You might also like

- Salient Features of The Companies Act 2013Document24 pagesSalient Features of The Companies Act 2013Ajay RoyNo ratings yet

- Index: 2. Memorandum of Company 3. Steps in Incorporation of A Company 4. Certificate of Incorporation 5. ConclusionDocument8 pagesIndex: 2. Memorandum of Company 3. Steps in Incorporation of A Company 4. Certificate of Incorporation 5. ConclusionSahil SaharanNo ratings yet

- Company-Law Concise NotesDocument40 pagesCompany-Law Concise NotesIcap Frtwo100% (4)

- MCQ's Question Bank on Company Law ConceptsDocument41 pagesMCQ's Question Bank on Company Law ConceptsManju Bubna90% (10)

- BUSINESS AND ENVIRONMENT: HOW BUSINESSES RELY ON LIMITED RESOURCESDocument132 pagesBUSINESS AND ENVIRONMENT: HOW BUSINESSES RELY ON LIMITED RESOURCESCalvin Zhuwau100% (3)

- Companies Act defines Section 8 companiesDocument45 pagesCompanies Act defines Section 8 companiesAmit SinghNo ratings yet

- Company Law Lecture NotesDocument47 pagesCompany Law Lecture NotesMandy Neoh76% (17)

- Company SecretaryDocument52 pagesCompany Secretaryirshad_cb100% (2)

- Project Report On Comparative Analysis of Public and Private Sector Steel Companies in IndiaDocument48 pagesProject Report On Comparative Analysis of Public and Private Sector Steel Companies in IndiaHillary RobinsonNo ratings yet

- CompaniesDocument258 pagesCompaniesBhagwan BachaiNo ratings yet

- Unit 2 Company LawDocument34 pagesUnit 2 Company LawPriya SekarNo ratings yet

- Unit 1Document27 pagesUnit 1GITANJALI MISHRANo ratings yet

- Lab Study Note-2021Document78 pagesLab Study Note-2021elizabeth shrutiNo ratings yet

- Business Law Campany ActDocument30 pagesBusiness Law Campany ActSimple WaltarNo ratings yet

- Companies Act 2013Document102 pagesCompanies Act 2013vallamdas007No ratings yet

- Company Law Unit - 1Document22 pagesCompany Law Unit - 1Anjali ShuklaNo ratings yet

- Company Law & Secretarial PracticeDocument13 pagesCompany Law & Secretarial PracticecitiNo ratings yet

- Module 5Document39 pagesModule 5you • were • trolledNo ratings yet

- Lab - Study Note - 1-MergedDocument84 pagesLab - Study Note - 1-MergedAAYUSH MODI IPM 2020 -25 BatchNo ratings yet

- Company LawDocument32 pagesCompany LawAnnonymous JoggerNo ratings yet

- Assignment On Company LawDocument15 pagesAssignment On Company Lawতাসমুন ইসলাম প্রান্তNo ratings yet

- Overview On The Companies Act, 1994Document44 pagesOverview On The Companies Act, 1994Tawsif MahbubNo ratings yet

- Company LawDocument9 pagesCompany LawSayyad Seenan AhmadNo ratings yet

- Company and FormationDocument24 pagesCompany and FormationSneha RochlaniNo ratings yet

- UNIT-4 Companies Act, 1956 (Part-I) : The Characteristics of The CompanyDocument11 pagesUNIT-4 Companies Act, 1956 (Part-I) : The Characteristics of The CompanyČhâïthü ChaithuNo ratings yet

- Corporate Law: Memorandum of AssociationDocument13 pagesCorporate Law: Memorandum of AssociationAnadi GuptaNo ratings yet

- Lab - Corporate Law, Competition Law & Consumer LawDocument37 pagesLab - Corporate Law, Competition Law & Consumer Lawbella cullenNo ratings yet

- MemorandumDocument9 pagesMemorandumJay RamNo ratings yet

- Companies Act 2013 provisions on OPC, small companies, dormant companies and women directorsDocument6 pagesCompanies Act 2013 provisions on OPC, small companies, dormant companies and women directorsGunjan LalwaniNo ratings yet

- Tata Group's Holding and Subsidiary StructureDocument41 pagesTata Group's Holding and Subsidiary StructureVanshdeep Singh SamraNo ratings yet

- 1.introduction, Features & Formation of CopaniesDocument35 pages1.introduction, Features & Formation of CopaniesIshan GuptaNo ratings yet

- Companies Act 2013: Key Features and TypesDocument7 pagesCompanies Act 2013: Key Features and TypesMohit RanaNo ratings yet

- Assignment of AsadDocument51 pagesAssignment of Asadsujan paulNo ratings yet

- Definition of key company law terms under 40 charactersDocument2 pagesDefinition of key company law terms under 40 characters18-UCO-327 Naveen Kumar.DNo ratings yet

- Genesis of The Companies ACT, 1956:: The Main Objects and Purposes of Statutes Relating To Companies Are As FollowsDocument49 pagesGenesis of The Companies ACT, 1956:: The Main Objects and Purposes of Statutes Relating To Companies Are As FollowsAriful Hassan SaikatNo ratings yet

- Business Law - Utkarsh BalamwarDocument6 pagesBusiness Law - Utkarsh BalamwarMamta BalamwarNo ratings yet

- Kinds of CompaniesDocument3 pagesKinds of CompaniesPadmasree HarishNo ratings yet

- Process of Company IncorporationDocument16 pagesProcess of Company IncorporationManju SujayNo ratings yet

- Classification of Companies (Part-Ii)Document16 pagesClassification of Companies (Part-Ii)Tania MajumderNo ratings yet

- Company: DefinitionDocument6 pagesCompany: DefinitionAnthony BlackNo ratings yet

- Company vs PartnershipDocument20 pagesCompany vs PartnershipSheiryNo ratings yet

- Chapter # 01: Salman Masood SheikhDocument29 pagesChapter # 01: Salman Masood Sheikhsohail merchantNo ratings yet

- company law notesDocument22 pagescompany law notesDeepak KumarNo ratings yet

- Unit No 2Document35 pagesUnit No 2awishNo ratings yet

- Company Law Types of CompanyDocument19 pagesCompany Law Types of CompanyAtulNo ratings yet

- Companies Act 2013 overviewDocument95 pagesCompanies Act 2013 overviewAshesh DasNo ratings yet

- Company Law UpDocument95 pagesCompany Law UpAshesh DasNo ratings yet

- Types of Legal Business Structure in IndiaDocument18 pagesTypes of Legal Business Structure in IndiaROHAN SHELKENo ratings yet

- Company Law - Unit IDocument61 pagesCompany Law - Unit IHarsh ThakurNo ratings yet

- Regulates Incorporation of A CompanyDocument11 pagesRegulates Incorporation of A CompanySandip SenNo ratings yet

- Introduction to Company Incorporation ProcessDocument6 pagesIntroduction to Company Incorporation ProcessOmama ArifNo ratings yet

- Introduction To Corporate AccountingDocument32 pagesIntroduction To Corporate AccountingshrutiNo ratings yet

- An Indispensable Tool For A Company in MakingDocument4 pagesAn Indispensable Tool For A Company in MakingDHRUV KALIANo ratings yet

- CLTCDocument7 pagesCLTCBasudev SahooNo ratings yet

- Memorandum of Association PRESENTATION (HR)Document30 pagesMemorandum of Association PRESENTATION (HR)gondalsNo ratings yet

- Law AssignmentDocument6 pagesLaw AssignmentaryanNo ratings yet

- MNR College of Engineering & TechnologyDocument38 pagesMNR College of Engineering & TechnologyDJSATYAMNo ratings yet

- The Company Law in India: Urvi Shah Assistant Professor of Law Unitedworld School of LawDocument48 pagesThe Company Law in India: Urvi Shah Assistant Professor of Law Unitedworld School of LawSunil ShawNo ratings yet

- Companies ActDocument107 pagesCompanies ActrohitbatraNo ratings yet

- Topic 1 - Business and ResourcesDocument40 pagesTopic 1 - Business and ResourcesBalachandran RamachandranNo ratings yet

- CLSP 20 MarkDocument16 pagesCLSP 20 Mark18-UCO-327 Naveen Kumar.DNo ratings yet

- What Is A CompanyDocument14 pagesWhat Is A CompanySimple WaltarNo ratings yet

- Mercantile Law NotesDocument21 pagesMercantile Law NotesPriyanka BarikNo ratings yet

- Punjabi University Patiala School of Management StudiesDocument16 pagesPunjabi University Patiala School of Management StudiesPriya SharmaNo ratings yet

- Business Development Business Development: Punjabi University Patiala School of Management StudiesDocument17 pagesBusiness Development Business Development: Punjabi University Patiala School of Management StudiesPriya SharmaNo ratings yet

- Recruitment & Selection ProcessDocument11 pagesRecruitment & Selection ProcessPriya SharmaNo ratings yet

- DR, REDDY LABORATORIES LTD. (Pitch Book)Document8 pagesDR, REDDY LABORATORIES LTD. (Pitch Book)Priya SharmaNo ratings yet

- Business Development Business Development: Punjabi University Patiala School of Management StudiesDocument13 pagesBusiness Development Business Development: Punjabi University Patiala School of Management StudiesPriya SharmaNo ratings yet

- Submitted By: Swati Sharma (1074) Hardeep Kaur (1068) Arshdeep Kaur (1091)Document14 pagesSubmitted By: Swati Sharma (1074) Hardeep Kaur (1068) Arshdeep Kaur (1091)Priya SharmaNo ratings yet

- A Seminar Report On Human Resource Development With Special To IndiaDocument16 pagesA Seminar Report On Human Resource Development With Special To IndiaPriya SharmaNo ratings yet

- Business Development Business Development: Punjabi University Patiala School of Management StudiesDocument14 pagesBusiness Development Business Development: Punjabi University Patiala School of Management StudiesPriya SharmaNo ratings yet

- HRD in IndiaDocument21 pagesHRD in IndiaPriya SharmaNo ratings yet

- Transportation Problem: Maximize Z 3x + 2x2Document4 pagesTransportation Problem: Maximize Z 3x + 2x2Priya SharmaNo ratings yet

- Assignment of Honda Activa 2Document10 pagesAssignment of Honda Activa 2Priya SharmaNo ratings yet

- Swati Sharma.1074Document2 pagesSwati Sharma.1074Priya SharmaNo ratings yet

- Selection Test: Name-Swati Sharma Roll No - 20421074 Class-MBADocument4 pagesSelection Test: Name-Swati Sharma Roll No - 20421074 Class-MBAPriya SharmaNo ratings yet

- Swati Sharma ApplicationDocument1 pageSwati Sharma ApplicationPriya SharmaNo ratings yet

- A Seminar Report On Human Resource Development With Special To IndiaDocument16 pagesA Seminar Report On Human Resource Development With Special To IndiaPriya SharmaNo ratings yet

- Assignment of Honda Activa 2Document10 pagesAssignment of Honda Activa 2Priya SharmaNo ratings yet

- Swati Sharma ApplicationDocument1 pageSwati Sharma ApplicationPriya SharmaNo ratings yet

- Practical 8 and Practical 9Document6 pagesPractical 8 and Practical 9Priya SharmaNo ratings yet

- Brand AwarnessDocument79 pagesBrand AwarnessPriya SharmaNo ratings yet

- Assignment of Honda Activa 2Document10 pagesAssignment of Honda Activa 2Priya SharmaNo ratings yet

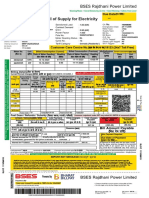

- Bill of Supply For Electricity: BSES Rajdhani Power LimitedDocument2 pagesBill of Supply For Electricity: BSES Rajdhani Power LimitedPriya SharmaNo ratings yet

- Distribution and Sales of Financial Products and Analysis of Working Capital Management of Shriram Fortune Solutions LimitedDocument49 pagesDistribution and Sales of Financial Products and Analysis of Working Capital Management of Shriram Fortune Solutions LimitedMohammad ShoebNo ratings yet

- Questionnaire of Honda Activa Jiten & BhavikDocument5 pagesQuestionnaire of Honda Activa Jiten & BhavikBhavik Jariwala78% (9)

- Summary of Pollution and Waste ManagementDocument3 pagesSummary of Pollution and Waste ManagementPriya SharmaNo ratings yet

- Plotting Curves and Solving Differential EquationsDocument61 pagesPlotting Curves and Solving Differential EquationsPriya SharmaNo ratings yet

- Questionnaire On FMCGDocument3 pagesQuestionnaire On FMCGfadi78660% (10)

- Job Satisfaction: Bharath Sanchar Nigam LimitedDocument41 pagesJob Satisfaction: Bharath Sanchar Nigam Limitedomkar jokeNo ratings yet

- Questionnaire of Honda Activa Jiten & BhavikDocument5 pagesQuestionnaire of Honda Activa Jiten & BhavikBhavik Jariwala78% (9)

- M.E Assignment (Fruits and Vegetable) 20421075 Sec. (B)Document20 pagesM.E Assignment (Fruits and Vegetable) 20421075 Sec. (B)Priya SharmaNo ratings yet

- Mangerial Accounting Assignment 1Document4 pagesMangerial Accounting Assignment 1Nidhi ShahNo ratings yet

- Wetherly PDFDocument30 pagesWetherly PDFMirasol DagondonNo ratings yet

- Transfer and Transmission of SharesDocument4 pagesTransfer and Transmission of SharesParul KhannaNo ratings yet

- FIJI LAW SOCIETY - Companies Bill Submission 070415Document9 pagesFIJI LAW SOCIETY - Companies Bill Submission 070415Seni NabouNo ratings yet

- Transfer of SharesDocument9 pagesTransfer of SharesamitkmeenaNo ratings yet

- Public Corporations and Government CompaniesDocument5 pagesPublic Corporations and Government CompaniesChetan KumarNo ratings yet

- Managerial App & RemunerationDocument63 pagesManagerial App & RemunerationSaloni SharmaNo ratings yet

- Public Vs Private Company NotesDocument3 pagesPublic Vs Private Company NotesBilal akbarNo ratings yet

- Advantages and Disadvantages of Public CompanyDocument10 pagesAdvantages and Disadvantages of Public CompanyPrasad KumbharNo ratings yet

- 736-Assignment-2 - Group2 2Document38 pages736-Assignment-2 - Group2 2Đoàn Thanh Chúc (FGW HN)No ratings yet

- Company LawDocument45 pagesCompany LawYussone Sir'Yuss67% (3)

- Key Features of A Company 1. Artificial PersonDocument19 pagesKey Features of A Company 1. Artificial PersonVijayaragavan MNo ratings yet

- Multiple Choice Questions on Vietnamese Enterprise LawDocument7 pagesMultiple Choice Questions on Vietnamese Enterprise Lawtrinh tranNo ratings yet

- Securities Markets: Learning ObjectivesDocument31 pagesSecurities Markets: Learning ObjectivesFrancisca FusterNo ratings yet

- Introduction To Companies: Financial Accounting & Reporting 5Document26 pagesIntroduction To Companies: Financial Accounting & Reporting 5athirah jamaludinNo ratings yet

- How to Value Private CompaniesDocument5 pagesHow to Value Private CompaniesJonhmark AniñonNo ratings yet

- Company Accounts - Accounting For Share Capital: Meaning of Key Terms Used in The ChapterDocument52 pagesCompany Accounts - Accounting For Share Capital: Meaning of Key Terms Used in The ChapterHarish RajputNo ratings yet

- MCQ Book - 1 PDFDocument130 pagesMCQ Book - 1 PDFlikithaNo ratings yet

- Differentiate Between Public Company and Private CompanyDocument7 pagesDifferentiate Between Public Company and Private CompanymayankNo ratings yet

- Classes of Corporation Organized Under The RCCDocument3 pagesClasses of Corporation Organized Under The RCCVedia Genon IINo ratings yet

- PrivCo Overview PresentationDocument22 pagesPrivCo Overview Presentationprivco99No ratings yet

- Forms and Formation of Business EnterpriseDocument33 pagesForms and Formation of Business EnterprisedaljitsodhiNo ratings yet

- Nawaz - My India ProjectDocument23 pagesNawaz - My India ProjectriyaNo ratings yet

- Corporate law notes on companies limited by guaranteeDocument7 pagesCorporate law notes on companies limited by guaranteeTayo AkinkuolieNo ratings yet