You might also like

- John J Murphy - Technical Analysis of The Financial MarketsDocument596 pagesJohn J Murphy - Technical Analysis of The Financial Marketsbarbarajeanlavender97% (75)

- WorldExplorationTrends2023 ReportDocument16 pagesWorldExplorationTrends2023 ReportKrash King100% (1)

- Moodys Credit Report Update On Baffinland June 2020Document8 pagesMoodys Credit Report Update On Baffinland June 2020NunatsiaqNewsNo ratings yet

- Sector Minero en El Perú - 2020 - BBVADocument63 pagesSector Minero en El Perú - 2020 - BBVAYensi Urbano CamonesNo ratings yet

- Chakana Copper Research Report Fox-Davies 021521Document24 pagesChakana Copper Research Report Fox-Davies 021521AndresNo ratings yet

- The Main Playing Field For The Next Round of Lithium DevelopmentDocument8 pagesThe Main Playing Field For The Next Round of Lithium DevelopmentMichael NgoieNo ratings yet

- The Gold Mine of The Future: Nick Holland, CEO Gold FieldsDocument28 pagesThe Gold Mine of The Future: Nick Holland, CEO Gold FieldsHENRY TORRESNo ratings yet

- CitrusDocument15 pagesCitrusPhilip CurranNo ratings yet

- 2021 Partech Africa Tech VC Report ReducedDocument39 pages2021 Partech Africa Tech VC Report ReducedymagNo ratings yet

- Peru A Mining CountryDocument37 pagesPeru A Mining CountryOlivia JacksonNo ratings yet

- 2021-04-12 Market OverviewDocument12 pages2021-04-12 Market Overviewadelafuente2012No ratings yet

- BofA Global Research-Commodity Strategist Year Ahead 2023 Commodity Outlook-99278411Document96 pagesBofA Global Research-Commodity Strategist Year Ahead 2023 Commodity Outlook-99278411杨舒No ratings yet

- MOS Mosaic Feb 2010 PresentationDocument22 pagesMOS Mosaic Feb 2010 PresentationAla BasterNo ratings yet

- Cream Minerals AdvancesDocument2 pagesCream Minerals AdvancesdouglashadfieldNo ratings yet

- Gold & Silver Mining Projects in EcuadorDocument25 pagesGold & Silver Mining Projects in EcuadorArthur OppitzNo ratings yet

- Nov 2020 Building Indonesia's New Gold Miner: Baru:Tsx Baruf:UsDocument32 pagesNov 2020 Building Indonesia's New Gold Miner: Baru:Tsx Baruf:UsscrsunvisNo ratings yet

- Peru Mining 2020 - Web VersionDocument65 pagesPeru Mining 2020 - Web VersionMiguel Ego-AguirreNo ratings yet

- Transaction Highlights: Krugold Resources, IncDocument5 pagesTransaction Highlights: Krugold Resources, IncAamir AzizNo ratings yet

- September 2023-1Document57 pagesSeptember 2023-1Aftab AhmedNo ratings yet

- OzMine2014TonyManini PresentationDocument25 pagesOzMine2014TonyManini Presentationaliminsyah.caneNo ratings yet

- Uranium Sector Gets Four Catalysts Are "ESG" Investors Gaining Interest, and Is It Time To Buy?Document7 pagesUranium Sector Gets Four Catalysts Are "ESG" Investors Gaining Interest, and Is It Time To Buy?ZerohedgeNo ratings yet

- MDKA Investor Presentation March 2023 CLSA ASEAN ForumDocument31 pagesMDKA Investor Presentation March 2023 CLSA ASEAN ForumHilman DarojatNo ratings yet

- Enterprise Risk Management at BarrickDocument3 pagesEnterprise Risk Management at BarrickjoyabyssNo ratings yet

- Energy Efficiency Copper HydrometallurgyDocument41 pagesEnergy Efficiency Copper Hydrometallurgyalexis diaz0% (1)

- Building The Third Pillar of Saudi Industry: September 2013Document29 pagesBuilding The Third Pillar of Saudi Industry: September 2013Anonymous q9eCZHMuSNo ratings yet

- 2 Maaden PDFDocument29 pages2 Maaden PDFAnonymous q9eCZHMuS100% (1)

- Australian Copper Conference 250310Document22 pagesAustralian Copper Conference 250310BerndNo ratings yet

- Annual ReportDocument120 pagesAnnual ReportBraulio Stefan Zorrilla PariachiNo ratings yet

- Maya Gold & Silver and Guy Goulet Exploring MoroccoDocument4 pagesMaya Gold & Silver and Guy Goulet Exploring MoroccoguygouletNo ratings yet

- DEFCON 2: TRR Moves Closer To A "War Footing" On Iran Concerns - Buying OilsDocument34 pagesDEFCON 2: TRR Moves Closer To A "War Footing" On Iran Concerns - Buying OilsNathan MartinNo ratings yet

- Korean Investment & Sekuritas MDKA - Gold Opens All LocksDocument7 pagesKorean Investment & Sekuritas MDKA - Gold Opens All LocksGumilang PrakarsaNo ratings yet

- Global Oil Supply and Demand Outlook To 2040 Online SummaryDocument9 pagesGlobal Oil Supply and Demand Outlook To 2040 Online SummarysaidNo ratings yet

- Erris New Corporate Presentation May 11th 2020Document26 pagesErris New Corporate Presentation May 11th 2020Niall Mc DermottNo ratings yet

- Projects in Manganese WorldDocument31 pagesProjects in Manganese WorldleniucvasileNo ratings yet

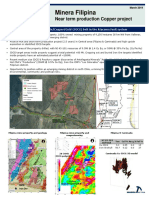

- Minera Filipina: Near Term Production Copper ProjectDocument2 pagesMinera Filipina: Near Term Production Copper ProjectBotacura Minerals acuña moralesNo ratings yet

- IA Commentary Draft 2Document2 pagesIA Commentary Draft 2wesley hudsonNo ratings yet

- MNO Investor Presentation 07 June 2023Document37 pagesMNO Investor Presentation 07 June 2023joseanselmoNo ratings yet

- TRQ Investor Presentation Feb 2017Document21 pagesTRQ Investor Presentation Feb 2017b1OSphereNo ratings yet

- 2022 Global Market Report CocoaDocument42 pages2022 Global Market Report Cocoasatya6a9246No ratings yet

- Ponto Investor-Presentation-March-2022Document19 pagesPonto Investor-Presentation-March-2022JoshLeighNo ratings yet

- Oil & Gas: Project Management Business Dev MentDocument23 pagesOil & Gas: Project Management Business Dev MentRichie RimbaniNo ratings yet

- Ho, To The Klondike!: Klondike Gold Corp. (TSXV:KG)Document23 pagesHo, To The Klondike!: Klondike Gold Corp. (TSXV:KG)Goldherz ReportNo ratings yet

- Erris Corporate Presentation, April 28th 2020Document26 pagesErris Corporate Presentation, April 28th 2020Niall Mc DermottNo ratings yet

- De Grey MiningDocument30 pagesDe Grey MiningSergey KNo ratings yet

- Sustainably Sourcing Magnet and Heavy Rare Earths To Meet Net Zero Carbon AmbitionsDocument47 pagesSustainably Sourcing Magnet and Heavy Rare Earths To Meet Net Zero Carbon Ambitions10evenwoodcloseNo ratings yet

- Polymetal International PLC: Novopetrovsky Initial Mineral Resource EstimateDocument4 pagesPolymetal International PLC: Novopetrovsky Initial Mineral Resource Estimategfhjgjkj hghgjNo ratings yet

- World Exploration Trends 2021Document13 pagesWorld Exploration Trends 2021ISAACNo ratings yet

- Andiamo FDC ResearchDocument35 pagesAndiamo FDC ResearchResearchtimeNo ratings yet

- Haywood Junior Exploration On Juggernaut TSX-V JUGRDocument2 pagesHaywood Junior Exploration On Juggernaut TSX-V JUGRJames HudsonNo ratings yet

- Germany To Invest 1 Billion in Critical Raw MaterialsDocument6 pagesGermany To Invest 1 Billion in Critical Raw MaterialsPhilip KennyNo ratings yet

- Unlocking The Potential in Madagascar's Natural ResourcesDocument1 pageUnlocking The Potential in Madagascar's Natural Resourcesjulianme77No ratings yet

- DIFC - MENA Energy InvestmentsDocument10 pagesDIFC - MENA Energy InvestmentsSIRINE TAJERNo ratings yet

- LATAM Markets Mining BrazilDocument1 pageLATAM Markets Mining BrazilSamuel DemonsaniNo ratings yet

- Mineral ResourcesDocument14 pagesMineral Resourceskhonor327No ratings yet

- Oil From SandDocument3 pagesOil From SandLisbeth Roos RoosNo ratings yet

- TSXV: RDS: The High Grade O'Brien Gold ProjectDocument22 pagesTSXV: RDS: The High Grade O'Brien Gold ProjectJZNo ratings yet

- 30.logic Bypass or Modificatirequest FormatDocument2 pages30.logic Bypass or Modificatirequest FormatRam Babu RamzzNo ratings yet

- In Tu MentalDocument3 pagesIn Tu MentalRam Babu RamzzNo ratings yet

- Centrifugal Pump and Mechanical Seal FormulaDocument3 pagesCentrifugal Pump and Mechanical Seal FormulaRam Babu Ramzz100% (1)

- Physical Separationand EnrichmentDocument200 pagesPhysical Separationand EnrichmentRam Babu RamzzNo ratings yet

- Hazard Vs RiskDocument4 pagesHazard Vs RiskRam Babu RamzzNo ratings yet

- Process Plant ManagerDocument1 pageProcess Plant ManagerRam Babu RamzzNo ratings yet

- Comparison of Sinter and Pellet Usage in An Integrated Steel PlantDocument11 pagesComparison of Sinter and Pellet Usage in An Integrated Steel PlantRam Babu RamzzNo ratings yet

- Imerys Press Release Vizag Opening 030621Document2 pagesImerys Press Release Vizag Opening 030621Ram Babu RamzzNo ratings yet

- Mill Scale in SinteringDocument6 pagesMill Scale in SinteringRam Babu RamzzNo ratings yet

- SHIVA KRISHNA RESUME New 2 PDFDocument3 pagesSHIVA KRISHNA RESUME New 2 PDFRam Babu RamzzNo ratings yet

- Simulation of Area 1 P.BDocument18 pagesSimulation of Area 1 P.BRam Babu RamzzNo ratings yet

- SB 101 Eriez Metal Separation Selection Guide PDFDocument8 pagesSB 101 Eriez Metal Separation Selection Guide PDFRam Babu RamzzNo ratings yet

- Permanent Associate MembersDocument20 pagesPermanent Associate MembersRishi GandhiNo ratings yet

- Objectives of Financial StatementsDocument3 pagesObjectives of Financial StatementsNelly GomezNo ratings yet

- Electrical Schematics For Ex326 KCKDocument4 pagesElectrical Schematics For Ex326 KCKpeter sdnNo ratings yet

- Fib Assignment SolutionsDocument15 pagesFib Assignment SolutionsMusangabu EarnestNo ratings yet

- Request For Quotation Number (Doh-Gb50-2021)Document5 pagesRequest For Quotation Number (Doh-Gb50-2021)Belinda Williams100% (1)

- Lesson 2 - Advanced Financial Statement Analysis and ValuationDocument66 pagesLesson 2 - Advanced Financial Statement Analysis and ValuationNoel Salazar JrNo ratings yet

- SK BirDocument2 pagesSK BirGem LarezaNo ratings yet

- First Come First Serve Scheme 2022 CircularDocument2 pagesFirst Come First Serve Scheme 2022 CircularAshish SharmaNo ratings yet

- Economics Money Banking & International Trade-1Document18 pagesEconomics Money Banking & International Trade-1Nandan Gowda100% (1)

- Distribution Control: Salma ElsayedDocument29 pagesDistribution Control: Salma ElsayedSalma El SayedNo ratings yet

- AbstractDocument45 pagesAbstractMelvin BrionesNo ratings yet

- Study of Investments in Bonds PDFDocument67 pagesStudy of Investments in Bonds PDFMkingNo ratings yet

- Other Auto Companies & HR - PuneDocument65 pagesOther Auto Companies & HR - Punerutuja chaudhary100% (1)

- Portfolio Restructuring DilemmaDocument7 pagesPortfolio Restructuring DilemmaVarun AgrawalNo ratings yet

- GIP-Syllabus 2022Document4 pagesGIP-Syllabus 2022aadilkhan15082009No ratings yet

- RA Sand BlastingDocument2 pagesRA Sand BlastingAbdus Samad100% (1)

- CB Insights - Tech MA Report Q3 2023Document40 pagesCB Insights - Tech MA Report Q3 2023Ishrak ZamanNo ratings yet

- I-Kon™ Record Blast: Case StudyDocument1 pageI-Kon™ Record Blast: Case StudyRMRE UETNo ratings yet

- Social Science Majorship 1VDocument18 pagesSocial Science Majorship 1VGrenly A. TumandaNo ratings yet

- 9 - 29 - M&aDocument2 pages9 - 29 - M&aPham Ngoc VanNo ratings yet

- Paper No 123 - An Inquiry Into The Socio-Economic ConditionsDocument24 pagesPaper No 123 - An Inquiry Into The Socio-Economic ConditionsVibhu VikramadityaNo ratings yet

- International Cash Management - 1Document28 pagesInternational Cash Management - 1sanjeevbhadiarNo ratings yet

- Statement20undap20signing20ceremony 20by20j1Document3 pagesStatement20undap20signing20ceremony 20by20j1api-67201372No ratings yet

- Cpec A Threat or A Game Changer For PakistanDocument3 pagesCpec A Threat or A Game Changer For PakistanAyesha FakharNo ratings yet

- Chapter 5 Time Value of MoneyDocument25 pagesChapter 5 Time Value of MoneyAhmed FathelbabNo ratings yet

- Hatten Land Forms Joint Venture With Singapore Fintech Group Hydra XDocument4 pagesHatten Land Forms Joint Venture With Singapore Fintech Group Hydra XWeR1 Consultants Pte LtdNo ratings yet

- 2014 Primary MASMO Maths Registration FormDocument1 page2014 Primary MASMO Maths Registration FormKhairudin Abdul AzizNo ratings yet

- Gayangan, Jenny Ann C. Bsa 3 Cost Accounting Number 1 Answer: CDocument3 pagesGayangan, Jenny Ann C. Bsa 3 Cost Accounting Number 1 Answer: CKarlo PalerNo ratings yet

- Amalgamation VS AbsorptionDocument7 pagesAmalgamation VS AbsorptionAbhinav RandevNo ratings yet