You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- RHB KWK 0722Document2 pagesRHB KWK 0722Besari Md DaudNo ratings yet

- Supply Chain Management of Coca-ColaDocument20 pagesSupply Chain Management of Coca-ColaAditya Dethe85% (33)

- Thesis 2Document50 pagesThesis 2EngrAbeer ArifNo ratings yet

- Mark Scheme: Accounting 5121Document12 pagesMark Scheme: Accounting 5121SaadArshadNo ratings yet

- Unit 1 Practice Exam 1Document8 pagesUnit 1 Practice Exam 1milk shakeNo ratings yet

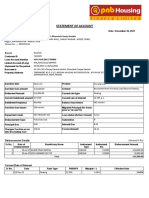

- Receivables Open Items Revaluation ReportDocument61 pagesReceivables Open Items Revaluation ReportShakhir MohunNo ratings yet

- 547 Abr 0000000083Document6 pages547 Abr 0000000083BERNACRIS REYESNo ratings yet

- Cash Budget: - This Budget Represents The Anticipated Receipts andDocument5 pagesCash Budget: - This Budget Represents The Anticipated Receipts andChristine JamesNo ratings yet

- BUAD 121 - Chapters 13, 14, 15 QuizDocument11 pagesBUAD 121 - Chapters 13, 14, 15 QuizKenisha ManicksinghNo ratings yet

- Acc 1102Document19 pagesAcc 1102Bonatan S. MuzzammilNo ratings yet

- 10 Quiz 1Document1 page10 Quiz 1Lovise DevanNo ratings yet

- 4 5805514475188521061Document8 pages4 5805514475188521061Gena HamdaNo ratings yet

- BusinessDocument13 pagesBusinessralph ghazziNo ratings yet

- AUDCLASS Midterm-ExamDocument7 pagesAUDCLASS Midterm-ExamBeverly MindoroNo ratings yet

- Sonai Gramin Bigarsheti Sahakari Patsanstha Maryadit: Loan Account Statement Date 02/05/2022 To 28/07/2022Document2 pagesSonai Gramin Bigarsheti Sahakari Patsanstha Maryadit: Loan Account Statement Date 02/05/2022 To 28/07/2022Bandopant KapaseNo ratings yet

- Class Work & Home Work Question of Final Account of Banking Conpany 22-23Document23 pagesClass Work & Home Work Question of Final Account of Banking Conpany 22-23DARK KING GamersNo ratings yet

- TOPIC 8 - Bank ReconciliationDocument4 pagesTOPIC 8 - Bank ReconciliationMOHD FITRI SAIMINo ratings yet

- Receivables ExerciseDocument3 pagesReceivables ExerciseJERICKO LIAN DEL ROSARIONo ratings yet

- Annual Statement of Provident Fund Accounts For The Year Ended 2006Document2 pagesAnnual Statement of Provident Fund Accounts For The Year Ended 2006DevNo ratings yet

- Ho Test JournalDocument14 pagesHo Test JournalEleonora VinessaNo ratings yet

- Cash BookDocument14 pagesCash BookSi Brian TohNo ratings yet

- ACC10008 Financial Information Systems Mid Semester Test - Semester 1, 2020Document8 pagesACC10008 Financial Information Systems Mid Semester Test - Semester 1, 2020Pratik GhimireNo ratings yet

- Q.P. Code: 62202: Managerial AccountingDocument6 pagesQ.P. Code: 62202: Managerial Accountinganshul bhutangeNo ratings yet

- Math Lit Session 1 - 4 Learner Guide 2023 EnglishDocument22 pagesMath Lit Session 1 - 4 Learner Guide 2023 EnglishSilindokuhle MazibukoNo ratings yet

- 2021 - Budget FormsDocument31 pages2021 - Budget FormsFreda Lyn Benito NamuroNo ratings yet

- Business School: ACCT1501 Accounting and Financial Management 1A Session 1 2016Document60 pagesBusiness School: ACCT1501 Accounting and Financial Management 1A Session 1 2016Sarthak GargNo ratings yet

- Quize 14Document15 pagesQuize 14Daniella Mae ElipNo ratings yet

- CPA 1 - Financial Accounting-1Document9 pagesCPA 1 - Financial Accounting-1LYNETTE NYAKAISIKI50% (2)

- 6a MTP Oct 2020Document13 pages6a MTP Oct 2020Bijay AgrawalNo ratings yet

- Annual Report Sikkim UniversityDocument54 pagesAnnual Report Sikkim UniversityAnirban LahiriNo ratings yet

- 6 PesDocument2 pages6 PessidraNo ratings yet

- Acc CH 8Document9 pagesAcc CH 8Trickster TwelveNo ratings yet

- Table 6.1 National Savings Schemes (Net Investment)Document2 pagesTable 6.1 National Savings Schemes (Net Investment)sidraNo ratings yet

- G Mango Accounting Pack Model DataDocument13 pagesG Mango Accounting Pack Model DataalphabetttNo ratings yet

- Irfan Fauzan Tugas 3Document25 pagesIrfan Fauzan Tugas 315 - Irfan Fauzan100% (1)

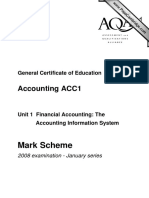

- Accounting Acc1 Unit 1 Financial Accounting: The Accounting Information SystemDocument16 pagesAccounting Acc1 Unit 1 Financial Accounting: The Accounting Information Systemsaffron parkesNo ratings yet

- Kenya Second Phase of The Arid Lands Resource Management Project INT Redacted Report 35Document1 pageKenya Second Phase of The Arid Lands Resource Management Project INT Redacted Report 35saurabh upadhyayNo ratings yet

- Cambridge O Level: Accounting 7707/23 October/November 2020Document14 pagesCambridge O Level: Accounting 7707/23 October/November 2020ImanNo ratings yet

- Tugas Pengantar Ak II (Daskun II)Document2 pagesTugas Pengantar Ak II (Daskun II)ElsNo ratings yet

- 'ACT1204 Audit of Cash and Cash Equivalents Quiz No. 4Document4 pages'ACT1204 Audit of Cash and Cash Equivalents Quiz No. 4markNo ratings yet

- MQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Document5 pagesMQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Rohit SoodNo ratings yet

- Paper 1Document9 pagesPaper 1Purity muchobellaNo ratings yet

- Statement 9923281112 30122022180050Document2 pagesStatement 9923281112 30122022180050Mohit ChinchkhedeNo ratings yet

- Bank Reporting Example NABILDocument54 pagesBank Reporting Example NABILSujit KoiralaNo ratings yet

- Bbe 1101 (Fund. of Accounting) Lecture Notes - Dealing With Bank OverdraftsDocument5 pagesBbe 1101 (Fund. of Accounting) Lecture Notes - Dealing With Bank OverdraftsSAMSON OYOO OTUKENENo ratings yet

- Finals QuizDocument12 pagesFinals QuizLeslie Beltran ChiangNo ratings yet

- AP - PreWeek - May 2022Document11 pagesAP - PreWeek - May 2022Miguel ManagoNo ratings yet

- Acc 3 Unit 3 Revision Questions 13Document12 pagesAcc 3 Unit 3 Revision Questions 13Danielle WatsonNo ratings yet

- Girdhar51 1603693312542 PDFDocument2 pagesGirdhar51 1603693312542 PDFjignesh parmarNo ratings yet

- Accounting 2020 Unit 1 KTT 6 - Solution BookDocument5 pagesAccounting 2020 Unit 1 KTT 6 - Solution BookJefferyNo ratings yet

- Formatted Brgy. Forms EditDocument21 pagesFormatted Brgy. Forms EditJoshua AssinNo ratings yet

- Bsbfia412-Case Study 2019Document15 pagesBsbfia412-Case Study 2019Pattaniya KosayothinNo ratings yet

- HI 5001 Accounting For Business DecisionsDocument5 pagesHI 5001 Accounting For Business Decisionsalka murarkaNo ratings yet

- Juni Sania - 201950493 - Jawaban UTS Aplikasi Audit Ganjil 20Document10 pagesJuni Sania - 201950493 - Jawaban UTS Aplikasi Audit Ganjil 20Cherry VanticaNo ratings yet

- BS Balaji Jan Kallyan 2020Document3 pagesBS Balaji Jan Kallyan 2020sanskar pandeyNo ratings yet

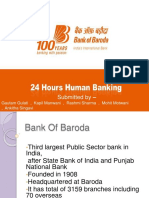

- Submitted by - : Gautam Gulati, Kapil Manwani, Rashmi Sharma, Mohit Motwani, Ankitha SingaviDocument36 pagesSubmitted by - : Gautam Gulati, Kapil Manwani, Rashmi Sharma, Mohit Motwani, Ankitha SingaviDipu SinghNo ratings yet

- Repayment ScheduleDocument3 pagesRepayment ScheduleSunil NNo ratings yet

- Edn - 74577 2Document2 pagesEdn - 74577 2narasimharao gorlaNo ratings yet

- Ase20093 01 Results Mark Scheme 220826 June 2022 SeriesDocument17 pagesAse20093 01 Results Mark Scheme 220826 June 2022 SeriesTheint ThiriNo ratings yet

- 2019 TSSM Exam 4 SolutionsDocument12 pages2019 TSSM Exam 4 Solutionsdyted73No ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- WelcomeDocument4 pagesWelcomeSaadArshadNo ratings yet

- New 789Document49 pagesNew 789SaadArshadNo ratings yet

- Urdu Sindhi Pashtu HelpDocument7 pagesUrdu Sindhi Pashtu HelpSaadArshadNo ratings yet

- KhachaDocument4 pagesKhachaSaadArshadNo ratings yet

- Hts LogDocument1 pageHts LogSaadArshadNo ratings yet

- Invoice No. 15: Quantity Description Unit Price TotalDocument1 pageInvoice No. 15: Quantity Description Unit Price TotalSaadArshadNo ratings yet

- Barcode-Generator deDocument8 pagesBarcode-Generator deSaadArshadNo ratings yet

- Gohar Golf Vista Payment ScheduleDocument6 pagesGohar Golf Vista Payment ScheduleSaadArshadNo ratings yet

- WelcomeDocument2 pagesWelcomeSaadArshadNo ratings yet

- Bill Saad Arshad Books 15-02-23Document5 pagesBill Saad Arshad Books 15-02-23SaadArshadNo ratings yet

- Bill Saad Arshad Books FinalDocument5 pagesBill Saad Arshad Books FinalSaadArshadNo ratings yet

- Mark Scheme June 2003 GCE: AccountingDocument11 pagesMark Scheme June 2003 GCE: AccountingSaadArshadNo ratings yet

- T Careers: Your HDocument27 pagesT Careers: Your HSaadArshadNo ratings yet

- Urdu Books Import Lahore Books DepoDocument6 pagesUrdu Books Import Lahore Books DepoSaadArshadNo ratings yet

- Noor e KareemDocument1 pageNoor e KareemSaadArshadNo ratings yet

- SahlibDocument273 pagesSahlibSaadArshadNo ratings yet

- Accounting Acc1 Unit 1 Financial Accounting: The Accounting Information SystemDocument12 pagesAccounting Acc1 Unit 1 Financial Accounting: The Accounting Information SystemSaadArshadNo ratings yet

- Accounting Acc1 Unit 1: Financial Accounting: The Accounting Information SystemDocument12 pagesAccounting Acc1 Unit 1: Financial Accounting: The Accounting Information SystemSaadArshadNo ratings yet

- Term Test OrganicDocument11 pagesTerm Test OrganicSaadArshadNo ratings yet

- Accounting Acc1 Unit 1 Financial Accounting: The Accounting Information SystemDocument12 pagesAccounting Acc1 Unit 1 Financial Accounting: The Accounting Information SystemSaadArshadNo ratings yet

- 27 Units Rs. 186.56: MR Anwar Hussain RanaDocument2 pages27 Units Rs. 186.56: MR Anwar Hussain RanaSaadArshadNo ratings yet

- 337 Units: Mansoor Ali DamaniDocument2 pages337 Units: Mansoor Ali DamaniSaadArshadNo ratings yet

- Accounting Acc1 Unit 1: Financial Accounting: The Accounting Information SystemDocument11 pagesAccounting Acc1 Unit 1: Financial Accounting: The Accounting Information SystemSaadArshadNo ratings yet

- Mark Scheme January 2004: AccountingDocument13 pagesMark Scheme January 2004: AccountingSaadArshadNo ratings yet

- Mark Scheme: Accounting ACC1Document12 pagesMark Scheme: Accounting ACC1SaadArshadNo ratings yet

- Mark Scheme: Accounting 5121Document14 pagesMark Scheme: Accounting 5121SaadArshadNo ratings yet

- June Series: AccountingDocument12 pagesJune Series: AccountingSaadArshadNo ratings yet

- Mark Scheme: Accounting ACC1Document11 pagesMark Scheme: Accounting ACC1SaadArshadNo ratings yet

- Commercial StudiesDocument3 pagesCommercial StudiesChandu SagiliNo ratings yet

- How To Create A Pitch Deck For InvestorsDocument2 pagesHow To Create A Pitch Deck For InvestorsRoselyn MatienzoNo ratings yet

- Outlier Innovations - Promotional ActivityDocument2 pagesOutlier Innovations - Promotional ActivitySiddharthNo ratings yet

- Perkin Elmer Icp Oes Winlab User GuideDocument569 pagesPerkin Elmer Icp Oes Winlab User GuideLuz Contreras50% (2)

- DataScience - SeminarDocument21 pagesDataScience - Seminariyasu ayenekuluNo ratings yet

- Hospitality: Our Custom Solutions Will Ensure That Each of Your Client's ClientDocument20 pagesHospitality: Our Custom Solutions Will Ensure That Each of Your Client's ClientgauravchauNo ratings yet

- People in OrganisationsDocument8 pagesPeople in OrganisationsBritney valladares100% (1)

- Inndividual Assignment Muhammad Fahmi Farhan Ikmal Bin Azhar Kamal 20C133Document8 pagesInndividual Assignment Muhammad Fahmi Farhan Ikmal Bin Azhar Kamal 20C133Fahmi FarhanNo ratings yet

- 1-DD-Akron-CORA-9519705-PROP-60 Months Commercial Paint Delivery 2018-07-18 PDFDocument3 pages1-DD-Akron-CORA-9519705-PROP-60 Months Commercial Paint Delivery 2018-07-18 PDFTolias EgwNo ratings yet

- Compehensive Competency Framework For The Federal Civil Service - Ver 1Document113 pagesCompehensive Competency Framework For The Federal Civil Service - Ver 1Leke OshiyemiNo ratings yet

- JK Jute Mills BIFR CaseDocument44 pagesJK Jute Mills BIFR CaseHemanth RaoNo ratings yet

- HRM Black BookDocument152 pagesHRM Black Book83 BJANVI JADHAVNo ratings yet

- BME01.HM3C.Chapter 9. Roa, GiovanniDocument5 pagesBME01.HM3C.Chapter 9. Roa, Giovannigiovanni roaNo ratings yet

- Business Ethics Now Chapter10Document13 pagesBusiness Ethics Now Chapter10AshchrisNo ratings yet

- Pronto Xi 760 - Foundation - Developer ToolsDocument6 pagesPronto Xi 760 - Foundation - Developer ToolsNéstor WaldydNo ratings yet

- 01.07.2021 Method Statement For Backfilling, Levelling & Compacting of Tie-InDocument7 pages01.07.2021 Method Statement For Backfilling, Levelling & Compacting of Tie-InPangky AbasoloNo ratings yet

- Advanced Financial Accounting & Reporting Business CombinationDocument8 pagesAdvanced Financial Accounting & Reporting Business CombinationAnonymous YtNo ratings yet

- Mid-Term Examination CB-EDocument2 pagesMid-Term Examination CB-EAli HassanNo ratings yet

- Accounting For Special Transaction 1Document9 pagesAccounting For Special Transaction 1Timon CarandangNo ratings yet

- SCM PPT StarbucksDocument11 pagesSCM PPT StarbucksMa Htay OoNo ratings yet

- What Is The General Objective of Planning For An Audit?Document2 pagesWhat Is The General Objective of Planning For An Audit?FuturamaramaNo ratings yet

- AC2024 ProblemDocument11 pagesAC2024 ProblemYashvardhan ChauhanNo ratings yet

- Learning Resource 7:: Share-Based CompensationDocument6 pagesLearning Resource 7:: Share-Based CompensationVianca Marella SamonteNo ratings yet

- Tyne MouldsDocument8 pagesTyne MouldsLevel BusinessNo ratings yet

- A Guide To Collecting & Investing - 2019Document21 pagesA Guide To Collecting & Investing - 2019steveNo ratings yet

- BIM - Building Information ModellingDocument20 pagesBIM - Building Information ModellingSyeda SumayyaNo ratings yet

- Product Details - Industry Mall - Siemens WWDocument1 pageProduct Details - Industry Mall - Siemens WWmateusT850No ratings yet

- Folleto. GA1-240202501-AA2-EV01.Document2 pagesFolleto. GA1-240202501-AA2-EV01.madeleinh vargasNo ratings yet