You might also like

- Quant Core 2020 exam breakdownDocument32 pagesQuant Core 2020 exam breakdownGabriel RoblesNo ratings yet

- MathEcon17 FinalExam SolutionDocument13 pagesMathEcon17 FinalExam SolutionCours HECNo ratings yet

- Exercises 4,5,6,7+test CanvasDocument5 pagesExercises 4,5,6,7+test CanvasEduardo MuñozNo ratings yet

- Econometrics 2012 ExamDocument9 pagesEconometrics 2012 ExamLuca SomigliNo ratings yet

- MTH3251 Financial Mathematics Exercise Book 15Document18 pagesMTH3251 Financial Mathematics Exercise Book 15DfcNo ratings yet

- JRF Qror QRB 2019Document4 pagesJRF Qror QRB 2019Rashmi SahooNo ratings yet

- STA 2101 Assignment 1 ReviewDocument8 pagesSTA 2101 Assignment 1 ReviewdflamsheepsNo ratings yet

- MATH1005 Final Exam From 2021Document14 pagesMATH1005 Final Exam From 2021Spamy SpamNo ratings yet

- UMich Math 404 Differential Equations HomeworkDocument2 pagesUMich Math 404 Differential Equations HomeworkSpencer DangNo ratings yet

- Problem Set #1. Due Sept. 9 2020.: MAE 501 - Fall 2020. Luc Deike, Anastasia Bizyaeva, Jiarong Wu September 2, 2020Document3 pagesProblem Set #1. Due Sept. 9 2020.: MAE 501 - Fall 2020. Luc Deike, Anastasia Bizyaeva, Jiarong Wu September 2, 2020Francisco SáenzNo ratings yet

- Midterm One 6711 F 10Document2 pagesMidterm One 6711 F 10Songya PanNo ratings yet

- PHD Comprehensive Exams Study Guide PDFDocument115 pagesPHD Comprehensive Exams Study Guide PDFMDraakNo ratings yet

- MIT18 S096F13 Pset2Document4 pagesMIT18 S096F13 Pset2TheoNo ratings yet

- Vmls Additional ExercisesDocument66 pagesVmls Additional ExercisesmarcosilvasegoviaNo ratings yet

- CQF Module 2 Examination: InstructionsDocument3 pagesCQF Module 2 Examination: InstructionsPrathameshSagareNo ratings yet

- QuestionDocument4 pagesQuestionManabendra GiriNo ratings yet

- Financial Econometrics AssignmentDocument14 pagesFinancial Econometrics AssignmentYuhan KENo ratings yet

- Tutorial Sheet 1Document3 pagesTutorial Sheet 1Thomas MannNo ratings yet

- Exam February 2015Document4 pagesExam February 2015zaurNo ratings yet

- HW3Document2 pagesHW3SNo ratings yet

- Math2801 2017 S1Document6 pagesMath2801 2017 S1JamesG_112No ratings yet

- Summative AssessmentDocument31 pagesSummative AssessmentAli Hammad ShahNo ratings yet

- Exercises Units 1,2,3Document8 pagesExercises Units 1,2,3Eduardo MuñozNo ratings yet

- Paperia 1 2022Document7 pagesPaperia 1 2022MauricioNo ratings yet

- Test1213 2qDocument3 pagesTest1213 2qmeettoavi059No ratings yet

- 103 ExercisesDocument70 pages103 Exerciseshungbkpro90No ratings yet

- Advanced Macroeconomics I Exam QuestionsDocument3 pagesAdvanced Macroeconomics I Exam QuestionszaurNo ratings yet

- 2016 MidtermDocument9 pages2016 MidtermThapelo SebolaiNo ratings yet

- Stochastic Calculus Midterm Exam: Prof. D. Filipovi C, E. Hapnes 29.10.2019Document2 pagesStochastic Calculus Midterm Exam: Prof. D. Filipovi C, E. Hapnes 29.10.2019UasdafNo ratings yet

- Midterm 2019Document2 pagesMidterm 2019UasdafNo ratings yet

- LEARNING RATIONAL FUNCTIONS, EQUATIONS AND INEQUALITIESDocument18 pagesLEARNING RATIONAL FUNCTIONS, EQUATIONS AND INEQUALITIESFaith Alquiza VillanuevaNo ratings yet

- Homework 2Document4 pagesHomework 2jerryNo ratings yet

- MAST90083 2021 S2 Exam PaperDocument4 pagesMAST90083 2021 S2 Exam Paperxiaotianxue84No ratings yet

- TUM Chair of Mathematical Finance Exercise Sheet 6Document2 pagesTUM Chair of Mathematical Finance Exercise Sheet 6Ka Wing HoNo ratings yet

- Pure maths IV exam assesses advanced topicsDocument5 pagesPure maths IV exam assesses advanced topicsnwokolobia nelsonNo ratings yet

- Mathematical Tripos: at The End of The ExaminationDocument26 pagesMathematical Tripos: at The End of The ExaminationDedliNo ratings yet

- Mathematical Tripos Part IADocument7 pagesMathematical Tripos Part IAChristopher HitchensNo ratings yet

- Problem Set 2: InstructionsDocument4 pagesProblem Set 2: InstructionsballechaseNo ratings yet

- ECON326 MidtermDocument5 pagesECON326 MidtermearlniewongcuirsNo ratings yet

- Coursework2 ProblemsDocument4 pagesCoursework2 ProblemsMikolaj PisarczykowskiNo ratings yet

- Libro Fasshauer Numerico AvanzadoDocument151 pagesLibro Fasshauer Numerico AvanzadoCarlysMendozaamorNo ratings yet

- Mathematical Association of AmericaDocument9 pagesMathematical Association of AmericathonguyenNo ratings yet

- 2023ScholarshipPaper FINALDocument13 pages2023ScholarshipPaper FINALabood fazilNo ratings yet

- Homework 1Document4 pagesHomework 1Bilal Yousaf0% (1)

- Unit 4Document15 pagesUnit 4Jyo ReddyNo ratings yet

- Assignment2 PDFDocument2 pagesAssignment2 PDFlaraNo ratings yet

- 1003 Handouts MathDocument35 pages1003 Handouts MathAquaNo ratings yet

- First Midterm ExamDocument10 pagesFirst Midterm ExamDebajyoti DattaNo ratings yet

- Putnam Linear AlgebraDocument6 pagesPutnam Linear AlgebrainfinitesimalnexusNo ratings yet

- Mathematical Association of AmericaDocument9 pagesMathematical Association of AmericathonguyenNo ratings yet

- Before You Begin Read These Instructions Carefully: Mathematical Tripos Part IADocument7 pagesBefore You Begin Read These Instructions Carefully: Mathematical Tripos Part IAZombie HeadNo ratings yet

- AF PS3 2014 15 SolutionDocument10 pagesAF PS3 2014 15 SolutionrtchuidjangnanaNo ratings yet

- Math5335 2018Document5 pagesMath5335 2018Peper12345No ratings yet

- 2015 Mock MT105ADocument4 pages2015 Mock MT105ANguyễn Đức Bình GiangNo ratings yet

- Shanghai Jiaotong University Shanghai Advanced Institution of FinanceDocument3 pagesShanghai Jiaotong University Shanghai Advanced Institution of FinanceIvan WangNo ratings yet

- Assignment 1Document2 pagesAssignment 1kfcsh5cbrcNo ratings yet

- Exercise1 BDocument2 pagesExercise1 Bapi-3737025No ratings yet

- Multiple Regression Analyisis ClearDocument27 pagesMultiple Regression Analyisis ClearArbi ChaimaNo ratings yet

- 1314sem1 Ma2213Document4 pages1314sem1 Ma2213jlee970125No ratings yet

- A-level Maths Revision: Cheeky Revision ShortcutsFrom EverandA-level Maths Revision: Cheeky Revision ShortcutsRating: 3.5 out of 5 stars3.5/5 (8)

- Estimating Parameters from SignalsDocument21 pagesEstimating Parameters from SignalsShedrine WamukekheNo ratings yet

- The Punctuation GuideDocument4 pagesThe Punctuation GuideShedrine WamukekheNo ratings yet

- OR Post: AZA Group. Investment in A HotelDocument8 pagesOR Post: AZA Group. Investment in A HotelShedrine WamukekheNo ratings yet

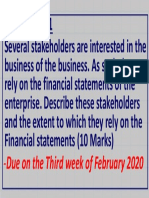

- Assignment 1: - Due On The Third Week of February 2020Document1 pageAssignment 1: - Due On The Third Week of February 2020Shedrine WamukekheNo ratings yet

- Stakeholders Who Uses Financial StatementsDocument4 pagesStakeholders Who Uses Financial StatementsShedrine WamukekheNo ratings yet

- Stakeholders Who Uses Financial StatementsDocument4 pagesStakeholders Who Uses Financial StatementsShedrine WamukekheNo ratings yet

- Theory of Estimation Ama 4306Document4 pagesTheory of Estimation Ama 4306Shedrine WamukekheNo ratings yet

- BMM 4107-International Trade Practices (A) - Yr 1 - S2Document2 pagesBMM 4107-International Trade Practices (A) - Yr 1 - S2Shedrine WamukekheNo ratings yet

- Risk Management: University of LeedsDocument47 pagesRisk Management: University of LeedsShedrine WamukekheNo ratings yet

- International Trade and Markets AssignmentDocument1 pageInternational Trade and Markets AssignmentShedrine WamukekheNo ratings yet

- MSc Dissertation HandbookDocument5 pagesMSc Dissertation HandbookShedrine WamukekheNo ratings yet

- Cost Accounting Question BankDocument48 pagesCost Accounting Question BankShedrine WamukekheNo ratings yet

- Numerical Analysis I Sma 2471Document3 pagesNumerical Analysis I Sma 2471Shedrine WamukekheNo ratings yet

- RM 2021 S2+ITLS6201 Individual Assignment Topics Rm10082021 v2Document1 pageRM 2021 S2+ITLS6201 Individual Assignment Topics Rm10082021 v2Shedrine WamukekheNo ratings yet

- CSCE-5150 Analysis of Computer Algorithms Homework 2: Question 1. (20 Points)Document2 pagesCSCE-5150 Analysis of Computer Algorithms Homework 2: Question 1. (20 Points)Shedrine WamukekheNo ratings yet

- Alpha Divergence About PCCADocument5 pagesAlpha Divergence About PCCAShedrine WamukekheNo ratings yet

- Dissertation Project YousryDocument5 pagesDissertation Project YousryShedrine WamukekheNo ratings yet

- 1101IBA Final Exam Case Study (B) Relying On Quality To Bring ControlDocument2 pages1101IBA Final Exam Case Study (B) Relying On Quality To Bring ControlShedrine WamukekheNo ratings yet

- Section B Moodle Assignment Practice Question - Apple Module 3 Tri 2, 21Document2 pagesSection B Moodle Assignment Practice Question - Apple Module 3 Tri 2, 21Shedrine WamukekheNo ratings yet

- Unit 1 Basic Mathematics For ManagementDocument229 pagesUnit 1 Basic Mathematics For ManagementkokueiNo ratings yet

- Optimize Structural Loads with Unknown FactorsDocument5 pagesOptimize Structural Loads with Unknown Factorslam phamNo ratings yet

- CS 9618 NotesDocument17 pagesCS 9618 NotesHaneyya UmerNo ratings yet

- The Math of Deep Learning Neural Networks Simplified (Part 2Document9 pagesThe Math of Deep Learning Neural Networks Simplified (Part 2agalassiNo ratings yet

- Module 2 Part 1: Vectors, Motion Along A Straight LineDocument29 pagesModule 2 Part 1: Vectors, Motion Along A Straight LineMelanie AbaldeNo ratings yet

- The Bakhshali ManuscriptDocument200 pagesThe Bakhshali ManuscriptArun Kumar Upadhyay100% (2)

- Extra CreditDocument1 pageExtra Creditapi-247933688No ratings yet

- Math 20.3 - Mathworks 11 Workbook PDFDocument125 pagesMath 20.3 - Mathworks 11 Workbook PDFKarol Kamieniecki100% (1)

- MA214LectureNotesFULL PDFDocument273 pagesMA214LectureNotesFULL PDFAryan MishraNo ratings yet

- Direct Step Method PDFDocument5 pagesDirect Step Method PDFDeepankumar Athiyannan0% (1)

- 2nd Periodical TESTDocument3 pages2nd Periodical TESTEvangelyn Bartolay67% (6)

- MR3 SolutionsDocument27 pagesMR3 SolutionsViet Quoc HoangNo ratings yet

- Calculating torsion in narrow rectangular and hollow cross sectionsDocument10 pagesCalculating torsion in narrow rectangular and hollow cross sectionsbatmanbittuNo ratings yet

- Talent and Olympiad Exams Resource Book Class 8 Math Brain Mapping Academy Hyderabad For IIT JEE Foundation Practice Test SeriesDocument136 pagesTalent and Olympiad Exams Resource Book Class 8 Math Brain Mapping Academy Hyderabad For IIT JEE Foundation Practice Test Seriesamit nigam72% (18)

- "Examen Final 3er Corte - Planeación de Producción" 1Document6 pages"Examen Final 3er Corte - Planeación de Producción" 1Juan Camilo AlfonsoNo ratings yet

- Norman Thomson Functional Programming With APLDocument2 pagesNorman Thomson Functional Programming With APLalexNo ratings yet

- ProbabilitProbability With Martingalesy With MartingalesDocument265 pagesProbabilitProbability With Martingalesy With MartingalesingramkNo ratings yet

- MA1505 12S2 Mid-Term Test InformationDocument6 pagesMA1505 12S2 Mid-Term Test InformationamehbeeNo ratings yet

- Design Via Root LocusDocument53 pagesDesign Via Root LocusAhmed ShareefNo ratings yet

- Mathematical Induction and RecursionDocument11 pagesMathematical Induction and RecursionJoseph DacanayNo ratings yet

- C Programming NotesDocument57 pagesC Programming NotesRAJESHNo ratings yet

- ch3 p01-50Document50 pagesch3 p01-50Jeanne JacksonNo ratings yet

- 1.1 MCQ+FRQ: Ap Calculus BC Scoring GuideDocument11 pages1.1 MCQ+FRQ: Ap Calculus BC Scoring Guidebl2ckiceNo ratings yet

- Multi-Step Word Problems in FractionsDocument2 pagesMulti-Step Word Problems in Fractionsjohnny abalosNo ratings yet

- Define Program, Course and Intended Learning OutcomesDocument6 pagesDefine Program, Course and Intended Learning OutcomesAime A. Alangue100% (1)

- Hyperbolas Part 1 T. BlessyTEDocument49 pagesHyperbolas Part 1 T. BlessyTEMando TejeroNo ratings yet

- 1101 12 Business Maths em Study MaterialDocument14 pages1101 12 Business Maths em Study MaterialKUMAR SENTHILNo ratings yet

- Response of A Continuous Guideway On Equally Spaced Supports Traversed by A Moving VehicleDocument7 pagesResponse of A Continuous Guideway On Equally Spaced Supports Traversed by A Moving VehicleanirbanNo ratings yet

- QbasicDocument9 pagesQbasicmustaphaNo ratings yet