You might also like

- ENT RESOURCEFUL MOCK Paper 2Document4 pagesENT RESOURCEFUL MOCK Paper 2Ayen Geoffrey AlexanderNo ratings yet

- Ent Prac 1Document2 pagesEnt Prac 1lubaajamesNo ratings yet

- s.5 Ent Paper 2 Midterm 2Document4 pagess.5 Ent Paper 2 Midterm 2King KetNo ratings yet

- S.6 Ent 2Document5 pagesS.6 Ent 2danielzashleybobNo ratings yet

- Business Budgets and Budgetary Control: Sma - AbsDocument4 pagesBusiness Budgets and Budgetary Control: Sma - AbsSai SumanNo ratings yet

- Ereta Education Cons P2Document2 pagesEreta Education Cons P2Ayen Geoffrey AlexanderNo ratings yet

- Uneeso Ent P2Document4 pagesUneeso Ent P2Otai Ezra100% (1)

- Uneb Uace Entrepreneurship Education 2018Document5 pagesUneb Uace Entrepreneurship Education 2018Barasa marvin33% (3)

- MACP.L II Question April 2019Document5 pagesMACP.L II Question April 2019Taslima AktarNo ratings yet

- UNNASE Ent PP2 S.6Document5 pagesUNNASE Ent PP2 S.6joshbigrank54No ratings yet

- Budget Practice QuestionsDocument8 pagesBudget Practice Questionsmohammad bilalNo ratings yet

- Introduction To SFAD (Class1)Document17 pagesIntroduction To SFAD (Class1)Asmer KhanNo ratings yet

- Ent 2 UaceDocument4 pagesEnt 2 UacedanielzashleybobNo ratings yet

- Question Compilation - 230316 - 072454Document9 pagesQuestion Compilation - 230316 - 072454Ranjan DhakalNo ratings yet

- EN E M A: DT R Examin TionDocument2 pagesEN E M A: DT R Examin TionLokesh GurseyNo ratings yet

- VII. Instructions: Startup Expenses & CapitalizationDocument8 pagesVII. Instructions: Startup Expenses & CapitalizationPriyanshi Agrawal 1820149No ratings yet

- Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20)Document4 pagesAnswer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20) Answer ALL The Questions (10 2 20)Harish KapoorNo ratings yet

- KL Business Finance May Jun 2017Document2 pagesKL Business Finance May Jun 2017Tanvir PrantoNo ratings yet

- 2.3 Paper 2.3 - Accounting For Business - 1Document6 pages2.3 Paper 2.3 - Accounting For Business - 1Himanshu SinghNo ratings yet

- Case Study of Hola KolaDocument5 pagesCase Study of Hola KolaRuohui ChenNo ratings yet

- AFM - IMM 110 (II) April 20, 2021Document3 pagesAFM - IMM 110 (II) April 20, 2021Aashish RanjanNo ratings yet

- HI5017 Progressive Tutorial Question Assignment T2 2020 PDFDocument8 pagesHI5017 Progressive Tutorial Question Assignment T2 2020 PDFIkramNo ratings yet

- Question BankDocument8 pagesQuestion Bankitzzmuskan4No ratings yet

- 15-Mca-Nr-Accounting and Financial ManagementDocument4 pages15-Mca-Nr-Accounting and Financial ManagementSRINIVASA RAO GANTA0% (2)

- IPE 481 - Term Final Question - January 2020Document6 pagesIPE 481 - Term Final Question - January 2020Shaumik RahmanNo ratings yet

- Assignment For Kohat University Ralated With Asif JevedDocument8 pagesAssignment For Kohat University Ralated With Asif JevedAfaq IffiNo ratings yet

- Business Budget - Assignment ProblemsDocument3 pagesBusiness Budget - Assignment ProblemsSHARATH JNo ratings yet

- Accounting For Managers-Assignment MaterialsDocument4 pagesAccounting For Managers-Assignment MaterialsYehualashet TeklemariamNo ratings yet

- Working Capital NumericalsDocument3 pagesWorking Capital NumericalsShriya SajeevNo ratings yet

- Cash BudgetDocument6 pagesCash BudgetSalahuddin ShahNo ratings yet

- ACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVDocument6 pagesACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVmy VinayNo ratings yet

- M 2012 June PDFDocument21 pagesM 2012 June PDFMoses LukNo ratings yet

- Budget Questions Hac1Document5 pagesBudget Questions Hac1odedeyi aishat0% (1)

- 8567Document9 pages8567SyedNo ratings yet

- 185f8question BankDocument18 pages185f8question Bank55amonNo ratings yet

- Ma 2Document3 pagesMa 2123 123No ratings yet

- Cash ManagementDocument16 pagesCash ManagementdhruvNo ratings yet

- Cash BudgetDocument4 pagesCash BudgetSANDEEP SINGH0% (1)

- Financial AccountingDocument4 pagesFinancial AccountingMaithili SUBRAMANIANNo ratings yet

- HI5017 Tutorial Question Assignment T2 2020Document10 pagesHI5017 Tutorial Question Assignment T2 2020shikha khanejaNo ratings yet

- Management Accounting 9mrQc9m4HBDocument3 pagesManagement Accounting 9mrQc9m4HBMadhuram SharmaNo ratings yet

- UntitledDocument6 pagesUntitledAlok TiwariNo ratings yet

- Months: Sales Purchases Wages ExpensesDocument2 pagesMonths: Sales Purchases Wages Expensespranay639No ratings yet

- AE24 Lesson 5Document9 pagesAE24 Lesson 5Majoy BantocNo ratings yet

- FFM Updated AnswersDocument79 pagesFFM Updated AnswersSrikrishnan SNo ratings yet

- Mba 1 Sem Management Accounting 4519201 S 2019 Summer 2019 PDFDocument4 pagesMba 1 Sem Management Accounting 4519201 S 2019 Summer 2019 PDFDeepakNo ratings yet

- Perunthalaivar Kamarajar Arts College Department of Commerce Practice Set - 1 Management Accounting - IiDocument4 pagesPerunthalaivar Kamarajar Arts College Department of Commerce Practice Set - 1 Management Accounting - IiAlbert JulieNo ratings yet

- BudgetingDocument130 pagesBudgetingRevathi AnandNo ratings yet

- Management Accounting (Acct 321) P2 PT 2ND Trimester 2017Document5 pagesManagement Accounting (Acct 321) P2 PT 2ND Trimester 2017Nodeh Deh SpartaNo ratings yet

- Mozammil 029Document4 pagesMozammil 029Iqbal Shan LifestyleNo ratings yet

- Extracts From The Company's Business Plan Are Shown BelowDocument4 pagesExtracts From The Company's Business Plan Are Shown BelowNancy NyamimaNo ratings yet

- MBA-I Sem - II Subject: Financial Management (202) : Assignment Submission: 5 Nov 2016Document3 pagesMBA-I Sem - II Subject: Financial Management (202) : Assignment Submission: 5 Nov 2016ISLAMICLECTURESNo ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Exam2505 2012Document8 pagesExam2505 2012Gemeda GirmaNo ratings yet

- Lecture 11Document26 pagesLecture 11Riaz Baloch Notezai100% (1)

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Mefa Question BankDocument6 pagesMefa Question BankShaik ZubayrNo ratings yet

- tổng hợp đề KTQT 2Document60 pagestổng hợp đề KTQT 2NHI HUYNH MANNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Slaters RuleDocument2 pagesSlaters RulelubaajamesNo ratings yet

- S3 Bio E.O.TDocument1 pageS3 Bio E.O.TlubaajamesNo ratings yet

- 273 1 NLSCL Sample 24Document8 pages273 1 NLSCL Sample 24lubaajamesNo ratings yet

- 241 1 NLSC Sample 24Document4 pages241 1 NLSC Sample 24lubaajames100% (1)

- 208 1 NLSC Sample 24 GuideDocument6 pages208 1 NLSC Sample 24 GuidelubaajamesNo ratings yet

- Chapter 2 Part 3 - Ratio AnalysisDocument13 pagesChapter 2 Part 3 - Ratio AnalysisMohamed HosnyNo ratings yet

- TAX AssignmentDocument8 pagesTAX AssignmentJaydeep KumarNo ratings yet

- CHAP 4 Multiple ChoiceDocument103 pagesCHAP 4 Multiple Choicelilgrace301No ratings yet

- Tutorial Set 3Document2 pagesTutorial Set 36kjmf82979No ratings yet

- Specific DeductionsDocument4 pagesSpecific DeductionswertyNo ratings yet

- Income Tax Important Questions 4Document4 pagesIncome Tax Important Questions 4Chembula JahnaviNo ratings yet

- Chap14 eDocument17 pagesChap14 eMichael Brian TorresNo ratings yet

- The EBITDA Vs Cash Flow Cheat Sheet - Oana Labes, MBA, CPADocument1 pageThe EBITDA Vs Cash Flow Cheat Sheet - Oana Labes, MBA, CPATadeu Andrade100% (1)

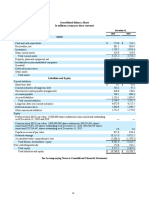

- Standalone Balance Sheet: As at 31 March, 2021 (All Amounts in Crores, Unless Otherwise Stated)Document4 pagesStandalone Balance Sheet: As at 31 March, 2021 (All Amounts in Crores, Unless Otherwise Stated)gitanjali srivastavNo ratings yet

- TAX Syllabus - May 2023 LECPADocument3 pagesTAX Syllabus - May 2023 LECPAkunyangNo ratings yet

- Budget PreparationDocument33 pagesBudget PreparationLizbethHazelRiveraNo ratings yet

- Business Math Q2 Week 3Document9 pagesBusiness Math Q2 Week 3john100% (1)

- Unit 3 Exam Review - Chapters 7-9Document6 pagesUnit 3 Exam Review - Chapters 7-9Vhia Rashelle GalzoteNo ratings yet

- AE 24 Module 1 BudgetingDocument14 pagesAE 24 Module 1 BudgetingShamae Duma-anNo ratings yet

- The Concept of Ibn Khaldun On Taxation SystemDocument17 pagesThe Concept of Ibn Khaldun On Taxation SystemRuffy KingNo ratings yet

- V3 Smart Technologies (Phil) IncDocument11 pagesV3 Smart Technologies (Phil) IncLuz BarnuevoNo ratings yet

- HUF Tax Benefits - How To Generate Income in HUF - EY - IndiaDocument2 pagesHUF Tax Benefits - How To Generate Income in HUF - EY - IndiaPhani SankaraNo ratings yet

- Assignment IMB2020024 IMB2020036Document8 pagesAssignment IMB2020024 IMB2020036Nirbhay Kumar MishraNo ratings yet

- 2020 Annual Report 43Document1 page2020 Annual Report 43Wilson BastidasNo ratings yet

- Allauddin KhiljiDocument6 pagesAllauddin KhiljiRuth Sneha INo ratings yet

- CA 51014 - Strategic Cost Management Capital BudgetingDocument9 pagesCA 51014 - Strategic Cost Management Capital BudgetingMark FloresNo ratings yet

- What Are Tax-Free Bonds and How They Work: by Sunil DhawanDocument2 pagesWhat Are Tax-Free Bonds and How They Work: by Sunil DhawanajitNo ratings yet

- Financial Accounting F3 25 August RetakeDocument12 pagesFinancial Accounting F3 25 August RetakeMohammed HamzaNo ratings yet

- Day 2 Chap 12 Rev. FI5 Ex PRDocument9 pagesDay 2 Chap 12 Rev. FI5 Ex PRCollin EdwardNo ratings yet

- Income Taxation 01 Chapter 1 SummaryDocument8 pagesIncome Taxation 01 Chapter 1 SummarySha LeenNo ratings yet

- Financial Accounting 2 SummaryDocument10 pagesFinancial Accounting 2 SummaryChoong Xin WeiNo ratings yet

- Finman Financial Ratio AnalysisDocument26 pagesFinman Financial Ratio AnalysisJoyce Anne SobremonteNo ratings yet

- Statement of Comprehensive Income (SOCI) and Statement of Financial Position (SOFP)Document37 pagesStatement of Comprehensive Income (SOCI) and Statement of Financial Position (SOFP)Iris NguNo ratings yet

- QUIZ 1 Principles of TaxationDocument6 pagesQUIZ 1 Principles of TaxationHector Quillo Ladua Jr.No ratings yet

- Edpm Module 1 Part LLDocument21 pagesEdpm Module 1 Part LLVishnu100% (1)