You might also like

- STEP 1: Setting Up Your UCC Contract Trust Account: (FIRST Package To Treasury)Document2 pagesSTEP 1: Setting Up Your UCC Contract Trust Account: (FIRST Package To Treasury)Jahe El97% (58)

- 5 Moving Average Signals That Beat Buy and Hold Backtested Stock MarketDocument47 pages5 Moving Average Signals That Beat Buy and Hold Backtested Stock MarketJoelNo ratings yet

- Leases Part 3 - Other Accounting IssuesDocument33 pagesLeases Part 3 - Other Accounting IssuesDanica RamosNo ratings yet

- Accounting Unit 1Document75 pagesAccounting Unit 1Huzaifa Abdullah50% (2)

- Cash Flow 05 With Answers Just Give SolutionsDocument21 pagesCash Flow 05 With Answers Just Give SolutionsEdi wow WowNo ratings yet

- BIR Sample Receipts and Invoices - V9 - OpsMemoDocument7 pagesBIR Sample Receipts and Invoices - V9 - OpsMemoYunit M Stariray100% (1)

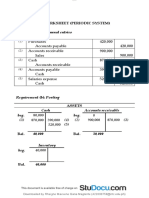

- Work Sheet Moises Dondoyano Information SystemDocument1 pageWork Sheet Moises Dondoyano Information SystemRJ DAVE DURUHA100% (5)

- AHM13e Chapter - 03 - Solution To Problems and Key To CasesDocument24 pagesAHM13e Chapter - 03 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- FP&A Industry Background and Arthayantra's JourneyDocument19 pagesFP&A Industry Background and Arthayantra's JourneyAbhi SangwanNo ratings yet

- Common Size Statement Analysis PDF Notes 1Document10 pagesCommon Size Statement Analysis PDF Notes 124.7upskill Lakshmi V0% (1)

- Income Tax Quiz AnswerDocument4 pagesIncome Tax Quiz AnswerMarco Alejandro Ibay100% (1)

- Lucerna Bacalso Surveyors year-end financial statementsDocument10 pagesLucerna Bacalso Surveyors year-end financial statementsRod80% (10)

- DNB 2018Document178 pagesDNB 2018Sachidananda KiniNo ratings yet

- Financial Feasibility: 4.1 Total Start Up Cash NeededDocument5 pagesFinancial Feasibility: 4.1 Total Start Up Cash NeededAmna Arif100% (1)

- PNB Refuses to Release Real Estate Mortgage After Spouses Ramos Settled Agricultural Loan (37 charactersDocument3 pagesPNB Refuses to Release Real Estate Mortgage After Spouses Ramos Settled Agricultural Loan (37 charactersNadzlah Bandila100% (1)

- Process Plant and Equipment Integrity Management-Module 1Document93 pagesProcess Plant and Equipment Integrity Management-Module 1Naren SukaihNo ratings yet

- Financial Accounting AssignmentsDocument3 pagesFinancial Accounting AssignmentsMemes CreatorNo ratings yet

- Summary of Operating Assumptions (For Example)Document5 pagesSummary of Operating Assumptions (For Example)Krishna SharmaNo ratings yet

- Investment 80000 Cost Reduction 22000 Life 5 Salvage 20000 Tax 21% Discounting Rate 10%Document7 pagesInvestment 80000 Cost Reduction 22000 Life 5 Salvage 20000 Tax 21% Discounting Rate 10%Sneha DasNo ratings yet

- Work Sheet 1 PDFDocument9 pagesWork Sheet 1 PDFProtik SarkarNo ratings yet

- Module 2 Capital Budgeting Handout For LMS 2020Document11 pagesModule 2 Capital Budgeting Handout For LMS 2020sandeshNo ratings yet

- Deferred Tax TutorialDocument2 pagesDeferred Tax Tutorial嘉慧No ratings yet

- Walking Stick For Blind With Sensors: Presented byDocument12 pagesWalking Stick For Blind With Sensors: Presented byAbbas MookhyNo ratings yet

- Ae 112 Prelim Assessment 1Document7 pagesAe 112 Prelim Assessment 1Chelssy ParadoNo ratings yet

- ACCT6005 COMPANY ACCOUNTING ASSESSMENT 2 CASE STUDYDocument8 pagesACCT6005 COMPANY ACCOUNTING ASSESSMENT 2 CASE STUDYRuhan SinghNo ratings yet

- CPA Review School of The Philippines Manila First Pre-Board Solutions TaxationDocument8 pagesCPA Review School of The Philippines Manila First Pre-Board Solutions TaxationLive LoveNo ratings yet

- ACCT 1107 - Assignment #4Document3 pagesACCT 1107 - Assignment #4hkarim8641No ratings yet

- PROBLEM 2-45:: Particulars Case A Case B Case CDocument6 pagesPROBLEM 2-45:: Particulars Case A Case B Case CSrihari KumarNo ratings yet

- Financial Decision Making: Module Code: UMADFJ-15-MDocument9 pagesFinancial Decision Making: Module Code: UMADFJ-15-MFaraz BakhshNo ratings yet

- Srinath SirDocument19 pagesSrinath Sirmy Vinay100% (1)

- Chapter 5Document5 pagesChapter 5bonfaceNo ratings yet

- Downloaded by Rheigne Maxxene Gana Maglente (422000758@ntc - Edu.ph)Document7 pagesDownloaded by Rheigne Maxxene Gana Maglente (422000758@ntc - Edu.ph)RheigneNo ratings yet

- Downloaded by Rheigne Maxxene Gana Maglente (422000758@ntc - Edu.ph)Document7 pagesDownloaded by Rheigne Maxxene Gana Maglente (422000758@ntc - Edu.ph)RheigneNo ratings yet

- California Dispensers Financial StatementsDocument9 pagesCalifornia Dispensers Financial StatementsHarsh MaheshwariNo ratings yet

- CF Assignment 1 Group 4Document41 pagesCF Assignment 1 Group 4Radha DasNo ratings yet

- Sujan Sir Assignment (MBA)Document18 pagesSujan Sir Assignment (MBA)Habibur RahmanNo ratings yet

- Sheet SolutionDocument1 pageSheet Solutionmmh771984No ratings yet

- Corporate FinanceDocument3 pagesCorporate FinanceAdrien PortemontNo ratings yet

- Presentation1 ReshmaDocument26 pagesPresentation1 ReshmaJOE NOBLE 2020519No ratings yet

- Problem 1: Costing and Production ReportDocument5 pagesProblem 1: Costing and Production ReportAya Ben MohamedNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- HO and Branches Combined StatmentDocument5 pagesHO and Branches Combined Statmentmmh771984No ratings yet

- Cash Flow ProblemsDocument10 pagesCash Flow Problemsmuhammad shamsadNo ratings yet

- Financial WorksheetDocument4 pagesFinancial WorksheetCarla GonçalvesNo ratings yet

- Accountin Principals Task 2Document15 pagesAccountin Principals Task 2Thivya KrishnanNo ratings yet

- 2017 BGSS 4E5N Prelim P2 AnsDocument6 pages2017 BGSS 4E5N Prelim P2 AnsDamien SeowNo ratings yet

- IGNOU MCA MCS-035 Free Solved Assignments 2010Document11 pagesIGNOU MCA MCS-035 Free Solved Assignments 2010Deepti SainiNo ratings yet

- Cash Flow QN 3Document4 pagesCash Flow QN 3Takudzwa LanceNo ratings yet

- McReath Original SolutionDocument2 pagesMcReath Original SolutionSuchi0% (1)

- CostingDocument46 pagesCostingRaghav KhakholiaNo ratings yet

- Audit of Intangible AssetsDocument8 pagesAudit of Intangible AssetsHira IdaceiNo ratings yet

- Manufacturing statement and financialsDocument3 pagesManufacturing statement and financialselmudaaNo ratings yet

- Ffa ADocument5 pagesFfa Aaccounts officerNo ratings yet

- Ia T23 AnsDocument2 pagesIa T23 Ansckwai0603No ratings yet

- 2016 PPDocument13 pages2016 PPumeshNo ratings yet

- Profit and Loss Statement For The Y.E. 31.1.20XX Balance Sheet As On 31.1.20XX Income: AssetsDocument4 pagesProfit and Loss Statement For The Y.E. 31.1.20XX Balance Sheet As On 31.1.20XX Income: AssetsSmriti singhNo ratings yet

- Net Sales Cash Accounts Receivable Merchandise Inventory Preapid Expense Property, Palnt, and EquipmentDocument6 pagesNet Sales Cash Accounts Receivable Merchandise Inventory Preapid Expense Property, Palnt, and EquipmentMadina MamasalievaNo ratings yet

- Cost Bookkeeping With AnswersDocument9 pagesCost Bookkeeping With AnswersHafsa HayatNo ratings yet

- Excess Cash or Need To Borrow 111,300 297,600 (155,100) (22,800) 118,500 187,800Document3 pagesExcess Cash or Need To Borrow 111,300 297,600 (155,100) (22,800) 118,500 187,800Marjon0% (1)

- The Financial Model: InputDocument4 pagesThe Financial Model: InputCarla GonçalvesNo ratings yet

- Asset Liability Expenses Income Owner's CapitalDocument4 pagesAsset Liability Expenses Income Owner's Capitalamitmehta29No ratings yet

- AnswersDocument4 pagesAnswersamitmehta29No ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Quiz 3032Document4 pagesQuiz 3032PG93No ratings yet

- Project ACRDocument30 pagesProject ACRMuneeb KhalidNo ratings yet

- FAC2601 Assignment 02Document4 pagesFAC2601 Assignment 02SibongileNo ratings yet

- Fin MathDocument3 pagesFin MathSk. Alifur RahmanNo ratings yet

- B2 2021 Nov AnsDocument13 pagesB2 2021 Nov AnsRashid AbeidNo ratings yet

- Get covered with Corona Rakshak PolicyDocument6 pagesGet covered with Corona Rakshak PolicyAJOONEE AUTO PARTSNo ratings yet

- CRM PresentationDocument16 pagesCRM PresentationNikita SabharwalNo ratings yet

- Sindh Waste To Energy Policy (Swep) 2021Document20 pagesSindh Waste To Energy Policy (Swep) 2021Sadaqat islamNo ratings yet

- This Study Resource Was: Chapter 2 HWDocument4 pagesThis Study Resource Was: Chapter 2 HWJoice BobosNo ratings yet

- Set-Up Reduction in An Interconnection Axle Manufacturing Cell Using SMEDDocument10 pagesSet-Up Reduction in An Interconnection Axle Manufacturing Cell Using SMEDVõ Hồng HạnhNo ratings yet

- Fundamental Security AnalysisDocument21 pagesFundamental Security AnalysisAbhisek ShawNo ratings yet

- April 2022Document316 pagesApril 2022Date AccountNo ratings yet

- SSRN Id4350992Document11 pagesSSRN Id4350992Ctkd teamNo ratings yet

- B170219B BBFN3323 InternationalfinanceDocument23 pagesB170219B BBFN3323 InternationalfinanceLIM JEI XEE BACC18B-1No ratings yet

- Organic Food ChinaDocument36 pagesOrganic Food ChinaSoumyabuddha DebnathNo ratings yet

- Problem Set 2Document2 pagesProblem Set 2Blubb1No ratings yet

- Akuntansi Keuangan Menengah - Chapter 14Document9 pagesAkuntansi Keuangan Menengah - Chapter 14nurul hasanahNo ratings yet

- Case 1 Phuket Beach HotelDocument7 pagesCase 1 Phuket Beach HotelYana Dela CernaNo ratings yet

- Loss of Resources and Reputation from Poor Environmental PracticesDocument2 pagesLoss of Resources and Reputation from Poor Environmental PracticesRockNo ratings yet

- Global Logistics Issues & SolutionsDocument6 pagesGlobal Logistics Issues & SolutionsAllyah Paula PostorNo ratings yet

- Chapter I: Introduction To Applied EconomicsDocument71 pagesChapter I: Introduction To Applied EconomicsNichole Balao-asNo ratings yet

- Be Dru Overview of Ethiopian CooperativesDocument26 pagesBe Dru Overview of Ethiopian CooperativesFisehaNo ratings yet

- Materials JITDocument5 pagesMaterials JITRawr rawrNo ratings yet

- Cash Problems SolutionDocument3 pagesCash Problems SolutionMagadia Mark JeffNo ratings yet

- 04.may 2022Document138 pages04.may 2022Dream creatorsNo ratings yet

- Accounting For MaterialsDocument31 pagesAccounting For Materialsmuriithialex2030No ratings yet