You might also like

- MRA Project Milestone 2Document20 pagesMRA Project Milestone 2Sandya Vb69% (16)

- Bilal Hyder I170743 20-SEPDocument10 pagesBilal Hyder I170743 20-SEPUbaid0% (1)

- JD Sdn. BHD Study CaseDocument5 pagesJD Sdn. BHD Study CaseSuperFlyFlyers100% (2)

- Module 2 - Davis, Michaels, and CoDocument5 pagesModule 2 - Davis, Michaels, and Coseth litchfieldNo ratings yet

- Finm1416 Individual Compenent 4Document5 pagesFinm1416 Individual Compenent 4Ma HiNo ratings yet

- 660 Final Assignment (Maruf)Document29 pages660 Final Assignment (Maruf)Maruf ChowdhuryNo ratings yet

- Chapter 6Document28 pagesChapter 6Faisal Siddiqui0% (1)

- Case StudyDocument6 pagesCase StudyArun Kenneth100% (1)

- Wardah 20396 PFM Assignment 3Document12 pagesWardah 20396 PFM Assignment 3wardah mukhtar0% (1)

- FM16 Ch21 Tool KitDocument41 pagesFM16 Ch21 Tool KitAdamNo ratings yet

- Practical Power Plant Engineering A Guide For Early Career Engineers PDFDocument652 pagesPractical Power Plant Engineering A Guide For Early Career Engineers PDFsahli medNo ratings yet

- CA Inter FM SM A MTP 2 May 2024 Castudynotes ComDocument19 pagesCA Inter FM SM A MTP 2 May 2024 Castudynotes ComsanjanavijjapuNo ratings yet

- Monte Carlo Analysis PMP ResourcesDocument3 pagesMonte Carlo Analysis PMP Resourcesharishr1968No ratings yet

- Airbnb SimulationDocument5 pagesAirbnb SimulationVianna NgNo ratings yet

- Monte Carlo Simulation Tutorial v2.0Document50 pagesMonte Carlo Simulation Tutorial v2.0moepoeNo ratings yet

- 2.4 Risk Analysis in Capital BudgetingDocument68 pages2.4 Risk Analysis in Capital BudgetingMaha Bianca Charisma CastroNo ratings yet

- Chapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1Document8 pagesChapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1ghzNo ratings yet

- Slide6 CapBud Risk AnalysisDocument82 pagesSlide6 CapBud Risk AnalysisFaisal KarimNo ratings yet

- Elearning1 MKDocument4 pagesElearning1 MKZumeidaNo ratings yet

- Engg. Economics ProjectDocument13 pagesEngg. Economics ProjectkawtharNo ratings yet

- Name: Course: SEGI Course Code: UCLAN Module Code: Registration Number Institution: Lecturer: Due Date: Student SignatureDocument8 pagesName: Course: SEGI Course Code: UCLAN Module Code: Registration Number Institution: Lecturer: Due Date: Student SignatureErick KinotiNo ratings yet

- 3.3 Cashflow Estimation and Risk Analysis Data Tables, Goal Seek and Scenario Analysis ExcerciseDocument11 pages3.3 Cashflow Estimation and Risk Analysis Data Tables, Goal Seek and Scenario Analysis ExcerciseRaghavendra NaduvinamaniNo ratings yet

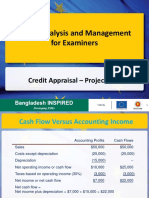

- Credit Analysis and Management For Examiners: Credit Appraisal - Project RiskDocument17 pagesCredit Analysis and Management For Examiners: Credit Appraisal - Project RisksabetaliNo ratings yet

- Break even Analysis Feasibility Study - Chapter 12 - مهمDocument11 pagesBreak even Analysis Feasibility Study - Chapter 12 - مهمwskrebNo ratings yet

- NPV Lesson 2 Workings - Class BDocument6 pagesNPV Lesson 2 Workings - Class BBarack MikeNo ratings yet

- Capital Budgeting AnswerDocument18 pagesCapital Budgeting AnswerPiyush ChughNo ratings yet

- CF Assignment 3 (B)Document13 pagesCF Assignment 3 (B)Just Some EditsNo ratings yet

- Chapter 21. Tool Kit For Mergers, Lbos, Divestitures, and Holding CompaniesDocument21 pagesChapter 21. Tool Kit For Mergers, Lbos, Divestitures, and Holding CompaniesJITIN ARORANo ratings yet

- Year 0 Year 1 Year 2 Year 3 Year 4 Year 5: Tangible Benefit WorksheetDocument4 pagesYear 0 Year 1 Year 2 Year 3 Year 4 Year 5: Tangible Benefit WorksheetMikelNo ratings yet

- Risk AnalysisDocument56 pagesRisk AnalysissukiratvirkNo ratings yet

- This Study Resource Was: (Question)Document3 pagesThis Study Resource Was: (Question)Mir Salman AjabNo ratings yet

- Investment Outlays: Long-Term AssetsDocument12 pagesInvestment Outlays: Long-Term AssetsRimpy SondhNo ratings yet

- Cash+flow+estimation (14-1759)Document9 pagesCash+flow+estimation (14-1759)M shahjamal QureshiNo ratings yet

- ch8 9 10Document1,155 pagesch8 9 10DavidNo ratings yet

- Slides - Capital Budgeting - 2Document8 pagesSlides - Capital Budgeting - 2Anish AdhikariNo ratings yet

- Chapter 11Document43 pagesChapter 11Rishu GargNo ratings yet

- Chapter 14 LEASINGDocument17 pagesChapter 14 LEASINGKaran KashyapNo ratings yet

- Solutions To Relevant Cost ProblemsDocument9 pagesSolutions To Relevant Cost ProblemsEljay VinsonNo ratings yet

- PMBOK 6th Ed 2017 (Risk Analysis Quantitatives)Document6 pagesPMBOK 6th Ed 2017 (Risk Analysis Quantitatives)Ahmad YayakNo ratings yet

- Next-X Inc - FinalDocument9 pagesNext-X Inc - FinalJam Xabryl AquinoNo ratings yet

- 11042024154808Document15 pages11042024154808agarwalpawan1No ratings yet

- Afm FinalDocument7 pagesAfm Finalpromptpaper1No ratings yet

- Capital Budgeting-ClassDocument91 pagesCapital Budgeting-ClassAditi AgrawalNo ratings yet

- MSQ-08 Capital BudgetingDocument20 pagesMSQ-08 Capital BudgetingJohn Carlo PeruNo ratings yet

- Hitungan Kuis 6 Bethesda Mining CompanyDocument6 pagesHitungan Kuis 6 Bethesda Mining Companyrica100% (1)

- All-Chapter-FM (1) (1) - 230602 - 235400Document19 pagesAll-Chapter-FM (1) (1) - 230602 - 235400alomgirhussan740No ratings yet

- Simulation AnalsisDocument4 pagesSimulation Analsispromptpaper1No ratings yet

- Chapter 12. Tool Kit For Cash Flow Estimation and Risk AnalysisDocument4 pagesChapter 12. Tool Kit For Cash Flow Estimation and Risk AnalysisHerlambang PrayogaNo ratings yet

- CH #12Document5 pagesCH #12BWB DONALDNo ratings yet

- Tugas Manajemen Keuangan 1,2,4Document8 pagesTugas Manajemen Keuangan 1,2,4Ivo ArselaNo ratings yet

- MTP-1 6 KeyDocument16 pagesMTP-1 6 KeynazcomputersitsNo ratings yet

- Introduction To Risk Analysis in Capital Budgeting: Practical ProblemsDocument14 pagesIntroduction To Risk Analysis in Capital Budgeting: Practical ProblemsDangerous GamerNo ratings yet

- Bharti School of Engineering ENGR 3426-Engineering Economics Project (DCF and Risk Analysis)Document23 pagesBharti School of Engineering ENGR 3426-Engineering Economics Project (DCF and Risk Analysis)Victor NwaborNo ratings yet

- EconomicsDocument3 pagesEconomicsNijat AhmadovNo ratings yet

- Cost Estimation & CVP Suggested SolutionDocument15 pagesCost Estimation & CVP Suggested SolutionNguyên Văn NhậtNo ratings yet

- FM ZadaciDocument48 pagesFM ZadaciPolovnaRobaNo ratings yet

- A1. Fm-2018-Sepdec-Sample-ADocument4 pagesA1. Fm-2018-Sepdec-Sample-ANirmal ShresthaNo ratings yet

- NPV For SfadDocument16 pagesNPV For SfadAmmar AsifNo ratings yet

- CapbdgtDocument25 pagesCapbdgtmajidNo ratings yet

- Case StudyDocument5 pagesCase Studyphượng nguyễn thị minhNo ratings yet

- The Quantum Financial Revolution Unlocking the Power of the FutureFrom EverandThe Quantum Financial Revolution Unlocking the Power of the FutureNo ratings yet

- Republic OF THE Philippines Department OF Budget AND ManagementDocument32 pagesRepublic OF THE Philippines Department OF Budget AND ManagementjcNo ratings yet

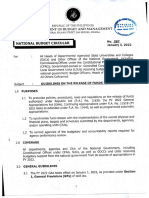

- National Budget Circular No 583 For Gaa 2021Document29 pagesNational Budget Circular No 583 For Gaa 2021KANo ratings yet

- PUP-Research Seminar I (Group IV)Document30 pagesPUP-Research Seminar I (Group IV)BB ViloriaNo ratings yet

- Foreign Exchange RiskDocument5 pagesForeign Exchange RiskBB ViloriaNo ratings yet

- VILORIA, BRYAN - Topic 1 (Internet Penetration and Broadband Subscription On Economic Growth)Document3 pagesVILORIA, BRYAN - Topic 1 (Internet Penetration and Broadband Subscription On Economic Growth)BB ViloriaNo ratings yet

- TOO 04 2016 19 August 2016Document2 pagesTOO 04 2016 19 August 2016BB ViloriaNo ratings yet

- By Department April 2019Document3 pagesBy Department April 2019BB ViloriaNo ratings yet

- The First Quality Books To ReadDocument2 pagesThe First Quality Books To ReadMarvin I. NoronaNo ratings yet

- Educational Psychology EDU-202 Spring - 2022 Dr. Fouad Yehya: Fyehya@aust - Edu.lbDocument31 pagesEducational Psychology EDU-202 Spring - 2022 Dr. Fouad Yehya: Fyehya@aust - Edu.lbLayla Al KhatibNo ratings yet

- Blood Is A Body Fluid in Human and Other Animals That Delivers Necessary Substances Such AsDocument24 pagesBlood Is A Body Fluid in Human and Other Animals That Delivers Necessary Substances Such AsPaulo DanielNo ratings yet

- Universal Declaration of Human Rights - United NationsDocument12 pagesUniversal Declaration of Human Rights - United NationsSafdar HussainNo ratings yet

- Noffke V DOD 2019-2183Document6 pagesNoffke V DOD 2019-2183FedSmith Inc.No ratings yet

- YaalDocument25 pagesYaalruseenyNo ratings yet

- Rousseau NotesDocument4 pagesRousseau NotesAkhilesh IssurNo ratings yet

- Luzande, Mary Christine B - Motivating and Managing Individuals - Moral LeadershipDocument15 pagesLuzande, Mary Christine B - Motivating and Managing Individuals - Moral LeadershipMAry Christine BatongbakalNo ratings yet

- 1 Relative Maxima, Relative Minima and Saddle PointsDocument3 pages1 Relative Maxima, Relative Minima and Saddle PointsRoy VeseyNo ratings yet

- Teaching and Assessment of Literature Studies and CA LitDocument9 pagesTeaching and Assessment of Literature Studies and CA LitjoshuaalimnayNo ratings yet

- Spelling Menu Days and MonthsDocument1 pageSpelling Menu Days and MonthsLisl WindhamNo ratings yet

- The Novel TodayDocument3 pagesThe Novel Todaylennon tanNo ratings yet

- Chapter 2Document14 pagesChapter 2Um E AbdulSaboorNo ratings yet

- Individual Workweek Accomplishment ReportDocument16 pagesIndividual Workweek Accomplishment ReportRenalyn Zamora Andadi JimenezNo ratings yet

- Analysis of Effectiveness of Heat Exchanger Shell and Tube Type One Shell Two Tube Pass As Cooling OilDocument6 pagesAnalysis of Effectiveness of Heat Exchanger Shell and Tube Type One Shell Two Tube Pass As Cooling OilHendrik V SihombingNo ratings yet

- An Aging Game Simulation Activity For Al PDFDocument13 pagesAn Aging Game Simulation Activity For Al PDFramzan aliNo ratings yet

- World War I Almanac Almanacs of American WarsDocument561 pagesWorld War I Almanac Almanacs of American WarsMatheus Benedito100% (1)

- Uttar Pradesh Universities Act 1973Document73 pagesUttar Pradesh Universities Act 1973ifjosofNo ratings yet

- Click Here For Download: (PDF) HerDocument2 pagesClick Here For Download: (PDF) HerJerahm Flancia0% (1)

- 17PME328E: Process Planning and Cost EstimationDocument48 pages17PME328E: Process Planning and Cost EstimationDeepak MisraNo ratings yet

- Accenture 172199U SAP S4HANA Conversion Brochure US Web PDFDocument8 pagesAccenture 172199U SAP S4HANA Conversion Brochure US Web PDFrajesh2kakkasseryNo ratings yet

- Management of Liver Trauma in Adults: Nasim Ahmed, Jerome J VernickDocument7 pagesManagement of Liver Trauma in Adults: Nasim Ahmed, Jerome J VernickwiraNo ratings yet

- Telesis Events - Construction Contract Essentials - WorkbookDocument52 pagesTelesis Events - Construction Contract Essentials - WorkbookassmonkeysNo ratings yet

- Marriage and Divorce Conflicts in The International PerspectiveDocument33 pagesMarriage and Divorce Conflicts in The International PerspectiveAnjani kumarNo ratings yet

- Florida Firearm Bill of SaleDocument4 pagesFlorida Firearm Bill of SaleGeemoNo ratings yet

- Brand Zara GAP Forever 21 Mango H&M: Brand Study of Zara Nancys Sharma FD Bdes Batch 2 Sem 8 Brand-ZaraDocument2 pagesBrand Zara GAP Forever 21 Mango H&M: Brand Study of Zara Nancys Sharma FD Bdes Batch 2 Sem 8 Brand-ZaraNancy SharmaNo ratings yet

- Pemahaman Sastra Mahasiswa Bahasa Dan Sastra Arab UIN Imam Bonjol Padang: Perspektif Ilmu SastraDocument31 pagesPemahaman Sastra Mahasiswa Bahasa Dan Sastra Arab UIN Imam Bonjol Padang: Perspektif Ilmu Sastrailham nashrullahNo ratings yet

- X2ho LteDocument7 pagesX2ho LtePrasoon PuthuvattilNo ratings yet