You might also like

- Minglana, Mitch T. BSA 201: Activity 5: Rolls-Royce Case (Porter'S Five Forces Analysis)Document2 pagesMinglana, Mitch T. BSA 201: Activity 5: Rolls-Royce Case (Porter'S Five Forces Analysis)Mitch Tokong MinglanaNo ratings yet

- CONSOLIDATED - PROGRAMME-RECEIVABLES-PREPAYMENT-GROUP-5-v2-1Document6 pagesCONSOLIDATED - PROGRAMME-RECEIVABLES-PREPAYMENT-GROUP-5-v2-1Mitch Tokong Minglana0% (1)

- Value Stream Design for Product FamilyDocument5 pagesValue Stream Design for Product FamilyMiljane PerdizoNo ratings yet

- Value Stream Design for Product FamilyDocument5 pagesValue Stream Design for Product FamilyMiljane PerdizoNo ratings yet

- ch01 Accounting in ActionDocument17 pagesch01 Accounting in ActionMạnh Hoàng Phi ĐứcNo ratings yet

- 01 Notes NPO WA For HasanDocument86 pages01 Notes NPO WA For HasanHassan MasoodNo ratings yet

- Annotated BibliographyDocument8 pagesAnnotated Bibliographyapi-285542278No ratings yet

- 11 Chapter III Marketing AspectDocument37 pages11 Chapter III Marketing AspectAzkaliverNo ratings yet

- Statutory Duties of AuditorsDocument1 pageStatutory Duties of AuditorsMitch Tokong MinglanaNo ratings yet

- Consolidated Financial Statement HandoutDocument9 pagesConsolidated Financial Statement HandoutMary Jane BarramedaNo ratings yet

- Prob 5Document1 pageProb 5Mitch Tokong MinglanaNo ratings yet

- Final 2nd MeetingDocument1 pageFinal 2nd MeetingChristopher CristobalNo ratings yet

- MasDocument4 pagesMasYaj CruzadaNo ratings yet

- The Balanced ScorecardDocument8 pagesThe Balanced ScorecardCaleb GetubigNo ratings yet

- P1 Course NotesDocument213 pagesP1 Course NotesJohn Sue Han100% (2)

- Payroll Controls: Expected Payroll Controls Are These in Existence at Sheridan?Document2 pagesPayroll Controls: Expected Payroll Controls Are These in Existence at Sheridan?MarieJoiaNo ratings yet

- Departmental Exam 1 - Attempt Review AAPDocument22 pagesDepartmental Exam 1 - Attempt Review AAPLiberty NovaNo ratings yet

- 10 General Interview QuestionsDocument6 pages10 General Interview QuestionsIvan Jggc - ccNo ratings yet

- Final Visit Inventory AuditDocument7 pagesFinal Visit Inventory Auditjeams vidalNo ratings yet

- Long Assignment - MinglanaDocument1 pageLong Assignment - MinglanaMitch Tokong MinglanaNo ratings yet

- Critical Analysis of Agricultural Development Bank's Financial PerformanceDocument23 pagesCritical Analysis of Agricultural Development Bank's Financial PerformanceDrRam Singh KambojNo ratings yet

- Gerald ResumeDocument6 pagesGerald ResumeGoVenky Infotech HrNo ratings yet

- Merchandising Accounting GuideDocument54 pagesMerchandising Accounting GuideApril SasamNo ratings yet

- Yesuf Research (1) .Docx..bakDocument45 pagesYesuf Research (1) .Docx..bakTesnimNo ratings yet

- Accounting for merchandising businessesDocument37 pagesAccounting for merchandising businessesGaret Julia Marie T.100% (1)

- Accounting For Capital Project FundsDocument8 pagesAccounting For Capital Project FundsMeklit AlemNo ratings yet

- Financial Statements: General Purpose FS: For Users Not in The Position ToDocument3 pagesFinancial Statements: General Purpose FS: For Users Not in The Position ToRoyce DenolanNo ratings yet

- Worksheet For Financial Acc. IDocument5 pagesWorksheet For Financial Acc. IFantay100% (1)

- T Chuma Research Project-McommDocument72 pagesT Chuma Research Project-McommIsaac ChinodaNo ratings yet

- Auditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamDocument10 pagesAuditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamGet BurnNo ratings yet

- Chapter 3Document20 pagesChapter 3abebe kumelaNo ratings yet

- Related PartiesDocument24 pagesRelated PartiesEsther PumihicNo ratings yet

- CostDocument2 pagesCostjeams vidalNo ratings yet

- AIS - Chapter 1 AIS OverviewDocument17 pagesAIS - Chapter 1 AIS OverviewErmias GuragawNo ratings yet

- Past Papers YEAR 3 PDFDocument172 pagesPast Papers YEAR 3 PDFraina mattNo ratings yet

- Facets of Cash ManagementDocument6 pagesFacets of Cash Managementjustin lytanNo ratings yet

- Notes ReceivableDocument10 pagesNotes ReceivableCaila Nicole ReyesNo ratings yet

- Acc 414 International AccountingDocument177 pagesAcc 414 International AccountingEmmanuel AbolajiNo ratings yet

- Fin254 Ch05 NNH TVM UpdatedDocument80 pagesFin254 Ch05 NNH TVM Updatedamir khanNo ratings yet

- Financial Management Training Report 2Document24 pagesFinancial Management Training Report 2Sue AwuondaNo ratings yet

- Introduction To Basic Accounting PrinciplesDocument51 pagesIntroduction To Basic Accounting PrinciplesNicole DizonNo ratings yet

- Erika Co investment property reportingDocument4 pagesErika Co investment property reportingjeams vidalNo ratings yet

- Republic of The Philippines University of Northern Philippines College of Business Administration & Accountancy Vigan CityDocument18 pagesRepublic of The Philippines University of Northern Philippines College of Business Administration & Accountancy Vigan CityFrances Nicole MartinezNo ratings yet

- FAR CPA Exam Practice QuestionsDocument8 pagesFAR CPA Exam Practice QuestionsDarlene JacaNo ratings yet

- Chapter 2 - The Professional Environment of CostDocument26 pagesChapter 2 - The Professional Environment of CostFeliciano, Princess G.No ratings yet

- MBA LECTURE-lecture 1Document160 pagesMBA LECTURE-lecture 1takawira chirimeNo ratings yet

- Local StudiesDocument5 pagesLocal StudiesJohn Mark CleofasNo ratings yet

- Topic 2 Internal AnalysisDocument60 pagesTopic 2 Internal Analysis黄洁宣No ratings yet

- TOA DRILL 3 (Practical Accounting 2)Document14 pagesTOA DRILL 3 (Practical Accounting 2)ROMAR A. PIGANo ratings yet

- Accounting As A SystemDocument34 pagesAccounting As A Systemjulian bakerNo ratings yet

- Case 4Document10 pagesCase 4Kenneth M. GonzalesNo ratings yet

- Corporate Governance Success Stories MENA PDFDocument64 pagesCorporate Governance Success Stories MENA PDFVarsha BhootraNo ratings yet

- The Conceptual Framework For Financial ReportingDocument11 pagesThe Conceptual Framework For Financial ReportingNoella Marie BaronNo ratings yet

- Accountancy Chapter 1Document9 pagesAccountancy Chapter 1Yhale DomiguezNo ratings yet

- Corporate Income TaxDocument24 pagesCorporate Income TaxRIRI RUMAIZHANo ratings yet

- Accounting For VAT in Th... Accounting Center, Inc.Document4 pagesAccounting For VAT in Th... Accounting Center, Inc.Martin EspinosaNo ratings yet

- Chapter 7Document30 pagesChapter 7Banana QNo ratings yet

- 02 Code of Ethics For Professional Accountants in The PhilippinesDocument22 pages02 Code of Ethics For Professional Accountants in The PhilippinesJoevitt Louis DelfinadoNo ratings yet

- Indicators RKPDocument13 pagesIndicators RKPJuvy ParaguyaNo ratings yet

- Accounting Record Keeping Practices in Small and Medium Sized Enterprise's (SME's) in Sri LankaDocument6 pagesAccounting Record Keeping Practices in Small and Medium Sized Enterprise's (SME's) in Sri LankaNiyonzimaNo ratings yet

- Introduction To AisDocument41 pagesIntroduction To AisMarieJoiaNo ratings yet

- Auditing: Page 1 of 8Document8 pagesAuditing: Page 1 of 8jeams vidalNo ratings yet

- AP Ppe Quizzer QDocument28 pagesAP Ppe Quizzer Qkimberly bumanlagNo ratings yet

- Richly Roboca IPPPE ME QuizDocument4 pagesRichly Roboca IPPPE ME Quizjeams vidalNo ratings yet

- Payroll Controls at SheridanDocument2 pagesPayroll Controls at Sheridanjeams vidalNo ratings yet

- Internal Control - Accounts Receivable Credit SalesDocument4 pagesInternal Control - Accounts Receivable Credit Salesjeams vidalNo ratings yet

- Erika Co investment property reportingDocument4 pagesErika Co investment property reportingjeams vidalNo ratings yet

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 pagesA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalNo ratings yet

- Materiality LevelDocument1 pageMateriality Leveljeams vidalNo ratings yet

- QuestionnaireDocument4 pagesQuestionnaireTroisNo ratings yet

- Internal Audit Manual PhilippinesDocument295 pagesInternal Audit Manual PhilippinesAnonymous dtceNuyIFI100% (8)

- Chapter Three: Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument71 pagesChapter Three: Product Costing and Cost Accumulation in A Batch Production Environmentjeams vidalNo ratings yet

- What Is A Cash Flow StatementDocument3 pagesWhat Is A Cash Flow Statementjeams vidalNo ratings yet

- Final Visit Inventory AuditDocument7 pagesFinal Visit Inventory Auditjeams vidalNo ratings yet

- Interim Visit 2Document2 pagesInterim Visit 2jeams vidalNo ratings yet

- Imprest vs Fluctuating Fund AccountingDocument2 pagesImprest vs Fluctuating Fund Accountingjeams vidalNo ratings yet

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 pagesA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalNo ratings yet

- Proof of Cash: Irene Mae C. Guerra, CPADocument17 pagesProof of Cash: Irene Mae C. Guerra, CPAjeams vidalNo ratings yet

- Determinants of Accounting Practices Among Street Food VendorsDocument15 pagesDeterminants of Accounting Practices Among Street Food VendorsShamae AfableNo ratings yet

- Imprest vs Fluctuating Fund AccountingDocument2 pagesImprest vs Fluctuating Fund Accountingjeams vidalNo ratings yet

- Cost Accounting & Control: (Introduction and OverviewDocument16 pagesCost Accounting & Control: (Introduction and Overviewjeams vidalNo ratings yet

- 4 - Accounting For OverheadDocument12 pages4 - Accounting For Overheadjeams vidalNo ratings yet

- Bank Reconciliation: Irene Mae C. Guerra, CPADocument25 pagesBank Reconciliation: Irene Mae C. Guerra, CPAjeams vidalNo ratings yet

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 pagesA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalNo ratings yet

- 2015 Senior Thesis TopicsDocument12 pages2015 Senior Thesis TopicspamelaNo ratings yet

- Assignment: Multimedia Keyboards Comfort Type KeyboardsDocument1 pageAssignment: Multimedia Keyboards Comfort Type Keyboardsjeams vidal0% (2)

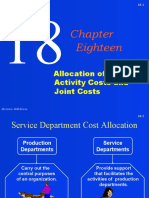

- Eighteen: Allocation of Support Activity Costs and Joint CostsDocument67 pagesEighteen: Allocation of Support Activity Costs and Joint Costsjeams vidalNo ratings yet

- Basic Accountin-WPS OfficeDocument4 pagesBasic Accountin-WPS Officejeams vidalNo ratings yet

- Conceptual Framework: (Underlying Assumptions and Qualitative CharacteristicsDocument25 pagesConceptual Framework: (Underlying Assumptions and Qualitative Characteristicsjeams vidalNo ratings yet

- INA128 INA129: Features DescriptionDocument20 pagesINA128 INA129: Features DescriptionCDDSANo ratings yet

- DataSheet IMA18-10BE1ZC0K 6041793 enDocument8 pagesDataSheet IMA18-10BE1ZC0K 6041793 enRuben Hernandez TrejoNo ratings yet

- Summarised Maths Notes (Neilab Osman)Document37 pagesSummarised Maths Notes (Neilab Osman)dubravko_akmacicNo ratings yet

- Atomic Structure QuestionsDocument1 pageAtomic Structure QuestionsJames MungallNo ratings yet

- Contemporary Issue in StrategyDocument13 pagesContemporary Issue in Strategypatrick wafulaNo ratings yet

- Batt ChargerDocument2 pagesBatt Chargerdjoko witjaksonoNo ratings yet

- 24.ratios, Rates and Proportions PDFDocument9 pages24.ratios, Rates and Proportions PDFMilsonNo ratings yet

- IGNOU MBA MS-11 Solved AssignmentDocument5 pagesIGNOU MBA MS-11 Solved AssignmenttobinsNo ratings yet

- ForwardMails PDFDocument7 pagesForwardMails PDFJesús Ramón Romero EusebioNo ratings yet

- 7 - NIBL - G.R. No. L-15380 Wan V Kim - DigestDocument1 page7 - NIBL - G.R. No. L-15380 Wan V Kim - DigestOjie SantillanNo ratings yet

- PhoneFreedom 365 0 Instalment Postpaid Phone Plan DigiDocument1 pagePhoneFreedom 365 0 Instalment Postpaid Phone Plan DigiJals JNo ratings yet

- USP FriabilityDocument2 pagesUSP Friabilityshdph100% (1)

- Document 25Document455 pagesDocument 25Pcnhs SalNo ratings yet

- Little ThingsDocument3 pagesLittle ThingszwartwerkerijNo ratings yet

- NABARD Dairy Farming Project - PDF - Agriculture - Loans PDFDocument7 pagesNABARD Dairy Farming Project - PDF - Agriculture - Loans PDFshiba prasad panjaNo ratings yet

- 6 Construction of ShoeDocument33 pages6 Construction of ShoevedNo ratings yet

- Creating Literacy Instruction For All Students ResourceDocument25 pagesCreating Literacy Instruction For All Students ResourceNicole RickettsNo ratings yet

- Sunera Best Practices For Remediating SoDsDocument7 pagesSunera Best Practices For Remediating SoDssura anil reddyNo ratings yet

- G7-UNIT - I. (Module - 1 (Week 1 - 3 (Microscopy & Levels of Org.)Document8 pagesG7-UNIT - I. (Module - 1 (Week 1 - 3 (Microscopy & Levels of Org.)Margie Gabo Janoras - DaitolNo ratings yet

- VIP 32 Hybrid VentDocument8 pagesVIP 32 Hybrid VentsagarNo ratings yet

- St. Francis de Sales Sr. Sec. School, Gangapur CityDocument12 pagesSt. Francis de Sales Sr. Sec. School, Gangapur CityArtificial GammerNo ratings yet

- FSRE SS AppendixGlossariesDocument27 pagesFSRE SS AppendixGlossariessachinchem020No ratings yet

- Spare Parts List: WarningDocument5 pagesSpare Parts List: WarningÃbdøū Èqúípmeńť MédîcàlNo ratings yet

- Online Test Series Syllabus Class 10 2019Document6 pagesOnline Test Series Syllabus Class 10 2019ABHISHEK SURYANo ratings yet

- Nelson Climate Change Plan UpdateDocument37 pagesNelson Climate Change Plan UpdateBillMetcalfeNo ratings yet

- Science MELCsDocument42 pagesScience MELCsRanjell Allain TorresNo ratings yet

- PathFit 1 (Lessons)Document10 pagesPathFit 1 (Lessons)Patawaran, Myka R.No ratings yet

- Lecture Euler EquationDocument33 pagesLecture Euler EquationYash RajNo ratings yet

- Internship Report Zannatul Ferdousi Alam YameemDocument51 pagesInternship Report Zannatul Ferdousi Alam YameemZannatul Ferdousi Alam YameemNo ratings yet

- Introduction To Financial Planning Unit 1Document57 pagesIntroduction To Financial Planning Unit 1Joshua GeddamNo ratings yet