You might also like

- Introduction To Government AccountingDocument34 pagesIntroduction To Government AccountingAnnamae Teoxon100% (1)

- Sample Financial Aid Appeal Letter Asking For More Money - Sample Letter HQDocument5 pagesSample Financial Aid Appeal Letter Asking For More Money - Sample Letter HQSeb TegNo ratings yet

- NISM Series XXII Fixed Income Securities Workbook May 2021Document182 pagesNISM Series XXII Fixed Income Securities Workbook May 2021Karthick S Nair100% (2)

- Exercise 3 - Group Accounts - SolutionDocument5 pagesExercise 3 - Group Accounts - SolutionAnh TramNo ratings yet

- Capital Budgeting Case StudyDocument3 pagesCapital Budgeting Case StudySafi Sheikh100% (1)

- GCash OrientationDocument27 pagesGCash OrientationArmiel SarmientoNo ratings yet

- Analiza FinanciaraDocument40 pagesAnaliza FinanciaraMarius LazarNo ratings yet

- Tugas 7 - ELRISKA TIFFANI - 142200111Document8 pagesTugas 7 - ELRISKA TIFFANI - 142200111Elriska Tiffani50% (2)

- Quiz 3 - Joint Obligations To Obligations With A Penal Clause - OBLICONDocument4 pagesQuiz 3 - Joint Obligations To Obligations With A Penal Clause - OBLICONmhikeedelantar100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAishwarya SenthilNo ratings yet

- FAR610 Consolidated Cashflow Past Semester FinalexamDocument18 pagesFAR610 Consolidated Cashflow Past Semester FinalexamANIS SYAKIRAH ADHWA MAHDILLAHNo ratings yet

- Cash Flow StatementDocument14 pagesCash Flow StatementMohd AtifNo ratings yet

- Assignment: Financial Ratios: Submitted byDocument4 pagesAssignment: Financial Ratios: Submitted byHarshit DalmiaNo ratings yet

- Jovero, Judith G. HRDM Iv-1 Mrs. Evelyn Celestial: The Components of Financial Statement Control EnvironmentDocument6 pagesJovero, Judith G. HRDM Iv-1 Mrs. Evelyn Celestial: The Components of Financial Statement Control EnvironmentKRISTINE CLAIRE VISTONo ratings yet

- Cash FlowsDocument12 pagesCash FlowsEjaz AhmadNo ratings yet

- FMDocument17 pagesFMRaghav Agarwal100% (3)

- SCF With DODocument3 pagesSCF With DOMuhammad Asif KhanNo ratings yet

- HE 2 Questions - Updated-1Document6 pagesHE 2 Questions - Updated-1halelz69No ratings yet

- Lecture 2 Answer1 1564205815261Document18 pagesLecture 2 Answer1 1564205815261Trinesh BhargavaNo ratings yet

- Cash Flow Statement Format: Add: Non-Cash Charges / Non-Business Expesnes Less: Non-Business IncomeDocument5 pagesCash Flow Statement Format: Add: Non-Cash Charges / Non-Business Expesnes Less: Non-Business IncomeTharani NagarajanNo ratings yet

- FinanceDocument34 pagesFinanceJared OtienoNo ratings yet

- Cash Flow Session With ExamplesDocument9 pagesCash Flow Session With ExamplesPAVAN KUMAR GUDAVALLETINo ratings yet

- Mo Hinh Ky Thuat Phan Tich Tai ChinhDocument39 pagesMo Hinh Ky Thuat Phan Tich Tai ChinhĐào Mạnh Quân Pete'rNo ratings yet

- Practice Session - 14 - MayDocument18 pagesPractice Session - 14 - MayprabhuNo ratings yet

- Answer #1: Total Current Liabilities 58709 Equipment Total Liabilities 68709Document9 pagesAnswer #1: Total Current Liabilities 58709 Equipment Total Liabilities 68709Abul Ala Daniyal QaziNo ratings yet

- Chemalite-B Cash Flow FormatDocument3 pagesChemalite-B Cash Flow FormatNishant WasadNo ratings yet

- WEEK 9 Solution To Questions On Statement of Cash FlowsDocument3 pagesWEEK 9 Solution To Questions On Statement of Cash Flowsvictoriaahmad95No ratings yet

- Topic 5 Workshop SolutionsDocument7 pagesTopic 5 Workshop SolutionsCậuBéQuàngKhănĐỏNo ratings yet

- Cash Flow Assignment 1Document9 pagesCash Flow Assignment 1Ramakrishna J RNo ratings yet

- 02 Profits, Cash Flows and Taxes - StudentsDocument25 pages02 Profits, Cash Flows and Taxes - StudentslmsmNo ratings yet

- Shareholders' Funds Reserves and SurplusDocument10 pagesShareholders' Funds Reserves and SurplusBalaji GaneshNo ratings yet

- SBS 19 20Document12 pagesSBS 19 20Arslan ShafqatNo ratings yet

- Chapter 17 Cash FlowDocument13 pagesChapter 17 Cash FlowToni MarquezNo ratings yet

- Assets Liabilities Equity Share Capital Retained Earnings No. Cash Supplies Rev. Exp. Account Receiveable Office Equipment Account PayableDocument16 pagesAssets Liabilities Equity Share Capital Retained Earnings No. Cash Supplies Rev. Exp. Account Receiveable Office Equipment Account PayableAhmad KholilNo ratings yet

- Shareholders' Funds Reserves and SurplusDocument3 pagesShareholders' Funds Reserves and SurplusBalaji GaneshNo ratings yet

- LF BC Corpo Correspondances EnoncéDocument2 pagesLF BC Corpo Correspondances Enoncévive la FranceNo ratings yet

- Statement of Cash FlowsDocument3 pagesStatement of Cash FlowsNihar MadkaikerNo ratings yet

- Numericals Schedule 3Document4 pagesNumericals Schedule 3Achyut AwasthiNo ratings yet

- An Overview of Financial Management: LessonDocument6 pagesAn Overview of Financial Management: LessonKliennt TorrejosNo ratings yet

- Final ExaminationsDocument5 pagesFinal ExaminationsBilal Khan BangashNo ratings yet

- Acc203 Assignment 2: Question 1-Corporate GovernanceDocument3 pagesAcc203 Assignment 2: Question 1-Corporate Governancesheenal naickerNo ratings yet

- Statement of Cash Flow: A Teaching NoteDocument6 pagesStatement of Cash Flow: A Teaching NoteMichealNo ratings yet

- Suggested Solution To Tutorial On SOCFDocument5 pagesSuggested Solution To Tutorial On SOCFLiyendra FernandoNo ratings yet

- Chapter 03 Financial Planning & ForecastingDocument18 pagesChapter 03 Financial Planning & ForecastingzamriNo ratings yet

- Transaction AssignmentDocument2 pagesTransaction AssignmentAbdullah - Al - Safoan 211-15-14629No ratings yet

- Cash Flow QuestionsDocument5 pagesCash Flow QuestionssigiryaNo ratings yet

- Malik Group of Companies (Disposal + Acquisition)Document1 pageMalik Group of Companies (Disposal + Acquisition).No ratings yet

- Ptedc CTRL: 2016 2015 Movement Analisis 1Document4 pagesPtedc CTRL: 2016 2015 Movement Analisis 1AnTonius TjandraNo ratings yet

- CORPORATE REPORTING Icag PDFDocument31 pagesCORPORATE REPORTING Icag PDFmohedNo ratings yet

- Orkshop Nswers: Bank A Bank B Assets Liabilities Assets LiabilitiesDocument7 pagesOrkshop Nswers: Bank A Bank B Assets Liabilities Assets LiabilitiesOmar SrourNo ratings yet

- Assg2 - Open UniversityDocument26 pagesAssg2 - Open UniversityAzrul MuhamedNo ratings yet

- 2016-2017 2017-2018 2018-2019 All Values in INR ThousandsDocument18 pages2016-2017 2017-2018 2018-2019 All Values in INR ThousandsSomlina MukherjeeNo ratings yet

- Practice Exam 1Document2 pagesPractice Exam 1Anonymous kE3eNfiFNo ratings yet

- FAWCM - Cash Flow 2Document29 pagesFAWCM - Cash Flow 2Jake RoosenbloomNo ratings yet

- Accounting 1Document2 pagesAccounting 1thu thienNo ratings yet

- Notes - Cash Flow Statement and ProblemsDocument4 pagesNotes - Cash Flow Statement and ProblemsDhruv MalhotraNo ratings yet

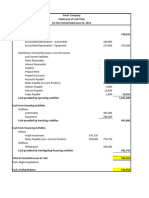

- CashFlow Smart CompanyDocument1 pageCashFlow Smart CompanyCheyenne CariasNo ratings yet

- Chapter 1-Problem 1 To 5: Charles Company Balance Sheet As On 31st Dec AssetsDocument9 pagesChapter 1-Problem 1 To 5: Charles Company Balance Sheet As On 31st Dec AssetsSimran HarchandaniNo ratings yet

- LF BC Corpo Correspondances CorrigéDocument4 pagesLF BC Corpo Correspondances Corrigévive la FranceNo ratings yet

- PFS - LO1 LTD Company Accounts - Questions 2021Document5 pagesPFS - LO1 LTD Company Accounts - Questions 2021Ludmila DorojanNo ratings yet

- HW2 - Preparing Statement of Cash FlowsDocument2 pagesHW2 - Preparing Statement of Cash FlowsDeepak KapoorNo ratings yet

- Financial Accounting by PmtycoonDocument56 pagesFinancial Accounting by PmtycoonsachinNo ratings yet

- AF1401 2020 Autumn Lecture 2Document38 pagesAF1401 2020 Autumn Lecture 2Dhan AnugrahNo ratings yet

- Group 2Document8 pagesGroup 2Gaurav SinghNo ratings yet

- Amity Global Business School Amity Global Business School: Valuation ConceptsDocument36 pagesAmity Global Business School Amity Global Business School: Valuation ConceptssachinremaNo ratings yet

- TUGAS AKUNTANSI DASAR PERTEMUAN 5 RICO ANANTA RANEX SAPUTRA NewDocument8 pagesTUGAS AKUNTANSI DASAR PERTEMUAN 5 RICO ANANTA RANEX SAPUTRA Newrico anantaNo ratings yet

- Basic Accounting: E) On January 4, He Bought Inventory Worth 200. He Sold Them For 400. While All The Purchases WereDocument3 pagesBasic Accounting: E) On January 4, He Bought Inventory Worth 200. He Sold Them For 400. While All The Purchases WereAditi VermaNo ratings yet

- Apl-Key AnswersDocument1 pageApl-Key AnswersAditi VermaNo ratings yet

- 2 Digital Marketing Glossary PDFDocument5 pages2 Digital Marketing Glossary PDFdenizsensozNo ratings yet

- First Name Surname Full Name Salary CommissionDocument26 pagesFirst Name Surname Full Name Salary CommissionAditi VermaNo ratings yet

- Compensation Options For Early Contributors Wolfpackbot: OriginalDocument1 pageCompensation Options For Early Contributors Wolfpackbot: OriginalMohamed FathiNo ratings yet

- 1-Conceptual Framework SummaryDocument11 pages1-Conceptual Framework Summaryyen yenNo ratings yet

- Session 7Document18 pagesSession 7Digvijay SinghNo ratings yet

- Social Science Research: Rachel E. Dwyer, Laura Mccloud, Randy HodsonDocument15 pagesSocial Science Research: Rachel E. Dwyer, Laura Mccloud, Randy Hodsonfignewton89No ratings yet

- The Acquisition of Consolidated Rail Corporation (A)Document15 pagesThe Acquisition of Consolidated Rail Corporation (A)Neetesh ThakurNo ratings yet

- Sample Coaching AgreementDocument2 pagesSample Coaching AgreementAmit DashNo ratings yet

- Colgate AR 2020.indd - PDFDocument100 pagesColgate AR 2020.indd - PDFali khanNo ratings yet

- S4hana Interest+CalculationsDocument23 pagesS4hana Interest+CalculationssrinivasNo ratings yet

- LK BMHS 30 September 2021Document71 pagesLK BMHS 30 September 2021samudraNo ratings yet

- TranslateDocument2 pagesTranslateBalmukund KumarNo ratings yet

- Project Management Final Paper 1Document10 pagesProject Management Final Paper 1JM SericaNo ratings yet

- Anggo Toyota Application FormDocument1 pageAnggo Toyota Application FormTempwell company Naga BranchNo ratings yet

- Three Perspectives On The Valuation of Derivative InstrumentsDocument10 pagesThree Perspectives On The Valuation of Derivative InstrumentsNiyati ShahNo ratings yet

- Quiz 8 - BTX 113Document3 pagesQuiz 8 - BTX 113Rae Vincent Revilla100% (1)

- Manorama InstituteDocument12 pagesManorama InstituteRuhi SaxenaNo ratings yet

- CPA Adeel ResumeDocument2 pagesCPA Adeel ResumeMH ULTRANo ratings yet

- BS Moudule 2Document5 pagesBS Moudule 2Ram VeenNo ratings yet

- Guidelines For TDS Deduction On Purchase of Immovable PropertyDocument4 pagesGuidelines For TDS Deduction On Purchase of Immovable Propertymib_santoshNo ratings yet

- Vivifi India Finance PVT LTDDocument11 pagesVivifi India Finance PVT LTDMohd lrfanNo ratings yet

- Muntiariani - NTUC Income-Security BondDocument2 pagesMuntiariani - NTUC Income-Security BondSyscom PrintingNo ratings yet

- Internship ReportDocument22 pagesInternship ReportBadari Nadh100% (1)

- 6 Igcse - Accounting - Errors - Past - Papers - UnlockedDocument58 pages6 Igcse - Accounting - Errors - Past - Papers - Unlockedshivom talrejaNo ratings yet

- A Project Report On Financial Statement of Icici Bank PuneDocument85 pagesA Project Report On Financial Statement of Icici Bank PuneAMIT K SINGH0% (1)