You might also like

- Stock Pitch: Walt Disney Co.: Sector: Consumer Services Industry: Media Conglomerate S Nyse: Dis Target Price: $127.28Document13 pagesStock Pitch: Walt Disney Co.: Sector: Consumer Services Industry: Media Conglomerate S Nyse: Dis Target Price: $127.28Zoe HanNo ratings yet

- The Military Orders: Maurice KeenDocument293 pagesThe Military Orders: Maurice KeenRaul-Alexandru TodikaNo ratings yet

- PWC Executing Successful IpoDocument13 pagesPWC Executing Successful Ipolalitkumar_itmbmNo ratings yet

- KPMG Fs Quarterly Newsletter q1 2020Document10 pagesKPMG Fs Quarterly Newsletter q1 2020VineetNo ratings yet

- Agritech PsebDocument20 pagesAgritech PsebJilani HussainNo ratings yet

- Runspree Dashboard Feb 22-Feb 26Document1 pageRunspree Dashboard Feb 22-Feb 26whyNo ratings yet

- Telematics DataDocument19 pagesTelematics DataRenauld SNo ratings yet

- 9 Annual Early Stage Venture Investing Conference: "What Do We Do Now?"Document17 pages9 Annual Early Stage Venture Investing Conference: "What Do We Do Now?"Growth2009No ratings yet

- An Overview of Private Equity Investing in Emerging MarketsDocument20 pagesAn Overview of Private Equity Investing in Emerging MarketsDavid KeresztesNo ratings yet

- Annual Report 202021Document128 pagesAnnual Report 202021AiswaryaNo ratings yet

- Contabilidad DepresiacionDocument23 pagesContabilidad Depresiacionjav nsnaNo ratings yet

- Runspree Dashboard Feb 22-Feb 26Document1 pageRunspree Dashboard Feb 22-Feb 26whyNo ratings yet

- 2015 Annual VC Valuations and Trends Report Excel FINALDocument61 pages2015 Annual VC Valuations and Trends Report Excel FINALrm7029No ratings yet

- Calculos de Cuotas en AmortzDocument19 pagesCalculos de Cuotas en AmortzMauricio NacionalNo ratings yet

- Runspree DashboardDocument1 pageRunspree DashboardfugoNo ratings yet

- Analysis of IT SectorDocument25 pagesAnalysis of IT SectorIshu SainiNo ratings yet

- Analysis of IT SectorDocument25 pagesAnalysis of IT SectorIshu SainiNo ratings yet

- Gujrat Ambuja ExportsDocument29 pagesGujrat Ambuja Exportsjai626545No ratings yet

- 10 D2 S4 JPaul EarmarkingDocument22 pages10 D2 S4 JPaul EarmarkingThinkingPinoyNo ratings yet

- Titan Financial ModelDocument15 pagesTitan Financial Modelyadhu krishnaNo ratings yet

- Time To Exit & IPOs - PitchBook - 1H - 2016Document14 pagesTime To Exit & IPOs - PitchBook - 1H - 2016Arthur CahuantziNo ratings yet

- CPR The-Evolution-of-Indias-Welfare-System-from-2008-2023Document23 pagesCPR The-Evolution-of-Indias-Welfare-System-from-2008-2023rrajesh31No ratings yet

- Annual Report 202021Document128 pagesAnnual Report 202021fddNo ratings yet

- Web Marketing - FarfetchDocument20 pagesWeb Marketing - FarfetchMafalda AntunesNo ratings yet

- F Wall Street 4-JNJ-Analysis (2009)Document1 pageF Wall Street 4-JNJ-Analysis (2009)smith_raNo ratings yet

- SUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeDocument37 pagesSUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeleoharshadNo ratings yet

- Pagos InformaticaDocument5 pagesPagos Informaticaetny.riveraNo ratings yet

- The Progressive Coporation: Asset Turnover Rate of 2007-2012 Year Total Asset Total Revenue Asset Turnover RateDocument2 pagesThe Progressive Coporation: Asset Turnover Rate of 2007-2012 Year Total Asset Total Revenue Asset Turnover RateZhichang ZhangNo ratings yet

- Book 1Document4 pagesBook 1PianoOfDawn 121No ratings yet

- Content MathDocument18 pagesContent MathChristopher Madronal100% (1)

- Venture Capital Update: Andy White Analysis ManagerDocument21 pagesVenture Capital Update: Andy White Analysis Managermarcmyomyint1663No ratings yet

- MSFT - 2012 - ModelDocument46 pagesMSFT - 2012 - ModelSAHEB SAHANo ratings yet

- Broadcom Networking Overview - For JP Morgan-20210111-FINALDocument33 pagesBroadcom Networking Overview - For JP Morgan-20210111-FINALMohsen GoodarziNo ratings yet

- YouGov - Vietnam e Commerce Overall Trends - Dec20 - 6Document39 pagesYouGov - Vietnam e Commerce Overall Trends - Dec20 - 6Diem QuynhNo ratings yet

- F Wall Street 4-MSFT-Analysis (2010) 20100817Document1 pageF Wall Street 4-MSFT-Analysis (2010) 20100817smith_raNo ratings yet

- Nanosonics-AR2020 Web PDFDocument108 pagesNanosonics-AR2020 Web PDFjo moNo ratings yet

- Nanosonics-AR2020 Web PDFDocument108 pagesNanosonics-AR2020 Web PDFjo moNo ratings yet

- 2019 - BDS Analytics Top 10 Trends 2019 PDFDocument63 pages2019 - BDS Analytics Top 10 Trends 2019 PDFluishberriooNo ratings yet

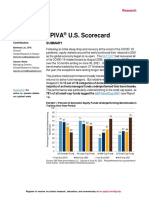

- Spiva Us Mid Year 2021Document36 pagesSpiva Us Mid Year 2021Gábor ZsédelyNo ratings yet

- Tabla AmortizacionDocument12 pagesTabla AmortizacionKarol Nataly PEREZ CALCETONo ratings yet

- SSI Earnings-Release 3Q2020Document13 pagesSSI Earnings-Release 3Q2020Hoàng HiệpNo ratings yet

- HKTDC MzU3OTAyNjA4 enDocument10 pagesHKTDC MzU3OTAyNjA4 enweiqin chenNo ratings yet

- Princeton BCFDocument40 pagesPrinceton BCFHajjiNo ratings yet

- WWW Lme Com en GB Metals Ferrous HRC FOB China#TabIndex 2Document3 pagesWWW Lme Com en GB Metals Ferrous HRC FOB China#TabIndex 2Karya BangunanNo ratings yet

- Sea Aud Dea Ipo Market Report 2021Document24 pagesSea Aud Dea Ipo Market Report 2021Sassi BaltiNo ratings yet

- Ex TemplateDocument37 pagesEx Templatenarunsingla123No ratings yet

- 2018 Eurobank Market ReportDocument24 pages2018 Eurobank Market ReportDeva RajaNo ratings yet

- Wipro SFM - CIA1.1 2Document12 pagesWipro SFM - CIA1.1 2Saloni Jain 1820343No ratings yet

- Performance Analysis ofDocument13 pagesPerformance Analysis ofUjjwalNo ratings yet

- Gmo Resources Strategy: FactsDocument2 pagesGmo Resources Strategy: FactsOwm Close CorporationNo ratings yet

- Corr Case StudiesDocument5 pagesCorr Case StudiesPrashant ChavanNo ratings yet

- Unilever Charts 2018Document17 pagesUnilever Charts 2018Lala BananaNo ratings yet

- Goldman Sachs - Weekly Fund Flows The Selling AcceleratesDocument9 pagesGoldman Sachs - Weekly Fund Flows The Selling AcceleratesRoadtosuccessNo ratings yet

- Impact of Multinational CorporationsDocument18 pagesImpact of Multinational CorporationsPhyo han kyaw PhillipNo ratings yet

- Study - Id89667 - Fintech in Asia PacificDocument77 pagesStudy - Id89667 - Fintech in Asia PacificAditiNo ratings yet

- TowerCo DeckDocument28 pagesTowerCo DeckThiruchelvapalanNo ratings yet

- Servay (Good) Cookies Inflight (7 - 10 March 2019), Mas WingDocument4 pagesServay (Good) Cookies Inflight (7 - 10 March 2019), Mas Wingwanzul31No ratings yet

- Microbiome Investment Dossier: June 01, 2020Document24 pagesMicrobiome Investment Dossier: June 01, 2020janismedNo ratings yet

- Msft-Clean 1Document13 pagesMsft-Clean 1api-580098249No ratings yet

- Capstone Food Beverage MA Coverage Report - Q1 2018 - 1Document8 pagesCapstone Food Beverage MA Coverage Report - Q1 2018 - 1IleanaNo ratings yet

- Complete Study of Employee Stock Ownership Plans Esop 1688222946Document9 pagesComplete Study of Employee Stock Ownership Plans Esop 1688222946Jayant JoshiNo ratings yet

- Ifrs 9 Example Lifetime ECL Trade Receivables Provision Matrix 01Document2 pagesIfrs 9 Example Lifetime ECL Trade Receivables Provision Matrix 01Jayant JoshiNo ratings yet

- Manju Bala's MOOT COURT ProjectDocument34 pagesManju Bala's MOOT COURT ProjectJayant JoshiNo ratings yet

- Retire in Style 1705842394Document20 pagesRetire in Style 1705842394Jayant JoshiNo ratings yet

- WhitePaper - Guide To Adopting Best Practices & Digitalisation of Accounts PayableDocument17 pagesWhitePaper - Guide To Adopting Best Practices & Digitalisation of Accounts PayableJayant JoshiNo ratings yet

- Maha Raksha Supreme 110N102V03 TCDocument18 pagesMaha Raksha Supreme 110N102V03 TCJayant JoshiNo ratings yet

- ICICI Prudential LifeDocument671 pagesICICI Prudential LifeReTHINK INDIANo ratings yet

- National Evaluation Series: Score ReportDocument8 pagesNational Evaluation Series: Score ReportChris NewsomNo ratings yet

- Supply Chain Resilience Definition Review and Theoretical Foundations For Further StudyDocument33 pagesSupply Chain Resilience Definition Review and Theoretical Foundations For Further StudyUmang SoniNo ratings yet

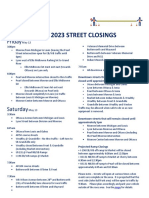

- 2023 Amway River Bank Run Street ClosingsDocument1 page2023 Amway River Bank Run Street ClosingsWXMINo ratings yet

- India Quiz: by Ganesh Shankar & Mohit MohanDocument112 pagesIndia Quiz: by Ganesh Shankar & Mohit MohansaswataboniNo ratings yet

- CoC - A Handful of DustDocument42 pagesCoC - A Handful of DustMikiNo ratings yet

- Modul English Aviation X SMST.1Document8 pagesModul English Aviation X SMST.1ravena putriNo ratings yet

- " Retraction of Jose P. Rizal ": Taguig City University College of CriminologyDocument4 pages" Retraction of Jose P. Rizal ": Taguig City University College of CriminologyMica MellizoNo ratings yet

- PRPC Rule Config Clist 33Document13 pagesPRPC Rule Config Clist 33Ekta ParabNo ratings yet

- Body Language and GesturesDocument3 pagesBody Language and GesturesGel BalaNo ratings yet

- Supplementary Financial Information (31 December 2020)Document71 pagesSupplementary Financial Information (31 December 2020)YoungRedNo ratings yet

- 236 12 Chapter Wise Govt Public Questions emDocument98 pages236 12 Chapter Wise Govt Public Questions emAnonymous d4pycHhcNo ratings yet

- Application Form: Plan International CambodiaDocument5 pagesApplication Form: Plan International CambodiaSong KeoNo ratings yet

- Max Life Online Term Plan Policy WordingsDocument14 pagesMax Life Online Term Plan Policy WordingsMandeep Paul SinghNo ratings yet

- UBC399 Syllabus Spring NabasnyDocument23 pagesUBC399 Syllabus Spring Nabasnyjnabasny1No ratings yet

- Standard Software PackagesDocument68 pagesStandard Software PackagesChukwu EmmanuelNo ratings yet

- Scrip Game Online, Browsing Sosmed, Youtube, Download Scrip by Ega Chanel V.4.5Document38 pagesScrip Game Online, Browsing Sosmed, Youtube, Download Scrip by Ega Chanel V.4.5abdur rohmanNo ratings yet

- Chapter 1 Not-For-Profit OrganizationDocument54 pagesChapter 1 Not-For-Profit OrganizationDivyansh ThakurNo ratings yet

- Heidegger and The Grammar of BeingDocument13 pagesHeidegger and The Grammar of BeingtrelteopetNo ratings yet

- Semi Lesson PlanDocument2 pagesSemi Lesson Planfigelyn adlawanNo ratings yet

- Lecture 8 - Modern PhysicsDocument16 pagesLecture 8 - Modern PhysicsSaad Shabbir100% (3)

- Design OptimizationDocument12 pagesDesign OptimizationNam VoNo ratings yet

- 59, Case Transferred To District of South Carolina US (Szymoniak) V AceDocument7 pages59, Case Transferred To District of South Carolina US (Szymoniak) V Acelarry-612445No ratings yet

- Oracle Certification ProgramDocument6 pagesOracle Certification ProgramVlada MladenovicNo ratings yet

- Chapter 8 - Between-Subjects DesignDocument17 pagesChapter 8 - Between-Subjects DesignSumendra RathoreNo ratings yet

- q4 Week 3 5 WHLP EappDocument3 pagesq4 Week 3 5 WHLP EappNathaniel Mark Versoza FormenteraNo ratings yet

- Likutei Ohr: Parshat NoachDocument2 pagesLikutei Ohr: Parshat Noachoutdash2No ratings yet

- Reguland Irreg VerbsDocument5 pagesReguland Irreg VerbsJose Victor Loayza AcostaNo ratings yet

- HardwareDocument30 pagesHardwareSonali SinghNo ratings yet