You might also like

- Answers - Chapter 5 Vol 2Document5 pagesAnswers - Chapter 5 Vol 2jamfloxNo ratings yet

- PAS 12 - Income Tax - AssignmentDocument8 pagesPAS 12 - Income Tax - Assignmentviva nazarenoNo ratings yet

- Income Taxes: ProblemsDocument12 pagesIncome Taxes: ProblemsCharles MateoNo ratings yet

- Special Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureDocument4 pagesSpecial Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureNoorodden50% (2)

- 2014 Volume 2 CH 5 AnswersDocument6 pages2014 Volume 2 CH 5 AnswersGirlie SisonNo ratings yet

- Accounting For Income TaxDocument6 pagesAccounting For Income TaxRyll BedasNo ratings yet

- TaxDocument8 pagesTaxClaire BarrettoNo ratings yet

- A. Journal Entries For 2020Document6 pagesA. Journal Entries For 2020Ollid Kline Jayson JNo ratings yet

- Income Tax AccountingDocument3 pagesIncome Tax Accountinghae1234No ratings yet

- Special Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureDocument5 pagesSpecial Liabilities - Income Taxes: Income Tax Rate Is 40% and Is Not Expected To Change in The FutureClarisse AlimotNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- Quiz Accounting For Income TaxDocument5 pagesQuiz Accounting For Income TaxCmNo ratings yet

- Lab Chapter 17Document5 pagesLab Chapter 17Tran Kim Tram PhanNo ratings yet

- Week 6 - ch19Document55 pagesWeek 6 - ch19bafsvideo4No ratings yet

- Lamagan, Kyla T. BSA 401 Intermediate Acct. 2 Final Output Problem 16-13 (IAA)Document14 pagesLamagan, Kyla T. BSA 401 Intermediate Acct. 2 Final Output Problem 16-13 (IAA)lana del reyNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income Taxchowchow123No ratings yet

- Intacc2 Assignment 6.1 AnswersDocument6 pagesIntacc2 Assignment 6.1 AnswersMingNo ratings yet

- Acctg110 FinalsDocument21 pagesAcctg110 FinalsRoman Dominic LlanoNo ratings yet

- Accounting For Taxes Employee BenefitsDocument6 pagesAccounting For Taxes Employee BenefitsBess Tuico MasanqueNo ratings yet

- Toaz - Info 89bf91d5 1612761367237 PRDocument7 pagesToaz - Info 89bf91d5 1612761367237 PRAEHYUN YENVYNo ratings yet

- Example 1 - Over and Under Provision of Current TaxDocument14 pagesExample 1 - Over and Under Provision of Current TaxPui YanNo ratings yet

- Bba F&a Notes & ProbDocument5 pagesBba F&a Notes & ProbMouly ChopraNo ratings yet

- Assignment 4 - SolutionsDocument2 pagesAssignment 4 - SolutionsstoryNo ratings yet

- IAS#12Document31 pagesIAS#12Shah KamalNo ratings yet

- Sample Test (Extract)Document6 pagesSample Test (Extract)Julie KimNo ratings yet

- FAR05 - Accounting For Income and Deferred TaxesDocument4 pagesFAR05 - Accounting For Income and Deferred TaxesDisguised owlNo ratings yet

- FA2-08 Income TaxesDocument3 pagesFA2-08 Income Taxeskrisha millo0% (1)

- Quiz BusFinHVRJULIANA VILLANUEVA ABM201-1Document10 pagesQuiz BusFinHVRJULIANA VILLANUEVA ABM201-1Juliana Angela VillanuevaNo ratings yet

- 2019 IntAcc Vol 3 CH 4 AnswersDocument9 pages2019 IntAcc Vol 3 CH 4 AnswersRizalito SisonNo ratings yet

- Difference Between Accounting Rules and Tax RulesDocument18 pagesDifference Between Accounting Rules and Tax RulesCezar Rishane Mae SaligueNo ratings yet

- Module 1 - Cherry Alfuerte - Train LawDocument41 pagesModule 1 - Cherry Alfuerte - Train Lawgerry dacerNo ratings yet

- Sample Financial Projections676Document21 pagesSample Financial Projections676assefamenelik1No ratings yet

- Tutorial QuestionsDocument2 pagesTutorial QuestionsNishika KaranNo ratings yet

- Finalchapter-16 2Document22 pagesFinalchapter-16 2Jud Rossette ArcebesNo ratings yet

- HO1 - Accounting For Income TaxDocument5 pagesHO1 - Accounting For Income TaxCharlesNo ratings yet

- Cost Residual Value Expected LifeDocument2 pagesCost Residual Value Expected LifeMandil BhandariNo ratings yet

- Chapter 25 and 26Document10 pagesChapter 25 and 26Sittie Aisah AmpatuaNo ratings yet

- Accounting For Income Tax QuestionsDocument13 pagesAccounting For Income Tax QuestionszeyyahjiNo ratings yet

- Tax Calculator 2018-19 (Farrukh Iqbal Khan)Document2 pagesTax Calculator 2018-19 (Farrukh Iqbal Khan)FarrukhNo ratings yet

- Appendix D Accounting For Deferred Income TaxesDocument2 pagesAppendix D Accounting For Deferred Income TaxesLan Hương Trần ThịNo ratings yet

- 7062 - Deferred Income Tax SolvingDocument9 pages7062 - Deferred Income Tax SolvingstrmsantiagoNo ratings yet

- Accounting For Income TaxationDocument8 pagesAccounting For Income Taxationangelian bagadiongNo ratings yet

- Accounting 7Document17 pagesAccounting 7Sophia Anne MonillasNo ratings yet

- Solution - Accounting For Income TaxesDocument12 pagesSolution - Accounting For Income TaxesKlarissemay MontallanaNo ratings yet

- Tidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxDocument7 pagesTidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxAlfatih 1453No ratings yet

- Advanced Financial Accounting IDocument21 pagesAdvanced Financial Accounting IAbdiNo ratings yet

- Complete Financial ModelDocument47 pagesComplete Financial ModelArrush AhujaNo ratings yet

- Group Activity 2 Answer KeyDocument4 pagesGroup Activity 2 Answer Keykrisha milloNo ratings yet

- Session 5Document19 pagesSession 5youssef.oubenaliNo ratings yet

- GPV & SCF (Assignment)Document16 pagesGPV & SCF (Assignment)Mica Moreen GuillermoNo ratings yet

- Chapter 1 LiabilitiesDocument5 pagesChapter 1 LiabilitiesAwish FernNo ratings yet

- Classroom Exercise - Unit 1-1Document2 pagesClassroom Exercise - Unit 1-1Hannah Jane ToribioNo ratings yet

- PT 4 - Statement of Cash FlowsDocument4 pagesPT 4 - Statement of Cash FlowsIrene QuilatanNo ratings yet

- Materi - INCOME TAX ACCOUNTING - 26march2021Document18 pagesMateri - INCOME TAX ACCOUNTING - 26march2021Septian Dwi AnggoroNo ratings yet

- Itemized: Gross Income From OperationsDocument9 pagesItemized: Gross Income From OperationsLyka RoguelNo ratings yet

- Book 3Document1 pageBook 3Quincy Lawrence DimaanoNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- The Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesFrom EverandThe Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesNo ratings yet

- Assignemnt No. 1Document1 pageAssignemnt No. 1Johanna Raissa CapadaNo ratings yet

- To Record 600 Shares@ 100 Ordinary Share at 80Document9 pagesTo Record 600 Shares@ 100 Ordinary Share at 80Johanna Raissa CapadaNo ratings yet

- Merger and ConsolidationDocument3 pagesMerger and ConsolidationJohanna Raissa CapadaNo ratings yet

- Section 8. Requirement of Registration of Securities. - 8.1. Securities Shall Not Be SoldDocument6 pagesSection 8. Requirement of Registration of Securities. - 8.1. Securities Shall Not Be SoldJohanna Raissa CapadaNo ratings yet

- 3 - 8 Jackie Chan LeasingDocument5 pages3 - 8 Jackie Chan LeasingJohanna Raissa CapadaNo ratings yet

- Sec144 149Document3 pagesSec144 149Johanna Raissa CapadaNo ratings yet

- Business LawDocument5 pagesBusiness LawJohanna Raissa CapadaNo ratings yet

- Empleo Robles SolMan Non-Financial LiabilitiesDocument6 pagesEmpleo Robles SolMan Non-Financial LiabilitiesJohanna Raissa CapadaNo ratings yet

- Warranty Liability Empleo Robles SolManDocument2 pagesWarranty Liability Empleo Robles SolManJohanna Raissa CapadaNo ratings yet

- SolMan Empleo Robles Intangible AssetDocument18 pagesSolMan Empleo Robles Intangible AssetJohanna Raissa CapadaNo ratings yet

- Career Definition and Denial: A Discourse Analysis of Graduate Trainees' Accounts of CareerDocument7 pagesCareer Definition and Denial: A Discourse Analysis of Graduate Trainees' Accounts of CareerJohanna Raissa CapadaNo ratings yet

- Income Tax Provisions Related To Charitable Trust in Brief: Income From Business Which Is Not IncidentalDocument5 pagesIncome Tax Provisions Related To Charitable Trust in Brief: Income From Business Which Is Not IncidentalAnkur MittalNo ratings yet

- NUST MCS Computer Software Engineering CurriculumDocument125 pagesNUST MCS Computer Software Engineering CurriculumSalah Ud Din AyubiNo ratings yet

- Project List & KPI - Ahmad Dzikrul FikriDocument3 pagesProject List & KPI - Ahmad Dzikrul Fikrikenny williamNo ratings yet

- Kumpulan Latihan IntermediateDocument27 pagesKumpulan Latihan IntermediateRina KusumaNo ratings yet

- Bill Gates - Business at The Speed of ThoughtDocument64 pagesBill Gates - Business at The Speed of Thoughtадміністратор Wake Up SchoolNo ratings yet

- Impact of Online Customer Reviews On Sales Outcomes: An Empirical Study Based On Prospect TheoryDocument18 pagesImpact of Online Customer Reviews On Sales Outcomes: An Empirical Study Based On Prospect TheoryAleena IrfanNo ratings yet

- Customer Information Sheet (CRL-FM-ADMN-049) - r1Document1 pageCustomer Information Sheet (CRL-FM-ADMN-049) - r1alvin salmingoNo ratings yet

- Loan LetterDocument1 pageLoan LetterMuhd HisyamuddinNo ratings yet

- Mini Importation Business Masterclass - Make Money in Nigeria With Mini ImportationDocument26 pagesMini Importation Business Masterclass - Make Money in Nigeria With Mini ImportationAzubuike Henry OziomaNo ratings yet

- Agency Contract AgreementDocument4 pagesAgency Contract Agreementkatpotayre potayreNo ratings yet

- Guidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFDocument200 pagesGuidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFShankar RavichandranNo ratings yet

- Published Document Recommendations For The Design of Structures To BS EN 1991-1-1Document10 pagesPublished Document Recommendations For The Design of Structures To BS EN 1991-1-1cuong100% (1)

- 2023 Budget Ordinance First ReadingDocument3 pages2023 Budget Ordinance First ReadinginforumdocsNo ratings yet

- CFA一级百题预测 财务Document90 pagesCFA一级百题预测 财务Evelyn YangNo ratings yet

- Summary Of: The Value of Saving A Life: Evidence From The Labor MarketDocument2 pagesSummary Of: The Value of Saving A Life: Evidence From The Labor MarketFreed DragsNo ratings yet

- Business English 9th Edition Guffey: Full Download atDocument20 pagesBusiness English 9th Edition Guffey: Full Download atPhươngNo ratings yet

- Dr. Ibha Rani - New Product DevelopmentDocument25 pagesDr. Ibha Rani - New Product DevelopmentIbha RaniNo ratings yet

- Procedural Requirement For StrikeDocument2 pagesProcedural Requirement For StrikeBarnz ShpNo ratings yet

- Chapter Five: Risk, Return, and The Historical RecordDocument37 pagesChapter Five: Risk, Return, and The Historical RecordAreej AlGhamdi100% (1)

- Chapter 5 CGTMSEDocument17 pagesChapter 5 CGTMSEMikeNo ratings yet

- Bottle Manufacturing UnitsDocument17 pagesBottle Manufacturing UnitsVIJAY PAREEKNo ratings yet

- What Is Cybersecurity Insurance and Why Is It ImportantDocument3 pagesWhat Is Cybersecurity Insurance and Why Is It ImportantJaveed A. KhanNo ratings yet

- Careem's Owner HandbookDocument103 pagesCareem's Owner HandbookgateebNo ratings yet

- Strategic Management Concepts Competitiveness and Globalization Hitt 11th Edition Solutions Manual Full DownloadDocument11 pagesStrategic Management Concepts Competitiveness and Globalization Hitt 11th Edition Solutions Manual Full Downloaddonnaparkermepfikcndx100% (36)

- Healthcare Technology Innovation Adoption - Electronic Health Records and Other Emerging Health Information Technology Innovations PDFDocument257 pagesHealthcare Technology Innovation Adoption - Electronic Health Records and Other Emerging Health Information Technology Innovations PDFOL Yra DiomandeNo ratings yet

- Ims HandoutDocument5 pagesIms HandoutDon Mcarthney Tugaoen100% (1)

- Government Accounting QuizDocument2 pagesGovernment Accounting QuizKate Fernandez100% (2)

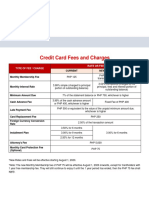

- Credit Card Fees and Charges: Type of Fee / Charge Rate or FeeDocument1 pageCredit Card Fees and Charges: Type of Fee / Charge Rate or FeeKram Yer EtentepmocNo ratings yet

- DeepWeb LinkDocument16 pagesDeepWeb LinkLucas Javier75% (4)

- Cash Flow StatementDocument10 pagesCash Flow StatementSheilaMarieAnnMagcalasNo ratings yet