You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Red Hat: When To Apply The Red Hat? Summary of Red HatDocument2 pagesRed Hat: When To Apply The Red Hat? Summary of Red HatNawazish KhanNo ratings yet

- RPG Group employee training to boost sales and customer relationshipsDocument3 pagesRPG Group employee training to boost sales and customer relationshipsNawazish KhanNo ratings yet

- RPG Group employee training to boost sales and customer relationshipsDocument3 pagesRPG Group employee training to boost sales and customer relationshipsNawazish KhanNo ratings yet

- Motivation vs Inspiration - What's the DifferenceDocument4 pagesMotivation vs Inspiration - What's the DifferenceNawazish KhanNo ratings yet

- Didn't Provide Enough Information About Its Testing On Innocent AnimalsDocument1 pageDidn't Provide Enough Information About Its Testing On Innocent AnimalsNawazish KhanNo ratings yet

- Ravi Rao MinicaseDocument7 pagesRavi Rao MinicaseNawazish KhanNo ratings yet

- CH #5Document9 pagesCH #5Abdul wahabNo ratings yet

- HR Analytics in Todays Business.: Made By: Mohd. Nawazish Khan Astha SinhaDocument6 pagesHR Analytics in Todays Business.: Made By: Mohd. Nawazish Khan Astha SinhaNawazish KhanNo ratings yet

- Time Value of Money SumsDocument13 pagesTime Value of Money SumsrahulNo ratings yet

- Attendance Below 60% - MBA Semester-IIIDocument6 pagesAttendance Below 60% - MBA Semester-IIINawazish KhanNo ratings yet

- RTFDocument17 pagesRTFNawazish KhanNo ratings yet

- 372 - Sentence Completion Advanced Level Test Quiz Online Exercise With Answers 4Document5 pages372 - Sentence Completion Advanced Level Test Quiz Online Exercise With Answers 4Nawazish KhanNo ratings yet

- S.No. Name of The Hostel Contact Details' Contact Person Contact No. RemarksDocument2 pagesS.No. Name of The Hostel Contact Details' Contact Person Contact No. RemarksNawazish KhanNo ratings yet

- Pawan Paradkar ResumeDocument2 pagesPawan Paradkar ResumeNawazish KhanNo ratings yet

- Mettur Salem 29112018Document46 pagesMettur Salem 29112018Ar Kethees WaranNo ratings yet

- Hawthorne StudiesDocument7 pagesHawthorne StudiesNawazish KhanNo ratings yet

- ManEco Assignment Disruptive TechsDocument2 pagesManEco Assignment Disruptive TechsNawazish KhanNo ratings yet

- Accessing criminal justice resource filesDocument65 pagesAccessing criminal justice resource filesNawazish KhanNo ratings yet

- Demand ForecastDocument16 pagesDemand ForecastPoonam SatapathyNo ratings yet

- Motivation: Concepts & TheoriesDocument56 pagesMotivation: Concepts & TheoriesNawazish KhanNo ratings yet

- Infosys Accounting PoliciesDocument13 pagesInfosys Accounting PoliciesNawazish KhanNo ratings yet

- Placement Preparation Record - 11-04-2021 To 22-05-2021Document1 pagePlacement Preparation Record - 11-04-2021 To 22-05-2021Nawazish KhanNo ratings yet

- Honda Motorcycle Labor Unrest in 2009Document5 pagesHonda Motorcycle Labor Unrest in 2009Nawazish KhanNo ratings yet

- Organizational Behaviour Session - 1Document45 pagesOrganizational Behaviour Session - 1Nawazish KhanNo ratings yet

- Demand ForecastDocument16 pagesDemand ForecastPoonam SatapathyNo ratings yet

- Demand for Money Function Stability in IndiaDocument29 pagesDemand for Money Function Stability in IndiaNawazish KhanNo ratings yet

- Green FashionDocument1 pageGreen FashionNawazish KhanNo ratings yet

- Manikanta Doki 1486 - IRDocument50 pagesManikanta Doki 1486 - IRNawazish KhanNo ratings yet

- 17.mengistu Zeleke PDFDocument78 pages17.mengistu Zeleke PDFWedi FitwiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

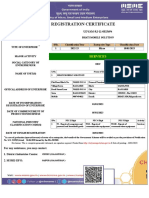

- Print - Udyam Registration CertificateDocument1 pagePrint - Udyam Registration CertificatelalitpooniaNo ratings yet

- CP Shipping Desk 2018Document18 pagesCP Shipping Desk 2018Farid OMARINo ratings yet

- Subject - An Application For The Post of JR - Executive (Merchandising)Document4 pagesSubject - An Application For The Post of JR - Executive (Merchandising)aman shovonNo ratings yet

- Mca Project Report Guidelines and FormatsDocument11 pagesMca Project Report Guidelines and Formatsvikram AjmeraNo ratings yet

- MY Price List With CSV SBDocument6 pagesMY Price List With CSV SBNini Syaheera Binti JasniNo ratings yet

- Autocratic Leadership Style of Henry Ford 1.1. DefinitionDocument3 pagesAutocratic Leadership Style of Henry Ford 1.1. DefinitionThảo Ngọc100% (2)

- Licence Conditions and Codes of PracticeDocument80 pagesLicence Conditions and Codes of PracticeEric GarciaNo ratings yet

- Note On House Rent AllowanceDocument5 pagesNote On House Rent AllowanceAbhisek SarkarNo ratings yet

- Vitamin B12 order invoiceDocument1 pageVitamin B12 order invoiceDanielVasquezNo ratings yet

- BIR Ruling 415-93Document2 pagesBIR Ruling 415-93Russell PageNo ratings yet

- Group 7 - ABFRL in Ethnic ApparelDocument66 pagesGroup 7 - ABFRL in Ethnic ApparelSWETANJALI MEHER Jaipuria JaipurNo ratings yet

- FluidLab-PA MPS-PA 3 0 Manual EN PDFDocument90 pagesFluidLab-PA MPS-PA 3 0 Manual EN PDFAngelica May BangayanNo ratings yet

- Itp For All MaterialsDocument59 pagesItp For All MaterialsTauqueerAhmad100% (1)

- Financial Analysis of HDFC BankDocument58 pagesFinancial Analysis of HDFC BankInderdeepSingh50% (2)

- Kuis Akun No 1Document10 pagesKuis Akun No 1Daveli NatanaelNo ratings yet

- Ces Report in BusinessDocument54 pagesCes Report in Businessnicole alcantaraNo ratings yet

- The Signal Report 2022 - FINAL PDFDocument28 pagesThe Signal Report 2022 - FINAL PDFANURADHA JAYAWARDANANo ratings yet

- Beyond Marketing: Customer Relationship Management (CRM)Document49 pagesBeyond Marketing: Customer Relationship Management (CRM)Diamond MC TaiNo ratings yet

- Customer Satisfaction and Brand Loyalty in Big BasketDocument73 pagesCustomer Satisfaction and Brand Loyalty in Big BasketUpadhayayAnkurNo ratings yet

- Maruti Suzuki Internship ReportDocument19 pagesMaruti Suzuki Internship ReportShashikant kumar 21ME15No ratings yet

- Indian Coffee House: History and Growth of a Popular Cafe ChainDocument47 pagesIndian Coffee House: History and Growth of a Popular Cafe ChainSalman RazaNo ratings yet

- Purchase Order Lines - 637912274292216749Document110 pagesPurchase Order Lines - 637912274292216749Anoop PurohitNo ratings yet

- Soal Toeic Bab 1Document5 pagesSoal Toeic Bab 1Rizal BastianNo ratings yet

- Types of Failure and ACID Property (Basics Transaction) by Aditi WaghelaDocument5 pagesTypes of Failure and ACID Property (Basics Transaction) by Aditi Waghelaapi-27570914100% (2)

- Bobble.AI Internship Offer LetterDocument3 pagesBobble.AI Internship Offer LetterNilesh Sukhdeve IINo ratings yet

- Assignment 01 - FMDocument2 pagesAssignment 01 - FMGAME OVERNo ratings yet

- Chapter 5 The Nineteenth Century Philippine Economy Society and The Chinese MestizosDocument27 pagesChapter 5 The Nineteenth Century Philippine Economy Society and The Chinese MestizosJuMakMat Mac50% (2)

- Scan To Scribd With CcscanDocument13 pagesScan To Scribd With CcscanclarkcclNo ratings yet

- Jurnal Analogi Hukum Prosedur Dan Akibat PKPUDocument5 pagesJurnal Analogi Hukum Prosedur Dan Akibat PKPUanindita putriNo ratings yet

- MKT 222222222Document21 pagesMKT 222222222Faisal AhmedNo ratings yet