You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Research Design: Definition: A Is A Framework or Blueprint For Conducting The Research ProjectDocument22 pagesResearch Design: Definition: A Is A Framework or Blueprint For Conducting The Research Projectvaswati ferdousNo ratings yet

- English in WorkplaceDocument154 pagesEnglish in WorkplacePatrickChanCFNo ratings yet

- C A S E 8 Panera Bread CompanyDocument24 pagesC A S E 8 Panera Bread CompanyMary Ann Melo100% (2)

- Business Continuity Management - BCM - AssessmentDocument93 pagesBusiness Continuity Management - BCM - Assessmentnormatividad teletrabajo100% (1)

- Significance of The StudyDocument2 pagesSignificance of The StudyFhikery Ardiente100% (1)

- Nre Fixed Deposit Plus Non CallableDocument1 pageNre Fixed Deposit Plus Non CallableDhiraj NemadeNo ratings yet

- Ex-Principal Now UPs Most Wanted Woman CriminalDocument2 pagesEx-Principal Now UPs Most Wanted Woman CriminalDhiraj NemadeNo ratings yet

- Frequently Asked Questions: Credit Guarantee Fund For Micro Units (CGFMU)Document4 pagesFrequently Asked Questions: Credit Guarantee Fund For Micro Units (CGFMU)Dhiraj NemadeNo ratings yet

- Not A Single Employee of Zerodha Works With A Revenue Target - CEO - The Hindu BusinessLine PDFDocument5 pagesNot A Single Employee of Zerodha Works With A Revenue Target - CEO - The Hindu BusinessLine PDFDhiraj NemadeNo ratings yet

- Informde de Hallazgos de AuditoriaDocument16 pagesInformde de Hallazgos de AuditoriaEsther Abihgail FlorianNo ratings yet

- Order Reference: SYGHABKEO: Basket Number: 1Document2 pagesOrder Reference: SYGHABKEO: Basket Number: 1GerardBalosbalosNo ratings yet

- ASES - Chapterwise Micro Level Action Plan Closure Summary & TimelineDocument21 pagesASES - Chapterwise Micro Level Action Plan Closure Summary & TimelineAnkit SainiNo ratings yet

- National Standard of The People's Republic of China: Replacing GB 5296.1-1997Document38 pagesNational Standard of The People's Republic of China: Replacing GB 5296.1-1997Hamed DadniaNo ratings yet

- Annexure-I Project Synopsis Format: Name of The Student: Roll No: 11204110154Document1 pageAnnexure-I Project Synopsis Format: Name of The Student: Roll No: 11204110154Seema RahulNo ratings yet

- Milestones Information GreenskyDocument1 pageMilestones Information GreenskyAdam BeilgardNo ratings yet

- RBI Grade B 2018 Phase II ESI Previous Year PaperDocument29 pagesRBI Grade B 2018 Phase II ESI Previous Year PaperParamita HalderNo ratings yet

- Quiz: MMI1060 Fall 2022 Quiz 5 - BondsDocument4 pagesQuiz: MMI1060 Fall 2022 Quiz 5 - BondsxtremewhizNo ratings yet

- Introduction To Finance Casestudy 4 ReportDocument7 pagesIntroduction To Finance Casestudy 4 ReportEnaraNo ratings yet

- Effect of Corporate Governance On Profitability of Quoted Manufacturing Companies in NigeriaDocument14 pagesEffect of Corporate Governance On Profitability of Quoted Manufacturing Companies in NigeriaEditor IJTSRDNo ratings yet

- 41565-Article Text-19911-1-10-20080922Document12 pages41565-Article Text-19911-1-10-20080922oluwasaanu dijiNo ratings yet

- Cambridge Igcse English Coursework Cover SheetDocument8 pagesCambridge Igcse English Coursework Cover Sheetafiwhhioa100% (2)

- November 2022 - QSDocument3 pagesNovember 2022 - QSfareen faridNo ratings yet

- G. Radhakrishnan Sr. Construction Engineer (Civil, Building & Structure) Mobile: - Sultanate of Oman +968 97768759 India +91 9003954578Document7 pagesG. Radhakrishnan Sr. Construction Engineer (Civil, Building & Structure) Mobile: - Sultanate of Oman +968 97768759 India +91 9003954578Vasanthan MohanNo ratings yet

- CHAPTER 2-Fundamentals of Risk ManagementDocument22 pagesCHAPTER 2-Fundamentals of Risk ManagementJerrine Koh0% (1)

- Last Six Months Important One Liner Revision Current Affairs PDFDocument344 pagesLast Six Months Important One Liner Revision Current Affairs PDFvishnu pandeyNo ratings yet

- Work Breakdown Structure TableDocument7 pagesWork Breakdown Structure TableTúy My Thái Chung BCU0432No ratings yet

- LES MEILLEURS TRANSITAIRES ALIBABA - Chine Vers Les Pays de LAfrique Et Dautres Pays Du MondeDocument22 pagesLES MEILLEURS TRANSITAIRES ALIBABA - Chine Vers Les Pays de LAfrique Et Dautres Pays Du Mondemabou5887No ratings yet

- Supply Chain Management 5Th Edition Chopra Test Bank Full Chapter PDFDocument36 pagesSupply Chain Management 5Th Edition Chopra Test Bank Full Chapter PDFedward.kibler915100% (10)

- Campushash: Evolving Business Model of An Entrepreneurial VentureDocument10 pagesCampushash: Evolving Business Model of An Entrepreneurial VentureTanujSood100% (1)

- Lesson 4 - The Steps in The Accounting CycleDocument5 pagesLesson 4 - The Steps in The Accounting Cycleamora elyseNo ratings yet

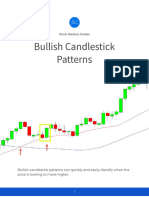

- Bullish Candlestick Patterns ListDocument8 pagesBullish Candlestick Patterns ListjeevandranNo ratings yet

- 2nd Periodical Test MATH11Document2 pages2nd Periodical Test MATH11Jubeth L. EspirituNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePuneet VermaNo ratings yet

- Business Concept Paper (Title)Document6 pagesBusiness Concept Paper (Title)Cristopher Rico DelgadoNo ratings yet