You might also like

- Oil Strategy - The Conviction ListDocument23 pagesOil Strategy - The Conviction ListBLBVORTEXNo ratings yet

- Fs SP 500 Utilities SectorDocument6 pagesFs SP 500 Utilities SectorBLBVORTEXNo ratings yet

- Ziopharm Slides To Accompany Q3 2019 Call 110719 FinalDocument13 pagesZiopharm Slides To Accompany Q3 2019 Call 110719 FinalBLBVORTEXNo ratings yet

- Blackrockgold Presentation July-3Document26 pagesBlackrockgold Presentation July-3BLBVORTEXNo ratings yet

- DVAX Coporate Presentation Strong Buy...Document26 pagesDVAX Coporate Presentation Strong Buy...BLBVORTEXNo ratings yet

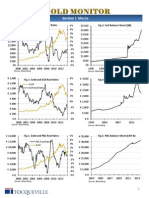

- Tocqueville Gold Monitor 4Q 2013Document11 pagesTocqueville Gold Monitor 4Q 2013Gold Silver WorldsNo ratings yet

- CIMB Navigating Thailand 2015 Dec 2014 PDFDocument212 pagesCIMB Navigating Thailand 2015 Dec 2014 PDFBLBVORTEXNo ratings yet

- BTG Petrobras January 2015Document7 pagesBTG Petrobras January 2015BLBVORTEXNo ratings yet

- Sarepta JPM 2019 FinalDocument26 pagesSarepta JPM 2019 FinalBLBVORTEXNo ratings yet

- BIS Working Papers 2Document35 pagesBIS Working Papers 2AdminAliNo ratings yet

- GloomBoomDoom Report Monetary TectonicsDocument4 pagesGloomBoomDoom Report Monetary TectonicsBLBVORTEXNo ratings yet

- KPMG China Pharmaceutical 201106Document62 pagesKPMG China Pharmaceutical 201106merc2No ratings yet

- CAPR ARM Investor DayDocument19 pagesCAPR ARM Investor DayBLBVORTEXNo ratings yet

- Current Tanker RatesSept12Document3 pagesCurrent Tanker RatesSept12BLBVORTEXNo ratings yet

- Neuralstem+Corporate+Presentation+website October+2014Document32 pagesNeuralstem+Corporate+Presentation+website October+2014BLBVORTEXNo ratings yet

- India Agriculture Inputs Seeds of Prosperity 26-02-14!15!05Document87 pagesIndia Agriculture Inputs Seeds of Prosperity 26-02-14!15!05BLBVORTEX100% (1)

- VIPS 2Q13 Post Earnings PresentationDocument28 pagesVIPS 2Q13 Post Earnings PresentationBLBVORTEXNo ratings yet

- Copper Mountain August 2014 Corp PresDocument29 pagesCopper Mountain August 2014 Corp PresBLBVORTEXNo ratings yet

- Commodities Update - CIBC - Dec 2Document8 pagesCommodities Update - CIBC - Dec 2BLBVORTEXNo ratings yet

- Sucden Financial Quarterly Metals Report October 2013Document60 pagesSucden Financial Quarterly Metals Report October 2013BLBVORTEXNo ratings yet

- IndiapharmaDocument151 pagesIndiapharmaBLBVORTEXNo ratings yet

- Philips Securities 2013 China Macroeconomic Semiannual Report 130726Document5 pagesPhilips Securities 2013 China Macroeconomic Semiannual Report 130726BLBVORTEXNo ratings yet

- CLSA Greed Fear 1 August 2013Document13 pagesCLSA Greed Fear 1 August 2013BLBVORTEXNo ratings yet

- Greater China Smartphone Sector 130904Document52 pagesGreater China Smartphone Sector 130904BLBVORTEXNo ratings yet

- Occ Asional Paper Series: China'S Economic Growth and RebalancingDocument56 pagesOcc Asional Paper Series: China'S Economic Growth and RebalancingRupojit RoyNo ratings yet

- UBS Research Focus, Sustainable Investing, July 2013.Document40 pagesUBS Research Focus, Sustainable Investing, July 2013.Glenn ViklundNo ratings yet

- OEl Gas LatAmDocument76 pagesOEl Gas LatAmBLBVORTEXNo ratings yet

- Strategy Bocom June 2013Document6 pagesStrategy Bocom June 2013BLBVORTEXNo ratings yet

- Asia Pacific Equities Malaysia May 8th 2013Document7 pagesAsia Pacific Equities Malaysia May 8th 2013BLBVORTEXNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Project On Online e PayDocument49 pagesProject On Online e PayAmaan RazviNo ratings yet

- Bressani Real Estate - Short Sale Listing Presentation 1-12-11Document14 pagesBressani Real Estate - Short Sale Listing Presentation 1-12-11Steve Bressani0% (1)

- KIA SELTOS BookingDocketDocument7 pagesKIA SELTOS BookingDocketNeelNo ratings yet

- 3 Day Cycle - Day 2. PART 2Document12 pages3 Day Cycle - Day 2. PART 2CristóbalTobalNo ratings yet

- Sip Project RutujaDocument16 pagesSip Project Rutujapsourabh638No ratings yet

- Swot QuizDocument1 pageSwot Quizdkenneth rbalimbin100% (1)

- CORPORATE FINANCE - Chap 11Document4 pagesCORPORATE FINANCE - Chap 11Nguyễn T. Anh Minh100% (1)

- Money (Rupiahs)Document5 pagesMoney (Rupiahs)Indarwati Siska PertiwiNo ratings yet

- Nationalization of Ethiopia's Bank of IssueDocument16 pagesNationalization of Ethiopia's Bank of IssueChinmoy MishraNo ratings yet

- Engineering Management 3 - OrganisingDocument87 pagesEngineering Management 3 - Organisingtk techboyNo ratings yet

- T0 2022-2023 MS FA - WorkbookDocument18 pagesT0 2022-2023 MS FA - WorkbookZhuozhi WuNo ratings yet

- Compound AmountDocument68 pagesCompound AmountKEYDAVE ARNADONo ratings yet

- Inventory Mgt: Concepts, Motives & ObjectivesDocument5 pagesInventory Mgt: Concepts, Motives & ObjectivesEKANSH DANGAYACH 20212619No ratings yet

- Black BookDocument26 pagesBlack BookYash soshteNo ratings yet

- Nöz Social & Search Strategy: (Mehraael Sawers) (08/05/2023)Document22 pagesNöz Social & Search Strategy: (Mehraael Sawers) (08/05/2023)api-704773576No ratings yet

- Accounting of DepreciationDocument9 pagesAccounting of DepreciationPrasad BhanageNo ratings yet

- British Charity Accounting Standards ImpactDocument24 pagesBritish Charity Accounting Standards ImpactTareq Yousef AbualajeenNo ratings yet

- Cash Flow and Capital Investment in Textile IndustryDocument76 pagesCash Flow and Capital Investment in Textile IndustryMuktadir BillahNo ratings yet

- Bank Charter Act 1844 - enDocument15 pagesBank Charter Act 1844 - enMaxBestNo ratings yet

- Charter - Diego SaldariniDocument2 pagesCharter - Diego SaldariniCuneyt CelikNo ratings yet

- Format CBFT - Pagos ExteriorDocument9 pagesFormat CBFT - Pagos ExteriorCarlos PasosNo ratings yet

- InvoiceDocument1 pageInvoice10-XII-Sci-A Saima ChoudharyNo ratings yet

- Primerica CredibilityDocument4 pagesPrimerica CredibilityMichael RoyNo ratings yet

- Iso9001 Germany Quality Management System 2024-08-30Document37 pagesIso9001 Germany Quality Management System 2024-08-30DISTRIBUCIONES ESFERA SA DE CV0% (1)

- Resources, Conservation and RecyclingDocument9 pagesResources, Conservation and RecyclingAsma Hairulla JaafarNo ratings yet

- Project Report UrjaDocument16 pagesProject Report Urjashubham jagtapNo ratings yet

- QualificationDocument536 pagesQualificationrajaa El ansariNo ratings yet

- Union Bank 1Document12 pagesUnion Bank 1bindu mathaiNo ratings yet

- Ferma-Sustainability 2021 FinalDocument24 pagesFerma-Sustainability 2021 FinalNeniNo ratings yet

- PPE Accounting for Apparel ManufacturerDocument4 pagesPPE Accounting for Apparel ManufacturerTeo ShengNo ratings yet