You might also like

- Power Plant Module 1 For FINALS PDFDocument8 pagesPower Plant Module 1 For FINALS PDFRex Sotelo BaltazarNo ratings yet

- Chapter ThreeDocument50 pagesChapter ThreeHalu FikaduNo ratings yet

- Economics of Power Generation: by A. Prof. Dr. Wael M.El-MaghlanyDocument13 pagesEconomics of Power Generation: by A. Prof. Dr. Wael M.El-MaghlanyahmedaboshadyNo ratings yet

- Cost of Power GenerationDocument12 pagesCost of Power GenerationPrasenjit GhoshNo ratings yet

- Economies of Power Generation Notes - Lecture IIDocument10 pagesEconomies of Power Generation Notes - Lecture IIkinyanjuimeru27No ratings yet

- Economics of Power GenerationDocument23 pagesEconomics of Power GenerationAbdullah NawabNo ratings yet

- Unit 5Document43 pagesUnit 5Kama RajNo ratings yet

- 8.power Plant EconomicsDocument28 pages8.power Plant EconomicsRAVI KIRAN CHALLAGUNDLA100% (1)

- Economics & PF Correction - 820985Document45 pagesEconomics & PF Correction - 820985paulNo ratings yet

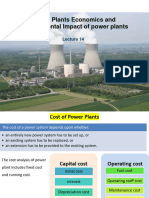

- Lec - 14 PP - Economics and Environmental Impact of PPsDocument42 pagesLec - 14 PP - Economics and Environmental Impact of PPsLog XNo ratings yet

- Chapter 4 Economics of Power GenerationDocument25 pagesChapter 4 Economics of Power GenerationkatlegoNo ratings yet

- X. Economics of Power PlantDocument11 pagesX. Economics of Power Plantreynaldgurion09No ratings yet

- PPE Lecture3Document25 pagesPPE Lecture3Alvin IsmailNo ratings yet

- Economics of Power Supply - PGTDocument3 pagesEconomics of Power Supply - PGTlawrence momanyiNo ratings yet

- Power Plant Engineering 5Document20 pagesPower Plant Engineering 5Anushree Ghosh100% (1)

- CH 1Document5 pagesCH 1imtisangyuNo ratings yet

- Group Members: Waseem Ahmad 11-EE-70 Nadeel Hussain 11-EE-94Document17 pagesGroup Members: Waseem Ahmad 11-EE-70 Nadeel Hussain 11-EE-94Waseem AhmadNo ratings yet

- Economic Comparision of Different Power SystemsDocument6 pagesEconomic Comparision of Different Power SystemsPahan AbeyrathneNo ratings yet

- PPE - Lecture3Document37 pagesPPE - Lecture317027 A. F. M. Al MukitNo ratings yet

- Unit 5Document87 pagesUnit 5er_sujithkumar13No ratings yet

- ITU Elk 421e Generation of Electrical EnergyDocument9 pagesITU Elk 421e Generation of Electrical EnergyBarış OrtaçNo ratings yet

- Open Electricity Economics - 3. The Cost of Electricity PDFDocument13 pagesOpen Electricity Economics - 3. The Cost of Electricity PDFfaheemshelotNo ratings yet

- Cost of Elec Energy - EEE-4903Document8 pagesCost of Elec Energy - EEE-4903Prio DurjoyNo ratings yet

- 7 TariffDocument22 pages7 TariffParvathy SureshNo ratings yet

- 5-Unit IV - Economic Generation and UtilizationDocument50 pages5-Unit IV - Economic Generation and UtilizationVeera Vamsi YejjuNo ratings yet

- Power System Economics NotesDocument83 pagesPower System Economics Notesdinesh100% (1)

- TARIFF DESIGN For GENERATING STATIONSDocument16 pagesTARIFF DESIGN For GENERATING STATIONSNaveen Chodagiri100% (1)

- IE SeminarDocument18 pagesIE SeminarRik PtlNo ratings yet

- Module 5Document7 pagesModule 5Renuka KutteNo ratings yet

- Installed Capital CostDocument11 pagesInstalled Capital CostHannah TusborgNo ratings yet

- Chapter 1 - Economics of Power GenerationDocument18 pagesChapter 1 - Economics of Power GenerationBF3nobel100% (1)

- Tariff PDFDocument3 pagesTariff PDFsushant7136No ratings yet

- Ppe Unit-VDocument42 pagesPpe Unit-VSiriganti RakeshNo ratings yet

- Life Cycle Cost CalculationDocument8 pagesLife Cycle Cost CalculationJames Bryle VillarealNo ratings yet

- Document From Jitendra Nath RaiDocument27 pagesDocument From Jitendra Nath RaiVinit SinghNo ratings yet

- Topic 9Document18 pagesTopic 9SUREINTHARAAN A/L NATHAN / UPMNo ratings yet

- Test Bank For Engineering Economy 16Th Edition by Sullivan Wicks Koelling Isbn 0133439275 9780133439274 Full Chapter PDFDocument25 pagesTest Bank For Engineering Economy 16Th Edition by Sullivan Wicks Koelling Isbn 0133439275 9780133439274 Full Chapter PDFmindy.sorrell339100% (14)

- Test Bank For Engineering Economy 16th Edition by Sullivan Wicks Koelling ISBN 0133439275 9780133439274Document35 pagesTest Bank For Engineering Economy 16th Edition by Sullivan Wicks Koelling ISBN 0133439275 9780133439274AshleyParksegn100% (23)

- Engineering CostDocument12 pagesEngineering CostH110Shreyan SarkarNo ratings yet

- Power Distribution and UtilizationDocument22 pagesPower Distribution and UtilizationRasmiaIrfanNo ratings yet

- Or R20 Unit 3Document44 pagesOr R20 Unit 3gunas4767No ratings yet

- AMC Lecture 2Document40 pagesAMC Lecture 2James HowellNo ratings yet

- Introduction To Quiz - Economics of Wind Energy - Coursera - L PDFDocument5 pagesIntroduction To Quiz - Economics of Wind Energy - Coursera - L PDFNikoNo ratings yet

- Introduction To Quiz: Economics of Wind EnergyDocument5 pagesIntroduction To Quiz: Economics of Wind EnergyNiko100% (1)

- 2 Economics of Power GenerationDocument23 pages2 Economics of Power GenerationAshwin kumarNo ratings yet

- PSOC PPT For All UnitsDocument73 pagesPSOC PPT For All Unitsswamy koduriNo ratings yet

- Economics & Marketing of Photovoltaic Systems: Learning OutcomesDocument13 pagesEconomics & Marketing of Photovoltaic Systems: Learning OutcomesMehmet KayaNo ratings yet

- U-5 Ppe NotesDocument15 pagesU-5 Ppe NotesSaikiran AitipamulaNo ratings yet

- Unit VDocument29 pagesUnit Vprathamwakde681No ratings yet

- Engineering Economy 16th Edition Sullivan Test BankDocument36 pagesEngineering Economy 16th Edition Sullivan Test Bankfoxysolon8cfh5100% (20)

- Dwnload Full Engineering Economy 16th Edition Sullivan Test Bank PDFDocument36 pagesDwnload Full Engineering Economy 16th Edition Sullivan Test Bank PDFserenafinnodx100% (12)

- CE Lecture# 03Document22 pagesCE Lecture# 03ATTA100% (1)

- Cost Analysis: Mr. P. Nandakumar Assistant Professor KvimisDocument27 pagesCost Analysis: Mr. P. Nandakumar Assistant Professor KvimisNanda KumarNo ratings yet

- Module 7: Replacement Analysis (Chap 9)Document35 pagesModule 7: Replacement Analysis (Chap 9)우마이라UmairahNo ratings yet

- Emc EseDocument251 pagesEmc EseAbhiNo ratings yet

- 4 Year Mechanical Power: Dr. Mohamed Hammam 2020Document14 pages4 Year Mechanical Power: Dr. Mohamed Hammam 2020Mohamed HammamNo ratings yet

- Engineering Economy 16th Edition Sullivan Test BankDocument5 pagesEngineering Economy 16th Edition Sullivan Test BankDanielThomasxjfoq100% (15)

- EE2004 5 TariffsDocument25 pagesEE2004 5 Tariffsanimation.yeungsinwaiNo ratings yet

- Desirable Characteristics of A Tariff: When There Is A Fixed Rate Per Unit of Energy ConsumedDocument4 pagesDesirable Characteristics of A Tariff: When There Is A Fixed Rate Per Unit of Energy ConsumedNishit KumarNo ratings yet

- Power (Work Done) / (Time Taken) : 2.6.5 Power From Hydro-SchemeDocument10 pagesPower (Work Done) / (Time Taken) : 2.6.5 Power From Hydro-SchemepanNo ratings yet

- TariffDocument4 pagesTariffpanNo ratings yet

- Lec 1..economics of Power GenerationDocument7 pagesLec 1..economics of Power GenerationpanNo ratings yet

- CodeDocument1 pageCodepanNo ratings yet

- COG July August 2012Document110 pagesCOG July August 2012confyNo ratings yet

- Wind Turbine Foundation Base Ring Under ErectionDocument63 pagesWind Turbine Foundation Base Ring Under Erectioncherinet SNo ratings yet

- Smart Grid Survey 2011 Research PaperDocument38 pagesSmart Grid Survey 2011 Research Paperdheerajdb99No ratings yet

- Williams 2024 WMB Analyst Day PresentationDocument176 pagesWilliams 2024 WMB Analyst Day PresentationrubenpeNo ratings yet

- RRREC - Solar Tariff PetitionDocument195 pagesRRREC - Solar Tariff PetitionMohammadSoaeb MominNo ratings yet

- Epira Law 2001Document35 pagesEpira Law 2001euroaccessNo ratings yet

- Staff Report On Electricity Markets and ReliabilityDocument187 pagesStaff Report On Electricity Markets and ReliabilityStephen LoiaconiNo ratings yet

- Energy Storage - The Basics - Scottish RenewablesDocument16 pagesEnergy Storage - The Basics - Scottish RenewablesMatt MaceNo ratings yet

- Memo PDFDocument1 pageMemo PDFJohn Keyster Bambao AlonzoNo ratings yet

- US Annual Energy Review 2008Document446 pagesUS Annual Energy Review 2008Spandan ChakrabartiNo ratings yet

- INVT IMars B Series Grid-Tied Solar Inverter User Manual (International)Document62 pagesINVT IMars B Series Grid-Tied Solar Inverter User Manual (International)Jose Tomas Carpio MilanoNo ratings yet

- MT95047FUDocument9 pagesMT95047FUAbburi KarthikNo ratings yet

- Physics Module Form 5 Chapter 3 - Electromagnet GCKL 2011: What Is An Electromagnet ? What Is A Magnetic Field?Document35 pagesPhysics Module Form 5 Chapter 3 - Electromagnet GCKL 2011: What Is An Electromagnet ? What Is A Magnetic Field?Muaz HaikalNo ratings yet

- Progress Test 8: GrammarDocument3 pagesProgress Test 8: Grammarka yra?No ratings yet

- Hypow 12 ScreenDocument28 pagesHypow 12 ScreenDragan TrajkovicNo ratings yet

- Windblatt 0310 EnglDocument16 pagesWindblatt 0310 EnglMeggy VillanuevaNo ratings yet

- Coal, Nuclear, Oil, Natural Gas Power Plant Case Study - SolutionDocument7 pagesCoal, Nuclear, Oil, Natural Gas Power Plant Case Study - SolutionKshitishNo ratings yet

- Green Finance and Its Impact On Sungrow Renewable Energy Bangladesh LimitedDocument72 pagesGreen Finance and Its Impact On Sungrow Renewable Energy Bangladesh LimitedKRZ. Arpon Root HackerNo ratings yet

- EE 442 642 IntroductionDocument14 pagesEE 442 642 IntroductionUSERNAME12340987No ratings yet

- Micro TurbineDocument22 pagesMicro Turbineravikiranzz12345100% (1)

- Bhutan Energy Efficiency Baseline Study Final Report 26 12 12-1Document96 pagesBhutan Energy Efficiency Baseline Study Final Report 26 12 12-1OnetwothreefourfunkNo ratings yet

- Shakya Rabin Thesis 2018Document43 pagesShakya Rabin Thesis 2018Rakesh ShinganeNo ratings yet

- The Low Carbon Menu: WhitepaperDocument34 pagesThe Low Carbon Menu: Whitepaperamitjain310No ratings yet

- Design and Construction of 2kilowatts Power Inverter For Farm House UseDocument73 pagesDesign and Construction of 2kilowatts Power Inverter For Farm House UseOlalusi Oluwaseyi Gabriel100% (3)

- 300 - CHP - EPA (Final) W-AppsDocument244 pages300 - CHP - EPA (Final) W-AppsmgkalfasNo ratings yet

- Power Plant EquipmentDocument54 pagesPower Plant EquipmentJoy PalitNo ratings yet

- Product Catalogue: Ro LiDocument147 pagesProduct Catalogue: Ro Li방성광No ratings yet

- SteamTurbine Brochure MidDocument20 pagesSteamTurbine Brochure MidSubrata Das100% (1)

- Introduction To Electrical Principles: Unit 202: Electrical Principles and Processes For Building Services EngineeringDocument68 pagesIntroduction To Electrical Principles: Unit 202: Electrical Principles and Processes For Building Services EngineeringSofea IzyanNo ratings yet

- Project SynopsisDocument4 pagesProject SynopsisShreya DGNo ratings yet