You might also like

- ERM - Experience From Japanese CompanyDocument38 pagesERM - Experience From Japanese CompanyNguyen Quoc HuyNo ratings yet

- MM Foundation of Risk Management V1Document12 pagesMM Foundation of Risk Management V1Imran MobinNo ratings yet

- STRICTLY PRIVATE and CONFIDENTIAL ChiefDocument56 pagesSTRICTLY PRIVATE and CONFIDENTIAL ChiefFaidz FuadNo ratings yet

- Chapter 2 - Risk DefinitionDocument25 pagesChapter 2 - Risk DefinitionVishwajit GoudNo ratings yet

- Understanding Risks in BankingDocument68 pagesUnderstanding Risks in BankingDharmendra PillaiNo ratings yet

- Business Finance 1 NotesDocument62 pagesBusiness Finance 1 Notessanu sayedNo ratings yet

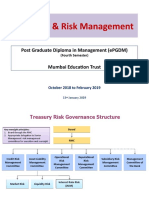

- Treasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Document10 pagesTreasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Jitendra YadavNo ratings yet

- Class IV-FinanceDocument19 pagesClass IV-FinanceVinayak RaoNo ratings yet

- FRR-ALM Ch4Document66 pagesFRR-ALM Ch4Marek KurzyńskiNo ratings yet

- Risk Management and Basel II: Indian Institute of Banking and FinanceDocument31 pagesRisk Management and Basel II: Indian Institute of Banking and FinanceKaran AsraniNo ratings yet

- RM For Cooperatives PICPA 2015Document70 pagesRM For Cooperatives PICPA 2015Rheneir MoraNo ratings yet

- 2.5 CC Trade ReceivablesDocument36 pages2.5 CC Trade ReceivablesDaefnate KhanNo ratings yet

- Risk Management For IFIsDocument192 pagesRisk Management For IFIsxymaan100% (1)

- Managing Cash & Investment (EY)Document12 pagesManaging Cash & Investment (EY)Anil KumarNo ratings yet

- 2identifying LRDocument44 pages2identifying LRFaizan KarimNo ratings yet

- ECGCDocument19 pagesECGCSOUVIK ROY MBA 2021-23 (Delhi)No ratings yet

- Board RAS Summary TemplateDocument10 pagesBoard RAS Summary Templateamit100% (1)

- GD20503 Financial Markets & InstitutionsDocument37 pagesGD20503 Financial Markets & InstitutionsWindyee TanNo ratings yet

- Financial Intermediation: Over Come ItDocument53 pagesFinancial Intermediation: Over Come ItDharmendra PillaiNo ratings yet

- Instructional Video Intro To Foundations of RiskDocument16 pagesInstructional Video Intro To Foundations of RiskVinod TPNo ratings yet

- Introduction To Treasury and Funds Management 27-11-2018Document51 pagesIntroduction To Treasury and Funds Management 27-11-2018faisal_sarwar82No ratings yet

- Fra Merged PDFDocument336 pagesFra Merged PDFSubhadip SinhaNo ratings yet

- Risk Appetite in Banking: Steve Townsend Tesco BankDocument15 pagesRisk Appetite in Banking: Steve Townsend Tesco BankrakhalbanglaNo ratings yet

- RVMS Risk and Value Measurement ServicesDocument67 pagesRVMS Risk and Value Measurement Services林木田No ratings yet

- Aon Risk Services Australia Limited: Ian JonesDocument29 pagesAon Risk Services Australia Limited: Ian JonesGarry HouseNo ratings yet

- Know Risk: Enterprise Credit Risk Management Framework For Economic & Regulatory CapitalDocument31 pagesKnow Risk: Enterprise Credit Risk Management Framework For Economic & Regulatory Capitalrubencito1No ratings yet

- HW#14 Ch9Document18 pagesHW#14 Ch9Young-Hun KimNo ratings yet

- Capital Market Fundamentals SummaryDocument7 pagesCapital Market Fundamentals SummaryIolandaNo ratings yet

- ALM Risk ManagementDocument42 pagesALM Risk ManagementIbnu NugrohoNo ratings yet

- The Business, Tax, and Financial Environments The Business, Tax, and Financial EnvironmentsDocument14 pagesThe Business, Tax, and Financial Environments The Business, Tax, and Financial EnvironmentsahspilotNo ratings yet

- Financial Markets and InstitutionsDocument11 pagesFinancial Markets and InstitutionsEarl Daniel RemorozaNo ratings yet

- Risk Management Analytics for Building a Risk WarehouseDocument118 pagesRisk Management Analytics for Building a Risk WarehouseJJNo ratings yet

- Mutual Funds Hedge Funds Description/ActivitiesDocument7 pagesMutual Funds Hedge Funds Description/ActivitiesSherlock HolmesNo ratings yet

- Progress of The Process: Cost and STP in Today's DC FundsDocument36 pagesProgress of The Process: Cost and STP in Today's DC Funds2imediaNo ratings yet

- Class Notes Financial Risk M: F PGDMDocument11 pagesClass Notes Financial Risk M: F PGDMprat05No ratings yet

- Course II "International Financial Markets and Institutions"Document22 pagesCourse II "International Financial Markets and Institutions"Valentina OlteanuNo ratings yet

- A Manual of Hedging Commodity Price Risk For CorporatesDocument23 pagesA Manual of Hedging Commodity Price Risk For CorporatesDavid GibsonNo ratings yet

- Treasury ManagementDocument108 pagesTreasury Managementchinmoymishra100% (1)

- Risk CrisilDocument21 pagesRisk Crisilapi-3833893No ratings yet

- Asset-Liability Management Core for BanksDocument9 pagesAsset-Liability Management Core for Bankssnigdha biswasNo ratings yet

- Corporate Profile at a GlanceDocument21 pagesCorporate Profile at a Glancekanikak97No ratings yet

- Banking 09 Capital Funding MGMT v2Document101 pagesBanking 09 Capital Funding MGMT v2Fuyao MiNo ratings yet

- Lbex-Docid 194031Document27 pagesLbex-Docid 194031Pamela MabizaNo ratings yet

- Investments - Background and Issues: Financial Versus Real AssetsDocument5 pagesInvestments - Background and Issues: Financial Versus Real AssetsLex Acads100% (1)

- Chapter 1Document30 pagesChapter 1FinanceNo ratings yet

- An Alternative Opportunity Set For Absolute Return Outcomes Global Institutional White Paper Part 1 of 2Document24 pagesAn Alternative Opportunity Set For Absolute Return Outcomes Global Institutional White Paper Part 1 of 2Liu BoscoNo ratings yet

- Lecture 2Document19 pagesLecture 2Pubg KrNo ratings yet

- Chap 1 Theories of FI PDFDocument48 pagesChap 1 Theories of FI PDFDharmendra PillaiNo ratings yet

- Equity: MarketsDocument113 pagesEquity: MarketsBurhanudin BurhanudinNo ratings yet

- IAIS Investment Risk Management ASSALDocument28 pagesIAIS Investment Risk Management ASSALAbhishek YadavNo ratings yet

- AZ Specialty Credit SolutionsDocument6 pagesAZ Specialty Credit Solutionstony BNo ratings yet

- Risk Management in MiningDocument48 pagesRisk Management in Miningpuput utomo100% (1)

- Equity Investment 1 - Securities MarketDocument36 pagesEquity Investment 1 - Securities Marketnur syahirah bt ab.rahmanNo ratings yet

- Merchant Banking and Financial ServicesDocument16 pagesMerchant Banking and Financial ServicesAaziya ANo ratings yet

- RE Capital Markets 6.9 330pDocument82 pagesRE Capital Markets 6.9 330pAirollNo ratings yet

- Asset Management CompaniesDocument8 pagesAsset Management CompaniesPalak AgarwalNo ratings yet

- The Simple Rules of Risk: Revisiting the Art of Financial Risk ManagementFrom EverandThe Simple Rules of Risk: Revisiting the Art of Financial Risk ManagementNo ratings yet

- Audit of The Inventory and Warehousing CycleDocument54 pagesAudit of The Inventory and Warehousing CycleIbnu NugrohoNo ratings yet

- 09 Internal ControlsDocument15 pages09 Internal ControlsIbnu NugrohoNo ratings yet

- ALM HartfordDocument16 pagesALM HartfordIbnu NugrohoNo ratings yet

- ALM Risk ManagementDocument42 pagesALM Risk ManagementIbnu NugrohoNo ratings yet

- ALM Life InsuranceDocument22 pagesALM Life InsuranceIbnu NugrohoNo ratings yet

- Asset Liability Management & Model Building: Heshy SummerDocument21 pagesAsset Liability Management & Model Building: Heshy SummerIbnu Nugroho100% (1)

- ALM DividenDocument16 pagesALM DividenIbnu NugrohoNo ratings yet

- ALM Duration to Solvency 2Document33 pagesALM Duration to Solvency 2Ibnu NugrohoNo ratings yet

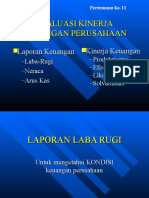

- Evaluasi Kinerja Keuangan PerusahaanDocument59 pagesEvaluasi Kinerja Keuangan PerusahaanIbnu NugrohoNo ratings yet

- MCQ - Project ManagementDocument301 pagesMCQ - Project ManagementAnshul BhallaNo ratings yet

- Viet lai cau sửa học sinhDocument7 pagesViet lai cau sửa học sinhahmad amdaNo ratings yet

- Determination of Forward and Futures PricesDocument40 pagesDetermination of Forward and Futures PricesKaushik BhattacharjeeNo ratings yet

- Genmath-3rd Quarter SummativeDocument3 pagesGenmath-3rd Quarter SummativeJENESA BAGUIONo ratings yet

- Treasury Securities in BangladeshDocument12 pagesTreasury Securities in BangladeshAmit KumarNo ratings yet

- Instant Download Ebook PDF Fundamentals of Corporate Finance 5th Canadian Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance 5th Canadian Edition PDF Scribdlauryn.corbett387100% (42)

- Chapter 22 Real Options: Corporate Finance, 3E (Berk/Demarzo)Document27 pagesChapter 22 Real Options: Corporate Finance, 3E (Berk/Demarzo)asdfghjkl007No ratings yet

- CA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDocument4 pagesCA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDhruv AgarwalNo ratings yet

- Unit 2 - Bank PassbookDocument34 pagesUnit 2 - Bank PassbookNandini PartaniNo ratings yet

- Institute of Actuaries of India: ExaminationsDocument7 pagesInstitute of Actuaries of India: ExaminationsRahul IyerNo ratings yet

- Au Ia1 Midterm ExamDocument4 pagesAu Ia1 Midterm ExamCherrylane EdicaNo ratings yet

- Inflation: Its Causes, Effects, and Social Costs: MacroeconomicsDocument61 pagesInflation: Its Causes, Effects, and Social Costs: MacroeconomicsTai612No ratings yet

- Group Assignment Cover Sheet: Student DetailsDocument9 pagesGroup Assignment Cover Sheet: Student DetailsMinh DucNo ratings yet

- Unit 3 FM (Ebit-Eps Analysis)Document4 pagesUnit 3 FM (Ebit-Eps Analysis)Sahil KadyanNo ratings yet

- Amended RBPF PolicyDocument2 pagesAmended RBPF Policynfk roeNo ratings yet

- Maths - Core-WorksheetsDocument122 pagesMaths - Core-WorksheetsML MLNo ratings yet

- The Evaluation of Credit Union Non-Maturity DepositsDocument84 pagesThe Evaluation of Credit Union Non-Maturity DepositsAnouar AichaNo ratings yet

- MODULE 2 Business FinanceDocument16 pagesMODULE 2 Business FinanceWinshei CaguladaNo ratings yet

- Corporate Finance Prof. Auh analyzes bond pricesDocument13 pagesCorporate Finance Prof. Auh analyzes bond prices신동호100% (1)

- AssignmentDocument16 pagesAssignmentSABORDO, MA. KRISTINA COLEENNo ratings yet

- Mundell-Fleming Model ExplainedDocument4 pagesMundell-Fleming Model Explainedavani devNo ratings yet

- Calculate WACC and Cost of EquityDocument1 pageCalculate WACC and Cost of EquitysauravNo ratings yet

- 20201213-Statements-9476 - (1) - UnlockedDocument4 pages20201213-Statements-9476 - (1) - UnlockedHamza AzamNo ratings yet

- Chapter 10Document32 pagesChapter 10REEMA BNo ratings yet

- Duration vs Convexity in Bond Portfolio ManagementDocument10 pagesDuration vs Convexity in Bond Portfolio ManagementMilton ChinhoroNo ratings yet

- General Math AssessmentDocument2 pagesGeneral Math AssessmentKristel CahiligNo ratings yet

- Accounting Quick Lesson1Document1 pageAccounting Quick Lesson1listenkidNo ratings yet

- FINC521-Most Important QuestionsDocument24 pagesFINC521-Most Important QuestionsAll rounder NitinNo ratings yet

- 14.02 Principles of Macroeconomics Fall 2004: Quiz 3 Thursday, December 2, 2004 7:30 PM - 9 PMDocument15 pages14.02 Principles of Macroeconomics Fall 2004: Quiz 3 Thursday, December 2, 2004 7:30 PM - 9 PMHassam ShahidNo ratings yet

- Loan Agreement 21Document74 pagesLoan Agreement 21befaj44984No ratings yet