You might also like

- 2022 KATALOG Nogara Sa Cijenama PDFDocument6 pages2022 KATALOG Nogara Sa Cijenama PDFAsmirr9No ratings yet

- 6 Inch Welding ReportsDocument6 pages6 Inch Welding Reportsatulpatil99No ratings yet

- Certificat 610Document1 pageCertificat 610Madalin Breda MadalinNo ratings yet

- WhatsApp Image 2024-04-21 at 4.26.48 PMDocument2 pagesWhatsApp Image 2024-04-21 at 4.26.48 PMMahesh JampalaNo ratings yet

- Adobe Scan 11 May 2023Document1 pageAdobe Scan 11 May 2023Su SiNo ratings yet

- 'Illin O: - Be Onducted BLLLCD For LT M of /quantity Conat. Staf StaffDocument1 page'Illin O: - Be Onducted BLLLCD For LT M of /quantity Conat. Staf StaffMahendar ErramNo ratings yet

- CO Cations: L OT RT IDocument12 pagesCO Cations: L OT RT IAlex A. Candari JrNo ratings yet

- T) 1ect: Vyrm Fy1Document3 pagesT) 1ect: Vyrm Fy1Ichal ZuhdyNo ratings yet

- Zns-Preparation-Pdf 29-Oct-2022 09-41-19Document5 pagesZns-Preparation-Pdf 29-Oct-2022 09-41-19Cristians VivasNo ratings yet

- 209454-226497 Stirling-Map-2015Document2 pages209454-226497 Stirling-Map-2015api-376565807No ratings yet

- Img 0002Document1 pageImg 0002khairun nissaNo ratings yet

- Adobe Scan 14 Feb 2022 PDFDocument6 pagesAdobe Scan 14 Feb 2022 PDFSanjiv GuptaNo ratings yet

- Atlas AB 804M 1090Document16 pagesAtlas AB 804M 1090Николай НекрасовNo ratings yet

- Scan 27 Jan. 2018Document5 pagesScan 27 Jan. 2018PkNo ratings yet

- CHP 9 Embedded SystemDocument6 pagesCHP 9 Embedded SystemDubbing MasterNo ratings yet

- UntitledDocument2 pagesUntitlednitudNo ratings yet

- Pages From 2010 EW Certs Brady To CaoDocument56 pagesPages From 2010 EW Certs Brady To CaoJoshtaxpayerNo ratings yet

- Lecture 3a. Introduction To Load Flow Analysis and Gauss SeidelDocument88 pagesLecture 3a. Introduction To Load Flow Analysis and Gauss Seidelwakolesha TadeoNo ratings yet

- WhatsApp Image 2022-02-21 at 14.36.38Document1 pageWhatsApp Image 2022-02-21 at 14.36.38Cristian PmazzoNo ratings yet

- Spectroscopy ContinuationDocument2 pagesSpectroscopy ContinuationDeepak KauthankarNo ratings yet

- Adobe Scan 24 Oct 2023Document1 pageAdobe Scan 24 Oct 2023gangaurassociates1No ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Maharashtra State Co.: Electricity Distribution LTDDocument1 pageMaharashtra State Co.: Electricity Distribution LTDSamay GadaNo ratings yet

- FILE - 20220310 - 172732 - Adobe Scan 10 THG 3, 2022Document3 pagesFILE - 20220310 - 172732 - Adobe Scan 10 THG 3, 202219Lê Quốc HùngNo ratings yet

- Pla, Sits Stttina:: - Physics I.Ab (XP (RJ Ient TL Rectilinear IotioDocument6 pagesPla, Sits Stttina:: - Physics I.Ab (XP (RJ Ient TL Rectilinear IotioOmar HamdanNo ratings yet

- Rlrraei: '., - Tt:-Es0.LDocument1 pageRlrraei: '., - Tt:-Es0.LandrewNo ratings yet

- Type He Wide Rudder Angle Repeat Back Unit Operator's ManualDocument6 pagesType He Wide Rudder Angle Repeat Back Unit Operator's ManualClarence ClarNo ratings yet

- BK91-1318-01-FSF-000-PIP-RFI-0029 Request For Inspection of Carbon Steel Pipe Material - SignedDocument293 pagesBK91-1318-01-FSF-000-PIP-RFI-0029 Request For Inspection of Carbon Steel Pipe Material - SignedPanneer SelvamNo ratings yet

- PI&D MEOA Storage A3formatDocument1 pagePI&D MEOA Storage A3formatAbhishek AwasthiNo ratings yet

- SCF Till 11janDocument18 pagesSCF Till 11janPriyanshu KumarNo ratings yet

- Diamond City Epaper 378Document60 pagesDiamond City Epaper 378vanditNo ratings yet

- Book 15 Dec 2023Document10 pagesBook 15 Dec 2023ipurchase799No ratings yet

- Work & EnergyDocument5 pagesWork & EnergyJahn CruzNo ratings yet

- Crushing TestDocument4 pagesCrushing TestDeepakNo ratings yet

- BMS34L00183Document2 pagesBMS34L00183Rohit Parmar (Computer Operator, Bangalore)No ratings yet

- Exp 8-10 Dld. LabDocument16 pagesExp 8-10 Dld. LabMohit YadavNo ratings yet

- ME 09 403 MOS 2011 JuneDocument2 pagesME 09 403 MOS 2011 JuneDhruve EBNo ratings yet

- Loading Effect On Po T: L EarDocument24 pagesLoading Effect On Po T: L EarmohanNo ratings yet

- Aamal Zikir HajiAbdulWahabBhaiDocument25 pagesAamal Zikir HajiAbdulWahabBhaiZyan TahsanNo ratings yet

- Ehs - 14001-2015Document23 pagesEhs - 14001-2015Nav TalukdarNo ratings yet

- PBX Dizit Translation Tabie: Office Data Lotpbx (1 /1) EDocument6 pagesPBX Dizit Translation Tabie: Office Data Lotpbx (1 /1) Ersingh2020No ratings yet

- L I L, Hol, Eq I If Nu Le F Ick: LonurnDocument1 pageL I L, Hol, Eq I If Nu Le F Ick: Lonurnjackim123No ratings yet

- Koolhaas Rem Delirious New York A Retroactive Manifesto For Manhattan PDFDocument321 pagesKoolhaas Rem Delirious New York A Retroactive Manifesto For Manhattan PDFInês LopesNo ratings yet

- Stock Audit NewDocument4 pagesStock Audit NewItsmebroNo ratings yet

- Lloyd 1Document1 pageLloyd 1iffatNo ratings yet

- Leasing ProblemsDocument11 pagesLeasing ProblemsAbhishek AbhiNo ratings yet

- Millsheet Siku Krakatau SteelDocument16 pagesMillsheet Siku Krakatau SteelMellany SeprinaNo ratings yet

- ABC AnalysisDocument3 pagesABC Analysisvjpalan081No ratings yet

- Schenck: Dados Tipo de Rotc:NteDocument4 pagesSchenck: Dados Tipo de Rotc:NteAntonio Marcos Dos SantosNo ratings yet

- Centrifugal Pump Drives For Boiler Feed Service: Lin KaoDocument8 pagesCentrifugal Pump Drives For Boiler Feed Service: Lin KaoramakantinamdarNo ratings yet

- Avenger MarchDocument26 pagesAvenger Marchjoseph allen soNo ratings yet

- Ac Circuits 1 PDFDocument24 pagesAc Circuits 1 PDFJhay Phee LlorenteNo ratings yet

- FBH Inspection ReportDocument1 pageFBH Inspection Reportaakash jangalwalaNo ratings yet

- VOLTAS Wall Mounted Air Conditioners USER MANUAL (Inverter Series)Document20 pagesVOLTAS Wall Mounted Air Conditioners USER MANUAL (Inverter Series)Ravindu Gamage100% (3)

- Emsd1 001 97Document1 pageEmsd1 001 97jackim123No ratings yet

- Copia Foii Matricole PDFDocument1 pageCopia Foii Matricole PDFEcaterina CurzacNo ratings yet

- Tnc 135 Точка По ТочкаDocument21 pagesTnc 135 Точка По ТочкаaLexusNo ratings yet

- E X Ercises: ExercisesDocument3 pagesE X Ercises: ExercisesPamelaDeLacruzZavalaNo ratings yet

- GeneralLuna2017 Audit Report-UnlockedDocument105 pagesGeneralLuna2017 Audit Report-UnlockedJ JaNo ratings yet

- Reviewer For 2nd Eval Auditing Theory Answer KeyDocument11 pagesReviewer For 2nd Eval Auditing Theory Answer KeyadssdasdsadNo ratings yet

- Law On Obligations and Contracts Quiz Bee Round 1 EasyDocument6 pagesLaw On Obligations and Contracts Quiz Bee Round 1 EasyadssdasdsadNo ratings yet

- Issuance Vested in "Higher Court.'' - The Issuance of The Writ Is Expressly Vested by ArticleDocument6 pagesIssuance Vested in "Higher Court.'' - The Issuance of The Writ Is Expressly Vested by ArticleadssdasdsadNo ratings yet

- Activity Ratio Influence On Profitability (At The Mining Company Listed in Indonesia Stock Exchange Period 2010-2013)Document23 pagesActivity Ratio Influence On Profitability (At The Mining Company Listed in Indonesia Stock Exchange Period 2010-2013)adssdasdsadNo ratings yet

- 10576-Article Text-41055-3-10-20191228 PDFDocument9 pages10576-Article Text-41055-3-10-20191228 PDFadssdasdsadNo ratings yet

- Impact of An Excise Tax On The Consumption of Sugar-Sweetened Beverages in Young People Living in Poorer Neighbourhoods of Catalonia, Spain: A Difference in Differences StudyDocument11 pagesImpact of An Excise Tax On The Consumption of Sugar-Sweetened Beverages in Young People Living in Poorer Neighbourhoods of Catalonia, Spain: A Difference in Differences StudyadssdasdsadNo ratings yet

- The Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityDocument15 pagesThe Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityadssdasdsadNo ratings yet

- Preweek Practical Accounting 2-21Document1 pagePreweek Practical Accounting 2-21adssdasdsadNo ratings yet

- An Initial Look at The TRAIN Law Are WeDocument20 pagesAn Initial Look at The TRAIN Law Are WeadssdasdsadNo ratings yet

- Preweek Practical Accounting 2-24Document1 pagePreweek Practical Accounting 2-24adssdasdsadNo ratings yet

- Preweek Practical Accounting 2-20Document1 pagePreweek Practical Accounting 2-20adssdasdsadNo ratings yet

- Virginia Wanjiku Mwangi Mba 2019Document87 pagesVirginia Wanjiku Mwangi Mba 2019adssdasdsadNo ratings yet

- COE by Sir OcampoDocument22 pagesCOE by Sir OcampoadssdasdsadNo ratings yet

- Chapter 1 To 4-3Document1 pageChapter 1 To 4-3adssdasdsadNo ratings yet

- Chapter 1 To 4-1Document1 pageChapter 1 To 4-1adssdasdsadNo ratings yet

- Water Wonders, Inc., Ocean Adventures Makers of Custom-Made Jet Skis, TheDocument3 pagesWater Wonders, Inc., Ocean Adventures Makers of Custom-Made Jet Skis, Thelaale dijaanNo ratings yet

- Commonly Used Tables For QueryDocument4 pagesCommonly Used Tables For QueryKunwarNo ratings yet

- Indian Process IndustryDocument7 pagesIndian Process Industryankushgup_agNo ratings yet

- PartnershipDocument9 pagesPartnershipGrace A. ManaloNo ratings yet

- April20 BusinessFinanceDocument3 pagesApril20 BusinessFinanceADRIANO, Glecy C.75% (8)

- Study Guide 2: Part One-Identifying Accounting TermsDocument4 pagesStudy Guide 2: Part One-Identifying Accounting TermsMr. IntelNo ratings yet

- Chawla Parties Upto 14 Jan-19Document104 pagesChawla Parties Upto 14 Jan-19mudassar nazarNo ratings yet

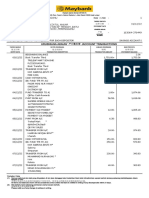

- Commercial Bank of Ethiopia: Account StatementDocument27 pagesCommercial Bank of Ethiopia: Account StatementSamuel Abebe60% (5)

- p2 - Guerrero Ch17Document19 pagesp2 - Guerrero Ch17JerichoPedragosa100% (2)

- B. S&OP Larri Lapide PDFDocument33 pagesB. S&OP Larri Lapide PDFDAVID CARMONANo ratings yet

- Myebpp PDFDownload WSPDFType E0 B2 FX2 Qu 1 BVSCXHHOLn 0 Yg 3 D3 D&Merchant Yn H2 B4 Ekh Fa NU9 SPH 5 W JKWW 3 D3 D&Document3 pagesMyebpp PDFDownload WSPDFType E0 B2 FX2 Qu 1 BVSCXHHOLn 0 Yg 3 D3 D&Merchant Yn H2 B4 Ekh Fa NU9 SPH 5 W JKWW 3 D3 D&삽sabrinaNo ratings yet

- 2008 CPIM Exam Content ManualDocument58 pages2008 CPIM Exam Content ManualelmozzNo ratings yet

- BIAYA: Konsep, Klasifikasi Dan PerilakuDocument48 pagesBIAYA: Konsep, Klasifikasi Dan PerilakuAziz SugihartoNo ratings yet

- Far1 Chapter 2Document63 pagesFar1 Chapter 2Erik NavarroNo ratings yet

- Reinforcement Activity 1 Financial Statement Amp WorksheetsDocument12 pagesReinforcement Activity 1 Financial Statement Amp Worksheetsapi-33442031249% (35)

- 02 BIR RegistrationDocument1 page02 BIR RegistrationJonel TorresNo ratings yet

- Balance SheetDocument7 pagesBalance SheetKashyap PandyaNo ratings yet

- Variable and Absorption Costing ActivityDocument4 pagesVariable and Absorption Costing ActivityRendyel PagariganNo ratings yet

- Tugas AKL - Pertemuan 10Document43 pagesTugas AKL - Pertemuan 10KA-5-BILQIS KHOERUNISANo ratings yet

- FromBaru ByChannelByDepo (REVISI) 2010Document62 pagesFromBaru ByChannelByDepo (REVISI) 2010aniNo ratings yet

- EDI 850 X12 SampleDocument6 pagesEDI 850 X12 Samplearajesh07No ratings yet

- ACCT 60100 - Fall 2020 - Pioneer October Case Solution - Presentation PDFDocument12 pagesACCT 60100 - Fall 2020 - Pioneer October Case Solution - Presentation PDFTruckNo ratings yet

- F & F PETY BILL PL Makwana 8.22Document9 pagesF & F PETY BILL PL Makwana 8.22Prakash MakwanaNo ratings yet

- Type Date Num Name Memo Split Amount Paid Bill Adj Pend Bal. 51000 Utilities 51010 Building ElectricityDocument2 pagesType Date Num Name Memo Split Amount Paid Bill Adj Pend Bal. 51000 Utilities 51010 Building ElectricityMonica DiazNo ratings yet

- Report 20230520163354Document23 pagesReport 20230520163354Akhil KumarNo ratings yet

- Chapter 03 Systems Design Job-Order CostingDocument38 pagesChapter 03 Systems Design Job-Order CostingFarihaNo ratings yet

- Corporate Financial Accounting 14th Edition Warren Solutions Manual 1Document89 pagesCorporate Financial Accounting 14th Edition Warren Solutions Manual 1john100% (36)

- ACC1002X Optional Questions - SOLUTIONS CHP 2Document6 pagesACC1002X Optional Questions - SOLUTIONS CHP 2edisonctrNo ratings yet

- Accounting AssignmentDocument6 pagesAccounting AssignmentBabe Shane LauronNo ratings yet

- Analisis Penerapan Metode Full Costing Dalam Perhitungan Harga Pokok Produksi Untuk Penetapan Harga JualDocument6 pagesAnalisis Penerapan Metode Full Costing Dalam Perhitungan Harga Pokok Produksi Untuk Penetapan Harga Jualindonesia haiNo ratings yet