You might also like

- Accountancy and Auditing-2017Document5 pagesAccountancy and Auditing-2017Jassmine RoseNo ratings yet

- Accounting For Managers-Assignment MaterialsDocument4 pagesAccounting For Managers-Assignment MaterialsYehualashet TeklemariamNo ratings yet

- Exam 19111Document6 pagesExam 19111atallah97No ratings yet

- Man Acc Qs 1Document6 pagesMan Acc Qs 1Tehniat Zafar0% (1)

- Bella Beauty Salon Adjusting Journal EntriesDocument7 pagesBella Beauty Salon Adjusting Journal EntriesFawad ShahNo ratings yet

- Pre Finals Manacc 1Document8 pagesPre Finals Manacc 1Gesselle Acebedo0% (1)

- IPE 481 - Term Final Question - January 2020Document6 pagesIPE 481 - Term Final Question - January 2020Shaumik RahmanNo ratings yet

- Review Myron Corporation's seasonal product sales budget and production requirementsDocument8 pagesReview Myron Corporation's seasonal product sales budget and production requirementsmohammad bilalNo ratings yet

- Kuis UTS Genap 21-22 ACCDocument3 pagesKuis UTS Genap 21-22 ACCNatasya FlorenciaNo ratings yet

- Quiz 2 - 09.10.18 Set A BDocument4 pagesQuiz 2 - 09.10.18 Set A BRey Joyce AbuelNo ratings yet

- Cost and Management Accounting -II - Work SheetDocument7 pagesCost and Management Accounting -II - Work SheetBeamlak WegayehuNo ratings yet

- Operational Budget Assignment IIIDocument7 pagesOperational Budget Assignment IIIzeritu tilahunNo ratings yet

- 202E06Document21 pages202E06foxstupidfoxNo ratings yet

- Lecture 7-8 Working CapitalDocument18 pagesLecture 7-8 Working CapitalAfzal AhmedNo ratings yet

- Tutorial 1Document5 pagesTutorial 1FEI FEINo ratings yet

- Budgets Exercises StudentDocument5 pagesBudgets Exercises Studentديـنـا عادل0% (1)

- Auditing 2019 P S CH 8Document16 pagesAuditing 2019 P S CH 8barakat801No ratings yet

- ACC 1110 Introductory Managerial Accounting Practice Final ExamDocument24 pagesACC 1110 Introductory Managerial Accounting Practice Final ExamMariela CNo ratings yet

- Ex06 - Comprehensive BudgetingDocument14 pagesEx06 - Comprehensive BudgetingANa Cruz100% (2)

- BREAK EVEN ANALYSISDocument7 pagesBREAK EVEN ANALYSISZubair JuttNo ratings yet

- Variable and Absorption Costing AnalysisDocument12 pagesVariable and Absorption Costing AnalysismeriiNo ratings yet

- 2.3 Paper 2.3 - Accounting For Business - 1Document6 pages2.3 Paper 2.3 - Accounting For Business - 1Himanshu SinghNo ratings yet

- Exam161 10Document7 pagesExam161 10patelp4026No ratings yet

- Cma Part 1 Mock 2Document44 pagesCma Part 1 Mock 2armaghan175% (8)

- MCQs Problems For Merchandising Business - For UploadDocument8 pagesMCQs Problems For Merchandising Business - For UploadIrish Trisha PerezNo ratings yet

- Cash Sales Credit Sales: ACCT201B Practice Questions Chapter 8Document9 pagesCash Sales Credit Sales: ACCT201B Practice Questions Chapter 8GuinevereNo ratings yet

- Drills - Comprehensive BudgetingDocument11 pagesDrills - Comprehensive BudgetingDan RyanNo ratings yet

- HI5017 Tutorial Question Assignment T2 2020Document10 pagesHI5017 Tutorial Question Assignment T2 2020shikha khanejaNo ratings yet

- Managerial Accounting AssignmentDocument7 pagesManagerial Accounting AssignmentBedri M Ahmedu100% (1)

- Exam2505 2012Document8 pagesExam2505 2012Gemeda GirmaNo ratings yet

- HW 2.2 Afm SendDocument10 pagesHW 2.2 Afm SendAbiodun OlokodanaNo ratings yet

- Exam189 10Document6 pagesExam189 10Rabah ElmasriNo ratings yet

- CVP Analysis and Absorption vs Variable CostingDocument3 pagesCVP Analysis and Absorption vs Variable CostingBenjamin0% (1)

- Trắc NghiệmDocument50 pagesTrắc NghiệmNGÂN CAO NGUYỄN HOÀNNo ratings yet

- STRATEGIC COSTMan QUIZ 3Document5 pagesSTRATEGIC COSTMan QUIZ 3StephannieArreolaNo ratings yet

- Cost AssignmentDocument4 pagesCost AssignmentSYED MUHAMMAD MOOSA RAZANo ratings yet

- Practical QuestionsDocument5 pagesPractical QuestionsBui Thi Lan Anh (FGW HCM)No ratings yet

- ENT 2Document4 pagesENT 2lubaajamesNo ratings yet

- San Pedro College: Accounting & Financial ManagementDocument4 pagesSan Pedro College: Accounting & Financial ManagementJuan FrivaldoNo ratings yet

- Budgeting and Variance Analysis QuestionsDocument13 pagesBudgeting and Variance Analysis QuestionsAli Rizwan100% (1)

- In Case of Doubts in Answers, Whatsapp 9730768982: Cost & Management Accounting - December 2019Document16 pagesIn Case of Doubts in Answers, Whatsapp 9730768982: Cost & Management Accounting - December 2019Ashutosh shahNo ratings yet

- Quality Cost Report ClassificationsDocument4 pagesQuality Cost Report ClassificationsPopol KupaNo ratings yet

- WCM NotesDocument2 pagesWCM NotesTharunNo ratings yet

- HI5017 Progressive Tutorial Question Assignment T2 2020 PDFDocument8 pagesHI5017 Progressive Tutorial Question Assignment T2 2020 PDFIkramNo ratings yet

- Ac 313 Marginal and Absorption CostingDocument4 pagesAc 313 Marginal and Absorption CostingAlex MaugoNo ratings yet

- Deso 04Document5 pagesDeso 04Nguyễn Quốc TuấnNo ratings yet

- Statement of Comprehensive Income (SCI) for Merchandising BusinessDocument23 pagesStatement of Comprehensive Income (SCI) for Merchandising BusinessMark Joseph BielzaNo ratings yet

- Seminar 11answer Group 10Document75 pagesSeminar 11answer Group 10Shweta Sridhar40% (5)

- Rift Valley University Yeka Campus Department of Accounting and Finance Assignment Of: Cost and ManagementiiDocument8 pagesRift Valley University Yeka Campus Department of Accounting and Finance Assignment Of: Cost and ManagementiiGet HabeshaNo ratings yet

- Management Accounting HWDocument5 pagesManagement Accounting HWHw SolutionNo ratings yet

- Advanced Managerial Accounting Final Exam Questions Gaza Company Project NPV IRRDocument7 pagesAdvanced Managerial Accounting Final Exam Questions Gaza Company Project NPV IRRRabah ElmasriNo ratings yet

- Modul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662Document30 pagesModul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662hendy DidoNo ratings yet

- BASTRCSX-Learning-Activity-5_with-answersDocument10 pagesBASTRCSX-Learning-Activity-5_with-answersChel EscuetaNo ratings yet

- ACT 202 Final Assignment Submission June 2020Document7 pagesACT 202 Final Assignment Submission June 2020Saiful Islam HridoyNo ratings yet

- Mid-Term Exam - SolutionDocument8 pagesMid-Term Exam - Solutionhababammar660No ratings yet

- AE24 Lesson 5Document9 pagesAE24 Lesson 5Majoy BantocNo ratings yet

- Quizz C1Document10 pagesQuizz C1Phương Vy TrầnNo ratings yet

- AFIN317 2016 Semester 1 Final ExamDocument7 pagesAFIN317 2016 Semester 1 Final ExamSandra K JereNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- File 2Document41 pagesFile 2Taslima AktarNo ratings yet

- IFA PL I Solution CMA June 2020 ExamDocument6 pagesIFA PL I Solution CMA June 2020 ExamTaslima AktarNo ratings yet

- IFA PL I Solution CMA June 2020 ExamDocument6 pagesIFA PL I Solution CMA June 2020 ExamTaslima AktarNo ratings yet

- MD Shohag Al-Mamun MBS ACMADocument6 pagesMD Shohag Al-Mamun MBS ACMATaslima AktarNo ratings yet

- IFA PL I Solution CMA June 2020 ExamDocument6 pagesIFA PL I Solution CMA June 2020 ExamTaslima AktarNo ratings yet

- IOM Personal History FormDocument4 pagesIOM Personal History Formnakib sarker100% (1)

- Research Proposal GuideDocument6 pagesResearch Proposal GuideTaslima AktarNo ratings yet

- Model Solutions: Cma December, 2020 Examination Professional Level - I Subject: 101. Intermediate Financial AccountingDocument7 pagesModel Solutions: Cma December, 2020 Examination Professional Level - I Subject: 101. Intermediate Financial AccountingTaslima AktarNo ratings yet

- Internship Report On Financial Analysis of A. G. Dresses Limited of Pinaki Group'Document7 pagesInternship Report On Financial Analysis of A. G. Dresses Limited of Pinaki Group'Taslima Aktar100% (1)

- New Master Paper (2nd Part)Document1 pageNew Master Paper (2nd Part)Taslima AktarNo ratings yet

- Biodata BanglaDocument2 pagesBiodata BanglaTaslima AktarNo ratings yet

- Letter of Transmittal Letter of Endorsement Acknowledgements Executive SummaryDocument3 pagesLetter of Transmittal Letter of Endorsement Acknowledgements Executive SummaryTaslima AktarNo ratings yet

- Importance of Financial Statement Analysis for Business Decision MakingDocument4 pagesImportance of Financial Statement Analysis for Business Decision MakingTaslima AktarNo ratings yet

- List of GraphsDocument1 pageList of GraphsTaslima AktarNo ratings yet

- 1.2. Rationale of The StudyDocument2 pages1.2. Rationale of The StudyTaslima AktarNo ratings yet

- Internship Report On Analysis of Financial Statements of A. G. Dresses Limited of Pinaki GroupDocument2 pagesInternship Report On Analysis of Financial Statements of A. G. Dresses Limited of Pinaki GroupTaslima AktarNo ratings yet

- Financial Statement of A.G, Dresess LTDDocument4 pagesFinancial Statement of A.G, Dresess LTDTaslima AktarNo ratings yet

- 123Document20 pages123Taslima AktarNo ratings yet

- New Master Paper (1ST Part)Document6 pagesNew Master Paper (1ST Part)Taslima AktarNo ratings yet

- MF PDFDocument2 pagesMF PDFTaslima AktarNo ratings yet

- CV 01Document1 pageCV 01Taslima AktarNo ratings yet

- CV 02Document1 pageCV 02Taslima AktarNo ratings yet

- AdDocument4 pagesAdTaslima AktarNo ratings yet

- Project of Anis 01Document8 pagesProject of Anis 01Taslima AktarNo ratings yet

- Mba182 CR 241019Document1 pageMba182 CR 241019Taslima AktarNo ratings yet

- Project of Anis 01Document8 pagesProject of Anis 01Taslima AktarNo ratings yet

- Mba182 Ais4 311019Document26 pagesMba182 Ais4 311019Taslima AktarNo ratings yet

- Town of BrightonDocument1 pageTown of BrightonTaslima AktarNo ratings yet

- 1Document15 pages1Taslima AktarNo ratings yet

- Chapter Five: Corporation Organization and OperationDocument8 pagesChapter Five: Corporation Organization and OperationSamuel DebebeNo ratings yet

- FRM2023 Candidate Guide EnglishDocument20 pagesFRM2023 Candidate Guide EnglishShhshshshNo ratings yet

- LEI Bulk - 1000 ItemsDocument542 pagesLEI Bulk - 1000 ItemsVyacheslavNo ratings yet

- Manipulation of Financial Statements V0.1Document17 pagesManipulation of Financial Statements V0.1Aniket RaneNo ratings yet

- SIP PROJECT - Praveen AgarwalDocument90 pagesSIP PROJECT - Praveen AgarwalRohit SachdevaNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document6 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)ABDUL HALIM BIN A WAHAB MoeNo ratings yet

- Modern Advanced Accounting in Canada Canadian 8th Edition Hilton Test BankDocument36 pagesModern Advanced Accounting in Canada Canadian 8th Edition Hilton Test Bankviviankellerbv5yy8No ratings yet

- Recognizing and Measuring Government GrantsDocument12 pagesRecognizing and Measuring Government GrantsGraciasNo ratings yet

- Managing Working Capital and Cash FlowDocument8 pagesManaging Working Capital and Cash FlowEnelrejLeisykGarillos100% (1)

- Muhammad Syahrin Bin Zulkefly 2019848422 BA242 5B FIN657 Sir Mohd Husnin Bin Mat YusofDocument3 pagesMuhammad Syahrin Bin Zulkefly 2019848422 BA242 5B FIN657 Sir Mohd Husnin Bin Mat YusofsyahrinNo ratings yet

- LLOYD'S - Final ORSA Guidance Sep11Document17 pagesLLOYD'S - Final ORSA Guidance Sep11Valerio ScaccoNo ratings yet

- Cash Flow Statement New For YoutubeDocument48 pagesCash Flow Statement New For YoutubeTapan BarikNo ratings yet

- Bcoc 136Document2 pagesBcoc 136Suraj JaiswalNo ratings yet

- Contract of Lease With Option To PurchaseDocument3 pagesContract of Lease With Option To PurchaseNeilJuan JuanNo ratings yet

- Kbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Document10 pagesKbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Hamed Al-RiyamiNo ratings yet

- Mchapter Two Accounting Cycle For Service Giving Business Nature of An AccountDocument12 pagesMchapter Two Accounting Cycle For Service Giving Business Nature of An AccountTIZITAW MASRESHANo ratings yet

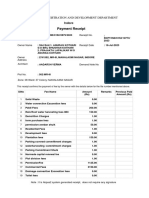

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaNo ratings yet

- Gover Rnment of Andhra PradeshDocument15 pagesGover Rnment of Andhra PradeshChoppa RamachandraiahNo ratings yet

- Land Bank ResoDocument1 pageLand Bank ResoErman GaraldaNo ratings yet

- Case Solution - A New Financial Policy at Swedish Match - ANIDocument20 pagesCase Solution - A New Financial Policy at Swedish Match - ANIAnisha Goyal33% (3)

- Chap 016Document8 pagesChap 016Bobby MarionNo ratings yet

- Answers To Problem Sets: How Much Should A Corporation Borrow?Document8 pagesAnswers To Problem Sets: How Much Should A Corporation Borrow?priyanka GayathriNo ratings yet

- 50 Kpis Cheat Sheet by Nicolas BoucherDocument1 page50 Kpis Cheat Sheet by Nicolas Boucherniah100% (1)

- DNB Bank in Lithuania overviewDocument9 pagesDNB Bank in Lithuania overviewDonata BrukmanaitėNo ratings yet

- Inclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionDocument48 pagesInclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionShashank YadavNo ratings yet

- Benjamin 2007 (Part)Document58 pagesBenjamin 2007 (Part)marcelluxNo ratings yet

- Ghana Stock Exchange CourseDocument7 pagesGhana Stock Exchange CoursePrinceNo ratings yet

- Digitalization of Securities MarketDocument8 pagesDigitalization of Securities Marketmrinal kumarNo ratings yet

- Reconcile Nostro Februari 2023Document56 pagesReconcile Nostro Februari 2023Riko RudyantoNo ratings yet

- Mathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Document52 pagesMathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Sadia Afrin ArinNo ratings yet