You might also like

- CHAPTER 4 ProvisionDocument3 pagesCHAPTER 4 ProvisionEyra MercadejasNo ratings yet

- Chapter 4 Intermediate AccountingDocument41 pagesChapter 4 Intermediate AccountingMae Ann Raquin100% (1)

- PAS 37 Provision Contingent Liability and AssetDocument25 pagesPAS 37 Provision Contingent Liability and AssetCurly Spaghetti 88No ratings yet

- Provisions, Contingent Liabilities & Contingent AssetsDocument59 pagesProvisions, Contingent Liabilities & Contingent AssetsAANo ratings yet

- Provisions Related Standards: Pas 37 - Provisions, Contingent Liabilities & Contingent AssetsDocument7 pagesProvisions Related Standards: Pas 37 - Provisions, Contingent Liabilities & Contingent AssetsJulie Mae Caling MalitNo ratings yet

- Provisions and ContingenciesDocument13 pagesProvisions and ContingenciesJuan ManuelNo ratings yet

- Ia Chapter 4 Valix 2019Document5 pagesIa Chapter 4 Valix 2019M100% (1)

- ModuleACC 309 Current LiabilitiesDocument8 pagesModuleACC 309 Current LiabilitiesEdward Glenn BaguiNo ratings yet

- Unit Iii Learning ActivityDocument10 pagesUnit Iii Learning ActivityChin FiguraNo ratings yet

- T. Pentikainen HelsinkiDocument12 pagesT. Pentikainen Helsinkijapan177No ratings yet

- Risk Analysis in Capital BudgetingDocument6 pagesRisk Analysis in Capital BudgetingPavan Kumar MylavaramNo ratings yet

- Chapter 15: Short-Term Liabilities QuestionsDocument191 pagesChapter 15: Short-Term Liabilities QuestionslibraolrackNo ratings yet

- PrOVISION THEORIES FOR LIABILITYDocument3 pagesPrOVISION THEORIES FOR LIABILITYMARY ACOSTANo ratings yet

- ProvisionDocument7 pagesProvisionAiden MagnoNo ratings yet

- Chapter 15: Short-Term Liabilities QuestionsDocument191 pagesChapter 15: Short-Term Liabilities QuestionsHanabusa Kawaii IdouNo ratings yet

- Current Liabilities and ContingenciesDocument12 pagesCurrent Liabilities and ContingenciesLu CasNo ratings yet

- CFA InstituteDocument11 pagesCFA Institutejuan carlos molano toroNo ratings yet

- 54987bosfndnov19 p1 cp1 U5 PDFDocument4 pages54987bosfndnov19 p1 cp1 U5 PDFAnkitaNo ratings yet

- FdsedjwhajdhkudshdhxDocument28 pagesFdsedjwhajdhkudshdhxJoylyn CombongNo ratings yet

- Sa Apr09 PogueDocument7 pagesSa Apr09 PogueDanish IqbalNo ratings yet

- Expected Adverse Deviation As A Measure of Risk DistributionDocument11 pagesExpected Adverse Deviation As A Measure of Risk DistributiontunaboyNo ratings yet

- Cfas Events After Reporting PeriodDocument18 pagesCfas Events After Reporting PeriodJerry ToledoNo ratings yet

- GONDA, ANN JERLYN - Financial Risk ManagementDocument40 pagesGONDA, ANN JERLYN - Financial Risk ManagementAngel GondaNo ratings yet

- Chapter 4 - Provision-Contingent LiabilityDocument7 pagesChapter 4 - Provision-Contingent LiabilityMarx Yuri JaymeNo ratings yet

- Contingent Assets and Contingent LiabilitiesDocument5 pagesContingent Assets and Contingent LiabilitiesRonan Ferrer100% (1)

- 10 Ias 37Document5 pages10 Ias 37Irtiza AbbasNo ratings yet

- CHAPTER 1-Introduction To RiskDocument8 pagesCHAPTER 1-Introduction To RiskgozaloiNo ratings yet

- Unit 10 Provisions, Contingent Liabilities - AssetsDocument25 pagesUnit 10 Provisions, Contingent Liabilities - AssetsSiphesihleNo ratings yet

- Analyst Prep VRM 2024Document425 pagesAnalyst Prep VRM 2024Useless IdNo ratings yet

- Ifrs at A Glance IFRS 7 Financial Instruments: DisclosuresDocument5 pagesIfrs at A Glance IFRS 7 Financial Instruments: DisclosuresNoor Ul Hussain MirzaNo ratings yet

- Note Bu I 9Document4 pagesNote Bu I 9Huế ThùyNo ratings yet

- IAS 37 - Provisions Contingent Assets and LiabilitiesDocument25 pagesIAS 37 - Provisions Contingent Assets and Liabilitiesfarukh.kitchlewNo ratings yet

- Short Term Liabilities GitagiaDocument19 pagesShort Term Liabilities GitagiaEmmanuelNo ratings yet

- Module 4Document56 pagesModule 4Jiane SanicoNo ratings yet

- CH-3 - Risk Assessment and Internal ControlDocument122 pagesCH-3 - Risk Assessment and Internal Controlatishayjjj123No ratings yet

- Ind As 37: Provisions, Contingent Liabilities and Contingent AssetsDocument5 pagesInd As 37: Provisions, Contingent Liabilities and Contingent AssetsDinesh KumarNo ratings yet

- Current Liabilities - ProvisionsDocument9 pagesCurrent Liabilities - ProvisionsJerome_JadeNo ratings yet

- IAS 37 - SummaryDocument5 pagesIAS 37 - Summarysitoulamanish100No ratings yet

- Ias 37Document2 pagesIas 37Foititika.net100% (2)

- Case 6: Murchison Technologies Inc.: An Audit Case Analysis ActivityDocument8 pagesCase 6: Murchison Technologies Inc.: An Audit Case Analysis ActivityCiana Sacdalan100% (1)

- Risk and CoverageDocument11 pagesRisk and CoverageKingNo ratings yet

- 4 Risk ReturnDocument14 pages4 Risk ReturnUtkarsh BhalodeNo ratings yet

- Torts OutlineDocument17 pagesTorts OutlineStephanie WhiteleyNo ratings yet

- Accounting ProjectDocument5 pagesAccounting ProjectSonia DietNo ratings yet

- p1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingenciesDocument6 pagesp1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingencieskimNo ratings yet

- Contingent LiabilityDocument2 pagesContingent LiabilityRidwan Al MahmudNo ratings yet

- Portfolio Credit RiskDocument12 pagesPortfolio Credit RiskHassan AlJishiNo ratings yet

- Rethinking The Solvency II Risk MarginDocument14 pagesRethinking The Solvency II Risk MarginFaheem AhmadNo ratings yet

- Reserving InsuranceDocument19 pagesReserving InsuranceDarwin DcNo ratings yet

- 2 8306 MarketMagic Slides Su20 PDFDocument33 pages2 8306 MarketMagic Slides Su20 PDFsodakshNo ratings yet

- Var Vs Expected Shortfall (Why VaR Is Not Subadditive, But ES Is) - HullDocument4 pagesVar Vs Expected Shortfall (Why VaR Is Not Subadditive, But ES Is) - HullKaushik NathNo ratings yet

- Chapter 7 Accounting For Provisions, Contingencies and Events After The Reporting PeriodDocument30 pagesChapter 7 Accounting For Provisions, Contingencies and Events After The Reporting Periodsamuel_dwumfourNo ratings yet

- LC Risk MGT CH 1Document7 pagesLC Risk MGT CH 1newaybeyene5No ratings yet

- PAS 37 AnswersDocument2 pagesPAS 37 AnswersxxpinkywitchxxNo ratings yet

- 74602bos60479 FND cp1 U4Document7 pages74602bos60479 FND cp1 U4kingdksNo ratings yet

- Chapter #2 (Part 1)Document17 pagesChapter #2 (Part 1)Consiko leeNo ratings yet

- Caparo Industries Plc. V Dickman 1990 UKDocument10 pagesCaparo Industries Plc. V Dickman 1990 UKSermon Md. Anwar HossainNo ratings yet

- 8.0 Introduction:.. Understanding Risk: FundsDocument13 pages8.0 Introduction:.. Understanding Risk: FundsAryan SinghiNo ratings yet

- The Financial Storm Warning for Investors: How to Prepare and Protect Your Wealth from Tax Hikes and Market CrashesFrom EverandThe Financial Storm Warning for Investors: How to Prepare and Protect Your Wealth from Tax Hikes and Market CrashesNo ratings yet

- TAIL RISK HEDGING: Creating Robust Portfolios for Volatile MarketsFrom EverandTAIL RISK HEDGING: Creating Robust Portfolios for Volatile MarketsNo ratings yet

- Unmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018Document1 pageUnmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018LokiNo ratings yet

- United States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018Document2 pagesUnited States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018LokiNo ratings yet

- Language Learning With Free PodcastsDocument3 pagesLanguage Learning With Free PodcastsLokiNo ratings yet

- Food - The GuardianDocument7 pagesFood - The GuardianLoki100% (1)

- Culture - The GuardianDocument8 pagesCulture - The GuardianLokiNo ratings yet

- 2019 Country Reports On Human Rights Practices - United States Department of StateDocument10 pages2019 Country Reports On Human Rights Practices - United States Department of StateLokiNo ratings yet

- Tax Gap: Corporate Income Tax Liability For Tax Year 2016Document1 pageTax Gap: Corporate Income Tax Liability For Tax Year 2016LokiNo ratings yet

- Tax Assessments: Required Supplementary Information (Unaudited) 208Document1 pageTax Assessments: Required Supplementary Information (Unaudited) 208LokiNo ratings yet

- Notes To The Financial Statements27Document1 pageNotes To The Financial Statements27LokiNo ratings yet

- Largest Income Tax Expenditures As of September 30, 2019Document2 pagesLargest Income Tax Expenditures As of September 30, 2019LokiNo ratings yet

- Notes To The Financial Statements26 PDFDocument1 pageNotes To The Financial Statements26 PDFLokiNo ratings yet

- Note 17. Collections and Refunds of Federal RevenueDocument3 pagesNote 17. Collections and Refunds of Federal RevenueLokiNo ratings yet

- Deferred Maintenance and RepairsDocument1 pageDeferred Maintenance and RepairsLokiNo ratings yet

- Note 23. Long-Term Fiscal ProjectionsDocument6 pagesNote 23. Long-Term Fiscal ProjectionsLokiNo ratings yet

- Note 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsDocument1 pageNote 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsLokiNo ratings yet

- Social Insurance: Social Security and MedicareDocument26 pagesSocial Insurance: Social Security and MedicareLokiNo ratings yet

- Sustainability of Fiscal PolicyDocument11 pagesSustainability of Fiscal PolicyLokiNo ratings yet

- Note 22. Social Insurance: 137 Notes To The Financial StatementsDocument18 pagesNote 22. Social Insurance: 137 Notes To The Financial StatementsLokiNo ratings yet

- Note 25. Disclosure Entities and Related PartiesDocument5 pagesNote 25. Disclosure Entities and Related PartiesLokiNo ratings yet

- Notes To The Financial Statements20Document6 pagesNotes To The Financial Statements20LokiNo ratings yet

- Note 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018Document3 pagesNote 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018LokiNo ratings yet

- Note 21. Fiduciary Activities: Thrift Savings PlanDocument2 pagesNote 21. Fiduciary Activities: Thrift Savings PlanLokiNo ratings yet

- Notes To The Financial Statements14Document1 pageNotes To The Financial Statements14LokiNo ratings yet

- Notes To The Financial Statements16Document2 pagesNotes To The Financial Statements16LokiNo ratings yet

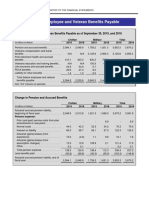

- Note 12. Federal Employee and Veteran Benefits PayableDocument10 pagesNote 12. Federal Employee and Veteran Benefits PayableLokiNo ratings yet

- Note 15. Insurance and Guarantee Program LiabilitiesDocument2 pagesNote 15. Insurance and Guarantee Program LiabilitiesLokiNo ratings yet

- Notes To The Financial Statements9Document1 pageNotes To The Financial Statements9LokiNo ratings yet

- Note 11. Federal Debt Securities Held by The Public and Accrued InterestDocument4 pagesNote 11. Federal Debt Securities Held by The Public and Accrued InterestLokiNo ratings yet

- Notes To The Financial Statements7Document3 pagesNotes To The Financial Statements7LokiNo ratings yet

- Note 13. Environmental and Disposal LiabilitiesDocument2 pagesNote 13. Environmental and Disposal LiabilitiesLokiNo ratings yet

- Inspection and Testing RequirementsDocument10 pagesInspection and Testing Requirementsnaoufel1706No ratings yet

- Owner Contractor AgreementDocument18 pagesOwner Contractor AgreementJayteeNo ratings yet

- Beebe ME Chain HoistDocument9 pagesBeebe ME Chain HoistDan VekasiNo ratings yet

- Lpe2501 Writing Portfolio Task 1 (Self-Editing Form)Document2 pagesLpe2501 Writing Portfolio Task 1 (Self-Editing Form)Sinorita TenggaiNo ratings yet

- Socialism and IslamDocument5 pagesSocialism and IslamAbdul kalamNo ratings yet

- A Coming Out Guide For Trans Young PeopleDocument44 pagesA Coming Out Guide For Trans Young PeopleDamilare Og0% (1)

- Water Quality Categorization Using WQI in Rural Areas of Haridwar, IndiaDocument16 pagesWater Quality Categorization Using WQI in Rural Areas of Haridwar, IndiaESSENCE - International Journal for Environmental Rehabilitation and ConservaionNo ratings yet

- RJK03S3DPADocument7 pagesRJK03S3DPAvineeth MNo ratings yet

- حماية الغير بالإشهار القانوني للشركة التجاريةDocument17 pagesحماية الغير بالإشهار القانوني للشركة التجاريةAmina hltNo ratings yet

- Two Nation Theory - Docx NarrativeDocument14 pagesTwo Nation Theory - Docx NarrativeSidra Jamshaid ChNo ratings yet

- Banyuwangi Legend PDFDocument10 pagesBanyuwangi Legend PDFVerolla PetrovaNo ratings yet

- Art 1455 and 1456 JurisprudenceDocument7 pagesArt 1455 and 1456 JurisprudenceMiguel OsidaNo ratings yet

- Compiled Case Digest For Criminal LawDocument54 pagesCompiled Case Digest For Criminal LawMicah Clark-Malinao100% (7)

- The PassiveDocument12 pagesThe PassiveCliver Rusvel Cari SucasacaNo ratings yet

- Entrep Q4 - Module 5Document10 pagesEntrep Q4 - Module 5Paula DT PelitoNo ratings yet

- Audit Eng LTRDocument2 pagesAudit Eng LTRumairashiq87No ratings yet

- PS Form 6387 Rural Money Order TransactionDocument1 pagePS Form 6387 Rural Money Order TransactionRoberto MonterrosaNo ratings yet

- Farm Animal Fun PackDocument12 pagesFarm Animal Fun PackDedeh KhalilahNo ratings yet

- Foaming at The MouthDocument1 pageFoaming at The Mouth90JDSF8938JLSNF390J3No ratings yet

- Installation of Baikal On Synology DSM5Document33 pagesInstallation of Baikal On Synology DSM5cronetNo ratings yet

- RIBA WorkstagesDocument1 pageRIBA WorkstagesCong TranNo ratings yet

- Claim Form - Part A' To 'Claim Form For Health Insurance PolicyDocument6 pagesClaim Form - Part A' To 'Claim Form For Health Insurance Policyanil sangwanNo ratings yet

- Daily Technical Report 15.03.2013Document4 pagesDaily Technical Report 15.03.2013Angel BrokingNo ratings yet

- Talend Data Quality DatasheetDocument2 pagesTalend Data Quality DatasheetAswinJamesNo ratings yet

- Hdil Judgement On SlumDocument43 pagesHdil Judgement On SlumSandeep NirbanNo ratings yet

- 1788-10 Series 310 Negative Pressure Glove Box ManualDocument10 pages1788-10 Series 310 Negative Pressure Glove Box Manualzivkovic brankoNo ratings yet

- Recruiting in Europe: A Guide For EmployersDocument12 pagesRecruiting in Europe: A Guide For EmployersLate ArtistNo ratings yet

- Ambrose Letter 73 To IrenaeusDocument4 pagesAmbrose Letter 73 To Irenaeuschris_rosebrough_1No ratings yet

- Shay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFDocument234 pagesShay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFMarko DabicNo ratings yet

- In The High Court of Calcutta: I.P. Mukerji and Md. Nizamuddin, JJDocument4 pagesIn The High Court of Calcutta: I.P. Mukerji and Md. Nizamuddin, JJsid tiwariNo ratings yet