You might also like

- Task 4c Math AssessmentDocument8 pagesTask 4c Math Assessmentapi-300180291No ratings yet

- Lesson Plan in Mathematics Grade 8 (Jhess)Document7 pagesLesson Plan in Mathematics Grade 8 (Jhess)Zetroc Jess82% (17)

- Math Ia FinalDocument26 pagesMath Ia FinalSanskar Gupta100% (2)

- BUS MATH Q3 L4. SLeM - 2S - Q3 - W4 - RatioDocument11 pagesBUS MATH Q3 L4. SLeM - 2S - Q3 - W4 - RatioSophia MagdaraogNo ratings yet

- Unit 3 FodDocument18 pagesUnit 3 FodkarthickamsecNo ratings yet

- Ratios and Proportions Business MathDocument22 pagesRatios and Proportions Business MathJan NaireNo ratings yet

- Ratio and Proportion:: Learners Module in Business MathematicsDocument13 pagesRatio and Proportion:: Learners Module in Business MathematicsJamaica C. Aquino50% (2)

- Odds Ratio Calculation and InterpretationDocument4 pagesOdds Ratio Calculation and InterpretationJing CruzNo ratings yet

- Math 11 ABM BUSMATH Q1 Week 3Document8 pagesMath 11 ABM BUSMATH Q1 Week 3Anacieto N. MercadoNo ratings yet

- Correlation ExplainedDocument11 pagesCorrelation ExplainedAlvin Wong100% (1)

- Arly As The 6th Century AD by Indian MathematiciansDocument42 pagesArly As The 6th Century AD by Indian MathematiciansHaryo WawanNo ratings yet

- Dee Hwa Liong Academy: Ratio and ProportionDocument12 pagesDee Hwa Liong Academy: Ratio and ProportionkelvinNo ratings yet

- Relations and Functions ExplainedDocument8 pagesRelations and Functions ExplainedBreyannah Elise CeriacoNo ratings yet

- RIP Correlation. Introducing The Predictive Power Score: Sign Up and Get An Extra One For FreeDocument11 pagesRIP Correlation. Introducing The Predictive Power Score: Sign Up and Get An Extra One For FreeVikash RryderNo ratings yet

- Attachment CODocument5 pagesAttachment COAngela RuleteNo ratings yet

- Common Core State Standards: National Glencoe Math, Course 2, © 2015Document14 pagesCommon Core State Standards: National Glencoe Math, Course 2, © 2015ahmed5030 ahmed5030No ratings yet

- Ratio and ProportionDocument53 pagesRatio and ProportionAbewenico LabajoNo ratings yet

- Math Success - Percents and RatiosDocument64 pagesMath Success - Percents and RatiosLớp Văn BằngNo ratings yet

- Lec 42Document27 pagesLec 42Mukesh BhardwajNo ratings yet

- MATH 6 - Q2 - Mod1Document12 pagesMATH 6 - Q2 - Mod13tj internetNo ratings yet

- 5-DLP-MATH9-Q3-WEEK 5-Part IDocument3 pages5-DLP-MATH9-Q3-WEEK 5-Part IJulius VillanuevaNo ratings yet

- Chapter08 Part 5Document19 pagesChapter08 Part 5api-232613595No ratings yet

- 1 - Brac University Student Honor CodeDocument6 pages1 - Brac University Student Honor CodeRejoanul IslamNo ratings yet

- Mathematics Lesson on RatiosDocument3 pagesMathematics Lesson on RatiostarbeecatNo ratings yet

- Math 11 Abm BM q1 Week 3Document10 pagesMath 11 Abm BM q1 Week 3Flordilyn DichonNo ratings yet

- 2nd Quarter Gen MathDocument2 pages2nd Quarter Gen MathLea Mae Vivo Gelera0% (1)

- Measures of RelationshipDocument11 pagesMeasures of RelationshipHarvin Bob PunoNo ratings yet

- Statistics For People Who Think They Hate Statistics 6th Edition Salkind Test Bank 1Document36 pagesStatistics For People Who Think They Hate Statistics 6th Edition Salkind Test Bank 1tylermorrisonaowkftpnzc100% (26)

- Math Relations Lesson: Transitivity, Reflexivity, SymmetryDocument4 pagesMath Relations Lesson: Transitivity, Reflexivity, SymmetrytheonNo ratings yet

- CQ CH 7Document3 pagesCQ CH 7api-356113513No ratings yet

- Ratio Analysis at Mahindra & Maghindra LTD Vinay Part BDocument64 pagesRatio Analysis at Mahindra & Maghindra LTD Vinay Part BPaneerNo ratings yet

- Math5 q2 Mod14 VisualizingTheRatioOfTwoQuantities v2Document20 pagesMath5 q2 Mod14 VisualizingTheRatioOfTwoQuantities v2Jiffrey JunioNo ratings yet

- Business Math - Ratio and ProportionDocument6 pagesBusiness Math - Ratio and ProportionYolanda Descallar100% (1)

- Simplifying Ratios: Q2 Math 5 Week 8 Lesson 2Document30 pagesSimplifying Ratios: Q2 Math 5 Week 8 Lesson 2Kenette QuinesNo ratings yet

- A Quick Intuition For Parametric EquationsDocument6 pagesA Quick Intuition For Parametric EquationsavnishNo ratings yet

- Number N of Items Purchased at A Constant Price P, The Relationship Between The Total Cost and The Number of Items Can Be Expressed As T PNDocument3 pagesNumber N of Items Purchased at A Constant Price P, The Relationship Between The Total Cost and The Number of Items Can Be Expressed As T PNIlham FalaniNo ratings yet

- Department of Education Lesson on Similarity of TrianglesDocument17 pagesDepartment of Education Lesson on Similarity of TrianglesMarjuline De GuzmanNo ratings yet

- Muhammad Luthfi Mahendra - 2001036085 - Chapter 6 ResumeDocument5 pagesMuhammad Luthfi Mahendra - 2001036085 - Chapter 6 Resumeluthfi mahendraNo ratings yet

- Why Do You Need To Scale Data in KNN: 3 AnswersDocument1 pageWhy Do You Need To Scale Data in KNN: 3 AnswersvaskoreNo ratings yet

- Math5 q2 Mod17 FindingTheMissingEquivalentRatiosDocument23 pagesMath5 q2 Mod17 FindingTheMissingEquivalentRatiosSally DelfinNo ratings yet

- Correlation Between Age and Vocabulary SizeDocument6 pagesCorrelation Between Age and Vocabulary SizeSkylar HsuNo ratings yet

- SHS BM Q1 WK 3Document12 pagesSHS BM Q1 WK 3Abegail Mendez EcsNo ratings yet

- M6u2 Conceptual Foundations 1Document5 pagesM6u2 Conceptual Foundations 1api-302577842No ratings yet

- TheMATStudyGuide PDFDocument16 pagesTheMATStudyGuide PDFMadan R HonnalagereNo ratings yet

- gould-ch04Document62 pagesgould-ch04AdmasuNo ratings yet

- STUDY NOTES 1 For PYC4807 PDFDocument4 pagesSTUDY NOTES 1 For PYC4807 PDFMbalenhle TshehlaNo ratings yet

- Math-Sp: COLLEGE PREP A.Y. 2023-2024Document25 pagesMath-Sp: COLLEGE PREP A.Y. 2023-2024Jemina PocheNo ratings yet

- Proportion: Lesso ns5Document14 pagesProportion: Lesso ns5Sophia MagdaraogNo ratings yet

- Appendix A-B-CDocument2 pagesAppendix A-B-CElgun ElgunNo ratings yet

- Math8 Q3 Mod4 IllustratingSAS v3Document31 pagesMath8 Q3 Mod4 IllustratingSAS v3Romelyn AlayonNo ratings yet

- How To Crack Test of Reasoning - Jai Kishan-FlattenedDocument447 pagesHow To Crack Test of Reasoning - Jai Kishan-Flattenedankita9qNo ratings yet

- Bachelor Thesis Eth ExampleDocument5 pagesBachelor Thesis Eth ExampleJanelle Martinez100% (2)

- Multidimensional Scaling by Optimizing Goodness of Fit To A Nonmetric HypothesisDocument27 pagesMultidimensional Scaling by Optimizing Goodness of Fit To A Nonmetric Hypothesismmonique.rizziNo ratings yet

- Math6 DLP q2 w1 Day 1Document5 pagesMath6 DLP q2 w1 Day 1karlo bernaldezNo ratings yet

- Content and Language Learning Goal: To Reinforce Key Words and Concepts RatioDocument4 pagesContent and Language Learning Goal: To Reinforce Key Words and Concepts RatioAstrid Leidy TrujilloNo ratings yet

- APA 7th Edition Tables FormatDocument8 pagesAPA 7th Edition Tables FormatLester ManiquezNo ratings yet

- Ch2 Association Slides Script PDFDocument101 pagesCh2 Association Slides Script PDFhuey992206No ratings yet

- Sim Math 8Document15 pagesSim Math 8May JavellanaNo ratings yet

- Ratio and ProportionDocument41 pagesRatio and ProportionAh RainNo ratings yet

- Lesson 2: Simple Comparative ExperimentsDocument8 pagesLesson 2: Simple Comparative ExperimentsIrya MalathamayaNo ratings yet

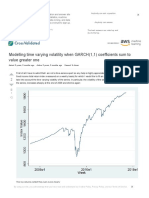

- Maximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedDocument4 pagesMaximum Likelihood - Modelling Time Varying Volatility When GARCH (1,1) Coefficients Sum To Value Greater One - Cross ValidatedJosé-Manuel Martin CoronadoNo ratings yet

- The Coefficient of Determination or R2 - Economic Theory BlogDocument3 pagesThe Coefficient of Determination or R2 - Economic Theory Bloglorenzo_stellaNo ratings yet

- EquilibrioDocument2 pagesEquilibriolorenzo_stellaNo ratings yet

- What Is The Difference Between Coefficient of Determination, and Coefficient of Correlation - Gaurav BansalDocument2 pagesWhat Is The Difference Between Coefficient of Determination, and Coefficient of Correlation - Gaurav Bansallorenzo_stellaNo ratings yet

- Jamminbook PDFDocument90 pagesJamminbook PDFDanny Dawson0% (1)

- Statistics, Probability, Distributions, & Error Propagation: James R. Graham 9/2/09Document39 pagesStatistics, Probability, Distributions, & Error Propagation: James R. Graham 9/2/09lorenzo_stellaNo ratings yet

- Arturo Himmer - Clarinet Plus! Vol.3 (In BB)Document28 pagesArturo Himmer - Clarinet Plus! Vol.3 (In BB)henry A.figueroa Parra100% (1)

- Relax to the soothing sounds of Moonlight SerenadeDocument1 pageRelax to the soothing sounds of Moonlight Serenadelorenzo_stella100% (1)

- Makin Whopee Da Alto Saxophone - Jazz Standards PDFDocument2 pagesMakin Whopee Da Alto Saxophone - Jazz Standards PDFlorenzo_stellaNo ratings yet

- Acscb 2017+siDocument15 pagesAcscb 2017+silorenzo_stellaNo ratings yet

- Arturo Himmer - Clarinet Plus! Vol.3 (In BB)Document28 pagesArturo Himmer - Clarinet Plus! Vol.3 (In BB)henry A.figueroa Parra100% (1)

- NoteinallegriaDocument1 pageNoteinallegrialorenzo_stellaNo ratings yet

- Biochimica Et Biophysica Acta 1828 (2013) 1013-1024Document29 pagesBiochimica Et Biophysica Acta 1828 (2013) 1013-1024lorenzo_stellaNo ratings yet

- Mo Better Blues PDFDocument7 pagesMo Better Blues PDFlorenzo_stellaNo ratings yet

- Mo Better Blues - MarsalisDocument1 pageMo Better Blues - Marsalislorenzo_stellaNo ratings yet

- Why Dont You Do RightDocument3 pagesWhy Dont You Do Rightlorenzo_stellaNo ratings yet

- Why Dont You Do RightDocument3 pagesWhy Dont You Do Rightlorenzo_stellaNo ratings yet

- Taguchi Methods: Reference For BusinessDocument11 pagesTaguchi Methods: Reference For Businessnitin_dhoot2005@yahoo.comNo ratings yet

- Adstock Modelling For The Long TermDocument12 pagesAdstock Modelling For The Long TermWim VerboomNo ratings yet

- The Geneva Mechanism ExplainedDocument11 pagesThe Geneva Mechanism ExplainedMonteiro727No ratings yet

- The Effect of Fraud Triangle in Detecting Financial Statement FraudDocument14 pagesThe Effect of Fraud Triangle in Detecting Financial Statement FraudEzra viollaNo ratings yet

- Analog Simulation Manual - 2Document72 pagesAnalog Simulation Manual - 2mefortruthNo ratings yet

- Lesson Plan in Mathematics 3 Quarter 1Document5 pagesLesson Plan in Mathematics 3 Quarter 1DoromalXD SorbitoNo ratings yet

- Quality ControlDocument33 pagesQuality ControlAydaLeeNo ratings yet

- Rajasthan Technical University B.Tech SyllabusDocument8 pagesRajasthan Technical University B.Tech SyllabusAmit BagrechaNo ratings yet

- Six Meter Heliax Duplexers: Low-Band VHF Heliax Duplexer Performance On 6 Meters, Notch StyleDocument20 pagesSix Meter Heliax Duplexers: Low-Band VHF Heliax Duplexer Performance On 6 Meters, Notch Stylelu1agpNo ratings yet

- Line-It-Up Math WorksheetDocument2 pagesLine-It-Up Math WorksheetI U100% (1)

- A. Null and Alternate Hypothesis: Post-Assessment-Written OutputsDocument6 pagesA. Null and Alternate Hypothesis: Post-Assessment-Written OutputsAngelika FerrerNo ratings yet

- JIT For Lean Manufacturing FinalDocument83 pagesJIT For Lean Manufacturing FinalMusical CorruptionNo ratings yet

- Pre CalculusDocument6 pagesPre CalculusRaeNo ratings yet

- Stereotypes GendersDocument4 pagesStereotypes Genders4jgzhmyprdNo ratings yet

- API 610 Notes PDFDocument0 pagesAPI 610 Notes PDFkkabbara100% (2)

- CH Computer NetworkingDocument7 pagesCH Computer NetworkingmahaNo ratings yet

- 16.2 Proceedings Ico Asnitech, PNP IndonesiaDocument168 pages16.2 Proceedings Ico Asnitech, PNP IndonesiaMustafa Akbar0% (1)

- Probability ScaleDocument4 pagesProbability ScaleMichaelKokolakisNo ratings yet

- Finite Cell Method: H-And P-Extension For Embedded Domain Problems in Solid MechanicsDocument13 pagesFinite Cell Method: H-And P-Extension For Embedded Domain Problems in Solid MechanicsAnkur NaraniwalNo ratings yet

- Multiple Regression ModelsDocument10 pagesMultiple Regression ModelsArun PrasadNo ratings yet

- 01 - 7-Class - Maths - Bridge Program - Atp NCS - 1-23Document23 pages01 - 7-Class - Maths - Bridge Program - Atp NCS - 1-23Rita TripathiNo ratings yet

- 403 S. H. S. C. E. Physics Objective and Essay TestsDocument11 pages403 S. H. S. C. E. Physics Objective and Essay TestsAyomide sayo-AdeyemiNo ratings yet

- PeterDocument30 pagesPeterJoão BeliniNo ratings yet

- Multisource and Multitemporal Data Fusion in Remote SensingDocument26 pagesMultisource and Multitemporal Data Fusion in Remote SensingJenniffer GuayaNo ratings yet

- Basic Mathematics 2011-QNDocument5 pagesBasic Mathematics 2011-QNEmanuel John BangoNo ratings yet

- Stock Watson 3U ExerciseSolutions Chapter7 Instructors PDFDocument12 pagesStock Watson 3U ExerciseSolutions Chapter7 Instructors PDFOtieno MosesNo ratings yet

- Distribution Table Probability and StatisticsDocument30 pagesDistribution Table Probability and StatisticsElena GomezNo ratings yet

- Chapter 7 PDFDocument25 pagesChapter 7 PDFbptlmohankumarNo ratings yet