You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- H00391794 D31CGDocument10 pagesH00391794 D31CGSanghamithra raviNo ratings yet

- Financial Management Test 2: Answer ALL QuestionsDocument3 pagesFinancial Management Test 2: Answer ALL Questionshemavathy100% (1)

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No ratings yet

- 02 MAS Final Preboard 2018 2019 WITH ANSWER 2 PDFDocument13 pages02 MAS Final Preboard 2018 2019 WITH ANSWER 2 PDFAshNor RandyNo ratings yet

- 02 MAS Final Preboard 2018 2019 WITH ANSWER 2Document13 pages02 MAS Final Preboard 2018 2019 WITH ANSWER 2Jims Leñar CezarNo ratings yet

- Managing Finincial Principles & Techniques Ms - SafinaDocument22 pagesManaging Finincial Principles & Techniques Ms - SafinajojirajaNo ratings yet

- NSE Financial Modeling Exam Questions and Solution - 2Document55 pagesNSE Financial Modeling Exam Questions and Solution - 2rahulnationalite83% (6)

- GP FINNANCEDocument12 pagesGP FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- Advanced Taxation and Strategic Tax Planning PDFDocument11 pagesAdvanced Taxation and Strategic Tax Planning PDFAnuk PereraNo ratings yet

- Revision Questions 2020 Part IVDocument31 pagesRevision Questions 2020 Part IVJeffrey KamNo ratings yet

- Af QP - CFSDocument4 pagesAf QP - CFSaman KumarNo ratings yet

- Simsr2 Mba B III FM Quep 1Document4 pagesSimsr2 Mba B III FM Quep 1Priyanka ReddyNo ratings yet

- NSE Financial Modeling Sample Exam Paper1Document10 pagesNSE Financial Modeling Sample Exam Paper1mkg75080% (5)

- AS 17 Segment ReportingDocument11 pagesAS 17 Segment ReportingNishant Jha Mcom 2No ratings yet

- FM&EconomicsQUESTIONPAPER MAY21Document6 pagesFM&EconomicsQUESTIONPAPER MAY21Harish Palani PalaniNo ratings yet

- Complete Task - Buderim GingerDocument9 pagesComplete Task - Buderim GingerOne OrgNo ratings yet

- Bba A&m 21Document2 pagesBba A&m 21Kundan JhaNo ratings yet

- Institute of Rural Management AnandDocument5 pagesInstitute of Rural Management AnandAmit Kr GodaraNo ratings yet

- Iclean Company Income Statements For 3 Years Ended December 2017, 2018 & 2019Document2 pagesIclean Company Income Statements For 3 Years Ended December 2017, 2018 & 2019Jamie YingNo ratings yet

- Fin 201 Term Paper Group A PDFDocument25 pagesFin 201 Term Paper Group A PDFGopal DeyNo ratings yet

- Afar (2018-2022)Document49 pagesAfar (2018-2022)Princess KeithNo ratings yet

- Exercise Topic 4Document7 pagesExercise Topic 4jr ylvsNo ratings yet

- Accounting 50 Imp Questions 1642414963Document75 pagesAccounting 50 Imp Questions 1642414963vishal kadamNo ratings yet

- IBF FINAL Exam SP 2020 ONLINE BDocument4 pagesIBF FINAL Exam SP 2020 ONLINE BSYED MANSOOR ALI SHAHNo ratings yet

- Mock Exam Paper For Accounting - MBADocument14 pagesMock Exam Paper For Accounting - MBARasanjaliGunasekeraNo ratings yet

- Capital Budgeting TybmsDocument38 pagesCapital Budgeting TybmsKushNo ratings yet

- FM Solved PapersDocument83 pagesFM Solved PapersAjabba87% (15)

- Bbap18011159 Fin 2013 (WM) Financial ManagementDocument8 pagesBbap18011159 Fin 2013 (WM) Financial ManagementRaynold RaphaelNo ratings yet

- Final Exam Cover Sheet: Accounting, Behaviour and Control ACCT3001Document9 pagesFinal Exam Cover Sheet: Accounting, Behaviour and Control ACCT3001Giovanni LinNo ratings yet

- FCES - Damanhour 3 Year - 2 Term: Management AccountingDocument11 pagesFCES - Damanhour 3 Year - 2 Term: Management Accountingahmedgalalali497No ratings yet

- ACC 404 RatiosDocument11 pagesACC 404 RatiosMahmud TuhinNo ratings yet

- Revison Lecture - Q1 Q2Document28 pagesRevison Lecture - Q1 Q2pes60804No ratings yet

- Ap 9401-2 SheDocument6 pagesAp 9401-2 SheLuzviminda SaspaNo ratings yet

- MTE - Spring 2020, Managerial AccountingDocument6 pagesMTE - Spring 2020, Managerial AccountingUTTAM KOIRALANo ratings yet

- Individual Assignment Financial Accounting and Report 1Document7 pagesIndividual Assignment Financial Accounting and Report 1Sahal Cabdi AxmedNo ratings yet

- Muhammad Ilham R - 201650584 - UTSDocument6 pagesMuhammad Ilham R - 201650584 - UTSIvonie NursalimNo ratings yet

- Solution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Document10 pagesSolution Class 12 - Accountancy Half Syllabus: For Admission Contact 1 / 10Shaindra SinghNo ratings yet

- Financial Analysis of Indigo Airlines From Lender's PerspectiveDocument12 pagesFinancial Analysis of Indigo Airlines From Lender's PerspectiveAnil Kumar Reddy100% (1)

- Type Answers On This Side of The Page OnlyDocument40 pagesType Answers On This Side of The Page Only嘉慧No ratings yet

- DepreciationDocument18 pagesDepreciationAhmad Hafiz100% (1)

- Assignment in Intermediateaccounting October 21Document12 pagesAssignment in Intermediateaccounting October 21Monica mangobaNo ratings yet

- Contents of An Interim Financial Report: Unit OverviewDocument5 pagesContents of An Interim Financial Report: Unit OverviewRITZ BROWNNo ratings yet

- Ge02 Model Question - Cma June 2018 - PacademiaDocument6 pagesGe02 Model Question - Cma June 2018 - PacademiaSumon Kumar DasNo ratings yet

- CBCS 3.3.3 Corporate Valuation and Restructuring 2020Document4 pagesCBCS 3.3.3 Corporate Valuation and Restructuring 2020Bharath MNo ratings yet

- BAFB3013 Financial ManagementDocument9 pagesBAFB3013 Financial ManagementSarah ShiphrahNo ratings yet

- Management Accounting - 1Document4 pagesManagement Accounting - 1amaljacobjogilinkedinNo ratings yet

- TIMERRRDocument6 pagesTIMERRRValentina Tan DuNo ratings yet

- Financial Management Paper 2.4 July 2023Document18 pagesFinancial Management Paper 2.4 July 2023johny SahaNo ratings yet

- S A Ipcc Nov 2011 - GR IDocument97 pagesS A Ipcc Nov 2011 - GR ISaibhumi100% (1)

- Final Exam On Accounting For Decision MakingDocument17 pagesFinal Exam On Accounting For Decision MakingSivasakti MarimuthuNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument7 pages© The Institute of Chartered Accountants of IndiaSarvesh JoshiNo ratings yet

- FAC133 FM - Capital Budgeting SumsDocument9 pagesFAC133 FM - Capital Budgeting SumsVedant Vinod MaheshwariNo ratings yet

- Ap 9201-2 SheDocument5 pagesAp 9201-2 SheShefannie PaynanteNo ratings yet

- Practice Questions (Not in Prescribed Textbook)Document7 pagesPractice Questions (Not in Prescribed Textbook)ayaNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Dethzaida AsebuqueNo ratings yet

- Profitability Position of Aditya BirlaDocument10 pagesProfitability Position of Aditya BirlaPalmodiNo ratings yet

- Affiliated To Bharathiar University Saravanampatti:: Coimbatore - 641 049Document4 pagesAffiliated To Bharathiar University Saravanampatti:: Coimbatore - 641 049Prasanna PNo ratings yet

- KCLAS Cost QPDocument4 pagesKCLAS Cost QPPrasanna PNo ratings yet

- Hit 6 1Document2 pagesHit 6 1Amit GodaraNo ratings yet

- Nabard Internship 2024 1712629456Document6 pagesNabard Internship 2024 1712629456Amit GodaraNo ratings yet

- Ibps Po MainsDocument4 pagesIbps Po MainsAmit GodaraNo ratings yet

- RR29022016Document32 pagesRR29022016Amit GodaraNo ratings yet

- Cold Preservation: Click HereDocument4 pagesCold Preservation: Click HereAmit GodaraNo ratings yet

- Click Here - : Fats & LipidsDocument4 pagesClick Here - : Fats & LipidsAmit GodaraNo ratings yet

- Watershed Development Fund (WDF)Document2 pagesWatershed Development Fund (WDF)anbukgiNo ratings yet

- DM-1 - Lesson 18Document9 pagesDM-1 - Lesson 18Amit GodaraNo ratings yet

- DM-1 - Lesson 12Document9 pagesDM-1 - Lesson 12Amit GodaraNo ratings yet

- Click Here - : EnzymesDocument4 pagesClick Here - : EnzymesAmit GodaraNo ratings yet

- Committee Table Questions Lyst6919Document106 pagesCommittee Table Questions Lyst6919Amit GodaraNo ratings yet

- Finance Commission Report: Anuj JindalDocument13 pagesFinance Commission Report: Anuj JindalAmit GodaraNo ratings yet

- Drying and DehydrationDocument4 pagesDrying and DehydrationAmit GodaraNo ratings yet

- Institute of Rural Management Anand: Mid Term Examination (Open Book)Document4 pagesInstitute of Rural Management Anand: Mid Term Examination (Open Book)Amit GodaraNo ratings yet

- All Committees (Tabular Format) : by - Anuj JindalDocument41 pagesAll Committees (Tabular Format) : by - Anuj JindalAmit GodaraNo ratings yet

- Fundamentals of Microbiology: Lesson 17 Bacterial NutritionDocument10 pagesFundamentals of Microbiology: Lesson 17 Bacterial NutritionAmit GodaraNo ratings yet

- DM-1 - Lesson 20Document10 pagesDM-1 - Lesson 20Amit GodaraNo ratings yet

- DM-1 - Lesson 14Document5 pagesDM-1 - Lesson 14Amit GodaraNo ratings yet

- DM-1 - Lesson 16Document11 pagesDM-1 - Lesson 16Amit GodaraNo ratings yet

- DM-1 - Lesson 10Document4 pagesDM-1 - Lesson 10Amit GodaraNo ratings yet

- DM-1 - Lesson 13Document5 pagesDM-1 - Lesson 13Amit GodaraNo ratings yet

- DM-1 - Lesson 15Document11 pagesDM-1 - Lesson 15Amit GodaraNo ratings yet

- DM-1 - Lesson 11Document10 pagesDM-1 - Lesson 11Amit GodaraNo ratings yet

- DM-1 - Lesson 5Document5 pagesDM-1 - Lesson 5Amit GodaraNo ratings yet

- DM-1 - Lesson 4Document8 pagesDM-1 - Lesson 4Amit GodaraNo ratings yet

- DM-1 - Lesson 8Document3 pagesDM-1 - Lesson 8Amit GodaraNo ratings yet

- DM-1 - Lesson 7Document6 pagesDM-1 - Lesson 7Amit GodaraNo ratings yet

- DM-1 - Lesson 9Document3 pagesDM-1 - Lesson 9Amit GodaraNo ratings yet

- DM-1 - Lesson 6Document8 pagesDM-1 - Lesson 6Amit GodaraNo ratings yet

- DM-1 - Lesson 3Document5 pagesDM-1 - Lesson 3Amit GodaraNo ratings yet

- Guide Specifications For Design and Construction of Segmental Concrete BridgesDocument105 pagesGuide Specifications For Design and Construction of Segmental Concrete Bridgessarjumulmi100% (4)

- Mg2451 Engineering Economics and Cost Analysis Unit I Introduction To EconomicsDocument36 pagesMg2451 Engineering Economics and Cost Analysis Unit I Introduction To EconomicsSrinivasNo ratings yet

- Hotels-Africa-2018-Knight FrankDocument7 pagesHotels-Africa-2018-Knight FrankafadigaNo ratings yet

- The Communist Manifesto BOOK REVIEWDocument5 pagesThe Communist Manifesto BOOK REVIEWSwati AnandNo ratings yet

- STR 052 04 JR2 GA20 ModelDocument1 pageSTR 052 04 JR2 GA20 ModelSigit PurnomoNo ratings yet

- Market StructureDocument4 pagesMarket StructurePranjal TiwariNo ratings yet

- Module 7 MANAGEMENT OF FOREIGN OPERATIONS AND INTERNATIONAL TRADE PDFDocument7 pagesModule 7 MANAGEMENT OF FOREIGN OPERATIONS AND INTERNATIONAL TRADE PDFRica SolanoNo ratings yet

- EE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsDocument20 pagesEE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsVindula LakshaniNo ratings yet

- Theory of ProductionDocument17 pagesTheory of Productionpraveenpatidar269No ratings yet

- PAS 34 Interim Financial Reporting: Learning ObjectivesDocument5 pagesPAS 34 Interim Financial Reporting: Learning ObjectivesFhrince Carl CalaquianNo ratings yet

- Does CEMEX Have A Global AdvantageDocument3 pagesDoes CEMEX Have A Global AdvantageCarla Mairal MurNo ratings yet

- ss30-1 Ri2 ch5 Communism As A Rejection of Liberalism 2014Document22 pagesss30-1 Ri2 ch5 Communism As A Rejection of Liberalism 2014api-263969748No ratings yet

- Savanorystė Lietuvoje - Socialinio Kapitalo Perspektyva: Justinas StaliūnasDocument12 pagesSavanorystė Lietuvoje - Socialinio Kapitalo Perspektyva: Justinas StaliūnasDarius DociusNo ratings yet

- NPSL Invoice 40% of Contract Value On Delivery of TR For Fire Water LineDocument7 pagesNPSL Invoice 40% of Contract Value On Delivery of TR For Fire Water LineAbuAbdullah KhanNo ratings yet

- Supply Chain Mumbai DabbawalasDocument14 pagesSupply Chain Mumbai DabbawalasShiv Deep Sharma 20mmb087No ratings yet

- The Determinants of Banks' Profits in Greece During The Period of EU Financial IntegrationDocument4 pagesThe Determinants of Banks' Profits in Greece During The Period of EU Financial IntegrationHaroon KhanNo ratings yet

- Activity 5 Unit 3 Importanc of THR Oil - 125545 PDFDocument2 pagesActivity 5 Unit 3 Importanc of THR Oil - 125545 PDFJimmy Ricardo Moo GüemezNo ratings yet

- PDF Applied Economics Module 4Document34 pagesPDF Applied Economics Module 4Raiza CabreraNo ratings yet

- Topic 2-Economics ModelsDocument17 pagesTopic 2-Economics ModelsAbid RanaNo ratings yet

- جديد كبارى-1 LRFDDocument35 pagesجديد كبارى-1 LRFDamaary31No ratings yet

- UAE VAT Dual Currency Invoice Template 1Document4 pagesUAE VAT Dual Currency Invoice Template 1Vijay Kumar Reddy ChallaNo ratings yet

- Invoice 4325298377Document1 pageInvoice 4325298377Vikash GuptaNo ratings yet

- Sosc Credit CardsDocument2 pagesSosc Credit CardsPersonal Finance GyanNo ratings yet

- TDS8 TH ScheduleDocument1 pageTDS8 TH ScheduleKumarNo ratings yet

- Presentation ATR 72-500Document13 pagesPresentation ATR 72-500Naveed AhmadNo ratings yet

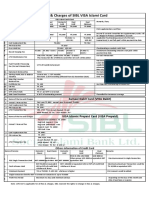

- Fees and Charges of SIBL Islami CardDocument1 pageFees and Charges of SIBL Islami CardMd YusufNo ratings yet

- Hni 72Document1 pageHni 72Arsh AhmadNo ratings yet

- Zava Sifu Le Nine ManDocument2 pagesZava Sifu Le Nine Manahmed mohammedNo ratings yet

- Reviewer On Tariff and Customs DutiesDocument48 pagesReviewer On Tariff and Customs DutiesMiguel Anas Jr.100% (6)

- Project TrackerDocument2 pagesProject TrackerRifky FarhanNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditFrom EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditRating: 5 out of 5 stars5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 5 out of 5 stars5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet