You might also like

- EPCA Seminar: Olefins Outlook: 9 October 2020Document13 pagesEPCA Seminar: Olefins Outlook: 9 October 2020Aswin KondapallyNo ratings yet

- LBNL 5119e PDFDocument46 pagesLBNL 5119e PDFIvan StanisavljevicNo ratings yet

- Stock Valuation of PT Sumber Alfaria TrijayaDocument7 pagesStock Valuation of PT Sumber Alfaria TrijayaIqbal MohammadNo ratings yet

- Chart DaysDocument1 pageChart DaysHeather MendoncaNo ratings yet

- Canara Robeco Emerging Equities: February 2018Document25 pagesCanara Robeco Emerging Equities: February 2018gowtham1993eeeNo ratings yet

- Drainase Dan Sanitasi: Kelompok 4 Kelas BDocument25 pagesDrainase Dan Sanitasi: Kelompok 4 Kelas BDimas AzhariNo ratings yet

- Electric Utility Industry 101: WebinarDocument32 pagesElectric Utility Industry 101: WebinarTechnical karanNo ratings yet

- Highlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldDocument19 pagesHighlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldkaiselkNo ratings yet

- Chart PricesDocument1 pageChart PricesHeather MendoncaNo ratings yet

- Atlanta TieredDocument1 pageAtlanta Tieredkettle1No ratings yet

- Aluminium Warehousing, Premiums and PricesDocument11 pagesAluminium Warehousing, Premiums and Pricesfiki arifNo ratings yet

- Chit Fund1Document2 pagesChit Fund1191061No ratings yet

- Commodity Chartbook: April 6, 2011Document8 pagesCommodity Chartbook: April 6, 2011andrewbloggerNo ratings yet

- Assumption and Data Sources:: Kettle1 ResearchDocument5 pagesAssumption and Data Sources:: Kettle1 Researchkettle1No ratings yet

- Chart PendingsDocument1 pageChart PendingsHeather MendoncaNo ratings yet

- Gantt Chart 17Document1 pageGantt Chart 17Bharti KashyapNo ratings yet

- Forum 8 - 14 April 2020Document3 pagesForum 8 - 14 April 2020patrianaaaNo ratings yet

- Liquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLDocument26 pagesLiquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLbadaberaNo ratings yet

- Equity Value: Date Observation Equity Value K-Ratio 1996 3.560552754 K-Ratio 2003 0.356055275 K-Ratio 2013 5.65220227Document4 pagesEquity Value: Date Observation Equity Value K-Ratio 1996 3.560552754 K-Ratio 2003 0.356055275 K-Ratio 2013 5.65220227Anonymous 5mSMeP2jNo ratings yet

- BalanceDocument1 pageBalanceapi-388936285No ratings yet

- Short and Medium Term OutlookDocument6 pagesShort and Medium Term OutlookTushar LanjekarNo ratings yet

- Svetlana SkapoularosDocument2 pagesSvetlana SkapoularoscyhomeNo ratings yet

- Precious Metals Weekly - 09 de JulioDocument24 pagesPrecious Metals Weekly - 09 de JulioMilton PaibaNo ratings yet

- Netra Early Warnings Signals Through Charts - Dec 2022Document19 pagesNetra Early Warnings Signals Through Charts - Dec 2022rashmi nandaNo ratings yet

- Índice de Tipo de Cambio Real Bilateral Por País - MensualDocument40 pagesÍndice de Tipo de Cambio Real Bilateral Por País - MensualHaydee BahamondeNo ratings yet

- Aircel Mobile TrendsDocument9 pagesAircel Mobile Trendsvikramv4uNo ratings yet

- Oleochemical Outlook Conference Highlights Changing Industry TrendsDocument14 pagesOleochemical Outlook Conference Highlights Changing Industry TrendsJessicalba LouNo ratings yet

- Montgomery County Maryland, August 2010 Market StatisticsDocument1 pageMontgomery County Maryland, August 2010 Market StatisticsJosette SkillingNo ratings yet

- PH Kingdom: Shopee Blibli Jakmall JD Id Lazada Tangga L Tokope DIA Bukala PAK Total OrderDocument8 pagesPH Kingdom: Shopee Blibli Jakmall JD Id Lazada Tangga L Tokope DIA Bukala PAK Total OrderdeeyondNo ratings yet

- Lanvyl TubesDocument5 pagesLanvyl TubesIshmeet SinghNo ratings yet

- Philippine Money Supply M1 (2012-2016) : Currency in Circulation Demand Deposits Total M1Document5 pagesPhilippine Money Supply M1 (2012-2016) : Currency in Circulation Demand Deposits Total M1mirika3shirinNo ratings yet

- Some Graphics About The Border and Migration: Download This As A PDF From Bit - Ly/wola - BorderDocument55 pagesSome Graphics About The Border and Migration: Download This As A PDF From Bit - Ly/wola - BorderJose Octavio Llopis HernandezNo ratings yet

- Pone - Atlas Copco Compressor 01 Accomp01 - 22V Comp Shaft 2 Ob Vertical 0.8 Max Amp .76Document1 pagePone - Atlas Copco Compressor 01 Accomp01 - 22V Comp Shaft 2 Ob Vertical 0.8 Max Amp .76Carlos MNo ratings yet

- SEB Report: Commodity Prices To Rise in Fourth QuarterDocument20 pagesSEB Report: Commodity Prices To Rise in Fourth QuarterSEB GroupNo ratings yet

- Business Fin Final StatsDocument14 pagesBusiness Fin Final StatsVarun SinghalNo ratings yet

- Company Info: Acquisition Date - July 31, 2008: MTD QTD YTD MTD MTD MTDDocument1 pageCompany Info: Acquisition Date - July 31, 2008: MTD QTD YTD MTD MTD MTDKeshav KandalaNo ratings yet

- Reksa Dana Principal ITB-Niaga: Pendapatan Tetap Fund Fact Sheet 30-Jun-2021Document1 pageReksa Dana Principal ITB-Niaga: Pendapatan Tetap Fund Fact Sheet 30-Jun-2021DporiesNo ratings yet

- Penaikan Harga BBM,: Menyempurnakan Liberalisasi Sektor MigasDocument18 pagesPenaikan Harga BBM,: Menyempurnakan Liberalisasi Sektor MigasAfandi WeNo ratings yet

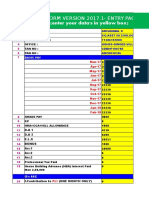

- Aitp - It Form Version 2017.1 - OriginalDocument15 pagesAitp - It Form Version 2017.1 - OriginalGuna SeelanNo ratings yet

- Mwo 121010Document10 pagesMwo 121010richardck50No ratings yet

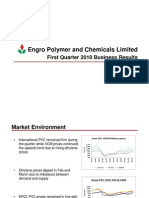

- 1Q 2010 Business ResultsDocument11 pages1Q 2010 Business ResultsmagicsohailNo ratings yet

- Long-term treasury investing amid potential inflationary pressuresDocument5 pagesLong-term treasury investing amid potential inflationary pressuresKamran BayramovNo ratings yet

- Wbs Arrear Calculator (ROPA 2009) (Revised)Document2 pagesWbs Arrear Calculator (ROPA 2009) (Revised)arup_maiti4241100% (2)

- 2T Loss AnalysisDocument15 pages2T Loss AnalysisBenson KarimiNo ratings yet

- 7.joko PrasetyoDocument1 page7.joko PrasetyoJoko PrasetyoNo ratings yet

- Hondacivic ArDocument2 pagesHondacivic Arapi-3709675No ratings yet

- Leave Card FormatDocument2 pagesLeave Card FormatNing NingNo ratings yet

- Unemployment DataDocument2 pagesUnemployment Datakettle1No ratings yet

- (45.1) Programa de Produccion Planta Villahermosa Semana 45 Del 6 Nov Al 12 NovDocument4 pages(45.1) Programa de Produccion Planta Villahermosa Semana 45 Del 6 Nov Al 12 Novvictor.ariasNo ratings yet

- Weekly Epi Update 28Document33 pagesWeekly Epi Update 28Arvind AthavaleNo ratings yet

- Pavimentación en Zona de Vias de Acceso Y Estacionamiento Taller de Mantenim. Curva AvanceDocument2 pagesPavimentación en Zona de Vias de Acceso Y Estacionamiento Taller de Mantenim. Curva AvanceVictor Pablo Cantaro MelgarejoNo ratings yet

- Commodity Chartbook 20101028Document8 pagesCommodity Chartbook 20101028andrewbloggerNo ratings yet

- Loan E.M.I. Calculator: Data To EnterDocument10 pagesLoan E.M.I. Calculator: Data To EnterNanjunda SwamyNo ratings yet

- AC 2011 ES Dec-May11Document2 pagesAC 2011 ES Dec-May11Sv NikhilNo ratings yet

- DNB Land-Based Farming 2017Document11 pagesDNB Land-Based Farming 2017Robertas KupstasNo ratings yet

- Sound of Snow Falling Theme Song LyricsDocument1 pageSound of Snow Falling Theme Song LyricseyaoNo ratings yet

- Winner AnnouncementDocument15 pagesWinner AnnouncementeyaoNo ratings yet

- Combo Set Menu Ax3mb2Document1 pageCombo Set Menu Ax3mb2eyaoNo ratings yet

- WearRAcon 2020 Submission ProposalDocument5 pagesWearRAcon 2020 Submission ProposaleyaoNo ratings yet

- The Top 50 Countries With The Largest Share of Older PopulationDocument2 pagesThe Top 50 Countries With The Largest Share of Older PopulationeyaoNo ratings yet

- What Sector To Invest in ChinaDocument3 pagesWhat Sector To Invest in ChinaeyaoNo ratings yet

- Efficient Portfolios in Excel Using The Solver and Matrix AlgebraDocument16 pagesEfficient Portfolios in Excel Using The Solver and Matrix AlgebraShubham MittalNo ratings yet

- CE Policy Address 2020Document88 pagesCE Policy Address 2020eyaoNo ratings yet

- Population Reference Bureau Annual-Report-2019Document10 pagesPopulation Reference Bureau Annual-Report-2019eyaoNo ratings yet

- The Top 50 With The Largest Number of Older AdultsDocument2 pagesThe Top 50 With The Largest Number of Older AdultseyaoNo ratings yet

- Water Pipe Robot With Soft Inflatable ActuatorsDocument7 pagesWater Pipe Robot With Soft Inflatable ActuatorseyaoNo ratings yet

- August Lock Installation ManualDocument12 pagesAugust Lock Installation ManualeyaoNo ratings yet

- OCDE - Health at A Glance 2019 - 4dd50c09-En PDFDocument243 pagesOCDE - Health at A Glance 2019 - 4dd50c09-En PDFJosé Anselmo de Carvalho JúniorNo ratings yet

- Top 50 Countries With The Largest Percentage of Older PopulationDocument4 pagesTop 50 Countries With The Largest Percentage of Older PopulationAlina PilipenkoNo ratings yet

- ICRA 2019 Design of A Soft Ankle Foot Orthosis Exosuit For Foot Drop AssistanceDocument8 pagesICRA 2019 Design of A Soft Ankle Foot Orthosis Exosuit For Foot Drop AssistanceeyaoNo ratings yet

- Homesound: Real-Time Audio Event Detection Based On High Performance Computing For Behaviour and Surveillance Remote MonitoringDocument22 pagesHomesound: Real-Time Audio Event Detection Based On High Performance Computing For Behaviour and Surveillance Remote MonitoringMochammad SofyanNo ratings yet

- ILO Domestic Worker ReportDocument13 pagesILO Domestic Worker ReporteyaoNo ratings yet

- Ballistocardiography and SensorsDocument19 pagesBallistocardiography and SensorseyaoNo ratings yet

- Audio-Based Assessment of CoughDocument11 pagesAudio-Based Assessment of CougheyaoNo ratings yet

- AI-Smartphone App 'Listens' To Cough To Diagnose DiseaseDocument2 pagesAI-Smartphone App 'Listens' To Cough To Diagnose DiseaseeyaoNo ratings yet

- August Lock Installation GuideDocument18 pagesAugust Lock Installation GuideeyaoNo ratings yet

- August Lock Installation Guide PDFDocument18 pagesAugust Lock Installation Guide PDFeyaoNo ratings yet

- A Novel Soft Elbow ExosuitDocument8 pagesA Novel Soft Elbow Exosuiteyao100% (1)

- World Population AgeingDocument46 pagesWorld Population Ageinggts07No ratings yet

- Blockchains Occam Problem PDFDocument7 pagesBlockchains Occam Problem PDFAlejandroHerreraGurideChileNo ratings yet

- August Lock SpecsDocument4 pagesAugust Lock SpecseyaoNo ratings yet

- Aging in PlaceDocument13 pagesAging in PlaceeyaoNo ratings yet

- 52 Useful Products For Independent Elderly Living Alone - Hobbr PDFDocument38 pages52 Useful Products For Independent Elderly Living Alone - Hobbr PDFeyaoNo ratings yet

- Continuously updated list of deadbolt locksDocument4 pagesContinuously updated list of deadbolt lockseyaoNo ratings yet

- August Lock Installation ManualDocument12 pagesAugust Lock Installation ManualeyaoNo ratings yet

- Instruction: Round Your Answers For Average Product of Capital and Average Product of Labor To 2Document17 pagesInstruction: Round Your Answers For Average Product of Capital and Average Product of Labor To 2Fachrizal AnshoriNo ratings yet

- ESG IT Architecture DeloitteDocument33 pagesESG IT Architecture Deloittecarlos.marino-godayNo ratings yet

- Uk Water Bill P5Document1 pageUk Water Bill P5Yu FengNo ratings yet

- Prueba Analytics TEST (CSat)Document32 pagesPrueba Analytics TEST (CSat)Karlos VergaraNo ratings yet

- Erp Receipt ReverseDocument15 pagesErp Receipt ReversesureshNo ratings yet

- CHAPTER ONE - Entrepreneurship and Free Enterprise: Prepared By: Enanu Tesfaw 1Document56 pagesCHAPTER ONE - Entrepreneurship and Free Enterprise: Prepared By: Enanu Tesfaw 1Mehari TemesgenNo ratings yet

- CAC1107200904 Accounting IADocument6 pagesCAC1107200904 Accounting IAGift MoyoNo ratings yet

- Philippine Accounting Standard 2Document20 pagesPhilippine Accounting Standard 2Jhon Cydric TiosaycoNo ratings yet

- Dissertation Les Restos Du CoeurDocument5 pagesDissertation Les Restos Du CoeurPaperWritingServiceSuperiorpapersOmaha100% (1)

- CFO Director Finance Controller in Toronto ON Canada Resume Yvonne QuDocument3 pagesCFO Director Finance Controller in Toronto ON Canada Resume Yvonne QuYvonneQuNo ratings yet

- Audit and Assurance June 2009 Past Paper (Question)Document6 pagesAudit and Assurance June 2009 Past Paper (Question)Serena JainarainNo ratings yet

- Auditing and Assurance - HonoursDocument2 pagesAuditing and Assurance - HonoursVardaan JaiswalNo ratings yet

- TTI Company Profile 2022Document9 pagesTTI Company Profile 2022michael thomasNo ratings yet

- PPL Brokers Setup and Usage: April 2020Document24 pagesPPL Brokers Setup and Usage: April 2020saxobobNo ratings yet

- Case Study Lawn CareDocument3 pagesCase Study Lawn CareRyan Coloma100% (1)

- Dasari Pavan KumarDocument5 pagesDasari Pavan KumarSandeep KoyyaNo ratings yet

- Sample List of Quality of ObjectivesDocument1 pageSample List of Quality of Objectivessolasmarine60% (5)

- NQA ISO 45001 Implementation GuideDocument36 pagesNQA ISO 45001 Implementation GuideSubhi El Haj Saleh100% (5)

- ADM 4341 - Internal Auditing HandoutDocument17 pagesADM 4341 - Internal Auditing HandoutSarah SivanesanNo ratings yet

- 5478 18339 1 PBDocument23 pages5478 18339 1 PBYusuf MuhammadNo ratings yet

- Henkel GRI 2019-Sustainability-ReportDocument194 pagesHenkel GRI 2019-Sustainability-ReportAlejandro GarciaNo ratings yet

- ZONE 15 - Super Markets & GroceryDocument2 pagesZONE 15 - Super Markets & GroceryDeepak SaravananNo ratings yet

- Dessler Hrm15 Inppt 03Document41 pagesDessler Hrm15 Inppt 03Noha MohNo ratings yet

- Abm 501 NotesDocument3 pagesAbm 501 NotesLeodian Diadem MercurioNo ratings yet

- Analyzing transactional processes and costs in supply chainsDocument2 pagesAnalyzing transactional processes and costs in supply chainsYvonne Ng Ming HuiNo ratings yet

- ProductDocument65 pagesProductSUMITNo ratings yet

- Terry Harris USADocument45 pagesTerry Harris USAAlex Astuhuaman100% (2)

- Unit I BA 26 Operations ManagementDocument47 pagesUnit I BA 26 Operations ManagementJade Berlyn AgcaoiliNo ratings yet

- Key Tips & Takeaways For GDPR Implementation Using COBIT 5Document2 pagesKey Tips & Takeaways For GDPR Implementation Using COBIT 5Atila TiniNo ratings yet

- Audit AR Aging Reports & InvoicesDocument2 pagesAudit AR Aging Reports & InvoicesAbhijith BalachandranNo ratings yet