You might also like

- Module 3 Yr. 2017Document89 pagesModule 3 Yr. 2017Xaky ODNo ratings yet

- Insurance Policy Administration Systems A Complete Guide - 2019 EditionFrom EverandInsurance Policy Administration Systems A Complete Guide - 2019 EditionNo ratings yet

- Managing Credit Risk in Corporate Bond Portfolios: A Practitioner's GuideFrom EverandManaging Credit Risk in Corporate Bond Portfolios: A Practitioner's GuideNo ratings yet

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Module 5 Yr. 2017Document85 pagesModule 5 Yr. 2017Xaky ODNo ratings yet

- IC 14 Regulations PDFDocument320 pagesIC 14 Regulations PDFanjana CrNo ratings yet

- 7 Clark Reinsurance PricingDocument8 pages7 Clark Reinsurance Pricingah mengNo ratings yet

- FUNDAMENTALS OF CASUALTY ACTUARIAL SCIENCE - CHAPTER 5 - Casualty PDFDocument120 pagesFUNDAMENTALS OF CASUALTY ACTUARIAL SCIENCE - CHAPTER 5 - Casualty PDFRafael Xavier Botelho0% (1)

- Valuation of Asset For The Purpose of InsuranceDocument13 pagesValuation of Asset For The Purpose of InsuranceAhmedAli100% (1)

- Ciin SyllabusDocument61 pagesCiin SyllabusejoghenetaNo ratings yet

- Acturial AnalysisDocument14 pagesActurial AnalysisRISHAB NANGIANo ratings yet

- Actuaries, Its Role and Function: Group Member Jyoti Gupta Disha Verma Kuldeep Hudda (Vitd)Document14 pagesActuaries, Its Role and Function: Group Member Jyoti Gupta Disha Verma Kuldeep Hudda (Vitd)Disha VermaNo ratings yet

- 05 Goldburd Khare Tevet PDFDocument106 pages05 Goldburd Khare Tevet PDFGiovanaNo ratings yet

- Legal Framework in InsuranceDocument36 pagesLegal Framework in InsuranceHarshit Srivastava 18MBA0050No ratings yet

- Caa Student Actuarial Analyst Handbooknov14Document62 pagesCaa Student Actuarial Analyst Handbooknov14SiphoKhosaNo ratings yet

- Stochastic Claims Reserving Methods in InsuranceFrom EverandStochastic Claims Reserving Methods in InsuranceRating: 3 out of 5 stars3/5 (1)

- 05 - LLMIT CH 5 Feb 08 PDFDocument22 pages05 - LLMIT CH 5 Feb 08 PDFPradyut TiwariNo ratings yet

- An Introductory Guide in The Construction of Actuarial Models: A Preparation For The Actuarial Exam C/4Document350 pagesAn Introductory Guide in The Construction of Actuarial Models: A Preparation For The Actuarial Exam C/4Kalev Maricq100% (1)

- w3 - Contract Provisions in Life InsuranceDocument31 pagesw3 - Contract Provisions in Life InsuranceNur AliaNo ratings yet

- MAX BUPA Health Insurance Company LTD: Claims ManualDocument13 pagesMAX BUPA Health Insurance Company LTD: Claims Manualjkhan_724384No ratings yet

- Dokumen - Tips Risk Management and Insurance Mcgraw Hill PDF Management and Insurance Mcgraw HillDocument2 pagesDokumen - Tips Risk Management and Insurance Mcgraw Hill PDF Management and Insurance Mcgraw HillGayathry Rajendran RCBSNo ratings yet

- Insurance ManagementDocument76 pagesInsurance ManagementDurga Prasad DashNo ratings yet

- Reinsurance Glossary 3Document68 pagesReinsurance Glossary 3أبو أنس - اليمنNo ratings yet

- Statistics and Probability-Lesson 1Document109 pagesStatistics and Probability-Lesson 1Airene CastañosNo ratings yet

- LOMA CatalogueDocument84 pagesLOMA CatalogueMarielle MaltoNo ratings yet

- Certificate in Insurance: Unit 1 - Insurance, Legal and RegulatoryDocument29 pagesCertificate in Insurance: Unit 1 - Insurance, Legal and RegulatorytamzNo ratings yet

- Enterprise Risk Management A Complete Guide - 2019 EditionFrom EverandEnterprise Risk Management A Complete Guide - 2019 EditionNo ratings yet

- Fixing of Sum Insured Under Fire Insurance PoliciesDocument17 pagesFixing of Sum Insured Under Fire Insurance PoliciesShayak Kumar GhoshNo ratings yet

- Use of A DFA Model To Evaluate Reinsurance Programs: Case StudyDocument30 pagesUse of A DFA Model To Evaluate Reinsurance Programs: Case StudyHesham Alabani100% (2)

- 01 - LLMIT CH 1 Feb 08Document18 pages01 - LLMIT CH 1 Feb 08Pradyut TiwariNo ratings yet

- General Linear Model (GLM)Document58 pagesGeneral Linear Model (GLM)Imran ShahrilNo ratings yet

- 3 - PRobabilityDocument17 pages3 - PRobabilityAnonymous UP5RC6JpGNo ratings yet

- Risks and Rewards For The Insurance Sector: The Big Issues, and How To Tackle ThemDocument26 pagesRisks and Rewards For The Insurance Sector: The Big Issues, and How To Tackle ThemPie DiverNo ratings yet

- A Cat Bond Premium Puzzle?: Financial Institutions CenterDocument36 pagesA Cat Bond Premium Puzzle?: Financial Institutions CenterchanduNo ratings yet

- Understanding U.S. LawDocument2 pagesUnderstanding U.S. LawShanmuganathan RamanathanNo ratings yet

- Candidate Guide SCR24Document16 pagesCandidate Guide SCR24Michael JunusNo ratings yet

- Boiler & MachineryDocument35 pagesBoiler & Machineryjoseph320@yahooNo ratings yet

- 02 - LLMIT CH 2 Feb 08Document24 pages02 - LLMIT CH 2 Feb 08Pradyut TiwariNo ratings yet

- Fundamentals of insurance terminology explainedDocument16 pagesFundamentals of insurance terminology explainedFaye Nandini SalinsNo ratings yet

- Pension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlFrom EverandPension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlNo ratings yet

- Module 2 Yr. 2017Document105 pagesModule 2 Yr. 2017Xaky ODNo ratings yet

- Reinsurance ReportDocument16 pagesReinsurance ReportaxyknoNo ratings yet

- Intro To Ratemaking SampleDocument51 pagesIntro To Ratemaking SampleEvelyn JacquelineNo ratings yet

- Life Insurance and Pension Business, Key Man Insurance and Human Life Value InsuranceDocument7 pagesLife Insurance and Pension Business, Key Man Insurance and Human Life Value InsuranceShivam GargNo ratings yet

- Quantitative Asset Management: Factor Investing and Machine Learning for Institutional InvestingFrom EverandQuantitative Asset Management: Factor Investing and Machine Learning for Institutional InvestingNo ratings yet

- Software Security Vulnerability A Complete Guide - 2020 EditionFrom EverandSoftware Security Vulnerability A Complete Guide - 2020 EditionNo ratings yet

- Share-Based Compensation: Learning ObjectivesDocument48 pagesShare-Based Compensation: Learning ObjectivesMark S MadsenNo ratings yet

- Strategic Underwriting RevisedDocument14 pagesStrategic Underwriting RevisedNiomi GolraiNo ratings yet

- CT1Document204 pagesCT1Akhil Garg0% (1)

- Insurance Qualifications FrameworkDocument1 pageInsurance Qualifications FrameworkWill SackettNo ratings yet

- ST8 General Insurance Pricing PDFDocument4 pagesST8 General Insurance Pricing PDFVignesh SrinivasanNo ratings yet

- CT5: Key concepts in life insuranceDocument15 pagesCT5: Key concepts in life insurancePriyaNo ratings yet

- Sa3 Pu 14 PDFDocument114 pagesSa3 Pu 14 PDFPolelarNo ratings yet

- Lloyd's Solvency II Tutorial GuideDocument9 pagesLloyd's Solvency II Tutorial Guidescribd4anoop100% (1)

- Rate Making: How Insurance Premiums Are SetDocument4 pagesRate Making: How Insurance Premiums Are SetSai Teja NadellaNo ratings yet

- 2016 The Institutes Full CatalogDocument40 pages2016 The Institutes Full CatalogJeremy JarvisNo ratings yet

- Table No 133Document2 pagesTable No 133ssfinservNo ratings yet

- Social Style Working RelationshipDocument2 pagesSocial Style Working Relationshipchemicalchouhan9303No ratings yet

- Entry, DiaPPPe or Crning)Document2 pagesEntry, DiaPPPe or Crning)chemicalchouhan9303No ratings yet

- Ammonium Hydroxide 2012 PetitionDocument47 pagesAmmonium Hydroxide 2012 Petitionchemicalchouhan9303No ratings yet

- Specific - Requirements-for-Water-DischargeDocument3 pagesSpecific - Requirements-for-Water-Dischargechemicalchouhan9303No ratings yet

- Ok Common Acquaintances)Document2 pagesOk Common Acquaintances)chemicalchouhan9303No ratings yet

- Social Style Teams RelationshipDocument2 pagesSocial Style Teams Relationshipchemicalchouhan9303No ratings yet

- Strategy in The Global EnvironmentDocument2 pagesStrategy in The Global Environmentchemicalchouhan9303No ratings yet

- Social Style AaDocument2 pagesSocial Style Aachemicalchouhan9303No ratings yet

- Entry, Dialogue or Closurerning)Document2 pagesEntry, Dialogue or Closurerning)chemicalchouhan9303No ratings yet

- Three Key Concepts For Productive Communication)Document2 pagesThree Key Concepts For Productive Communication)chemicalchouhan9303No ratings yet

- Competitive Positioning in Different Industry EnvironmentsonDocument2 pagesCompetitive Positioning in Different Industry Environmentsonchemicalchouhan9303No ratings yet

- Comfort - The Key To 7 Trust and Confidenceearning)Document2 pagesComfort - The Key To 7 Trust and Confidenceearning)chemicalchouhan9303No ratings yet

- z2 - M70315 - HE - Primer - Marketing - FNL - WebDocument20 pagesz2 - M70315 - HE - Primer - Marketing - FNL - Webchemicalchouhan9303No ratings yet

- Choosing A Global StrategyDocument2 pagesChoosing A Global Strategychemicalchouhan9303No ratings yet

- Functional Strategies and The Generic Building Blocks of Competitive AdvantagenDocument2 pagesFunctional Strategies and The Generic Building Blocks of Competitive Advantagenchemicalchouhan9303No ratings yet

- Data and Customers Become Critical - Org)Document2 pagesData and Customers Become Critical - Org)chemicalchouhan9303No ratings yet

- Human Relations in Industryorg)Document2 pagesHuman Relations in Industryorg)chemicalchouhan9303No ratings yet

- Distinctive Competencies and Competitive AdvantageDocument2 pagesDistinctive Competencies and Competitive Advantagechemicalchouhan9303No ratings yet

- Complementary Products and Network Effectsg)Document2 pagesComplementary Products and Network Effectsg)chemicalchouhan9303No ratings yet

- Rebuild Your Organization - Org)Document2 pagesRebuild Your Organization - Org)chemicalchouhan9303No ratings yet

- Competitive Advantage No Longer Comes - Org)Document2 pagesCompetitive Advantage No Longer Comes - Org)chemicalchouhan9303No ratings yet

- Good Preparation: Considered CommunicationDocument2 pagesGood Preparation: Considered Communicationchemicalchouhan9303No ratings yet

- U. S. Steel Corporation Brought Together Around 158b.org)Document2 pagesU. S. Steel Corporation Brought Together Around 158b.org)chemicalchouhan9303No ratings yet

- Scientific Management and The Image of Managersb - Org)Document2 pagesScientific Management and The Image of Managersb - Org)chemicalchouhan9303No ratings yet

- Cablevision in Late 2015 by French telecommunicationsFDrive)Document2 pagesCablevision in Late 2015 by French telecommunicationsFDrive)chemicalchouhan9303No ratings yet

- Men and Women of The Corporation - The Populationib - Org)Document2 pagesMen and Women of The Corporation - The Populationib - Org)chemicalchouhan9303No ratings yet

- Revenue From Concerts and From The Sale of Recorded Music in Theg)Document2 pagesRevenue From Concerts and From The Sale of Recorded Music in Theg)chemicalchouhan9303No ratings yet

- Inadequate To Maintain Desired Customer deliveryFDrive)Document2 pagesInadequate To Maintain Desired Customer deliveryFDrive)chemicalchouhan9303No ratings yet

- The Components of Due DiligenceFDrive)Document2 pagesThe Components of Due DiligenceFDrive)chemicalchouhan9303No ratings yet

- Bring-Down Provision, Requiring That representationsDFDrive)Document2 pagesBring-Down Provision, Requiring That representationsDFDrive)chemicalchouhan9303No ratings yet

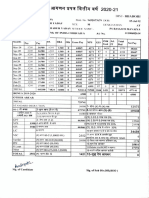

- Annual Report 2020-21Document121 pagesAnnual Report 2020-21Chhavi GajnaniNo ratings yet

- Employability Skills - Term IIDocument5 pagesEmployability Skills - Term IISSDLHO sevenseasNo ratings yet

- Business Implications of Sustainability Practices in Supply ChainsDocument25 pagesBusiness Implications of Sustainability Practices in Supply ChainsBizNo ratings yet

- Data Warehousing: A Strategic Tool for Business InsightsDocument30 pagesData Warehousing: A Strategic Tool for Business InsightsMrudul BhattNo ratings yet

- MAS BackgroundDocument2 pagesMAS BackgroundJie FifieNo ratings yet

- Ifr-Apc 311Document8 pagesIfr-Apc 311hkndarshanaNo ratings yet

- South Est BankDocument78 pagesSouth Est BankGolpo MahmudNo ratings yet

- AGRASOC ReviewerDocument30 pagesAGRASOC ReviewerSabrina YuNo ratings yet

- Entrepreneurship Relevance to SHS StudentsDocument7 pagesEntrepreneurship Relevance to SHS StudentsAndrea Grace Bayot AdanaNo ratings yet

- 5.a Study On Utilization and Convenient of Credit CardDocument11 pages5.a Study On Utilization and Convenient of Credit CardbsshankarraviNo ratings yet

- AXIS BANK NDocument20 pagesAXIS BANK Nankit5849733% (3)

- Analysts See Upside in These Stocks Like Netflix & TeslaDocument14 pagesAnalysts See Upside in These Stocks Like Netflix & TeslaBenjamin ChongNo ratings yet

- Parfums Cacharel de L'Oréal 1997-2007:: Decoding and Revitalizing A Classic BrandDocument21 pagesParfums Cacharel de L'Oréal 1997-2007:: Decoding and Revitalizing A Classic BrandrheaNo ratings yet

- Financial assistance proposal for 108-acre farm projectDocument11 pagesFinancial assistance proposal for 108-acre farm projectDilip Devidas JoshiNo ratings yet

- Income Tax Agadan PrapatraDocument3 pagesIncome Tax Agadan Prapatraat.amitkumarbstNo ratings yet

- Social Support For Expatriates Through Virtual Platforms: Exploring The Role of Online and Offline ParticipationDocument33 pagesSocial Support For Expatriates Through Virtual Platforms: Exploring The Role of Online and Offline ParticipationAniss AitallaNo ratings yet

- #34 Naranjo V Biomedica Health Care (Magsino)Document2 pages#34 Naranjo V Biomedica Health Care (Magsino)Trxc MagsinoNo ratings yet

- 4bs1 02 Que 20231122Document24 pages4bs1 02 Que 20231122supercoolhashir100% (1)

- Aws Qc5-91 - Standard For Certification of Welding EducatorsDocument12 pagesAws Qc5-91 - Standard For Certification of Welding Educatorscamelod555No ratings yet

- Duality Theory - Assignment A) Primal ProblemDocument5 pagesDuality Theory - Assignment A) Primal ProblemSohaib ArifNo ratings yet

- CASE 1 Planning For Rise of Cloud Computing at MicrosoftDocument3 pagesCASE 1 Planning For Rise of Cloud Computing at MicrosoftVarunKeshariNo ratings yet

- CIR v. PDI (Waiver)Document30 pagesCIR v. PDI (Waiver)Jerwin DaveNo ratings yet

- MPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)Document24 pagesMPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)trickyhunter9999No ratings yet

- Indonesian Outlook 2024-2029 - March 13th 2024Document10 pagesIndonesian Outlook 2024-2029 - March 13th 2024Saefuddin SaefuddinNo ratings yet

- Martin Pring On Market Momentum - IndicadoresDocument357 pagesMartin Pring On Market Momentum - IndicadoresÉdipo Henrique83% (6)

- PRC-Cebu CPA Exam Schedule October 2022Document26 pagesPRC-Cebu CPA Exam Schedule October 2022Marlon BaltarNo ratings yet

- 2,3,8,10Document2 pages2,3,8,10SzaeNo ratings yet

- EssentialismDocument1 pageEssentialismMehrdad FereydoniNo ratings yet

- Aral Pan 9 EquationDocument5 pagesAral Pan 9 EquationRashiel Jane Paronia CelizNo ratings yet

- ARBURG Customer Service Contact List 2021Document2 pagesARBURG Customer Service Contact List 2021Moises GeberNo ratings yet