument97 pagesMateri Training Risk Champion 2023 v.3 AEIPutri jayantiNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- Ch18 Answer KeyDocument20 pagesCh18 Answer KeyWed CornelNo ratings yet

- Policy On Accounts ReceivableDocument8 pagesPolicy On Accounts ReceivableMazhar Hussain Ch.No ratings yet

- Certification RoadMapDocument8 pagesCertification RoadMapTakudzwa Calvin ChibudaNo ratings yet