You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- An Analysis of Delta Air Lines - Based OnDocument5 pagesAn Analysis of Delta Air Lines - Based OnYan FengNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Restored Republic Via A GCR 11 23 2022Document8 pagesRestored Republic Via A GCR 11 23 2022小田 和弘No ratings yet

- Corporate Liquidation 1.) Quinte Company Has Become Insolvent and A Statement of Affairs Is Being Prepared. The FollowingDocument29 pagesCorporate Liquidation 1.) Quinte Company Has Become Insolvent and A Statement of Affairs Is Being Prepared. The Followingreno100% (5)

- GENERAL INSTRUCTIONS: Shade The Letter ThatDocument9 pagesGENERAL INSTRUCTIONS: Shade The Letter ThatrenoNo ratings yet

- Office of The Punong BarangayDocument2 pagesOffice of The Punong BarangayIrismae Sobrevega100% (2)

- C. A Secured Claim of P450,000 and An Unsecured Claim of P50,000Document8 pagesC. A Secured Claim of P450,000 and An Unsecured Claim of P50,000renoNo ratings yet

- A Project Report On Group InsuranceDocument64 pagesA Project Report On Group Insurancesharinair1393% (15)

- The Balance Sheet and Notes To The Financial Statements: HapterDocument38 pagesThe Balance Sheet and Notes To The Financial Statements: Hapterreno100% (1)

- de Barretto vs. Villanueva.Document2 pagesde Barretto vs. Villanueva.Rain HofileñaNo ratings yet

- Quiz 1Document2 pagesQuiz 1renoNo ratings yet

- Sets (Sol)Document4 pagesSets (Sol)renoNo ratings yet

- Week 2 Research DesignDocument33 pagesWeek 2 Research DesignrenoNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- Problem 1: Rizal Review CenterDocument6 pagesProblem 1: Rizal Review CenterrenoNo ratings yet

- Auditing Theory and Principles Thanks GuysDocument51 pagesAuditing Theory and Principles Thanks GuysrenoNo ratings yet

- Auditing Theory and Principles Thanks GuysDocument51 pagesAuditing Theory and Principles Thanks GuysrenoNo ratings yet

- Local Media6699498234507278299Document10 pagesLocal Media6699498234507278299renoNo ratings yet

- A. Hypotheses: (Ho and H1) : Scoretm Sum of Squares DF Mean Square F SigDocument4 pagesA. Hypotheses: (Ho and H1) : Scoretm Sum of Squares DF Mean Square F SigrenoNo ratings yet

- Theory of Account About AuditDocument2 pagesTheory of Account About AuditrenoNo ratings yet

- 12Document1 page12renoNo ratings yet

- Review of Related Literature and Studies Related Study (Foreign)Document10 pagesReview of Related Literature and Studies Related Study (Foreign)renoNo ratings yet

- State Your Problem in A Declarative Form, Be Specific So That The Scope of Your Study Will Be DeterminedDocument4 pagesState Your Problem in A Declarative Form, Be Specific So That The Scope of Your Study Will Be DeterminedrenoNo ratings yet

- AccountingDocument10 pagesAccountingrenoNo ratings yet

- AccDocument4 pagesAccrenoNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- AccountingDocument3 pagesAccountingrenoNo ratings yet

- Hacof Company Profile 2021 Revised 8Document12 pagesHacof Company Profile 2021 Revised 8Ahmed HanadNo ratings yet

- Summary Of: The Value of Saving A Life: Evidence From The Labor MarketDocument2 pagesSummary Of: The Value of Saving A Life: Evidence From The Labor MarketFreed DragsNo ratings yet

- BIOMED Case StudyDocument3 pagesBIOMED Case StudyGanesh BirleNo ratings yet

- UntitledDocument9 pagesUntitledRexi Chynna Maning - AlcalaNo ratings yet

- Unit-1 IhrmDocument25 pagesUnit-1 IhrmAshish mishraNo ratings yet

- Recruitment Case StudyDocument12 pagesRecruitment Case Studyarchangelkhel100% (1)

- SR - No. Security - Name Isin Scrip - ID Intraday Stock ListDocument10 pagesSR - No. Security - Name Isin Scrip - ID Intraday Stock ListSashang S VNo ratings yet

- C-23 FinalDocument3 pagesC-23 FinalAdityaVikramVermaNo ratings yet

- Managerial Economics-CasesDocument3 pagesManagerial Economics-Casessherryl caoNo ratings yet

- Ims HandoutDocument5 pagesIms HandoutDon Mcarthney Tugaoen100% (1)

- Case Study - Industrial LawDocument4 pagesCase Study - Industrial LawNurul Ain Mohd FauziNo ratings yet

- Sci PDF 1710857465640Document65 pagesSci PDF 1710857465640kasarmama7No ratings yet

- CHP 3 Insurer Ownership, Financial & - Operational StructureDocument24 pagesCHP 3 Insurer Ownership, Financial & - Operational StructureIskandar Zulkarnain Kamalluddin100% (1)

- News Release INDY Result 6M22Document7 pagesNews Release INDY Result 6M22Rama Usaha MandiriNo ratings yet

- Report FM FinalDocument31 pagesReport FM FinalSaif JillaniNo ratings yet

- Sample SOP - Global Business ManagementDocument2 pagesSample SOP - Global Business Managementsop247.comNo ratings yet

- Aerostructures Supplier Quality Requirements Control of Nonconforming ProductDocument20 pagesAerostructures Supplier Quality Requirements Control of Nonconforming ProductGấu Du CônNo ratings yet

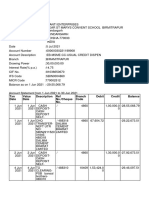

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument7 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaideep MishraNo ratings yet

- JNE Hybrid - PACKING LIST BANG DEDE 13-OKTOBERDocument2 pagesJNE Hybrid - PACKING LIST BANG DEDE 13-OKTOBERFarhan SawieNo ratings yet

- Dream Construction Profile 9.9Document8 pagesDream Construction Profile 9.9virNo ratings yet

- Discount and Finance House of India LTD (DFHI)Document4 pagesDiscount and Finance House of India LTD (DFHI)Aditya YadavNo ratings yet

- 6QQMN331 Sample Essay 2Document28 pages6QQMN331 Sample Essay 2dance.yards0vNo ratings yet

- Intermediate Accounting 2 (Notes Payable) - Problem 2Document3 pagesIntermediate Accounting 2 (Notes Payable) - Problem 2DM MontefalcoNo ratings yet

- StashFin IntroDocument12 pagesStashFin IntroMohit Garg100% (1)

- Hoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89Document72 pagesHoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89E Frank CorneliusNo ratings yet