You might also like

- Designing Brand Identity: A Comprehensive Guide to the World of Brands and BrandingFrom EverandDesigning Brand Identity: A Comprehensive Guide to the World of Brands and BrandingNo ratings yet

- Greeting CardsDocument32 pagesGreeting CardsArchana PooniaNo ratings yet

- Coaching Prices 2023 One-PagerDocument1 pageCoaching Prices 2023 One-PagerMukuka MbeweNo ratings yet

- Tweeter EtcDocument8 pagesTweeter EtcAbhishek KakraliaNo ratings yet

- Thesis On Resort PlanningDocument20 pagesThesis On Resort Planningcindy_kayNo ratings yet

- Product List - SoftwareDocument2 pagesProduct List - SoftwareThana BalanNo ratings yet

- Case Study K9FUELBARDocument2 pagesCase Study K9FUELBARAnonymous xH0aLu100% (1)

- In Class Activity 10 - Sheet1 PDFDocument1 pageIn Class Activity 10 - Sheet1 PDFpalak khuggarNo ratings yet

- Annual Marketing Budget TemplateDocument17 pagesAnnual Marketing Budget TemplateS CapNo ratings yet

- SKIM October 2015 Pricing WebinarDocument55 pagesSKIM October 2015 Pricing WebinarShilpi IslamNo ratings yet

- Performance TestDocument13 pagesPerformance TestSashauna GrahamNo ratings yet

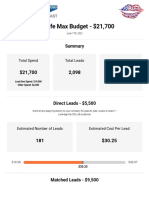

- CDLLife Max Budget - $21,700Document3 pagesCDLLife Max Budget - $21,700Brian KnightNo ratings yet

- Msla Business FeesDocument1 pageMsla Business FeesNBC MontanaNo ratings yet

- QSO 533 Week 4 Homework Starter FileDocument35 pagesQSO 533 Week 4 Homework Starter FileMellaniNo ratings yet

- Individual Assign #2 Answer TemplateDocument11 pagesIndividual Assign #2 Answer TemplateHarjinder KaurNo ratings yet

- Faculty of Management Science: Name: Fazil Ahmed Sec: B STUDENT ID: (27-2019)Document6 pagesFaculty of Management Science: Name: Fazil Ahmed Sec: B STUDENT ID: (27-2019)fazil ahmedNo ratings yet

- 5 Days MDP Course: Fabrikam ResidencesDocument19 pages5 Days MDP Course: Fabrikam ResidencesParnika JainNo ratings yet

- Cambridge Software Corporation: Case AnalysisDocument11 pagesCambridge Software Corporation: Case AnalysisMilind GuptaNo ratings yet

- Estructura de Costos RUMMACDocument6 pagesEstructura de Costos RUMMACValeria ShopNo ratings yet

- Marketing Budget Plan1Document4 pagesMarketing Budget Plan1brunoess.psdNo ratings yet

- CLV AnalysisDocument5 pagesCLV AnalysiskasataccountsNo ratings yet

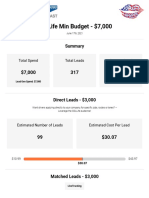

- CDLLife Min Budget - $7,000Document2 pagesCDLLife Min Budget - $7,000Brian KnightNo ratings yet

- Tutorial 3costDocument4 pagesTutorial 3costhwi91No ratings yet

- 05-ROAS Spreadsheet TemplateDocument26 pages05-ROAS Spreadsheet TemplatewaelNo ratings yet

- Savtech: Save Checks With SavtechDocument21 pagesSavtech: Save Checks With SavtechDavid KellerNo ratings yet

- Promotion BudgetDocument6 pagesPromotion BudgetRatidzai MuyamboNo ratings yet

- Thoery of The FirmDocument2 pagesThoery of The FirmKin0% (1)

- Rolling StoreDocument34 pagesRolling StoreAmie Jane MirandaNo ratings yet

- The Office Furniture Store Data FileDocument16 pagesThe Office Furniture Store Data FileVy Nguyễn Trần TườngNo ratings yet

- 2022 Marketing Plan Template (Mayple)Document47 pages2022 Marketing Plan Template (Mayple)TNo ratings yet

- Student Names Student Id Test 1 Test 2 Test 3 Final Internal Assesment Final GradeDocument12 pagesStudent Names Student Id Test 1 Test 2 Test 3 Final Internal Assesment Final GradeThùy DungNo ratings yet

- W1WS-Rimbawan-Bayu Sadewo-AdvancedDocument2 pagesW1WS-Rimbawan-Bayu Sadewo-AdvancedrimbawanbayusadewoNo ratings yet

- Cambridge Software Case HandoutDocument2 pagesCambridge Software Case HandoutSravan Kumar RapakaNo ratings yet

- According To The Case, The Distribution Method Is Shown BelowDocument4 pagesAccording To The Case, The Distribution Method Is Shown BelowrizqighaniNo ratings yet

- Strategic Cost ManagementDocument44 pagesStrategic Cost ManagementSeymur AbdurahmanovNo ratings yet

- Microeconomics Assignment q4Document2 pagesMicroeconomics Assignment q4Ahsan OrbinNo ratings yet

- NVU Comp Plan Master V - 03Document15 pagesNVU Comp Plan Master V - 03pofoya3158No ratings yet

- (IFA 11) - Rendy Filiang - 1402210324Document6 pages(IFA 11) - Rendy Filiang - 1402210324RENDY FILIANGNo ratings yet

- Cost of Goods ManufacturedDocument26 pagesCost of Goods ManufacturedAb.Rahman AfghanNo ratings yet

- 02 Cost Benefit AnalysisDocument4 pages02 Cost Benefit AnalysisMnM -No ratings yet

- Vision Global Amway Plan 2014Document46 pagesVision Global Amway Plan 2014Benjamin PuentesNo ratings yet

- Happy Bites - AFDM Term ProjectDocument20 pagesHappy Bites - AFDM Term Projectshayan.arif96No ratings yet

- Name: Description: Practice Marketing - Individual Corporation (Multiplayer)Document6 pagesName: Description: Practice Marketing - Individual Corporation (Multiplayer)Carlos Andres Contreras GajardoNo ratings yet

- Budget DefenseDocument19 pagesBudget Defenseapi-687516998No ratings yet

- 2020 Week 5 Funds 70513Document62 pages2020 Week 5 Funds 70513Belal HossainNo ratings yet

- Group14 - Section E - Assignement 02Document42 pagesGroup14 - Section E - Assignement 02Back UpNo ratings yet

- CSC Case AnalysisDocument3 pagesCSC Case AnalysisJuhee PritanjaliNo ratings yet

- CDLLife Recommended Budget - $11,000Document2 pagesCDLLife Recommended Budget - $11,000Brian KnightNo ratings yet

- Money Matter$ Pricing For ProfitDocument22 pagesMoney Matter$ Pricing For Profityen yenNo ratings yet

- Grant BudgetDocument6 pagesGrant Budgetapi-354983120No ratings yet

- Social Media Creator Pricing GuideDocument33 pagesSocial Media Creator Pricing GuideDanielNo ratings yet

- Final Business PlanDocument12 pagesFinal Business PlanRalph HumpaNo ratings yet

- Pay Guide - Clerks - Private Sector Award (MA000002) : DisclaimerDocument44 pagesPay Guide - Clerks - Private Sector Award (MA000002) : DisclaimerYasmeen KashifNo ratings yet

- Business Pricing JzelDocument25 pagesBusiness Pricing JzelGina AquinoNo ratings yet

- Quarterly Budget Stauts Review: Task Budget Cost VarianceDocument1 pageQuarterly Budget Stauts Review: Task Budget Cost Variancekamlesh0106No ratings yet

- Team Wakanda PowerPoint Business ProposalDocument11 pagesTeam Wakanda PowerPoint Business ProposalAlNo ratings yet

- Potential IncomeDocument3 pagesPotential IncomedonnacartwrightNo ratings yet

- MindMeister PriceListDocument1 pageMindMeister PriceListNelson ArellanoNo ratings yet

- Tuition Fees MastersDocument4 pagesTuition Fees MastersGaston FouegoNo ratings yet

- Toa 1Document16 pagesToa 1api-347891721No ratings yet

- A Reference Model For Migrating From CMMI-DEV v1.3 To CMMI v2.0Document10 pagesA Reference Model For Migrating From CMMI-DEV v1.3 To CMMI v2.0progisNo ratings yet

- CDMP Study Group: Session 7 - Data Management Capability Maturity ModelsDocument25 pagesCDMP Study Group: Session 7 - Data Management Capability Maturity ModelsprogisNo ratings yet

- Data Maturity Framework - Scorecard QuestionnaireDocument3 pagesData Maturity Framework - Scorecard Questionnaireprogis0% (1)

- Integrating Lean, Six Sigma, and CMMI: David N. CardDocument34 pagesIntegrating Lean, Six Sigma, and CMMI: David N. CardprogisNo ratings yet

- CMMI For Systems Engineers v1.2Document606 pagesCMMI For Systems Engineers v1.2progisNo ratings yet

- Cs 224N Default Final Project: Question Answering On Squad 2.0Document24 pagesCs 224N Default Final Project: Question Answering On Squad 2.0progisNo ratings yet

- Linear Algebraic Structure of Word Senses, With Applications To PolysemyDocument14 pagesLinear Algebraic Structure of Word Senses, With Applications To PolysemyprogisNo ratings yet

- CS 224n Assignment #3: Dependency Parsing: 1. Machine Learning & Neural Networks (8 Points)Document7 pagesCS 224n Assignment #3: Dependency Parsing: 1. Machine Learning & Neural Networks (8 Points)progisNo ratings yet

- Incrementality in Deterministic Dependency ParsingDocument8 pagesIncrementality in Deterministic Dependency ParsingprogisNo ratings yet

- CS 224n Assignment #2: Word2vec (43 Points)Document4 pagesCS 224n Assignment #2: Word2vec (43 Points)progisNo ratings yet

- A New Linear Tire Model With Varying Parameters: Moad Kissai, Bruno Monsuez, Adriana Tapus, Didier MartinezDocument9 pagesA New Linear Tire Model With Varying Parameters: Moad Kissai, Bruno Monsuez, Adriana Tapus, Didier MartinezprogisNo ratings yet

- Cs 224N: Assignment #4: 1. Neural Machine Translation With Rnns (45 Points)Document7 pagesCs 224N: Assignment #4: 1. Neural Machine Translation With Rnns (45 Points)progisNo ratings yet

- Globally Normalized Transition-Based Neural NetworksDocument12 pagesGlobally Normalized Transition-Based Neural NetworksprogisNo ratings yet

- 05 - Lesson 3 Safety Frameworks For Self Driving - C1M3L3 - Safety - Frameworks - For - Self Driving PDFDocument24 pages05 - Lesson 3 Safety Frameworks For Self Driving - C1M3L3 - Safety - Frameworks - For - Self Driving PDFprogisNo ratings yet

- Universal Dependencies: A Cross-Linguistic TypologyDocument8 pagesUniversal Dependencies: A Cross-Linguistic TypologyprogisNo ratings yet

- 11 Lesson-6-Vehicle-Actuation C1M4L6 - Vehicle ActuationDocument15 pages11 Lesson-6-Vehicle-Actuation C1M4L6 - Vehicle ActuationprogisNo ratings yet

- 03 Carla-Installation-Guide CARLA Setup Guide Windows x64 PDFDocument22 pages03 Carla-Installation-Guide CARLA Setup Guide Windows x64 PDFprogisNo ratings yet

- 02 - Lesson 1 Supplementary Reading Carla Overview Self Driving Car Simulation - CARLA - An - Open - Urban - Driving - SimulatorDocument16 pages02 - Lesson 1 Supplementary Reading Carla Overview Self Driving Car Simulation - CARLA - An - Open - Urban - Driving - SimulatorprogisNo ratings yet

- 05 Lesson-3-Software-Architecture C1M2L3 - Software Architecture PDFDocument15 pages05 Lesson-3-Software-Architecture C1M2L3 - Software Architecture PDFprogisNo ratings yet

- 07 Lesson-4-Advanced-Steering-Control-Mpc C1M6L4 - Advanced Steering Control MethodsDocument14 pages07 Lesson-4-Advanced-Steering-Control-Mpc C1M6L4 - Advanced Steering Control MethodsprogisNo ratings yet

- 07 Lesson-4-Longitudinal-Vehicle-Modeling C1M4L4 - Longitudinal Vehicle ModelDocument9 pages07 Lesson-4-Longitudinal-Vehicle-Modeling C1M4L4 - Longitudinal Vehicle ModelprogisNo ratings yet

- Hardware Configuration Design: Module 2, Lesson 2Document23 pagesHardware Configuration Design: Module 2, Lesson 2progisNo ratings yet

- Autonomous Automobile Trajectory Tracking For Off-Road Driving: Controller Design, Experimental Validation and RacingDocument6 pagesAutonomous Automobile Trajectory Tracking For Off-Road Driving: Controller Design, Experimental Validation and RacingprogisNo ratings yet

- 03 Lesson-2-The-Kinematic-Bicycle-Model C1M4L2 - The Kinematic Bicycle Model PDFDocument9 pages03 Lesson-2-The-Kinematic-Bicycle-Model C1M4L2 - The Kinematic Bicycle Model PDFprogisNo ratings yet

- Birhan Final Research PaperDocument109 pagesBirhan Final Research PaperyibeltalNo ratings yet

- T10 - Financial Reporting QualityDocument30 pagesT10 - Financial Reporting QualityJhonatan Perez VillanuevaNo ratings yet

- History of Schneider ElectricDocument12 pagesHistory of Schneider ElectricKerin BerlianaNo ratings yet

- Advanced Manufacturing Tutorial AnswersDocument12 pagesAdvanced Manufacturing Tutorial Answerswilfred chipanguraNo ratings yet

- SSRN Id1709011Document30 pagesSSRN Id1709011Cristiana CarvalhoNo ratings yet

- India Ethanol Price 2022 CCEA-02.11.22Document2 pagesIndia Ethanol Price 2022 CCEA-02.11.22SRINIVASAN TNo ratings yet

- Green Buying Behavior Among Mauritian Consumers: Extending The TPB ModelDocument19 pagesGreen Buying Behavior Among Mauritian Consumers: Extending The TPB ModelGlobal Research and Development ServicesNo ratings yet

- Restructuring Notification 09mar2020Document19 pagesRestructuring Notification 09mar2020DAG SS2No ratings yet

- Accounting Information Systems - Yola-170-171Document2 pagesAccounting Information Systems - Yola-170-171dindaNo ratings yet

- Lifebank Microfinance Foundation, Inc. Ikabuhi Microfinance ProgramDocument1 pageLifebank Microfinance Foundation, Inc. Ikabuhi Microfinance ProgramJocelyn JabianNo ratings yet

- GROUP 9 - Case StudyDocument11 pagesGROUP 9 - Case StudyMariella Alexis JavierNo ratings yet

- Notice of RegistrationDocument1 pageNotice of Registrationbra9tee9tini100% (1)

- Presenting Furnito - The Next Generation Odoo Ecommerce Theme For Furniture Industry PDFDocument4 pagesPresenting Furnito - The Next Generation Odoo Ecommerce Theme For Furniture Industry PDFjuanatoNo ratings yet

- Paez Case Study NotesDocument2 pagesPaez Case Study NotessNo ratings yet

- Wedding Planning SystemDocument37 pagesWedding Planning SystemDennySipa50% (6)

- CHG002335304 - Pre-Invoice - Transport of Paper Sales - ImplementationDocument4 pagesCHG002335304 - Pre-Invoice - Transport of Paper Sales - ImplementationcathyNo ratings yet

- Inv 0019Document1 pageInv 0019urkirannandaNo ratings yet

- FM Chapter 3 Devienna Antonetta Sudiarto 201950456Document3 pagesFM Chapter 3 Devienna Antonetta Sudiarto 201950456Devienna AntonettaNo ratings yet

- 2015 EmployerDocument31 pages2015 EmployerJames LaiNo ratings yet

- Loan Amortization Calculator BestDocument11 pagesLoan Amortization Calculator BestHenok mekuriaNo ratings yet

- 240kWpSolarEPCCUPDilimanBidDocs Revised BidBulletinno.1Document211 pages240kWpSolarEPCCUPDilimanBidDocs Revised BidBulletinno.1Jason HallNo ratings yet

- Ra List ReportDocument218 pagesRa List Reportsatish vermaNo ratings yet

- AvocadoDocument3 pagesAvocadonezzaNo ratings yet

- Transportation Freight Trucking and Towing Open MyFlorida BusinessDocument5 pagesTransportation Freight Trucking and Towing Open MyFlorida BusinessalejandrosantizoNo ratings yet

- ENT QuizDocument25 pagesENT QuizSwagy BoyNo ratings yet

- UGRD Schedule 2021 Main Campus Ver 1.4Document48 pagesUGRD Schedule 2021 Main Campus Ver 1.4Ahmed NisarNo ratings yet

- SMS 209 Intro To Finance PDFDocument87 pagesSMS 209 Intro To Finance PDFDvd AdonisNo ratings yet

- Indonesia Jakarta Rental Apartment Q1 2021Document2 pagesIndonesia Jakarta Rental Apartment Q1 2021Grace SaragihNo ratings yet

- Project Management Unit 2 PDFDocument16 pagesProject Management Unit 2 PDFVaibhav MisraNo ratings yet

- Instructions:: Candor Cash Flow SolutionDocument1 pageInstructions:: Candor Cash Flow SolutionPirvuNo ratings yet