You might also like

- Fundamental Analysis of Banking SectorsDocument63 pagesFundamental Analysis of Banking SectorsDeepak Kashyap75% (4)

- SBSA Statement 2023-01-09Document39 pagesSBSA Statement 2023-01-09Maestro ProsperNo ratings yet

- Shane Koyczans PlacesDocument3 pagesShane Koyczans Placesapi-501779888No ratings yet

- AcknowlegdementDocument29 pagesAcknowlegdementYamini MehtaNo ratings yet

- Comparative Study Between Private Sectors Bank and Public Sector BanksDocument36 pagesComparative Study Between Private Sectors Bank and Public Sector BanksjudeNo ratings yet

- Project Report PDFDocument27 pagesProject Report PDFGOURAB BANIK Umeschandra CollegeNo ratings yet

- Chapter PageDocument76 pagesChapter PageGuru prasad.pNo ratings yet

- WORKING CAPITAL ManagementDocument38 pagesWORKING CAPITAL ManagementAmit PasiNo ratings yet

- Introduction To Banking Business in India: Chapter - 1Document21 pagesIntroduction To Banking Business in India: Chapter - 1MAMUNINo ratings yet

- A Study On Project Report On Commercial BankDocument8 pagesA Study On Project Report On Commercial BankGAME SPOT TAMIZHANNo ratings yet

- 08 - Chapter 1 PreambleDocument25 pages08 - Chapter 1 PreambleAnonymous Q6EAsy3mSNo ratings yet

- Project Report On NPA Policies of Bank of MaharashtraDocument64 pagesProject Report On NPA Policies of Bank of MaharashtraAMIT K SINGH88% (8)

- Comparative Study of The Public Sector Amp Private Sector BankDocument70 pagesComparative Study of The Public Sector Amp Private Sector BankSetuAgrawalNo ratings yet

- Banking SectorDocument9 pagesBanking Sectorsneha pandeyNo ratings yet

- Banking LawDocument13 pagesBanking Lawprithvi yadavNo ratings yet

- Research ReportDocument66 pagesResearch ReportSuraj DubeyNo ratings yet

- A Research Report ON Service Quality AND Customer Satisfaction of Kotak Mahindra BankDocument88 pagesA Research Report ON Service Quality AND Customer Satisfaction of Kotak Mahindra BankchaudharinitinNo ratings yet

- Comparative Study On Services of Public Sector and Private Sector BanksDocument49 pagesComparative Study On Services of Public Sector and Private Sector BanksvimalaNo ratings yet

- Assignment ON: Indian School of Mines (Ism)Document31 pagesAssignment ON: Indian School of Mines (Ism)Utkarsh SankrityayanNo ratings yet

- Role of Banking Sector in Indian EconomyDocument6 pagesRole of Banking Sector in Indian EconomySandeep TiwariNo ratings yet

- A Project Report ON: Submitted in Partial Fulfillment of The Requirement of Award of The Degree ofDocument23 pagesA Project Report ON: Submitted in Partial Fulfillment of The Requirement of Award of The Degree ofBinit AgarwallaNo ratings yet

- Comparative Study On Seavices of Public Sector and Private Sector Banks OptDocument49 pagesComparative Study On Seavices of Public Sector and Private Sector Banks OptWashik Malik100% (1)

- Sbi Mutual FundDocument78 pagesSbi Mutual Fundsshane kumar33% (3)

- Loans and AdvancesDocument83 pagesLoans and Advancespandu kmpNo ratings yet

- Corporation Bank Report FinalDocument61 pagesCorporation Bank Report FinalJasmandeep brarNo ratings yet

- DCB Bank - SipDocument59 pagesDCB Bank - SipRiya AgrawalNo ratings yet

- SemIX. Banking Law - Abhijeet Mishra - Project.03Document22 pagesSemIX. Banking Law - Abhijeet Mishra - Project.03AbhijeetMishraNo ratings yet

- Arunesh FileDocument78 pagesArunesh FileI'mkingamarNo ratings yet

- Aman's SynopsisDocument10 pagesAman's SynopsisAman KumarNo ratings yet

- VijayDocument5 pagesVijayvijaymehta19No ratings yet

- Final ProjectDocument64 pagesFinal ProjectVarun JainNo ratings yet

- Industry Profile Introduction To Banking:: A Study On Working Capital Analysis at Canara Bank SidlaghattaDocument74 pagesIndustry Profile Introduction To Banking:: A Study On Working Capital Analysis at Canara Bank SidlaghattaVinutha GowdaNo ratings yet

- Comparative Study On Services of Public Sector and Private Sector BanksDocument48 pagesComparative Study On Services of Public Sector and Private Sector BanksRanjan Kishor92% (13)

- Bank of IndiaDocument22 pagesBank of IndiaLeeladhar Nagar100% (1)

- Comparative Study Between Private Sector Banks and Public Sector BanksDocument68 pagesComparative Study Between Private Sector Banks and Public Sector BanksRhytz Singh100% (1)

- Banking LawDocument52 pagesBanking LawKillspreeNo ratings yet

- "Customer Attitude Towards Commercial Loan": A Research Project OnDocument57 pages"Customer Attitude Towards Commercial Loan": A Research Project OnSurender Dhuran PrajapatNo ratings yet

- Manasi Banking Law AshishDocument22 pagesManasi Banking Law AshishAshish SinghNo ratings yet

- A Study of Rural Banking in India-SynopsisDocument4 pagesA Study of Rural Banking in India-SynopsisNageshwar singh100% (4)

- YesbbnkDocument50 pagesYesbbnklatest updateNo ratings yet

- "Credit Risk Management in State Bank of India": Title of The ProjectDocument43 pages"Credit Risk Management in State Bank of India": Title of The Projectswarali deshmukhNo ratings yet

- A Study of Financial Institution in India SakshiDocument27 pagesA Study of Financial Institution in India Sakshisakshi.rane.17819No ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument19 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaAbhijit Singh ChaturvediNo ratings yet

- Banking Is A Vital System For Developing Economy For The NationDocument13 pagesBanking Is A Vital System For Developing Economy For The NationVinit SinghNo ratings yet

- Banking - Banking Sector in IndiaDocument65 pagesBanking - Banking Sector in Indiapraveen_rautela100% (1)

- Internship Report of National Bank of PakistanDocument104 pagesInternship Report of National Bank of PakistanHusnain BalochNo ratings yet

- Preface: of Public Sector and Private Sector Banks"Document47 pagesPreface: of Public Sector and Private Sector Banks"madhuri100% (1)

- Executive SummaryDocument57 pagesExecutive SummarySony BhagchandaniNo ratings yet

- Comparative Study of The Public Sector Amp Private Sector BankDocument68 pagesComparative Study of The Public Sector Amp Private Sector Bankankurp68No ratings yet

- A Study On Financial Statement Analysis of HDFCDocument63 pagesA Study On Financial Statement Analysis of HDFCKeleti SanthoshNo ratings yet

- ParveezDocument55 pagesParveezRameem PaNo ratings yet

- State Bank of India Welcomes You To Explore The World of Premier Bank in IndiaDocument4 pagesState Bank of India Welcomes You To Explore The World of Premier Bank in Indiakishan kanojiaNo ratings yet

- Synopsis Tittle of The Project: A Study of Rural Banking in A State (Maharashtra)Document4 pagesSynopsis Tittle of The Project: A Study of Rural Banking in A State (Maharashtra)Rohit UbaleNo ratings yet

- UntitledDocument52 pagesUntitledAjay ChahalNo ratings yet

- Project - Loans and AdvancesDocument60 pagesProject - Loans and AdvancesRajendra Gawate75% (12)

- Retail Banking at HDFC BankDocument59 pagesRetail Banking at HDFC BankHardip MatholiyaNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Understanding the Nigerian Financial System for Secondary School StudentsFrom EverandUnderstanding the Nigerian Financial System for Secondary School StudentsNo ratings yet

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- Akash Project 23 JuneDocument54 pagesAkash Project 23 Junepratibha bawankuleNo ratings yet

- Project On: Submitted ByDocument16 pagesProject On: Submitted Bypratibha bawankuleNo ratings yet

- ZoologyDocument33 pagesZoologypratibha bawankuleNo ratings yet

- Akash Project 23 JuneDocument54 pagesAkash Project 23 Junepratibha bawankuleNo ratings yet

- Phd. ProDocument2 pagesPhd. Propratibha bawankuleNo ratings yet

- Prerna HaldiramDocument42 pagesPrerna Haldirampratibha bawankuleNo ratings yet

- Prerna HaldiramDocument42 pagesPrerna Haldirampratibha bawankuleNo ratings yet

- Parle GDocument10 pagesParle Gpratibha bawankuleNo ratings yet

- CHAPTERDocument12 pagesCHAPTERpratibha bawankuleNo ratings yet

- Samsung ProjectDocument14 pagesSamsung Projectpratibha bawankuleNo ratings yet

- Parle GDocument10 pagesParle Gpratibha bawankuleNo ratings yet

- Samsung ProjectDocument14 pagesSamsung Projectpratibha bawankuleNo ratings yet

- Apple ProjectDocument50 pagesApple Projectpratibha bawankule50% (2)

- Anmol Mba 2018Document15 pagesAnmol Mba 2018pratibha bawankuleNo ratings yet

- Raymond ProjectDocument5 pagesRaymond Projectpratibha bawankuleNo ratings yet

- SupriyaDocument4 pagesSupriyapratibha bawankuleNo ratings yet

- A Study of Marketing Statergy of Haldiram ProjectDocument17 pagesA Study of Marketing Statergy of Haldiram Projectpratibha bawankuleNo ratings yet

- Ayurvedic CollegeDocument3 pagesAyurvedic Collegepratibha bawankuleNo ratings yet

- A Study of Marketing Statergy of Haldiram ProjectDocument17 pagesA Study of Marketing Statergy of Haldiram Projectpratibha bawankuleNo ratings yet

- IntroductionDocument41 pagesIntroductionpratibha bawankuleNo ratings yet

- INTRODUCTIO1Document14 pagesINTRODUCTIO1pratibha bawankuleNo ratings yet

- IntroductionDocument41 pagesIntroductionpratibha bawankuleNo ratings yet

- INTRODUCTION Final MonaDocument17 pagesINTRODUCTION Final Monapratibha bawankule100% (1)

- Chetan Kale PDFDocument33 pagesChetan Kale PDFpratibha bawankuleNo ratings yet

- Pooja SynopsisDocument54 pagesPooja Synopsispratibha bawankuleNo ratings yet

- Hitesh ProjectDocument41 pagesHitesh Projectpratibha bawankuleNo ratings yet

- IntroductionDocument41 pagesIntroductionpratibha bawankuleNo ratings yet

- PrastavanaDocument105 pagesPrastavanapratibha bawankuleNo ratings yet

- Module 2 ProblemsDocument15 pagesModule 2 ProblemsCristina TayagNo ratings yet

- Financial Accounting:: Lecturer:Agil AzizovDocument28 pagesFinancial Accounting:: Lecturer:Agil AzizovKəmalə AslanzadəNo ratings yet

- 2nd Merit List BSC Hons Agriculture E Agriculture and Environment BAHAWALPUR BWP Merit Spring 2021Document1 page2nd Merit List BSC Hons Agriculture E Agriculture and Environment BAHAWALPUR BWP Merit Spring 2021MubashirNo ratings yet

- Department of Education: Barangay G.S. Rosario, Carranglan, Nueva EcijaDocument4 pagesDepartment of Education: Barangay G.S. Rosario, Carranglan, Nueva EcijaDiaRamosAysonNo ratings yet

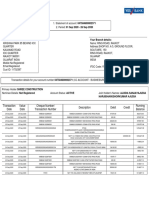

- Your Branch DetailsDocument4 pagesYour Branch DetailsShree ConstructionNo ratings yet

- Agricultural Finance and Agricultural Credit-Role of Institutional and Non - Institutional Agencies-Rural IndebtednessDocument30 pagesAgricultural Finance and Agricultural Credit-Role of Institutional and Non - Institutional Agencies-Rural IndebtednessKIRUTHIKANo ratings yet

- Lecture On Amortization and Amortization ScheduleDocument3 pagesLecture On Amortization and Amortization ScheduleAeiaNo ratings yet

- BAC 211 Assignment 2018Document4 pagesBAC 211 Assignment 2018vincentNo ratings yet

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Document6 pagesStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNo ratings yet

- STMT - 0000000000017286767 - 0 - 10000480057 - 3173958 - 20 Oct 2023 4Document8 pagesSTMT - 0000000000017286767 - 0 - 10000480057 - 3173958 - 20 Oct 2023 4mirayarslan83No ratings yet

- Daily Fund Report-PCSO Daily Report PDFDocument2 pagesDaily Fund Report-PCSO Daily Report PDFFranz Thelen Lozano CariñoNo ratings yet

- Estmt 2021Document8 pagesEstmt 2021Carla Bermudez RamirezNo ratings yet

- SBL Internship ReportDocument30 pagesSBL Internship ReportPrajwol ThapaNo ratings yet

- Remittance Application Form MAR2022 E - Form PDFDocument2 pagesRemittance Application Form MAR2022 E - Form PDFAlldyNo ratings yet

- Auto Debit Arrangement - 20201019 - 095034 PDFDocument3 pagesAuto Debit Arrangement - 20201019 - 095034 PDFRobert Adrian De RuedaNo ratings yet

- Directory of Banks and Financial Institutions Operating in Tanzania June 2016Document11 pagesDirectory of Banks and Financial Institutions Operating in Tanzania June 2016Lucas P. KusareNo ratings yet

- Ejercicios Semana 3 Sesión 1 B (Evaluación de Proyectos)Document3 pagesEjercicios Semana 3 Sesión 1 B (Evaluación de Proyectos)Alison Joyce Herrera Maldonado0% (1)

- Fine004 Test 1 2Document18 pagesFine004 Test 1 2Nageshwar SinghNo ratings yet

- Kenya Infrastructure Bond Terms IFB1-2018-20 Dated 19.11.2018Document2 pagesKenya Infrastructure Bond Terms IFB1-2018-20 Dated 19.11.2018Willing ZvirevoNo ratings yet

- Strategic Cost Management and Performance Evaluation: RequiredDocument2 pagesStrategic Cost Management and Performance Evaluation: Requiredritz meshNo ratings yet

- Banking Question PapersDocument12 pagesBanking Question Papersmohak khinNo ratings yet

- WDB Vý Gû E Vswks WefvmDocument1 pageWDB Vý Gû E Vswks WefvmDipto Kumar BiswasNo ratings yet

- SBI PO ResultDocument6 pagesSBI PO ResultgelcodoNo ratings yet

- Lecture 5Document84 pagesLecture 5Lee Li HengNo ratings yet

- Literature Review On Housing LoanDocument8 pagesLiterature Review On Housing Loanfihum1hadej2100% (1)

- Câu Hỏi chap 23,24,28,29 in marcoeconomicsDocument23 pagesCâu Hỏi chap 23,24,28,29 in marcoeconomicschang vicNo ratings yet

- Rool No 32 BlackBook A Study Related To Consumer Perception Towards Payment Bank and Its Impact On Indian EconomyDocument67 pagesRool No 32 BlackBook A Study Related To Consumer Perception Towards Payment Bank and Its Impact On Indian Economynishanth naikNo ratings yet

- Property Loan Agreement: I. The PartiesDocument2 pagesProperty Loan Agreement: I. The PartiesSsekitoleko TwahaNo ratings yet