You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- There May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowDocument6 pagesThere May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowNaeem Ahmed HattarNo ratings yet

- Scalping and Pre-set Value Trading: Football Double Chance Market - Betfair ExchangeFrom EverandScalping and Pre-set Value Trading: Football Double Chance Market - Betfair ExchangeNo ratings yet

- Problem 1: Short-Run Costs (15 Points)Document6 pagesProblem 1: Short-Run Costs (15 Points)Sanaa2510No ratings yet

- Micro Lecture06ADocument33 pagesMicro Lecture06Athu.nguyenhoangthanh.bbs21No ratings yet

- Micro Eportfolio Competition Spreadsheet Data-Fall 18Document4 pagesMicro Eportfolio Competition Spreadsheet Data-Fall 18api-334921583No ratings yet

- Profit MaximizationDocument20 pagesProfit MaximizationMary Pauline AyoNo ratings yet

- Team Member's: Varun Aggarwal Jyoti Chauhan Shashank Rana Preeti Pawaria Rahul Yadav Vijay Kundra Nitin Kumar Sapna RanaDocument75 pagesTeam Member's: Varun Aggarwal Jyoti Chauhan Shashank Rana Preeti Pawaria Rahul Yadav Vijay Kundra Nitin Kumar Sapna Ranagoyal_khushbu88No ratings yet

- 6.2 - Tutorial QuestionsDocument14 pages6.2 - Tutorial QuestionsMacxy TanNo ratings yet

- Micro-Econ Final PresentationDocument9 pagesMicro-Econ Final PresentationmichellebaileylindsaNo ratings yet

- Pie Kelompok 3Document15 pagesPie Kelompok 3Marsha HafizhaNo ratings yet

- Chapter Four: Supply II: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong UniversityDocument29 pagesChapter Four: Supply II: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong Universitymaria rafiqNo ratings yet

- Eportfolio AssignmentDocument17 pagesEportfolio Assignmentapi-409603904No ratings yet

- ECO1018 Supply Decision 2023 - 2024Document13 pagesECO1018 Supply Decision 2023 - 2024aaliya dubcatNo ratings yet

- Problem Set #3 Submit Via Gradescope by Tuesday October 13, 10:00pmDocument4 pagesProblem Set #3 Submit Via Gradescope by Tuesday October 13, 10:00pmAskIIT IanNo ratings yet

- Managerial DecisionsDocument85 pagesManagerial DecisionsVy NguyenNo ratings yet

- Module IIDocument36 pagesModule IIYash UpasaniNo ratings yet

- Ôn tập 3Document7 pagesÔn tập 3Gia HânNo ratings yet

- Econ 2 Chapter 4Document13 pagesEcon 2 Chapter 4Angelica MayNo ratings yet

- Perfect Competition Profit MacDocument51 pagesPerfect Competition Profit MacSmurf AccountNo ratings yet

- ECO2 AssignmentDocument5 pagesECO2 AssignmentDrakenlor GonshiNo ratings yet

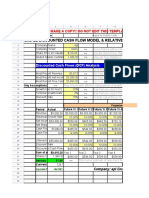

- Simple Discounted Cash Flow Model & Relative ValuationDocument14 pagesSimple Discounted Cash Flow Model & Relative ValuationlearnNo ratings yet

- Assignment 3: Course Title: ECO101Document4 pagesAssignment 3: Course Title: ECO101Rashik AhmedNo ratings yet

- Profit, Loss and Perfect CompetitionDocument31 pagesProfit, Loss and Perfect CompetitionPaula BatulanNo ratings yet

- Break Even Answer KeyDocument8 pagesBreak Even Answer Keyyea okayNo ratings yet

- Lecture 7 Competitive Market (Lec)Document17 pagesLecture 7 Competitive Market (Lec)Fathimath ShaheeraNo ratings yet

- Managerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Solutions Manual Full Chapter PDFDocument63 pagesManagerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Solutions Manual Full Chapter PDFKennethRiosmqoz100% (14)

- Chapter 5 - Cost-Volume-Profit Relationships: Click On LinksDocument34 pagesChapter 5 - Cost-Volume-Profit Relationships: Click On LinksRena AfrianiNo ratings yet

- Market TypesDocument32 pagesMarket TypesJintu Moni BarmanNo ratings yet

- Profit Maximization Under Monopolistic Competition: Choosing The Profit-Maximizing Output and PriceDocument5 pagesProfit Maximization Under Monopolistic Competition: Choosing The Profit-Maximizing Output and PriceCarla Mae F. DaduralNo ratings yet

- Latihan Kelompok - Firms in Competitive MarketsDocument6 pagesLatihan Kelompok - Firms in Competitive MarketsMarsha Hafizha100% (1)

- Eco Project FinalDocument36 pagesEco Project FinalSakshamNo ratings yet

- 11.3 Break Even in Units ($75,000/15,000 Units) - Fixed Cost Is $37,500Document14 pages11.3 Break Even in Units ($75,000/15,000 Units) - Fixed Cost Is $37,500Rizzah Nianiah100% (1)

- Fundamentals of Economics 6th Edition Boyes Solutions Manual DownloadDocument6 pagesFundamentals of Economics 6th Edition Boyes Solutions Manual DownloadLonnie Beck100% (27)

- Lecture 09MP 10-11 1s PDFDocument7 pagesLecture 09MP 10-11 1s PDFFranco ImperialNo ratings yet

- Firms in Competitive Markets: Introduction: A Scenario Characteristics of Perfect CompetitionDocument7 pagesFirms in Competitive Markets: Introduction: A Scenario Characteristics of Perfect CompetitionFranco ImperialNo ratings yet

- Scenario AnalysisDocument2 pagesScenario AnalysisDickson WongNo ratings yet

- Sales Data: Period-1 Period-2 Did We Have An Increase in Sales From Period-1 To Period-2?Document18 pagesSales Data: Period-1 Period-2 Did We Have An Increase in Sales From Period-1 To Period-2?aliNo ratings yet

- Business Plan in EntrepreneurshipDocument10 pagesBusiness Plan in EntrepreneurshipRhealynBalboaLopezNo ratings yet

- FinalDocument20 pagesFinalMaryamNo ratings yet

- Team Wakanda PowerPoint Business ProposalDocument11 pagesTeam Wakanda PowerPoint Business ProposalAlNo ratings yet

- SwasDocument28 pagesSwasAnusha ShinuNo ratings yet

- Managerial EcononicsDocument7 pagesManagerial Econonicsjay1ar1guyenaNo ratings yet

- Micro Eco, Ch-6Document20 pagesMicro Eco, Ch-6Umma Tanila RemaNo ratings yet

- ECON 1012 - ProductionDocument62 pagesECON 1012 - ProductionTami GayleNo ratings yet

- Ratio AnalysisDocument9 pagesRatio Analysisdevilscage1234No ratings yet

- MODULE 3 CVP ANALYSIS - GROUP 2 AE6 Strategic Business AnalysisDocument5 pagesMODULE 3 CVP ANALYSIS - GROUP 2 AE6 Strategic Business AnalysisJaime PalizardoNo ratings yet

- Chapter: Firms in Competitive MarketsDocument42 pagesChapter: Firms in Competitive MarketsSazzad Hossain SakibNo ratings yet

- Oligopoly and Cournot ModelDocument10 pagesOligopoly and Cournot ModelBerk YAZARNo ratings yet

- Profits and Perfect Competition: (Unit VI.i Problem Set Answers)Document12 pagesProfits and Perfect Competition: (Unit VI.i Problem Set Answers)nguyen tuanhNo ratings yet

- Valuation of Business: CA Aaditya JainDocument3 pagesValuation of Business: CA Aaditya JainSunita YadavNo ratings yet

- Eportfolio Micro EconomicsDocument10 pagesEportfolio Micro Economicsapi-352017375No ratings yet

- Model - SuperChemDocument8 pagesModel - SuperChemJash LakhanpalNo ratings yet

- Chapter 9+10+11 - Revision QuestionsDocument23 pagesChapter 9+10+11 - Revision QuestionszonkezintlanuzembetaNo ratings yet

- Short Run EquilibriumDocument5 pagesShort Run EquilibriumGhosty RoastyNo ratings yet

- Chapter 5 CVP Analysis-1Document29 pagesChapter 5 CVP Analysis-1Ummay HabibaNo ratings yet

- Chapter 8 - How Firms Make Decisions: Profit Maximization Answers To Even-Numbered ProblemsDocument3 pagesChapter 8 - How Firms Make Decisions: Profit Maximization Answers To Even-Numbered Problemshussnain tararNo ratings yet

- CH 4Document21 pagesCH 4JAPNo ratings yet

- Chapter 11 Valuation Common StockDocument39 pagesChapter 11 Valuation Common StockHùng PhanNo ratings yet

- Practice 8 - ECON1010Document12 pagesPractice 8 - ECON1010sonNo ratings yet

- Lecture 4-1Document33 pagesLecture 4-1ChristopherNo ratings yet

- Sowing Growth: Master of Arts in Law and Diplomacy Capstone ProjectDocument40 pagesSowing Growth: Master of Arts in Law and Diplomacy Capstone ProjectChristopherNo ratings yet

- LESSON Myths of Entr. ShipDocument15 pagesLESSON Myths of Entr. ShipChristopherNo ratings yet

- Lecture 13 11 - 15Document30 pagesLecture 13 11 - 15ChristopherNo ratings yet

- Lecture 12 11 - 10Document26 pagesLecture 12 11 - 10ChristopherNo ratings yet

- Tech and InnovationDocument6 pagesTech and InnovationChristopherNo ratings yet

- Instructor: Melissa Knox Knoxm@uw - Edu 10/29/2016Document33 pagesInstructor: Melissa Knox Knoxm@uw - Edu 10/29/2016sumanT9No ratings yet

- Econ 200, Autumn 2016Document30 pagesEcon 200, Autumn 2016ChristopherNo ratings yet

- Lecture 7 10 - 20Document23 pagesLecture 7 10 - 20ChristopherNo ratings yet

- Lecture 9 10 - 27Document27 pagesLecture 9 10 - 27ChristopherNo ratings yet

- Lecture 5Document32 pagesLecture 5ChristopherNo ratings yet

- Entrepreneurship and Communication-1Document275 pagesEntrepreneurship and Communication-1ChristopherNo ratings yet

- Lecture 8 10 - 25Document26 pagesLecture 8 10 - 25ChristopherNo ratings yet

- Lecture 6Document36 pagesLecture 6ChristopherNo ratings yet

- Entrepreneurship and Communication-1Document275 pagesEntrepreneurship and Communication-1ChristopherNo ratings yet

- Human Resource Management Practices and Firm PerfoDocument16 pagesHuman Resource Management Practices and Firm PerfoChristopherNo ratings yet

- 04 Barrena-MartinezDocument16 pages04 Barrena-MartinezChristopherNo ratings yet

- Entrepreneurship and Communication-1Document275 pagesEntrepreneurship and Communication-1ChristopherNo ratings yet

- Funai Labour Economics I Eco 213 Lecture NotesDocument78 pagesFunai Labour Economics I Eco 213 Lecture NotesChristopherNo ratings yet

- Role of Human Resource Management Strategy in Organizational Performance in KenyaDocument7 pagesRole of Human Resource Management Strategy in Organizational Performance in KenyaChristopherNo ratings yet

- HR - Bcom HBC 2104 Introduction To MicroeconomicsDocument13 pagesHR - Bcom HBC 2104 Introduction To MicroeconomicsChristopherNo ratings yet

- Topic 1 - Introduction To Labour Economics: Professor H.J. Schuetze Economics 370Document16 pagesTopic 1 - Introduction To Labour Economics: Professor H.J. Schuetze Economics 370kindalemNo ratings yet

- HRM Practices and Employee Performance in Agricultural SectorDocument7 pagesHRM Practices and Employee Performance in Agricultural SectorOIRCNo ratings yet

- Business Plan SampleDocument14 pagesBusiness Plan Samplekothanzawoo1979No ratings yet

- Entrepreneurship and Communication-1Document275 pagesEntrepreneurship and Communication-1ChristopherNo ratings yet

- HBH 2402 PR NotesDocument26 pagesHBH 2402 PR NotesChristopherNo ratings yet

- Effects of Reward Management On Employee PerformanceDocument65 pagesEffects of Reward Management On Employee PerformanceChristopherNo ratings yet

- HRM Practices and Employee Performance in Agricultural SectorDocument7 pagesHRM Practices and Employee Performance in Agricultural SectorOIRCNo ratings yet

- Entrepreneurship Business PlanDocument13 pagesEntrepreneurship Business PlanChristopherNo ratings yet

- Cost & Management Accounting - MGT402 Power Point Slides Lecture 22Document10 pagesCost & Management Accounting - MGT402 Power Point Slides Lecture 22AnsariRiazNo ratings yet

- Lecture 4 - Insurance Company Operations (FULL)Document31 pagesLecture 4 - Insurance Company Operations (FULL)Ziyi YinNo ratings yet

- Containment ZonesDocument25 pagesContainment ZoneslilprofcragzNo ratings yet

- NEA TitleDocument21 pagesNEA TitlejdjNo ratings yet

- LindbeckDocument48 pagesLindbeckMartin JacquesNo ratings yet

- Service Leader Development Program: Agustus 2021Document76 pagesService Leader Development Program: Agustus 2021Ichwan Ramdhani AriefNo ratings yet

- Case 3 - Group 5, Section 2Document8 pagesCase 3 - Group 5, Section 2sd_tataNo ratings yet

- Femip Instruments enDocument4 pagesFemip Instruments enValter SilvaNo ratings yet

- Ps 3Document5 pagesPs 3Phong TrNo ratings yet

- Candlestick Pattern & Chart Pattern 1.0Document61 pagesCandlestick Pattern & Chart Pattern 1.0Akib khan90% (21)

- LP Philco Enero27 22Document38 pagesLP Philco Enero27 22jose floresNo ratings yet

- Financial Management Theory and Practice An Asia 1St Edition Brigham Test Bank Full Chapter PDFDocument45 pagesFinancial Management Theory and Practice An Asia 1St Edition Brigham Test Bank Full Chapter PDFMeganPrestonceim100% (12)

- Ac312, Assignment 1, Dela CruzDocument4 pagesAc312, Assignment 1, Dela CruzChelsea Dela CruzNo ratings yet

- Baptisms 27th Jul 1879 To 3rd Dec 1909 by DateDocument219 pagesBaptisms 27th Jul 1879 To 3rd Dec 1909 by Dateapi-20829797650% (4)

- Trade Bodies PDFDocument121 pagesTrade Bodies PDFSharjeel AshrafNo ratings yet

- Lecture 2 - Statement of Comprehensive IncomeDocument52 pagesLecture 2 - Statement of Comprehensive IncomeGonzalo Jr. RualesNo ratings yet

- Pestel Analysis of ZaraDocument3 pagesPestel Analysis of ZaraZain AliNo ratings yet

- Trade Lic-2021-2024Document1 pageTrade Lic-2021-2024Sadam KhanNo ratings yet

- 21st Century LiteratureDocument9 pages21st Century LiteratureNolan NolanNo ratings yet

- Richard Pieris Exports PLCDocument9 pagesRichard Pieris Exports PLCDPH ResearchNo ratings yet

- A Project Report ON Derivatives: Submitted ToDocument34 pagesA Project Report ON Derivatives: Submitted ToAnu PillaiNo ratings yet

- Notification - Transmission Charges For DICs - Billing Month - August - 2021Document34 pagesNotification - Transmission Charges For DICs - Billing Month - August - 2021Yogesh MuleNo ratings yet

- UCSP Economic Institutions and Market TransactionsDocument36 pagesUCSP Economic Institutions and Market TransactionsApple Biacon-CahanapNo ratings yet

- Chapter# 5 Accounting Transaction CycleDocument16 pagesChapter# 5 Accounting Transaction CycleMuhammad IrshadNo ratings yet

- RV Capital Letter 2019-06Document10 pagesRV Capital Letter 2019-06Rocco HuangNo ratings yet

- Final Assessment - Introduction To Economics - 05082021Document1 pageFinal Assessment - Introduction To Economics - 05082021TabishNo ratings yet

- Problem 1: Problem 9: Problem 17:: SolutionDocument9 pagesProblem 1: Problem 9: Problem 17:: SolutionJacob SantosNo ratings yet

- Naskah Soal PPU English QuizDocument6 pagesNaskah Soal PPU English Quizmiftahul faridNo ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document2 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)Mian EnterprisesNo ratings yet

- Film Budget Template StudioBinderDocument41 pagesFilm Budget Template StudioBinderDavid AzoulayNo ratings yet