You might also like

- ARIMA Modelling and Forecasting: By: Amar KumarDocument22 pagesARIMA Modelling and Forecasting: By: Amar KumarAmar Kumar100% (1)

- 12 Week A YearDocument9 pages12 Week A YearAmar Kumar67% (3)

- Deep Learning Tutorial: Release 0.1Document137 pagesDeep Learning Tutorial: Release 0.1estraj1954No ratings yet

- Ggplot2 Cheat SheetDocument1 pageGgplot2 Cheat SheetMarcos Vinicius BoscariolNo ratings yet

- Forensic Analysis of GlassDocument17 pagesForensic Analysis of GlassAbrea AbellaNo ratings yet

- 5 6301056647770931988Document133 pages5 6301056647770931988Mradul Dixit100% (1)

- Math g9 WK 3 4 Activity Sheets Regular Spa FinalDocument4 pagesMath g9 WK 3 4 Activity Sheets Regular Spa FinalJeffrey ManligotNo ratings yet

- 7037 The Most Used WordsDocument48 pages7037 The Most Used WordsmalikmobeenNo ratings yet

- 1 - Machine Learning (Start)Document32 pages1 - Machine Learning (Start)Anmol DurgapalNo ratings yet

- Optimization of Welding Process ParameterDocument62 pagesOptimization of Welding Process ParameteraktekshareNo ratings yet

- UdacityCourse Lesson 1 2 3 4Document145 pagesUdacityCourse Lesson 1 2 3 4krishna chaitanya100% (1)

- Anaconda Cheat SheetDocument1 pageAnaconda Cheat SheetBrianNo ratings yet

- Applied Sciences: Improved Yolov5: Efficient Object Detection Using Drone Images Under Various ConditionsDocument16 pagesApplied Sciences: Improved Yolov5: Efficient Object Detection Using Drone Images Under Various ConditionsEd swertNo ratings yet

- Byte of Python PDFDocument129 pagesByte of Python PDFamokNo ratings yet

- Machine Learning Interview GuideDocument41 pagesMachine Learning Interview GuideAnonymous dFIemPqrNo ratings yet

- AI Notes UpdatingDocument95 pagesAI Notes Updatingsmilingeyes_nicNo ratings yet

- Super Cheatsheet Machine LearningDocument15 pagesSuper Cheatsheet Machine LearningAkhil Kandregula100% (1)

- Machine Learning Part 8Document42 pagesMachine Learning Part 8Sujit KumarNo ratings yet

- Machine LearningDocument111 pagesMachine LearningDghddfNo ratings yet

- Description of Nitric Acid Manufacturing ProcessDocument3 pagesDescription of Nitric Acid Manufacturing ProcessSameer PandeyNo ratings yet

- Platinum Group Metals and Compounds: Article No: A21 - 075Document72 pagesPlatinum Group Metals and Compounds: Article No: A21 - 075firda haqiqiNo ratings yet

- Cheatsheets For Deep Learning 1650192034Document95 pagesCheatsheets For Deep Learning 1650192034desdentado30No ratings yet

- GARCH Family of ModelsDocument40 pagesGARCH Family of ModelsDr. Sunita AroraNo ratings yet

- Bernd Klein Python Data Analysis LetterDocument514 pagesBernd Klein Python Data Analysis LetterRajaNo ratings yet

- Simple Linear Regression With An Example Using NumPy - by Arun Ramji Shanmugam - Analytics Vidhya - MediumDocument10 pagesSimple Linear Regression With An Example Using NumPy - by Arun Ramji Shanmugam - Analytics Vidhya - Mediumvojkan73No ratings yet

- Templates: Your Own Sub HeadlineDocument22 pagesTemplates: Your Own Sub HeadlineAmar KumarNo ratings yet

- LSCM: Individual Assignment-Analysis of IBM Global Supply ChainDocument7 pagesLSCM: Individual Assignment-Analysis of IBM Global Supply ChainAmar Kumar100% (1)

- Lec16 - AutoencodersDocument18 pagesLec16 - AutoencodersHoàng Anh NguyễnNo ratings yet

- CS60010: Deep Learning CNN - Part 3: Sudeshna SarkarDocument167 pagesCS60010: Deep Learning CNN - Part 3: Sudeshna SarkarDEEP ROYNo ratings yet

- CNC Programming Tutorials Examples G and M Codes by Thanh TranDocument151 pagesCNC Programming Tutorials Examples G and M Codes by Thanh TranBerkan KılıçNo ratings yet

- Hybrid Electric Propulsion For Military VehiclesDocument84 pagesHybrid Electric Propulsion For Military VehiclesObject477No ratings yet

- QM OverviewDocument16 pagesQM Overviewrvk386No ratings yet

- Machine Learning For Beginners. The Simplified GuideDocument24 pagesMachine Learning For Beginners. The Simplified Guideharish400No ratings yet

- Lesson 5 Deep Neural Net Optimization Tuning InterpretabilityDocument105 pagesLesson 5 Deep Neural Net Optimization Tuning InterpretabilityVIJENDHER REDDY GURRAMNo ratings yet

- Lesson 4 Deep Neural Network and ToolsDocument159 pagesLesson 4 Deep Neural Network and ToolsVIJENDHER REDDY GURRAMNo ratings yet

- Machine Learning Sirs NotesDocument82 pagesMachine Learning Sirs NotesShriganesh BhandariNo ratings yet

- ANL252 StudyGuideDocument382 pagesANL252 StudyGuideShirley LohNo ratings yet

- PytestDocument193 pagesPytestezeNo ratings yet

- SAP Travel Management ..Document23 pagesSAP Travel Management ..Amar Kumar100% (1)

- Cement ChemistryDocument33 pagesCement ChemistryPratap Reddy Vasipalli100% (1)

- Channel PartnerDocument7 pagesChannel PartnerAmar Kumar100% (1)

- Lab Manual For CCNA 3 Instructor VersionDocument262 pagesLab Manual For CCNA 3 Instructor VersionChiefJohnVanderpuije100% (1)

- Image Search Engine Resource GuideDocument15 pagesImage Search Engine Resource Guideishwar12173No ratings yet

- VIP Cheatsheet: Convolutional Neural Networks: Afshine Amidi and Shervine Amidi November 26, 2018Document5 pagesVIP Cheatsheet: Convolutional Neural Networks: Afshine Amidi and Shervine Amidi November 26, 2018Saurabh RaghuvanshiNo ratings yet

- Computer Vision ResourcesDocument7 pagesComputer Vision ResourcesHarsh PatelNo ratings yet

- XG BoostDocument4 pagesXG BoostNur Laili100% (1)

- Python Programming NotesDocument144 pagesPython Programming NotesShan AtrayNo ratings yet

- 6 XG Boost - Jupyter NotebookDocument3 pages6 XG Boost - Jupyter Notebookvenkatesh m100% (1)

- Python For You and Me: Release 0.3.alpha1Document143 pagesPython For You and Me: Release 0.3.alpha1Zafar Ansari100% (1)

- Python Interview QuestionDocument8 pagesPython Interview QuestionSandeep taleNo ratings yet

- PythonDocument209 pagesPythonsekhar sNo ratings yet

- Face Detection & Emotion RecognitionDocument26 pagesFace Detection & Emotion RecognitionNishu TiwariNo ratings yet

- Full Stats NotesDocument126 pagesFull Stats NotesSamantha KarindiraNo ratings yet

- Acceleo User GuideDocument56 pagesAcceleo User GuiderrefusnikNo ratings yet

- MIDTERM EXAM (ICS 461 Artificial Intelligence)Document9 pagesMIDTERM EXAM (ICS 461 Artificial Intelligence)Aya AbdAllah AmmarNo ratings yet

- Assdadasx CC CDocument46 pagesAssdadasx CC CramaNo ratings yet

- Machine LearningDocument118 pagesMachine Learningviswanath kaniNo ratings yet

- Object Oriented ProgrammingDocument11 pagesObject Oriented ProgrammingAli Shana'aNo ratings yet

- Coding AssignmentDocument5 pagesCoding Assignmentanshul goyalNo ratings yet

- 0802 Python TutorialDocument151 pages0802 Python TutorialHamza Aryan100% (1)

- ML Cheatsheet PDFDocument211 pagesML Cheatsheet PDFsatyapb2002100% (1)

- Python For Data ScienceDocument321 pagesPython For Data ScienceAntonio Martín AlcántaraNo ratings yet

- Numpy-User-1 10 1Document107 pagesNumpy-User-1 10 1AliasNo ratings yet

- Lab 1 - 04 October 2018: Machine Learning 2018-2019Document40 pagesLab 1 - 04 October 2018: Machine Learning 2018-2019Asad MuhammadNo ratings yet

- Analysing Ad BudgetDocument4 pagesAnalysing Ad BudgetSrikanth100% (1)

- Artigo NSGA-IIDocument23 pagesArtigo NSGA-IIHoldolf BetrixNo ratings yet

- Adobe Campaign Configuration v6.1 enDocument213 pagesAdobe Campaign Configuration v6.1 enKyeong Jung Kim50% (2)

- CHP 4 IIOTDocument26 pagesCHP 4 IIOTRitesh5No ratings yet

- Testingexperience12 12 10Document124 pagesTestingexperience12 12 10roddiaos100% (1)

- Least Squares Problems: How To State and Solve Them, Then Evaluate Their SolutionsDocument63 pagesLeast Squares Problems: How To State and Solve Them, Then Evaluate Their SolutionsHông Hoa100% (1)

- AOA Analysis of Well Known AlgorithmsDocument29 pagesAOA Analysis of Well Known AlgorithmsBalaji JadhavNo ratings yet

- Cheatsheet Supervised LearningDocument4 pagesCheatsheet Supervised Learningan7l7aNo ratings yet

- Supervised LearningDocument6 pagesSupervised LearninglpNo ratings yet

- CS 229 - Supervised Learning CheatsheetDocument13 pagesCS 229 - Supervised Learning CheatsheettempeuedanNo ratings yet

- VIP Cheatsheet: Unsupervised Learning: Afshine Amidi and Shervine Amidi September 9, 2018Document3 pagesVIP Cheatsheet: Unsupervised Learning: Afshine Amidi and Shervine Amidi September 9, 2018MridulNo ratings yet

- Its About KIDS: Information Summary About Incredible Institute in PanvanDocument13 pagesIts About KIDS: Information Summary About Incredible Institute in PanvanAmar KumarNo ratings yet

- Rotation Shifts - SCNDocument6 pagesRotation Shifts - SCNAmar KumarNo ratings yet

- SAP MSS EHP6 POWL Based Leave Approval Refresh ..Document4 pagesSAP MSS EHP6 POWL Based Leave Approval Refresh ..Amar KumarNo ratings yet

- Random ForestDocument13 pagesRandom ForestAmar KumarNo ratings yet

- EHP 5 New ProcurementiDocument5 pagesEHP 5 New ProcurementimkhicharNo ratings yet

- What Is Data ScienceDocument8 pagesWhat Is Data ScienceAmar KumarNo ratings yet

- Ifsc-Code of Icici Bank Branches in IndiaDocument10,725 pagesIfsc-Code of Icici Bank Branches in IndiaVenkatachalam KolandhasamyNo ratings yet

- SDM Presentation - Sales PotentialDocument6 pagesSDM Presentation - Sales PotentialAmar KumarNo ratings yet

- Glimpse CertificateDocument1 pageGlimpse CertificateAmar KumarNo ratings yet

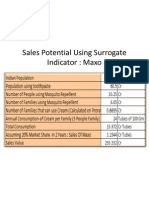

- Sales Potential Using Surrogate Indicator: MaxoDocument1 pageSales Potential Using Surrogate Indicator: MaxoAmar KumarNo ratings yet

- SPIL CaseDocument3 pagesSPIL CaseAmar KumarNo ratings yet

- Amar Kumar G12007 Ruchika GuptaDocument10 pagesAmar Kumar G12007 Ruchika GuptaAmar KumarNo ratings yet

- Bright Engg CompDocument6 pagesBright Engg CompAmar KumarNo ratings yet

- Dell View1Document3 pagesDell View1Pradeep SadasivanNo ratings yet

- Food Chemistry: Wil A.M. Van Loon, Jozef P.H. Linssen, Aagje Legger, Maarten A. Posthumus, Alphons G.J. VoragenDocument9 pagesFood Chemistry: Wil A.M. Van Loon, Jozef P.H. Linssen, Aagje Legger, Maarten A. Posthumus, Alphons G.J. VoragenEcemnur BaşaranNo ratings yet

- Samson Temperature RegulatorDocument6 pagesSamson Temperature RegulatorDai Gia Chan DatNo ratings yet

- A Critical Re-Evaluation of Gideon Toury's Target-Oriented Approach To Translation" PhenomenaDocument156 pagesA Critical Re-Evaluation of Gideon Toury's Target-Oriented Approach To Translation" Phenomenasaeed.mousaviNo ratings yet

- 1.4006 en PDFDocument2 pages1.4006 en PDFdiego.peinado8856No ratings yet

- Gear Box Test SetupDocument20 pagesGear Box Test SetupKarthii AjuNo ratings yet

- Real Analysis Problem SolutionDocument6 pagesReal Analysis Problem SolutionAparajeeta GuhaNo ratings yet

- OOP in C++ - Lecture 5Document11 pagesOOP in C++ - Lecture 5zaibakhan8No ratings yet

- Secondary Education Examination: Grade-SheetDocument1 pageSecondary Education Examination: Grade-SheetSuMit SoMai THapaNo ratings yet

- Cebex 100Document2 pagesCebex 100Riyan Aditya NugrohoNo ratings yet

- 1memo Physics, NmuDocument63 pages1memo Physics, NmuHlulo WyntonNo ratings yet

- Tong TesterDocument10 pagesTong TesterGanesh Kumar Naidu100% (1)

- HackerEarth Maximize Friendship PowerDocument1 pageHackerEarth Maximize Friendship PowerPrinkal GangradeNo ratings yet

- Gottfried Wilhelm LeibnizDocument26 pagesGottfried Wilhelm LeibnizPranesh C NNo ratings yet

- ECE 3125 Communication Engineering II ECE 3242 Digital CommunicationDocument22 pagesECE 3125 Communication Engineering II ECE 3242 Digital CommunicationEng-Ahmed ShabellNo ratings yet

- Sabin's TheoryDocument7 pagesSabin's Theorycatherinepriya100% (3)

- ABT Energy Management SystemDocument4 pagesABT Energy Management SystemAlok GhildiyalNo ratings yet

- BYD TANG Spec SheetDocument4 pagesBYD TANG Spec SheetUberLeBratNo ratings yet

- Year Departure (Millions) Fatal Accidents Fataliies: U.S. Airline Saftey, Scheduled Commercial Carriers, 1985-2006Document9 pagesYear Departure (Millions) Fatal Accidents Fataliies: U.S. Airline Saftey, Scheduled Commercial Carriers, 1985-2006Surendra Singh GaudNo ratings yet

- HP 75 Owner's HandbookDocument348 pagesHP 75 Owner's HandbookjjirwinNo ratings yet

- Memory Management and Tuning Options in Red Hat Enterprise LinuxDocument4 pagesMemory Management and Tuning Options in Red Hat Enterprise LinuxC SanchezNo ratings yet