You might also like

- Copal Partners ModuleDocument210 pagesCopal Partners ModulescribedheenaNo ratings yet

- KKR - Consolidated Research ReportsDocument60 pagesKKR - Consolidated Research Reportscs.ankur7010No ratings yet

- Investment Memo TemplateDocument3 pagesInvestment Memo TemplateColin DanielNo ratings yet

- Digital Media and Internet Sector Update - Spring 2012 FinalDocument52 pagesDigital Media and Internet Sector Update - Spring 2012 Finalstupac7864No ratings yet

- Global Corporate and Investment Banking An Agenda For ChangeDocument96 pagesGlobal Corporate and Investment Banking An Agenda For ChangeSherman WaltonNo ratings yet

- Gso Lenders of Last Resort 2013Document12 pagesGso Lenders of Last Resort 2013Stanley WangNo ratings yet

- 300 - PEI - Jun 2019 - DigiDocument24 pages300 - PEI - Jun 2019 - Digimick ryanNo ratings yet

- PrivCo Private Company Knowledge BankDocument85 pagesPrivCo Private Company Knowledge BankAlex Schukin100% (1)

- 07 Heinz Private EquityDocument27 pages07 Heinz Private EquityfwfsdNo ratings yet

- LBO Analysis CompletedDocument9 pagesLBO Analysis CompletedVenkatesh NatarajanNo ratings yet

- Tech 2017 M&ADocument18 pagesTech 2017 M&APedro SousaNo ratings yet

- Autonomy Presentation 1 505952Document14 pagesAutonomy Presentation 1 505952Roberto BaldwinNo ratings yet

- Lecture 5 - A Note On Valuation in Private EquityDocument85 pagesLecture 5 - A Note On Valuation in Private EquitySinan DenizNo ratings yet

- Avid Cost of Venture Debt With Warrants and Net Interest TemplateDocument13 pagesAvid Cost of Venture Debt With Warrants and Net Interest TemplateSeemaNo ratings yet

- JAZZ Sellside MA PitchbookDocument47 pagesJAZZ Sellside MA PitchbookSamarth MarwahaNo ratings yet

- Jes Staley, Investment Bank Chief Executive Officer: February 15, 2011Document20 pagesJes Staley, Investment Bank Chief Executive Officer: February 15, 2011pepecolatanNo ratings yet

- PitchbookDocument15 pagesPitchbookAnonymous DTIFVdNo ratings yet

- DigitalBridge - PTC 2023 - Inaugural KeynoteDocument22 pagesDigitalBridge - PTC 2023 - Inaugural KeynoteJuan VicarioNo ratings yet

- Illustrative LBO AnalysisDocument21 pagesIllustrative LBO AnalysisBrian DongNo ratings yet

- WST TrainingDocument7 pagesWST TrainingAli Gokhan KocanNo ratings yet

- Alvarez and Marsal City of Harrisburg Report Debt Restructuring Report 09152013 PDFDocument43 pagesAlvarez and Marsal City of Harrisburg Report Debt Restructuring Report 09152013 PDFEmily PrevitiNo ratings yet

- Pitchprogram 10 Minutepitch 131112165615 Phpapp01 PDFDocument16 pagesPitchprogram 10 Minutepitch 131112165615 Phpapp01 PDFpcmtpcmtNo ratings yet

- MSC FINANCE BUYOUT EVALUATION CHINA EDUCATIONDocument9 pagesMSC FINANCE BUYOUT EVALUATION CHINA EDUCATIONNikhilesh MoreNo ratings yet

- Restructuring Debt and EquityDocument20 pagesRestructuring Debt and EquityErick SumarlinNo ratings yet

- Alcatel-Lucent Credit Facilities NoticeDocument81 pagesAlcatel-Lucent Credit Facilities NoticeHilal MilmoNo ratings yet

- Pitchbook StrategyDocument25 pagesPitchbook Strategydfk1111No ratings yet

- Defining Free Cash Flow Top-Down ApproachDocument2 pagesDefining Free Cash Flow Top-Down Approachchuff6675100% (1)

- Hold Check Point Software: Transferring Coverage With A HOLDDocument25 pagesHold Check Point Software: Transferring Coverage With A HOLDJacob ZiemannNo ratings yet

- Lbo Model Long FormDocument6 pagesLbo Model Long FormadsadasMNo ratings yet

- Equity Investments in Unlisted CompaniesDocument32 pagesEquity Investments in Unlisted CompaniesANo ratings yet

- Fidelity Model Worksheet Mar 2019Document25 pagesFidelity Model Worksheet Mar 2019Bobby ChristiantoNo ratings yet

- Piper Jaffray - US LBO MarketDocument40 pagesPiper Jaffray - US LBO MarketYoon kookNo ratings yet

- GS DellDocument20 pagesGS DelljwkNo ratings yet

- Introduction To Bond MathDocument43 pagesIntroduction To Bond MathnazNo ratings yet

- Netflix Equity Debt Convertible Investment Banking Pitch BookDocument15 pagesNetflix Equity Debt Convertible Investment Banking Pitch BookphuNo ratings yet

- Georgetown Case Competition: ConfidentialDocument17 pagesGeorgetown Case Competition: ConfidentialPatrick BensonNo ratings yet

- Ey 2022 Practitioner Cost of Capital WaccDocument26 pagesEy 2022 Practitioner Cost of Capital WaccFrancescoNo ratings yet

- Discussion of Valuation MethodsDocument21 pagesDiscussion of Valuation MethodsCommodityNo ratings yet

- LBO Fundamentals: Structure, Performance & Exit StrategiesDocument40 pagesLBO Fundamentals: Structure, Performance & Exit StrategiesSouhail TihaniNo ratings yet

- Fortress Investment GroupDocument8 pagesFortress Investment GroupAishwarya Ratna PandeyNo ratings yet

- Handbook: 2022 EDITIONDocument247 pagesHandbook: 2022 EDITIONFarhana Lukman DSNo ratings yet

- Practitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeDocument25 pagesPractitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeМаксим ЧернышевNo ratings yet

- Strategic Lending Plan: September 2011 Final DocumentDocument11 pagesStrategic Lending Plan: September 2011 Final DocumentFinley FinnNo ratings yet

- Jazz Pharmaceuticals Investment Banking Pitch BookDocument20 pagesJazz Pharmaceuticals Investment Banking Pitch BookAlexandreLegaNo ratings yet

- ConAgra Presentation Backing Its Ralcorp BidDocument10 pagesConAgra Presentation Backing Its Ralcorp BidDealBookNo ratings yet

- Merger Model PP Allocation BeforeDocument100 pagesMerger Model PP Allocation BeforePaulo NascimentoNo ratings yet

- Wealth & Asset ManagementDocument17 pagesWealth & Asset ManagementVishnuSimmhaAgnisagarNo ratings yet

- Valuation Techniques Review DocumentDocument42 pagesValuation Techniques Review DocumentCommodityNo ratings yet

- Project Matador Teaser: New Serbian Silo-Port OpportunityDocument5 pagesProject Matador Teaser: New Serbian Silo-Port Opportunityspartak_serbiaNo ratings yet

- Tesla SolarCity LawsuitDocument415 pagesTesla SolarCity LawsuitLucas ManfrediNo ratings yet

- Affirm Holdings - BarclaysDocument12 pagesAffirm Holdings - BarclaysSarut BeerNo ratings yet

- Autonomy Overview Highlights Growth and ProfitabilityDocument14 pagesAutonomy Overview Highlights Growth and ProfitabilityRishabh Bansal100% (1)

- Goldman Sachs Presentation To Credit Suisse Financial Services ConferenceDocument20 pagesGoldman Sachs Presentation To Credit Suisse Financial Services ConferenceEveline WangNo ratings yet

- InvestAsian Investment Deck NewDocument14 pagesInvestAsian Investment Deck NewReidKirchenbauerNo ratings yet

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsFrom EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNo ratings yet

- The Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondFrom EverandThe Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

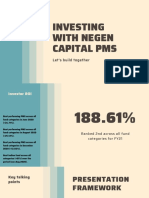

- INVESTING WITH NEGEN CAPITAL PMS: BEST PERFORMING FUND ACROSS CATEGORIESDocument12 pagesINVESTING WITH NEGEN CAPITAL PMS: BEST PERFORMING FUND ACROSS CATEGORIESSumit SagarNo ratings yet

- NCERT - Economic & Commercial Geography of India X (Old Edition)Document169 pagesNCERT - Economic & Commercial Geography of India X (Old Edition)Sumit SagarNo ratings yet

- (NCERT) Principles of Geography XI (Old Edition) PDFDocument157 pages(NCERT) Principles of Geography XI (Old Edition) PDFPranshu SharmaNo ratings yet

- NCERT - Principle Basic of Geography XI (Old Edition)Document231 pagesNCERT - Principle Basic of Geography XI (Old Edition)Sumit SagarNo ratings yet

- Course Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallDocument3 pagesCourse Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallSumit SagarNo ratings yet

- Negen Capital: (Portfolio Management Service)Document5 pagesNegen Capital: (Portfolio Management Service)Sumit SagarNo ratings yet

- Zac Efron Workout RoutineDocument9 pagesZac Efron Workout RoutineKhôi Nguyên100% (1)

- How To Save Your TimeDocument1 pageHow To Save Your TimeSumit SagarNo ratings yet

- (Prelims Spotlight) Important Amendments in The Indian Constitution - CivilsdailyDocument10 pages(Prelims Spotlight) Important Amendments in The Indian Constitution - CivilsdailySumit SagarNo ratings yet

- East Coast 2015 Letter Twin LightsDocument15 pagesEast Coast 2015 Letter Twin LightsSumit SagarNo ratings yet

- Givernyannual 2004Document16 pagesGivernyannual 2004Sumit SagarNo ratings yet

- AnnalPrg Exam RT 2022 Engl 130821Document1 pageAnnalPrg Exam RT 2022 Engl 130821Pruthaviraj BNo ratings yet

- BSK Ass 1Document8 pagesBSK Ass 1Sumit SagarNo ratings yet

- Folding Faulting - NegiDocument31 pagesFolding Faulting - NegiSumit SagarNo ratings yet

- Underground: WaterDocument12 pagesUnderground: WaterSumit Sagar0% (1)

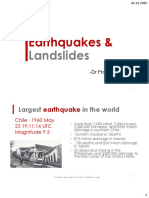

- Earthquakes and LandslidesDocument19 pagesEarthquakes and LandslidesSumit SagarNo ratings yet

- Rock mass classification and excavation guidelinesDocument6 pagesRock mass classification and excavation guidelinesSumit SagarNo ratings yet

- Law Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiesDocument2 pagesLaw Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiespratikNo ratings yet

- Scanned With Camscanner: Kanishak Kataria: Air 1 Upsc Cse 2018Document3 pagesScanned With Camscanner: Kanishak Kataria: Air 1 Upsc Cse 2018Sumit SagarNo ratings yet

- Law Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiesDocument2 pagesLaw Commission, Enforcement Directorate, Cabinet Secretary & Other Key Govt BodiespratikNo ratings yet

- Master Document For FamilyDocument15 pagesMaster Document For FamilySumit SagarNo ratings yet

- Self Note - Historical Development of EducationDocument3 pagesSelf Note - Historical Development of EducationFINEworksNo ratings yet

- Hand and Seal: JSPSC-Statutory-Appoint: Prez - 62 Yrs - Report: GovernrDocument4 pagesHand and Seal: JSPSC-Statutory-Appoint: Prez - 62 Yrs - Report: Governrpratik100% (1)

- PT 365 Updation-2Document92 pagesPT 365 Updation-2ChaithanyaNo ratings yet

- Cheetah: SR N O Name Picture Distributi ONDocument5 pagesCheetah: SR N O Name Picture Distributi ONSumit SagarNo ratings yet

- Biodiversity Hotspots in IndiaDocument9 pagesBiodiversity Hotspots in IndiaSumit SagarNo ratings yet

- NHRC CIC CVC CBI Lokpal: Home Ministry Responsible Only To ParliamentDocument4 pagesNHRC CIC CVC CBI Lokpal: Home Ministry Responsible Only To ParliamentpratikNo ratings yet

- Parag Parikh Pole Star of Value InvestinDocument3 pagesParag Parikh Pole Star of Value InvestinSumit SagarNo ratings yet

- Architecture MCQ (Rohit Kumar Verma 170544)Document8 pagesArchitecture MCQ (Rohit Kumar Verma 170544)Sumit SagarNo ratings yet

- Architecture MCQsDocument8 pagesArchitecture MCQsSumit SagarNo ratings yet

- Auditing Problems Test Bank 2 Auditing Problems Test Bank 2Document16 pagesAuditing Problems Test Bank 2 Auditing Problems Test Bank 2xjammerNo ratings yet

- Christopher Collins Feburary Bank StatementDocument2 pagesChristopher Collins Feburary Bank StatementJim BoazNo ratings yet

- Illustrative Financial Statements O 201210Document316 pagesIllustrative Financial Statements O 201210Yogeeshwaran Ponnuchamy100% (1)

- Intacc Chapter 1Document2 pagesIntacc Chapter 1Niño Albert EugenioNo ratings yet

- Module 11 - PFRS 17 Insurance ContractsDocument8 pagesModule 11 - PFRS 17 Insurance ContractsAKIO HIROKINo ratings yet

- Theories, Concepts and Practices of Accounting and Auditing in The Philippines - Jirah Rose FloresDocument30 pagesTheories, Concepts and Practices of Accounting and Auditing in The Philippines - Jirah Rose Floresjirah rose flores0% (1)

- Downloadable Solution Manual For Financial Accounting IFRS 3rd Edition Weygandt Ch01 2Document68 pagesDownloadable Solution Manual For Financial Accounting IFRS 3rd Edition Weygandt Ch01 2Neti Kesumawati100% (1)

- CPPIB's Private Equity Strategy vs Fund of FundsDocument3 pagesCPPIB's Private Equity Strategy vs Fund of FundsJitesh Thakur100% (1)

- Derivagem - Version 1.52: "Options, Futures and Other Derivatives" 7/E "Fundamentals of Futures and Options Markets" 6/EDocument61 pagesDerivagem - Version 1.52: "Options, Futures and Other Derivatives" 7/E "Fundamentals of Futures and Options Markets" 6/Eمحمد احمد جیلانیNo ratings yet

- Board Directors Removal GuideDocument34 pagesBoard Directors Removal GuideJamie Rose AragonesNo ratings yet

- Company Law CIA 3Document13 pagesCompany Law CIA 3shivaniNo ratings yet

- Financial Markets: Mid-Term ExaminationDocument13 pagesFinancial Markets: Mid-Term ExaminationJazzmine DalangpanNo ratings yet

- Discounted Payback Period 2Document2 pagesDiscounted Payback Period 2Sharulatha SNo ratings yet

- Account MCQ PDFDocument93 pagesAccount MCQ PDFsunil kalura100% (1)

- Fundamentals of Corporate Finance Canadian Canadian 8th Edition Ross Test BankDocument26 pagesFundamentals of Corporate Finance Canadian Canadian 8th Edition Ross Test BankMadelineTorresdazb100% (54)

- Auditing Receivables ObjectivesDocument2 pagesAuditing Receivables ObjectivesKimberly LiwanagNo ratings yet

- MNG Comm. Report 2020-21 (Ann-C)Document18 pagesMNG Comm. Report 2020-21 (Ann-C)shabishahNo ratings yet

- Colgate Palmolive ModelDocument51 pagesColgate Palmolive ModelAde FajarNo ratings yet

- Ten Years of IfrsDocument12 pagesTen Years of IfrsAmal Ben RamdhaneNo ratings yet

- Fin430 - Dec2019Document6 pagesFin430 - Dec2019nurinsabyhahNo ratings yet

- Merchandise 1Document33 pagesMerchandise 1JcNo ratings yet

- Zkhokhar - 1336 - 3711 - 1 - CHAPTER 04 - JOB-ORDER COSTING - PROBLEMSDocument34 pagesZkhokhar - 1336 - 3711 - 1 - CHAPTER 04 - JOB-ORDER COSTING - PROBLEMSnabeel nabiNo ratings yet

- Course Out Line TalilaDocument5 pagesCourse Out Line TalilatalilaNo ratings yet

- NismDocument17 pagesNismRohit Shet50% (2)

- 80 Minute MBA London Buisness Forum WebDocument103 pages80 Minute MBA London Buisness Forum WebSubrato SahaNo ratings yet

- Basel III: Post-Crisis Reforms: Implementation TimelineDocument5 pagesBasel III: Post-Crisis Reforms: Implementation TimelineHamza AmiriNo ratings yet

- Adani ResponseDocument413 pagesAdani ResponseZerohedgeNo ratings yet

- Solvency-Ability of An Entity To: Transactions and UseDocument6 pagesSolvency-Ability of An Entity To: Transactions and UseCarl Yry BitengNo ratings yet

- Byco Petroleum Pakistan LTD Income Statement: Period Ending: 2019Document22 pagesByco Petroleum Pakistan LTD Income Statement: Period Ending: 2019mohammad bilalNo ratings yet

- Question Bank For NPODocument17 pagesQuestion Bank For NPOSanyam BohraNo ratings yet