You might also like

- Corporate Governance: A practical guide for accountantsFrom EverandCorporate Governance: A practical guide for accountantsRating: 5 out of 5 stars5/5 (1)

- ETHICSDocument12 pagesETHICSImranNo ratings yet

- p1 Governance, Risk and EthicsDocument57 pagesp1 Governance, Risk and Ethicsjudyaggrey100% (1)

- Business Finance Summary of ReportDocument8 pagesBusiness Finance Summary of ReportMARL VINCENT L LABITADNo ratings yet

- Corporate Social ResponsibilityDocument7 pagesCorporate Social ResponsibilitydhafNo ratings yet

- Topic 7 Corporate GovernanceDocument12 pagesTopic 7 Corporate Governanceadamskbd100% (1)

- Business Ethics: Assignment OnDocument9 pagesBusiness Ethics: Assignment OnSomesh KumarNo ratings yet

- What Is Corporate GovernanceDocument13 pagesWhat Is Corporate GovernanceReniva KhingNo ratings yet

- Corporate Governance MAINDocument25 pagesCorporate Governance MAINprashantgoruleNo ratings yet

- Module I. Governance and Internal ControlDocument9 pagesModule I. Governance and Internal ControlCleofe Jane PatnubayNo ratings yet

- Presentation On Corporate Governance: BY Group ADocument32 pagesPresentation On Corporate Governance: BY Group AcherrymaniarNo ratings yet

- Good Governance 3Document14 pagesGood Governance 3Gino LiqueNo ratings yet

- BODY (Slide 2) : CindyDocument11 pagesBODY (Slide 2) : CindymichelleNo ratings yet

- Corporate Governance-1Document12 pagesCorporate Governance-1Rahul TWVQU21No ratings yet

- Corporate Governance and CSRDocument31 pagesCorporate Governance and CSRYash SoniNo ratings yet

- Final Project of BRM & FDocument36 pagesFinal Project of BRM & FRamzan IdreesNo ratings yet

- International AccountingDocument4 pagesInternational AccountingJoey WongNo ratings yet

- Corporate GovernanceDocument20 pagesCorporate GovernanceJimbo Manalastas100% (1)

- Corporate NotesDocument89 pagesCorporate NotesDon GordonNo ratings yet

- Acf PresenntationDocument6 pagesAcf PresenntationanjuNo ratings yet

- Business Ethics - SummaryDocument8 pagesBusiness Ethics - SummaryNguyễn HiềnNo ratings yet

- Project On Corporate GovernanceDocument22 pagesProject On Corporate GovernancePallavi PradhanNo ratings yet

- What Is Corporate GovernanceDocument9 pagesWhat Is Corporate GovernanceNitin TembhurnikarNo ratings yet

- Corporate GovernanceDocument6 pagesCorporate GovernanceSatyam KumarNo ratings yet

- Corporate GovernanceDocument32 pagesCorporate GovernanceummarimtiyazNo ratings yet

- External AnswersDocument13 pagesExternal AnswersSurya TejaNo ratings yet

- Aa l3 Ethics F 2176724 S NTBDocument84 pagesAa l3 Ethics F 2176724 S NTBvahobovabdullajon21No ratings yet

- 310 Corporate GovernanceDocument24 pages310 Corporate GovernanceManojNo ratings yet

- Corporate Governance and Business EthicsDocument41 pagesCorporate Governance and Business EthicsMarie GuillermoNo ratings yet

- PIS - Corporate Governance PDFDocument16 pagesPIS - Corporate Governance PDFMohammed FarhanNo ratings yet

- Corporate Governance & Capital Markets: Augustues P. LambinoDocument74 pagesCorporate Governance & Capital Markets: Augustues P. LambinoAnn Gloghienette Orais PerezNo ratings yet

- Corporate Governance - Presentation-12Document53 pagesCorporate Governance - Presentation-12Puneet MittalNo ratings yet

- Discussion QuestionsDocument121 pagesDiscussion QuestionsDnyaneshwar KharatmalNo ratings yet

- Corporate Govenance and Ethical ConsiderationsDocument10 pagesCorporate Govenance and Ethical ConsiderationsCristine Joy AsduloNo ratings yet

- Auditing It Governance ControlsDocument29 pagesAuditing It Governance ControlsJaira MoradaNo ratings yet

- Sample Thesis On Corporate GovernanceDocument7 pagesSample Thesis On Corporate GovernanceWriteMyMathPaperSingapore100% (2)

- Unit - 1 - Conceptual Framework of Corporate GovernanceDocument15 pagesUnit - 1 - Conceptual Framework of Corporate GovernanceRajendra SomvanshiNo ratings yet

- CORPORATE GOVER-WPS OfficeDocument4 pagesCORPORATE GOVER-WPS OfficeMarie Mhel DacapioNo ratings yet

- Corporate Governance - Convictions and RealitiesDocument10 pagesCorporate Governance - Convictions and Realitieskarthik kpNo ratings yet

- Enron Corporation and AndersonDocument14 pagesEnron Corporation and AndersonAzizki WanieNo ratings yet

- 310 Corporate GovernanceDocument37 pages310 Corporate Governancemakrandbhagwat2000No ratings yet

- Lecture 6 - GovernanceDocument36 pagesLecture 6 - GovernanceMahpara FatimaNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate GovernanceVir Ved Ratna Jaipuria LucknowNo ratings yet

- GGSR PrelimDocument102 pagesGGSR PrelimTintin Ruiz0% (2)

- 10 X08 BudgetingDocument36 pages10 X08 Budgetinglalala010899No ratings yet

- Corporate Governance - Unit 1Document24 pagesCorporate Governance - Unit 1Xcill EnzeNo ratings yet

- Corporate Governance Is The System of Rules, Practices and Processes by Which A Company Is Directed and ControlledDocument8 pagesCorporate Governance Is The System of Rules, Practices and Processes by Which A Company Is Directed and ControlledNicefebe Love SampanNo ratings yet

- CSC-AE10-GBERMIC-Module 2Document6 pagesCSC-AE10-GBERMIC-Module 2Marjorie Rose GuarinoNo ratings yet

- Corporate Governance: Acctg 216: Governance, Business Ethics, Risk Management and Internal ControlDocument67 pagesCorporate Governance: Acctg 216: Governance, Business Ethics, Risk Management and Internal ControlGilner PomarNo ratings yet

- Corporate Governance - A Conceptual AnalysisDocument36 pagesCorporate Governance - A Conceptual Analysissameer_kiniNo ratings yet

- 202004181917242491nlbharti CORPORATE GOVERNANCEDocument26 pages202004181917242491nlbharti CORPORATE GOVERNANCEAnurag SinghNo ratings yet

- Corporate Governance and Business EthicsDocument5 pagesCorporate Governance and Business EthicsLamia JabraneNo ratings yet

- Assignment ECGDocument13 pagesAssignment ECGsaitteyNo ratings yet

- Business Ethics Governance and Risk unT2v2WlAhbjDocument4 pagesBusiness Ethics Governance and Risk unT2v2WlAhbjbhawnaNo ratings yet

- Corporte GovernanceDocument13 pagesCorporte GovernanceGaurav KumarNo ratings yet

- Corp. Governance 1Document11 pagesCorp. Governance 1ridhiNo ratings yet

- Corporate Governance in The Phil. Research PaperDocument15 pagesCorporate Governance in The Phil. Research PaperRizel C. Montante0% (1)

- 13 Corporate GovernanceDocument58 pages13 Corporate GovernanceMAE ANNE YAONo ratings yet

- Corporate Governance Value & Ethics Unit-1Document17 pagesCorporate Governance Value & Ethics Unit-1SachinSinghalNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Recruit Select Induct Staff 2Document3 pagesRecruit Select Induct Staff 2raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement A Business Plan1Document2 pagesDevelop and Implement A Business Plan1raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

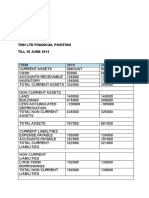

- Manage Finances: TMH LTD Financial Position TILL 30 JUNE 2015Document4 pagesManage Finances: TMH LTD Financial Position TILL 30 JUNE 2015raj ramukNo ratings yet

- Establish and Maintain Whs Safety System1Document46 pagesEstablish and Maintain Whs Safety System1raj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement Marketing Strategies2Document10 pagesDevelop and Implement Marketing Strategies2raj ramukNo ratings yet

- Develop and Implement A Business Plan2Document14 pagesDevelop and Implement A Business Plan2raj ramukNo ratings yet

- Recruit Induct and Select Staff1Document8 pagesRecruit Induct and Select Staff1raj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Develop and Implement Marketing StrategiesDocument8 pagesDevelop and Implement Marketing Strategiesraj ramukNo ratings yet

- Revenue, Expenditure and Capital Investment Proposal/Plan: Manage FinancesDocument25 pagesRevenue, Expenditure and Capital Investment Proposal/Plan: Manage Financesraj ramukNo ratings yet

- Prepare Vegetables, Fruit, Eggs and Farinaceous DishesDocument30 pagesPrepare Vegetables, Fruit, Eggs and Farinaceous Dishesraj ramuk75% (4)

- Prepare Meat DishesDocument20 pagesPrepare Meat Dishesraj ramukNo ratings yet

- Develop and Implement A Business Plan1Document2 pagesDevelop and Implement A Business Plan1raj ramukNo ratings yet

- Develop and Implement A Business Plan2Document14 pagesDevelop and Implement A Business Plan2raj ramukNo ratings yet

- Produce and Serve Food For BuffetsDocument14 pagesProduce and Serve Food For Buffetsraj ramukNo ratings yet

- Manage Finances: TMH LTD Financial Position TILL 30 JUNE 2015Document4 pagesManage Finances: TMH LTD Financial Position TILL 30 JUNE 2015raj ramukNo ratings yet

- Prepare and Present Sandwiches: Answer 1: - (A)Document19 pagesPrepare and Present Sandwiches: Answer 1: - (A)raj ramukNo ratings yet

- 20 April Produce Cakes and Pasteries and BreadsDocument16 pages20 April Produce Cakes and Pasteries and Breadsraj ramuk50% (2)

- c3 Assignment UnknownDocument5 pagesc3 Assignment Unknownraj ramukNo ratings yet

- Prepare Poultry DishesDocument17 pagesPrepare Poultry Dishesraj ramukNo ratings yet

- Prepare Seafood DishesDocument21 pagesPrepare Seafood Dishesraj ramuk100% (1)

- 20 April Final PREPARE MEAT DISHESDocument17 pages20 April Final PREPARE MEAT DISHESraj ramukNo ratings yet

- Asisgnment No 2 PREPARE MEAT DISHESDocument6 pagesAsisgnment No 2 PREPARE MEAT DISHESraj ramuk100% (1)

- Family Law Int 1-19010126126-Kashish JainDocument5 pagesFamily Law Int 1-19010126126-Kashish JainKASHISH JAINNo ratings yet

- Case TheoryDocument3 pagesCase TheoryAichiiko CoversNo ratings yet

- University of Eldoret Human Resource Policies and Procedures ManualDocument128 pagesUniversity of Eldoret Human Resource Policies and Procedures ManualMr.MAXWELL ONYANGONo ratings yet

- B.F. Metal (Corporation) v. LomotanDocument3 pagesB.F. Metal (Corporation) v. LomotanAndrew AmbrayNo ratings yet

- Pil AmbaDocument8 pagesPil AmbaAmba CobbahNo ratings yet

- Re: Applicability of Anti-Dummy Law On Partly-Nationalized ActivitiesDocument4 pagesRe: Applicability of Anti-Dummy Law On Partly-Nationalized ActivitieszelayneNo ratings yet

- The Poisons Act 1919: AnswerDocument3 pagesThe Poisons Act 1919: AnswerHabibur RahmanNo ratings yet

- CHAPTER-1 1.1.: Natural PersonDocument10 pagesCHAPTER-1 1.1.: Natural PersonMaaz AlamNo ratings yet

- Indian Penal Code (IPC Notes) Indian Penal Code (IPC Notes)Document37 pagesIndian Penal Code (IPC Notes) Indian Penal Code (IPC Notes)Swastik GroverNo ratings yet

- Practical Exercise 1.2. Solution Anticipatory BailDocument4 pagesPractical Exercise 1.2. Solution Anticipatory BailAnkush JadaunNo ratings yet

- Title 6 - PD 1563Document11 pagesTitle 6 - PD 1563Mary Jane AsnaniNo ratings yet

- Jail Officer Up To The Rank of Jail Superintendent and Other Law Enforcement Agencies, and Agencies Under The Criminal Justice SystemDocument3 pagesJail Officer Up To The Rank of Jail Superintendent and Other Law Enforcement Agencies, and Agencies Under The Criminal Justice SystembogartsidoNo ratings yet

- Coinsource OH Notice of ChargesDocument3 pagesCoinsource OH Notice of ChargesLKNo ratings yet

- Loloee Request To Seal DocumentsDocument4 pagesLoloee Request To Seal DocumentsKristin LamNo ratings yet

- Garcia V Executive SecDocument2 pagesGarcia V Executive SecAngeline RodriguezNo ratings yet

- CDI 2 PrelimDocument17 pagesCDI 2 PrelimRosa Mae TiburcioNo ratings yet

- Nonimmigrant Visa - Review Security InformationDocument2 pagesNonimmigrant Visa - Review Security InformationVivek SinhaNo ratings yet

- The Exclusive Jurisdiction of Flag States: A Limitation On Pro-Active Port States?Document32 pagesThe Exclusive Jurisdiction of Flag States: A Limitation On Pro-Active Port States?Aimi AzemiNo ratings yet

- Community Service As PunishmentDocument20 pagesCommunity Service As PunishmentLelouchNo ratings yet

- Lorrin FreemanDocument3 pagesLorrin FreemanLorrin Freeman FilesNo ratings yet

- 8) Edigardo v. Bondoc vs. Atty. Olimpio R. DatuDocument1 page8) Edigardo v. Bondoc vs. Atty. Olimpio R. DatuMarco LucmanNo ratings yet

- US vs. ConfradaDocument4 pagesUS vs. ConfradaLorelain ImperialNo ratings yet

- Outline Professional ResponsabilityDocument34 pagesOutline Professional ResponsabilitykyleNo ratings yet

- The Last Homecoming and Trial of RizalDocument1 pageThe Last Homecoming and Trial of RizalrizthieNo ratings yet

- Final ExaminationsDocument29 pagesFinal ExaminationsCharlie SumagaysayNo ratings yet

- Jaypaul V. Cayeux 1954 MR 181Document4 pagesJaypaul V. Cayeux 1954 MR 181Milazar NigelNo ratings yet

- Sub-Decree No. 37 SD.P On Organization and Functioning of Competition Commission of Cambodia (17.02.2022) ENDocument5 pagesSub-Decree No. 37 SD.P On Organization and Functioning of Competition Commission of Cambodia (17.02.2022) ENSenghak DyNo ratings yet

- Mutiny in Marienburg PDFDocument250 pagesMutiny in Marienburg PDFRagamonNo ratings yet

- Industrial Employment Standing Orders Act 1946Document24 pagesIndustrial Employment Standing Orders Act 1946Gaurav Kant50% (2)

- 78 SCRA 470 Republic of The Philippines VS Purisima PDFDocument3 pages78 SCRA 470 Republic of The Philippines VS Purisima PDFRovelyn PamotonganNo ratings yet