Professional Documents

Culture Documents

Profitability Evaluation of Intelligent Transport System Investment

Profitability Evaluation of Intelligent Transport System Investment

Uploaded by

СлаваCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Profitability Evaluation of Intelligent Transport System Investment

Profitability Evaluation of Intelligent Transport System Investment

Uploaded by

СлаваCopyright:

Available Formats

Profitability Evaluation of Intelligent Transport System

Investments

Pekka Leviäkangas1 and Jukka Lähesmaa2

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

Abstract: The objective of this study was to consider evaluation methods for intelligent transport system 共ITS兲 investments, to point out

some shortcomings of traditional methods 共mainly benefit-cost analysis兲, to develop alternative methods, and to make recommendations

for how the profitability of ITS investment should be evaluated. The results can be used when ITS investments are compared with each

other and also when ITS investments are compared with road building investments. This work identifies the fundamental differences

between ITS and road infrastructure investments and how they impact on the profitability evaluation. The conclusion is that traditional

cost-benefit analysis 共BCA兲, which was developed for investments in physical infrastructure, does not capture all the benefits or costs

related to ITS. Economic evaluation methods for ITS investments need improving. This work illustrates how BCA could be used to take

into consideration the option value of ITS investment and risks caused by, for example, different time horizons of investments. The work

also discusses and demonstrates the use of multicriteria analysis in profitability evaluation. It illustrates how a method called analytical

hierarchy process could be utilized to evaluate other risks that do not have specific monetary values and to compare the results of different

profitability analyses. These evaluation methods can be used within the project assessment framework in the transport sector to highlight

different aspects of the profitability and efficiency of transport investments. None of the methods themselves can reflect all aspects in

decision making, but by using a suitable set of different methods depending on the decision situation and by comparing the results, a wider

and more realistic picture of investments can be obtained.

DOI: 10.1061/共ASCE兲0733-947X共2002兲128:3共276兲

CE Database keywords: Intelligent transportation systems; Profits; Investments; Benefit cost ratios.

Introduction ing better access to more advanced technology and applications,

users are increasingly accustomed to different types of services

Future of Intelligent Transport Systems provided by new communications technology. Consumer accep-

tance is therefore more readily achieved than a decade ago. In

Transport authorities and infrastructure managers are investing summary, the market for ITS is growing rapidly, and there seems

increasingly in intelligent transport systems 共ITS兲, also often re- to be both a supply push and a demand pull for this growth. As an

ferred to as advanced transport telematics 共ATT兲. This is a result example, Fig. 1 shows how the U.S. Department of Transporta-

of several overlapping and correlated trends. First, the new tech- tion 共USDOT兲 and ITS America predict the ITS market to de-

nology has matured to the point where it begins to expand in- velop.

creasingly to other fields of society, such as transport and infra- While investments in ITS are growing, by comparison those in

structure, apart from military and consumer goods. Second, with conventional physical infrastructure seem to be falling 共as well as

the markets becoming more saturated, the real prices of new tech- compared to traffic demand兲. This is especially the case in the

nology have plummeted. Mobile wireless communication is one industrialized world where the ageing infrastructure badly needs

of the key technologies applied to ITS, and, for example, there rehabilitation. For instance, the Finnish Ministry of Transport and

was a 85% drop in the wholesale market price of mobile phones Communications 共Ministry 1998, p. 21兲 has estimated that the

within 10 years 共Finnish Electronics Wholesalers Association upgrading and rehabilitation of the substructures of road networks

1999兲. Third, because of market saturation, with more people hav- can only be done every 100 years if road budgets are kept at their

present levels. This is too long an interval for the infrastructure to

maintain its service level. The Ministry does not see any possi-

1

Senior Research Scientist, VTT Building and Transport 共Technical

Research Center of Finland兲, P.O. Box 18021, FIN-90571 Oulu, Finland. bilities for radical increases in infrastructure budgets in the fore-

E-mail: pekka.leviakangas@vtt.fi seeable future. At the same time, capacity enhancement is seen as

2

Management Consultant, SysOpen IT Business Consulting, a conflicting goal to sustainable mobility 共and requiring too much

Valimopolku 4, FIN-00380 Helsinki, Finland. E-mail: capital that is needed elsewhere兲. Therefore, ITS provides a natu-

jukka.lahesmaa@sysopen.fi ral solution for utilizing the existing infrastructure capacity more

Note. Discussion open until October 1, 2002. Separate discussions efficiently and in an environmentally acceptable manner.

must be submitted for individual papers. To extend the closing date by Fig. 2 shows that ITS is slowly increasing its share of invest-

one month, a written request must be filed with the ASCE Managing

ments, although the figures are still very modest 共8.40 million

Editor. The manuscript for this paper was submitted for review and pos-

sible publication on August 21, 2000; approved on September 25, 2001. euros estimated for 1999兲. Upgrading and replacement invest-

This paper is part of the Journal of Transportation Engineering, Vol. ments seem to be outweighing capital investments, currently 218

128, No. 3, May 1, 2002. ©ASCE, ISSN 0733-947X/2002/3- million euros, and capital investments have fallen to 134 million

276 –286/$8.00⫹$.50 per page. euros. Hence, ITS combined with other upgrading measures is

276 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

1. BCA is just one tool among many, although it has gained

wide acceptance as the de facto standard evaluation method;

thus, it provides just one view of the profitability of the

investment in question.

2. BCA has been applied for so long and in such a uniform

manner for infrastructure investment evaluation that its im-

provement has been neglected; in other words, it has been

more or less stagnant for several decades, at least for those

who apply it in practice.

It should be emphasized, however, that BCA is probably still

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

the best available tool for socio-economic profitability evaluation,

as other methods are virtually nonexistent. Therefore, the authors

Fig. 1. Government, commercial and consumer ITS U.S. market wish not to be overly critical toward BCA but rather to provide

growth up to 2015 共Hardison and Mudge 1997兲 some alternative aspects for profitability evaluation and economic

analysis of ITS investments, especially where ITS and traditional

investments are seen as excluding alternatives.

expected in the future to solve many of the existing capacity and Objectives and Structure of this Work

safety problems faced by the Finnish National Roads Administra-

tion 共Finnra兲. In other words, ITS is increasingly replacing tradi- The objectives of this study are as follows:

tional investments, at least to some extent. By the year 2010, ITS • The first objective is to provide a deeper insight into the prof-

investments and maintenance will probably play a key role in itability and economic evaluation of ITS investments in the

Finnra’s expense budget if current trends continue. particular situation where it must be contrasted with traditional

engineering measures.

• Second, to present some potential alternative tools for project

Problems with Current Profitability Evaluation Methods profitability evaluation, with a view to enabling traffic profes-

Economic evaluation methods have not evolved apace with new sionals to view the project from another angle in addition to

approaches to developing and improving infrastructure. The need traditional BCA. It must be emphasized that ready-made, in-

for alternative evaluation methods was recognized in the report stantly applicable tools are not presented but rather some

Development Needs of Project Assessment in the Transport Sec- methods which can be applied in various ways to support prac-

tor 共Niskanen et al. 1998兲. The report proposed the use of multi- tical decision making.

criteria analysis and verbal descriptions to supplement benefit- • Finally, the objective is to contribute to future and ongoing

cost analysis 共BCA兲 within the project assessment framework in research concerning the profitability and economic evaluation

the transport sector. This principle was also included in the guide- of road and other infrastructure and ITS investments.

lines for the evaluation of ITS projects 共Kulmala et al. 1998兲. Case examples will be presented from the road sector, where

However, these guidelines do not include recommendations on the authors feel there is great potential for ITS, which to date has

which methods should be used to perform alternative analysis, drawn the mainstream of transport telematics profitability re-

although the need to develop such guidelines and methods was search in Finland. However, other traffic modes must not be for-

emphasized 共Kulmala et al. 1998兲. gotten, as analyses of profitability are most often at the project

At the moment, road investments are still, by and large, evalu- level and deal with a single mode only. The case examples are

ated on the basis of traditional BCA. Given that the alternative also from Finland, and any conclusions drawn from them must be

methods are few, this is understandable. However, traditional viewed cautiously if applied to other countries with different cir-

BCA does not capture the entire essence of ITS investments. cumstances.

There are two main reasons for this. This work summarizes some of the relevant findings of a study

initiated by the Finnish Ministry of Transport and Communica-

tions and carried out by the authors 共Leviäkangas and Lähesmaa

1999兲 as part of a larger transport telematics research and devel-

opment program 共Kulmala 1998兲. That report is downloadable

from the Internet from www.vtt.fi/rte/projects/tetra 共click the

Finnish pages’ project no. 5, and go to the end of the proceeding

page兲.

Fundamental Differences between Intelligent

Transport System Investments and Conventional

Investments in Physical Infrastructure

Introductory Remarks

Bristow et al. 共1997兲 argued that because ITS is now an actual aid

for improving transportation networks, ITS project appraisal

needs to be developed to the same level as the appraisal of con-

Fig. 2. Finnra’s investment expenses for public roads. Expense fig-

ventional transport infrastructure investments. However, based on

ures for 1998 and 1999 are budget estimates.

their review of ITS evaluation procedures, they argued that ap-

JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002 / 277

J. Transp. Eng. 2002.128:276-286.

needed for the benefits to recover the costs. The higher the time

value of money, that is, the discounting rate, the more difficult

this task becomes. For telematics investments, the time value is

not that important because the time span is shorter, also in a

technical sense. What is critical for them is whether the benefits

will exceed the costs in the medium run 共5–10 years兲. Conse-

quently, when comparing investment alternatives with traditional

BCA, telematics investments need proportionally higher benefits

compared with investment cost in order to compete in the profit-

ability contest. The differences between the investments are fur-

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

ther characterized in Table 1.

Impact of Differences on Investment Risk

In regard to comparisons between traditional road infrastructure

investments and ITS investments, Leviäkangas 共1998兲 argued that

many other aspects exist to investment evaluation besides tradi-

tional BCA. For example, in a case where the road authority is

Fig. 3. Fictitious cash flows of physical infrastructure 共panel A兲 and

considering whether to build a new road link or to upgrade the

ITS 共panel B兲 investments

existing piece of infrastructure, the value of the real option in the

latter alternative is neglected in the comparison process. In this

propriate methods for ITS have not yet been established. It seems case, the real option comes with the fact that by upgrading the

necessary to develop evaluation guidelines specifically for ITS existing road 共by traditional engineering solutions, ITS, or both兲

projects because existing appraisal techniques may not be appro- the road authority reserves a valuable option to build the new link

priate for dealing with the specific features of ITS applications. later if traffic demand so indicates in the future. Investing heavily

The USDOT has acknowledged that the financing of ITS is in the present situation could be a mistake, provided there is un-

different from conventional infrastructure for at least three rea- certainty related to the socioeconomic profitability of the invest-

sons 共Haynes et al. 1995兲 ment. This uncertainty could be due to the difficulties of obtaining

1. Conventional infrastructure finance aims mainly to support reliable traffic forecasts. Another shortcoming of BCA pointed out

the government led provision of basic amenities to the pub- by Leviäkangas 共1998兲 is that BCA does not recognize risk-return

lic. ITS financing aims to improve the present performance trade-off, which is one of the cornerstone principles of modern

of transportation infrastructure with greater participation by investment theory. According to this principle, the higher the risks

the private sector. of the project, the higher should be the required return on it.

2. One of the main drivers in the ITS concept is the ability to Despite this fact, most transport authorities worldwide apply fixed

reduce adverse environmental effects, such as air pollution, discounting rates when ranking projects.

which were externalized in conventional transportation sys- Leviäkangas 共1998兲 continues his arguments by identifying

tems. different risk profiles for traditional infrastructure investments

3. Conventional infrastructure finance is based on known tech- and ITS/upgrading investments. The first effecting factor is the

nologies; whereas, ITS financing is oriented to performance different sheer volume of ITS and traditional infrastructure invest-

improvements by the implementation of new technologies. ment. Clearly, an investment of hundreds of millions carries an

The cash flow profile for ITS and traditional investments is entirely different risk loading than an investment of some mil-

radically different. The cash flows of fictitious ITS and physical lions, especially from the viewpoint of the investor, which in this

infrastructure investments are illustrated in Fig. 3. 共Here the term case is the road authority representing ultimately the taxpayer.

‘‘cash flow’’ means the flow of benefits and costs that are usually Secondly, the length of time for capital investments impacts on

expressed in monetary terms. From society’s point of view, these risk is the time during which an investment is expected to pay for

are not pure cash flows.兲 What is obvious from cash flow profiles itself and possibly be upgraded or salvaged. Again, it should be

is the heavy front-end loading of costs and back-end loading of obvious that tying down the capital for, say, 30 years is riskier

benefits in traditional investments. This makes the time value of than doing so for 10 years. Consequently, if risk adjustment of

money an extremely important factor, because a long time span is discounting rates is also seen to be appropriate for these types of

Table 1. Differences between Intelligent Transport System 共ITS兲 and Physical Infrastructure Investments

Physical infrastructure

Costs ITS investment investment

Investment cost Relatively small 共e.g., 2– 4 million euros兲 Usually high 共e.g., 100–200 million euros兲

Life time Short/Medium 共e.g., 5–10 years兲 Long 共e.g., 30–50 years兲

Salvage value after full depreciation Usually no value Significant value 共e.g., 20% of investment cost兲

Operating costs of the system Significant to total costs No operating costs 共or at least these costs

are insignificant兲

Effect on other costs of the road Sometimes indirect effects, for example on the Usually direct effects, for example, on repair and

authority efficiency of winter maintenance maintenance costs

User costs Accident and time costs often cancel each other out Usually all user costs decrease

278 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

Table 2. Investment Behavioral Patterns with Different Approaches and Preferences for Risk.

Investment behavior in different investment alternatives

Risk⇒impact Traditional Intelligent Transport System

Sunken cost⇒unrecoverable investment Risk-taker, low preference in liquidity and Risk-averse, high preference in liquidity and

opportunity cost of capital opportunity cost of capital

Technological⇒unrealized benefits, operating Risk-averse, conservative Risk-taker, pioneer

costs, operating errors

Strategic/forecasting error⇒unrealized Risk-taker, deterministic, low preference for Risk-averse, preference in flexibility, high

benefits time value of money time value preference

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

Environmental risk⇒higher sunken cost, Risk-taker, low image preference Risk-averse, high image preference

bad image, time delays

Uncertainty of impacts on drivers and Risk-averse, conservative Risk-taker, pioneer, experimenting

environment⇒unrealized benefits

User acceptance⇒consumer dissatisfaction Risk-averse, conservative, demand-driven, Risk-taker, pioneer, proactively market driven

market adaptive

investments, the two arguments shift the required return to a The Evaluation Process for Road Transport Telematics study

higher level for traditional investments and to a lower one for 共EVA study兲 produced a manual for an evaluation process for road

ITS. transport informatics, but the manual could also be used more

One should also look at the risks related to ITS investments broadly to evaluate different kinds of ITS applications. EVA pro-

共implicitly, the risks of traditional upgrading measures are consid- vided guidelines for the benefit-cost evaluation process, proposed

ered here as insignificant兲 what criteria 共costs and benefits兲 should be included in the BCA,

• ITS solutions are still in their infancy and have not undergone and gave recommendations on the valuation of criteria 共Bobinger

the same degree of technological evolution as other engineer- et al. 1991兲. Later, the CORD project gave specific guidelines on

ing solutions 共i.e., conventional measures for infrastructure, the evaluation of different ITS application areas, like urban traffic

tested and improved upon for decades兲. They therefore carry a management and information or in-vehicle information systems

certain risk related to their reliability and the impacts they 共Zhang and Kompfner 1993兲. The CORD guidelines gave recom-

have on traffic. ITS can fail and malfunction or may not have mendations on the evaluation process of ITS impacts in general,

the desired impacts to generate the expected benefits. Few re-

but did not give guidelines for carrying out BCA.

search results are yet available on the actual effects of ITS

Two levels of analysis can be identified in the use of BCA. The

solutions.

first concerns systems or subsystems, such as road weather infor-

• Many ITS solutions may still not be fully accepted by motor-

mation systems within a country or region. The second has to do

ists. Thus, ITS carries a consumer-acceptance risk, which in

turn entails the risk of not achieving the desired impacts. with specific projects, such as building a weather-controlled speed

It would seem, however, that the risks of ITS are diminishing limit system on a stretch of road.

with time. On average, today’s computers, mobile phones and The majority of known international ITS BCA concerns the

other high-tech applications are more reliable than ever before. utilization of different ITS applications as a whole, not with spe-

Some of the improvement is due to organizational, and some are cific investment objects. Lind 共1996兲 has estimated what might be

due to technological learning and evolution. When these discus- the possible effects and benefit-cost ratios of certain ITS sub-

sion and arguments are reflected in investment behavior, different systems in the Gothenburg region based on two different sce-

behavioral patterns can be identified, as shown in Table 2. narios for the year 2020. In the United Kingdom, a BCA of ITS

applications from eight application areas was performed during a

review of the potential benefits of road transport telematics

Benefit-Cost Analysis for Intelligent Transport projects 共Perrett and Stevens 1996兲. Relatively similar BCAs have

System also been performed in Canada 共Zavergiu 1996兲 and Australia

共Booz Allen Hamilton 1998兲. Armstrong et al. 共1993兲 investigated

Introduction and evaluated the conclusions and methodologies of selected ITS

benefit-cost studies in the United States.

Benefit-cost analysis is a widely used method for measuring the

profitability of different kinds of investments in the transport sec-

tor. Since the 1970s, Finnra has provided instructions on how to Finnish Experience

make road transport sector investment calculations and what val-

ues to use for user costs. Later, other transport modes in Finland In Finland, BCAs have been performed only for individual

adopted Finnra’s methods, in which the user costs are time, ve- telematics systems. The socio-economic profitability of the E18

hicle, accident, exhaust fumes, and noise costs. Usually in the weather-controlled motorway between the cities of Kotka and

case of road building investments, all these user costs will fall and Hamina was estimated before the system was built 共Lähesmaa

benefit society. The total benefits are then compared with invest- 1995兲. Subsequently, once the actual effects of the system on

ment costs, and a conclusion is drawn as to whether the invest- traffic had been studied, the benefit-cost calculations were re-

ment is profitable. Typically, time savings are the most important peated 共Lähesmaa 1997兲. The benefit-cost ratios of nine case ITS

factors dictating profitability. investments were estimated in a study of the best telematics ap-

JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002 / 279

J. Transp. Eng. 2002.128:276-286.

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

Fig. 4. Analytical hierarchy process comparing telematics solutions 共Lähesmaa et al. 1998兲

plications when these were set in rural areas in southeastern Fin- to all of them is their ability to deal with two or more criteria

land 共Lähesmaa et al. 1998兲. The main concern of the applica- measured in different units. Three main reasons for the use

tions was to improve traffic safety. of multicriteria analysis to evaluate ITS investments are as

The results from these studies showed that the benefit-cost follows:

ratio of rural area ITS investments is likely to remain relatively

1. Many of the benefits of ITS investment do not have mon-

low. More specifically, the benefit-cost ratio of the E18 motorway

etary value 共e.g., service to drivers, comfort兲.

was approximately 0.5, and the benefit-cost ratio of all nine case

2. The shortcomings of traditional BCA can be avoided, so that

investments was less than 1, which means that the applications

are not profitable. In some cases the benefit-cost ratio was even the results of the comparison process reflect the preferences

found to be negative. of decision makers.

The benefit-cost ratios were poor because of the significance 3. Criteria, such as a substantial difference in required capital

of time and vehicle costs in the socioeconomic calculation meth- outlays between ITS and road building investments and risks

ods used by Finnra. With the use of telematics applications, travel related to the investments, can be considered in the compari-

times would have increased on average by 1–2 s at intersections son.

and by no more than 1 min on road sections. These small changes The EVA manual includes guidelines for using multicriteria

often increased time and vehicle costs more than they reduced analysis in the ITS project evaluation. EVA deals with several

accident costs. In sensitivity analysis, it was found that invest- MCA techniques and gives recommendations on how to build

ments would become profitable only if speeds were increased by MCA comparison and assign priorities to the criteria. However, it

the telematics application, even though this would mean a con- does not recommend any specific MCA method 共Bobinger et al.

siderable rise in the number of accidents. Quite explicitly, the 1993兲.

current Finnish evaluation framework prefers time savings over Lähesmaa et al. 共1998兲 used a multicriteria analysis method

traffic safety. called analytical hierarchy process 共AHP兲 to compare telematics

solutions with each other and with road building investments in

two cases. AHP starts with the building of the hierarchical tree,

Multicriteria Analyses

relating main objectives to subobjectives in several layers of de-

tail. Next, the decision makers assign a degree of importance or

Introduction to Multicriteria Analyses (MCA) weight to the criteria and alternatives in the tree based on the

There exist a number of different evaluation and decision tech- numerical facts or their own opinions and appreciation 共Saaty and

niques that could be regarded as multicriteria analysis. Common Kearns 1985兲.

Table 3. Examples of Analytical Hierarchy Process Comparison

Step Examples of interpretation

共1兲 Pair-wise comparisons of the cases regarding each criterion When sense of security is considered, Case 4 is more preferable

than Case 14.

共2兲 Creation of the ranking order based on each criteria by When operational risks are considered, the weights of the cases

combining the pair-wise comparisons of the five experts are the following: Case 2, 0.054; Case 4, 0.16; Case 5, 0.15;

Case 6, 0.08; Case 8, 0.06; Case 13, 0.41; Case 14, 0.07. So,

Case 13 is most preferred and seems to carry the smallest risk.

共3兲 Pair-wise comparisons of the criterion ‘‘Risks’’ is slightly less important criterion than ‘‘service to the

road user.’’

共4兲 Creation of the weights for each criteria by combining the The weights for the criteria are following: Service to the road

pair-wise comparisons of the five experts user, 0.33; financial parameters, 0.12; importance of the site,

0.38; risks, 0.16. So, importance of the site was considered the

most important criterion.

共5兲 Creation of the final ranking order by combining the The final ranking order of the cases as shown in Fig. 6

individual ranking orders

280 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

Fig. 5. Relative ranking order of cases based on financial parameters 共benefit-cost ratio of case 13 is equal to 1.兲

Comparison of Intelligent Transport System was less important than where traffic problems are more critical.

Investments Consequently, the AHP hierarchy 共i.e., the preferences of decision

makers兲 puts the most emphasis on the absolute efficiency of

The AHP hierarchy shown in Fig. 4 was designed to compare

investments rather than the relative ratio between benefits and

telematics solutions 共Lähesmaa et al. 1998兲. The comparisons

costs.

were based on financial parameters of investments, the knowledge

of decision makers, and preferences regarding the effects on ser-

vice provided to road users, on risk incurred by investments, and Comparison of Intelligent Transport System and Road

on the importance of different road sections and intersections. Building Investments

Six promising cases of different types of transport telematics

solutions were compared in the AHP process. For the criterion, The AHP method was also used to compare telematics and road

financial parameters, the ranking was based on the cost-benefit building investments. One case was an intersection area near the

ratios and return on investment 共ROI兲 of each case. Rankings by city of Lappeenranta 共Finnra 1996兲. The main direction is along a

other criteria were based on experience and opinion. Five deci- two-line highway, which has two intersections close to each other

sion makers from Finnra’s southeastern region were interviewed, with high traffic volume. Weekdays have typical morning and

and the results were used in the AHP hierarchy to assign priorities evening peak hours, with cars commuting to and from work. In

to the alternatives and criteria. Table 3 presents an example of summer, there is tidal traffic on Friday and Sunday evenings.

how the steps in the AHP comparison were taken as well as how However, hourly traffic is relatively low the rest of the time 共Lä-

the values were assigned to the hierarchy. hesmaa et al. 1998兲.

Fig. 5 shows the order of cases based on financial parameters, In the telematic solution, variable speed limits and information

and Fig. 6 shows the ranking order based on the AHP process. In boards would be used to lower speeds in the main direction dur-

Fig. 6, the white bars show the standard deviation; the smaller its ing peak hours. This would ease access to the highway at inter-

value the more consistent are the opinions of the decision makers. sections and increase overall capacity. Traffic safety would also

These figures show a substantial difference in the ranking improve slightly. However, no significant improvement was ex-

order. For example, if the decision was based solely on BCA, pected in accident rates as most accidents do not occur during

Case 4, variable speed limits at the Käyrälampi intersection peak hours. The investment cost of this telematic solution was

would receive top priority. The investment is inexpensive and estimated at around 0.50 million euros. An alternative solution

would increase traffic safety relatively well without interfering was to build a new graded interchange at the location, at a cost of

with traffic too much during construction. However, in the AHP some 15.10 million euros. If the decision were based on BCA, a

process, Case 4 was the last one to be selected, because there is new interchange would be built. This would decrease travel time

far less traffic at this intersection than in other case locations, and and increase safety, and the benefit-cost ratio of the investment

traffic problems are not that severe. For these reasons, the deci- would be about 1.5 共Finnra 1996兲. The telematic solution would

sion makers felt that this solution would serve road users less than increase travel time in the main direction during periods when

other case solutions and that spending money on this intersection speed limits are lowered because of high traffic volumes. Even if

Fig. 6. Relative ranking order of cases based on analytical hierarchy process

JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002 / 281

J. Transp. Eng. 2002.128:276-286.

this increase of travel time were on average only 1 to 2 s per teria are selected to avoid double counting, some of this will

vehicle and the solution had positive effects on access to the occur because decision makers subconsciously connect vari-

highway and on traffic safety, the value of time costs would be so ous facts anyway.

significant that the benefit-cost ratio of the telematics application • A comparison with AHP is always on a case-by-case basis.

would be less than 1 共Lähesmaa et al. 1998兲. The results cannot be compared with other investments. New

The AHP hierarchy in Fig. 7 was used to compare the building comparisons have to be made if new alternatives are to appear.

of the interchange and telematics investments. In this case, the Therefore, the authors suggest that MCA alone should not be

BCA was done totally using the AHP method. This made it pos- used to make final decisions but only as an aid in structuring the

sible to assign the priorities of decision makers to the evaluation process. Furthermore, MCA provides an opportunity to take into

process concerning how the benefits of different impacts are seen account many important factors affecting the decision that have

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

and how the substantial difference in investment costs is valued in no explicit monetary or other numerical value. On the other hand,

the comparison. there is always the question of utility the investor pursues. It is the

The same decision makers from Finnra’s southeastern region definition of utility that very much dictates the tools that are avail-

compared interchange and telematics investments based on each able for use. If the utility is defined as net present value of dis-

criterion on the AHP hierarchy. Next, they also assigned degrees counted benefits, then the traditional BCA is a good tool 共BCA

of importance to the criteria. This comparison showed that maximizes the net present value of benefits under constrained

telematics investment was seen as modestly more preferable to budget兲. When we have benefits which cannot be valued and thus

the interchange investment. Compared with traditional BCA there discounted to the present, we simply must adopt different meth-

were two major differences. With the AHP method, the disadvan- ods and tools. Here is where MCA can provide some help.

tages of the telematics solution regarding travel time in the main

direction were not considered as important compared to the ad-

vantages, as they were in BCA. On the other hand, savings in Analyses based on Financial Theory

investment costs of the telematics solution were felt to be more

important than mere numerical differences, principally because

Risk-Adjusted Discounting Rates

many similar problem locations in the area also need urgent im-

provements. If telematics were chosen, some funds could be used Arrow and Lind 共1994兲 discuss the risk and uncertainty in public

to improve other locations. Channeling lots of money into this investment decisions and conclude that risk adjustment of dis-

one intersection would create serious funding difficulties for other counting rates is appropriate if the uncertain costs and benefits

targets of development. 共i.e., the risks兲 of the particular investments are borne by private

individuals 共or a specified group of people or organizations兲. On

the other hand, if the public body representing the investor is able

Opinions on use of Multicriteria Analyses

to distribute the risks evenly across the population, risk adjust-

A modified AHP method was used earlier in Detroit to create ment lacks justification. Thus the question is by no means simple.

preference weights for transportation planning goals of the FAST- Arrow and Lind 共1994兲 used an irrigation project as an example,

TRAC operational field test. On the basis of that study, Levine where the farms’ income is dependent to some extent on the suc-

and Underwood 共1996兲 argued that in an environment such as that cessfulness of the project. In a case like this, risk adjustment

of ITS, in which policy goals are diverse and potentially conflict- should be done. In road projects, which are also limited geo-

ing, MCA methods can aid in policy and system design by gaug- graphically 共only the areas and people within the vicinity of the

ing the relative preferences of strongly interested individuals and road are affected significantly兲 as well as user-wise 共only the mo-

groups. torists using the road are affected significantly兲, the benefits are

In the Finnish studies, the authors found remarkable differ- directed to a specific group. Hence, there is some argument for

ences in decisions based solely on BCA or MCA. The main dis- risk adjustment. But, as stated by Stiglitz there are no simple,

advantages of using the AHP method in these cases were the definite answers to the question of the right discounting rate.

following: ‘‘The value of the social rate of discount depends on a number of

• The AHP method is subjective, and the set of criteria selected factors, and indeed I have argued it may vary from project to

for the hierarchy cannot be wholly complete. Even if the cri- project depending, for instance, on the distributional conse-

Fig. 7. AHP hierarchy comparing telematics and road building investments 共Lähesmaa et al. 1998兲

282 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

quences of the project. These results may be frustrating for those E(R̃ GDP)⫽the expected, uncertain growth of national income,

who seek simple answers, but such are not to be found.’’ 共Stiglitz GDP; and  s ⫽the 共social兲 risk of the project compared to the

1994, p. 155兲. national income growth.

Arrow and Lind 共1994, p. 161兲 also point out that the time and This simplified model implies that the project is worth carry-

risk preferences relevant for government action could simply be ing out provided that when using its risk adjusted discounting rate

established as matter of national policy. The rate of discount and R p , the calculus produces a positive net present value. In other

attitude toward risk could be specified by the appropriate authori- words, when doing the actual project appraisal, the social dis-

ties, and the procedures for evaluation would incorporate these counting rate may be adjusted according to Eq. 共3兲 and then be

time and risk preferences. This approach relieves the authorities used as normal in the cost-benefit calculus.

from too much theoretical consideration, which in the end only Some points here need further discussion. Although the social

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

blurs the decision-making rules. return on a project is conceptually clear 共i.e., the net present value

Taking the risk into account by adjusting discounting rates is of discounted costs and benefits兲, the minimum allowed social

one policy. Another policy is to include the risk premiums within return is not. In CAPM, the reference minimum rate was obtained

the valuation formula, that is, calculate the certainty equivalent from state bonds, or similar, which can be considered as risk-free

value of each risk separately and use fixed discounting rates. investments. For public investments, this reference rate is not

These two policies are in fact identical according to investment available, at least not directly. One solution is to use the decided

theory. Little and Mirrlees 共1994兲 showed how the Capital Asset discounting rate, which in Finland for transport infrastructure in-

Pricing Model 共CAPM兲 can be applied to public investments and vestments has been 6% 共annual basis兲. Thus, it is a matter of

their risk valuation. Instead of calculating asset betas 共兲 indicat- agreement, as proposed by Arrow and Lind 共1994兲. The fact that

ing the asset’s risk in relation to overall market risk, they derived annual GDP growth might be less than 6% poses no problem. The

a kind of project risk measure for public projects, indicating the important issue here is that the project should contribute to eco-

project’s social profits in relation to national income. Their anal- nomic growth and welfare. However, if  is large and R GDP is

ogy with CAPM is straightforward. lower than R s , this could even lead to a negative discounting rate,

The original CAPM assumes the form 共Copeland and Weston at least in theory. 共The rates discussed here are in nominal terms.

1988, p. 204兲 If nominal rates are used, then also the cost and benefit compo-

nents must be in nominal terms, as they are in standard cost-

E 共 R̃ 兲 ⫽R f ⫹ 关 E 共 R̃ m 兲 ⫺R f 兴  (1)

benefit calculus.兲

where  is Another problem is the time risk or risk of forecasting error.

CAPM and the related models usually assume historical betas,

cov共 R̃,R̃ m 兲 that is, the risks are measured as ex post. Then, the risks are

⫽ (2)

m2 applied as such ex ante. This is one of the major risks in long-

term, strategic investments: the longer the time horizon, the

where E(R̃)⫽expected uncertain return on project, investment or greater the risk of forecasting error.

asset; the tilde 共⬃兲 denotes the uncertainty of the parameter; R f Using Finnish historical data, Leviäkangas and Lähesmaa

⫽risk-free return, for example, return on state bonds; E(R̃ m ) 共1999, appendix A兲 calculated the time risk adjusted discounting

⫽expected, uncertain return on market portfolio, that is, a diver- rates for ITS investments. The results implied that the discounting

sified investment in the stock market; and ⫽risk measure of the rates for ITS investments should be 1 to 2% units lower for ITS

project, asset, or investment against the market portfolio invest- than that used normally for infrastructure investments. This

ment, that is, the covariance between project return and market means that ITS investments become ‘‘more easily’’ profitable than

return divided by the variance of market return. conventional investments.

If ⬎1, the project is riskier than the market portfolio invest-

ment, and the required return on it should be more than R m . If Case of Real Options

⬍1, the required return, that is, the discounting rate, should be

less than R m . In any case, the return should not be lower than the The first presentation of the options theory was made by Black

risk-free rate R f . The risk is measured simply by how volatile the and Scholes 共1973兲 in their classic article. Typically, an option is

asset is in relation to the market. This model, used routinely in regarded as a right to sell or buy a security 共or any other asset兲 for

capital markets, shows how the risk adjustment of discounting a predetermined price. The owner of the option also has the free-

rates may be done. dom not to exercise his or her right to buy or sell, depending on

Little and Mirrlees 共1994兲 simply replaced the market return the market situation. A practical guide to the options approach is

with national income growth. Thus, they measured what is the given by Dixit and Pindyck 共1995兲. They provide numerous el-

risk of a project in relation to overall economic development, that ementary examples of situations where the options approach is

is, national income, which often is operationalized as gross do- applicable. Ingersoll and Ross 共1992兲 showed that even the sim-

mestic product 共GDP兲. Although their theoretical approach was plest of projects has an option value, that is, it competes with

more refined than shown below, the idea remains essentially the itself postponed. Thus all projects are subject to the postponement

same. The CAPM modification may now be written as alternative, which creates a real option with a calculable value.

Brennan and Schwartz 共1993兲 showed how the options approach

cov共 R̃ p ,R̃ GDP兲 may be applied to the natural resource investment valuation prob-

E 共 R̃ p 兲 ⫽R s ⫹ 关 E 共 R̃ GDP兲 ⫺R s 兴

GDP

2 lem. They took the case of a mine and treated it as an option.

Trigeorgis 共1993兲 identifies the value of options in a situation

⫽R s ⫹ 关 E 共 R̃ GDP兲 ⫺R s 兴  s (3) where there exist numerous real options, and furthermore, where

these options interact with each other. Trigeorgis 共1993兲 also

where E(R̃ p )⫽the expected, uncertain social return on the shows that the value of flexibility manifests familiar option prop-

project; R s ⫽the minimum allowed social return on the projects; erties.

JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002 / 283

J. Transp. Eng. 2002.128:276-286.

Table 4. Summary of Results when Applying Option Theory 共Leviäkangas and Lähesmaa 1999, p. 28兲

Investment cost Benefit cost ratio Black-Scholes Benefit cost ratio

Type of investment 共millions of euros兲 without option benefit option value with option value

ITS 共VMS, VSL兲 0.50 0.67 3.1 6.87

共10-year period兲 million euros

Capital 共2-level intersection兲 15.13 1.00 — —

共20-year period兲

Sercu and Uppal 共1994兲 applied the options approach in an

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

cost 共15.13 million euros兲; X⫽exercise price of the option; in this

international capital budgeting case. They showed in their article case, the investment cost of building the intersection later, that is,

that irreversible international capital investments include real op- 21.85 million euros, assuming that it will be more expensive to

tions that affect the investment decision at hand. The traditional carry out the work later; ⫽standard deviation of the returns of

net present value 共NPV兲 rule ignores these options. In their par- the underlying asset; in this case, the standard deviation of the

ticular case, the NPV method underestimated the true value of social return on the project 共0.1兲; T⫽the time to maturity of the

investment. It therefore seems obvious that the option theory can option; in this case, the 10-year period gained by investing in ITS;

be applied to almost any investment decision, regardless of the R f ⫽risk-free interest rate; that is, the minimum required social

nature of the investment. Kemna puts it as follows: ‘‘The value of rate of return 共6%兲; N(d)⫽cumulative probability for a normally

flexibility associated with investment projects can be derived distributed unit variable z at point d; and e⫽Neper’s number

from the value of real options, because options are the perfect tool ⫽2.718282.

to value the impact of future decisions on uncertain cash flows. Secondly, in order to confirm results of option calculus, the

For example, these real options can be found in several stages of authors also used the state preference model to determine how

investment projects, like the option to postpone an investment, to well-off the investor 共i.e., the road authority兲 would be when

maintain the scale and life of the project, to shut-down tempo- choosing different investment strategies. The probabilities used in

rarily or to abandon the project.’’ 共Kemma 1987兲 this model were taken from real historical data on Finnish road

It must be emphasized that option values are in reality not traffic volumes for 1981–1997 共Leviäkangas and Lähesmaa 1999,

direct benefits for the investor, but rather possibilities to adopt a appendix B兲. The results of this verifying method confirmed that

flexible investment behavior. Often the option value is referred to there truly exists an option value for the ITS alternative, which is

as the value of flexibility. substantial with regard to ITS investment.

Here, a real world case project is used to demonstrate how the The results are summarized in Table 4. As observed, the option

option theory may be applied to road ITS investments. Our option values are significant compared with the cost of ITS investment.

calculation is elementary and lacks theoretical sophistication. Fur- The Black-Scholes option valuation method yielded to an option

thermore, it should be regarded as an experimental demonstration value of 3.1 million euros 共the state preference approach showed

because the application of option theory in this field surely needs a value of 1.3 million euros; also Monte Carlo simulation may be

more research. However, it shows the idea, which hopefully can used to study option values兲. These figures are of paramount sig-

be refined by other researchers in the future. The calculus and nificance when considering an ITS investment of 0.50 million

more detailed information on the case project appear in the work euros. Therefore, if ITS 共or upgrading兲 alternatives are suspected

by Leviäkangas and Lähesmaa 共1999, appendix B兲. It is shown to include any option elements, they can be surprisingly high in

that two different and independent approaches produce positive monetary/benefit terms. Traditional BCA disregards these ben-

option values for ITS investments when compared to traditional efits.

capital investments. The investment alternatives are as follows:

1. A new two-level intersection for two main roads crossing;

this investment alternative serves for 20 years at least. Budgetary Aspects

2. An ITS investment of variable message signs 共VMS兲 and The traditional engineering measures of capacity expansion and

variable speed limit 共VSL兲 signs; the signs warn of a dan- safety improvement are heavy and expensive. ITS should be re-

gerous crossing and alert drivers that other vehicles may be garded more as a strategy than an operational measure to avoid

approaching the crossing area; the speed limits change ac-

heavy construction operations in new traffic infrastructure. Taking

cording to the traffic flow density so that vehicles can

ITS and telematics as a strategic approach on the aggregate level,

smoothly join the main direction flow, and the risk of cross-

it is possible to ease the financial burden of governmental bud-

ing accidents is reduced. This alternative serves for 10 years,

gets. If only a portion of larger scale investments can be post-

and should then be renewed or replaced by the first invest-

poned or even avoided by implementing telematics systems, a

ment alternative.

significant fiscal impact on the budget is achieved.

Two alternative option valuation methods are used. The first,

The following example reflects the situation in one of the re-

the Black-Scholes model, takes the form

gional units of Finnra 共Finnra 1998兲. The purpose is to illustrate

c⫽SN 共 d 1 兲 ⫺Xe ⫺R f T N 共 d 2 兲 how ITS can be used as an optional investment strategy, not to

diminish the importance of traditional engineering measures,

where

which are of course always needed 共Leviäkangas and Lähesmaa

ln共 S/X 兲 ⫹R f T 1 1999, p. 28 –30兲.

d 1⫽ ⫹ 冑T, d 2 ⫽d 1 ⫺ 冑T The total investment plan for 1997–2005 yielded to 284.1 mil-

冑T 2

lion euros, of which 256.9 million euros were for new projects to

where c⫽value of the option; S⫽current price of the underlying be initiated. It was assumed by the authors that out of the 11

asset; in this case, the two-level intersection building investment investment projects there were two projects that could be replaced

284 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

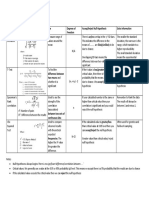

Table 5. Risks and Prospective Tools for Risk Accounting

Prospective tool for risk

Risk⇒impact accounting

Sunken cost⇒ Option theory

unrecoverable investment

Technological⇒unrealized benefits, Multicriteria analysis

operating costs, operating errors

Strategic/forecasting error⇒ Option theory and risk-adjusted

unrealized benefits discounting rate

Fig. 8. Alternative investment programs for the Finnra’s southeast- Environmental risk⇒higher sunken

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

Multicriteria analysis

ern region cost, bad image, time delays

Uncertainty of impacts on drivers and Multicriteria analysis

eironment⇒unrealized benefits

User acceptance⇒ Multicriteria analysis

entirely by ITS, and the other two could be postponed by 8 years.

consumer dissatisfaction

After these adjustments, the total investment plan yielded to 126.8

million euros and new projects to 99.6 million euros, which is

roughly 60% less for the investment plan period compared to the

vice, and driver comfort. However, even these can be evaluated in

original plan. However, it is important to realize that investment

monetary terms provided that adequate research is carried out.

pressures will increase in the future if ITS investments prove

We have presented some tools that deal fully or partly with the

inadequate in the long-run. The difference between the example

above problems resulting from the different nature of invest-

investment programs in one of Finnra’s regions is shown in Fig.

ments. From the risk management point of view, Table 2 can be

8. The original program shows darker 共back area兲, and the ITS

reviewed, and different tools may be adopted for risk accounting

emphasizing program shows pale 共front area兲 共Leviäkangas and

共see Table 5兲.

Lähesmaa 1999, p. 30兲.

Option theory and risk adjustment of discounting rates are

prospective methods for some risks while others have to be dealt

with using other tools, namely multicriteria analysis 共or similar

Conclusion

evaluation tools兲. Multicriteria analysis, of course, allows the in-

clusion of several alternative tools for aggregate level evaluation,

On the basis of theoretical discussion and evidence from case

each tool contributing to certain risk management aspects.

analyses, it is possible to make the following statements on alter-

These evaluation methods can be used within the project as-

native methods of comparing the profitability of ITS and physical

sessment framework in the transport sector to highlight different

infrastructure investments.

aspects of the profitability and efficiency of transport investments.

None of the methods themselves can reflect all the aspects in

First Statement. ITS and infrastructure investments differ in so

decision making, but by using a suitable set of different methods

many respects that the traditional BCA developed for the latter

depending on the decision situation and by comparing the results,

type of investments is an insufficient tool for producing sound

a wider and more realistic picture of investments can be obtained.

decision-making rules for investment selection.

However, these tools need to be developed further so that they

can be applied in standard practice and in management systems.

Second Statement. Multicriteria analysis produces different in-

vestment selection rules than BCA adopted in a straightforward

manner. Furthermore, MCA captures better the decision-makers’

and experts’ preferences and goal settings, although these items Notation

cannot be measured with a single yardstick.

The following symbols are used in this paper:

Third Statement. Some of the differences are manageable by ad- c ⫽ value of option;

justing the benefit-cost calculus. For example, the different time E( ) ⫽ expectation operator;

risk profiles of ITS and infrastucture investments can be taken e ⫽ Neper’s number⫽2.718282;

into account by adjusting discounting rates. N(d) ⫽ cumulative probability for normally distributed

unit variable at point d;

Fourth Statement. Some of the ITS investment benefits can be R ⫽ interest rate, return or discounting rate;

captured by using option valuation techniques. The items valued S ⫽ current price of underlying asset;

by option tools can be regarded as ‘‘financial flexibility ’’ or T ⫽ time to maturity of option;

‘‘postponing uncertain, risky and heavy investments 共until we are X ⫽ exercise price of option;

sure we really need them兲.’’ It is most interesting that this option  ⫽ risk of project compared to systematic risk;

was implicitly recognized by Finnish road authorities when they ⫽ standard deviation; and

favored ITS alternatives when using multicriteria analysis 共AHP ⬃ ⫽ uncertainty operator.

in that particular case兲 despite the fact that traditional BCA Subscript

strongly favored traditional engineering solutions. f ⫽ identifier for risk-free;

GDP ⫽ identifier for gross domestic product, i.e., national

Fifth Statement. Many aspects nevertheless remain without clear income;

valuation rules where ITS investments are concerned. For ex- m ⫽ identifier for market; and

ample, one can list items such as budget impacts, improved ser- s ⫽ identifier for social or socioeconomic.

JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002 / 285

J. Transp. Eng. 2002.128:276-286.

Acknowledgments Leviäkangas, P. 共1998兲. ‘‘Some new aspects and ideas for economic

evaluation of ITS investments.’’ Proc., 5th World Congress on Intel-

The writers wish to thank the anonymous reviewers of the paper ligent Transport Systems, Seoul, South Korea.

for useful comments. The Ministry of Transport and Communica- Leviäkangas, P., and Lähesmaa, J. 共1999兲. ‘‘Profitability comparison be-

tions Finland and Dr. Harri Kallberg provided us the opportunity tween I.T.S. investments and traditional investments in infrastruc-

ture.’’ Ministry of Transport and Communication Finland, Rep. and

to carry out this research. The writers thank both for this oppor-

Memoranda B 24/99, Ministry of Transport and Communications,

tunity. The ideas, conclusions, and recommendations of this paper Helsinki, Finland.

represent only those of the writers. Levine, J., and Underwood, S. E. 共1996兲. ‘‘A multiattribute analysis of

goals for intelligent transportation system planning.’’ Transp. Res.,

Part C: Emerg. Technol., 4共2兲, 97–111.

Downloaded from ascelibrary.org by KMUTT KING MONGKUT'S UNIV TECH on 10/18/14. Copyright ASCE. For personal use only; all rights reserved.

References Lind, G. 共1996兲. ‘‘Test-site-oriented scenario assessment. Possible effects

of transport telematics in the Gothenburg region.’’ KFB Rep. 1996:13,

Arrow, K. J., and Lind, R. C. 共1994兲. ‘‘Risk and uncertainty: Uncertainty Kommunikationsforskningsberedningen, Stockholm, Sweden.

and the evaluation of public investment decisions,’’ Cost-Benefit Little, I. M. D., and Mirrlees, J. A. 共1994兲. ‘‘The costs and benefits of

analysis, 2nd Ed., Richard Layard and Stephen Glaister, eds., Cam- analysis: Project appraisal and planning twenty years on,’’ Cost-

bridge Univ. Press, New York, pp. 160–178. benefit analysis, 2nd Ed., R. Layard and S. Glaister, eds., Cambridge

Black, F., and Scholes, M. 共1973兲. ‘‘The pricing of options and corporate Univ. Press, New York, 199–231.

liabilities.’’ Journal of Political Economy, 81, 637– 654. Lähesmaa, J. 共1995兲. ‘‘Sääohjatun tien yhteiskuntataloudellinen edullis-

Bobinger R., et al. 共1991兲. ‘‘Evaluation process for road transport infor- uus.’’ 共Socio-economic profitability of weather controlled road兲. Offi-

matics. EVA-manual.’’ Commission of the European Communities, cial public research report of Kaakkois-Suomen tiepiiri 共Finnra South-

EVA project V1035, Munich, Germany. eastern Region兲, Kouvola, Finland.

Booz Allen Hamilton Ltd 共1998兲. ‘‘Intelligent transport solutions for aus- Lähesmaa, J. 共1997兲. ‘‘Kotka—Hamina Sääohjatun tien yhteiskuntata-

tralia. Technical Rep.’’ Booz Allen Hamilton Ltd, Sydney, Australia. loudellisuus.’’ 共Socio-economic profitability of the Kotka—Hamina

Brennan, M. and Schwartz, E. 共1993兲. ‘‘A new approach to evaluating weather controlled road兲, Finnra Publications 36/1997, Helsinki, Fin-

natural resource investments,’’ The new corporate finance. Where land.

theory meets practice, D. H. Chew, ed., McGraw-Hill, New York, Lähesmaa, J., Schirokoff, A., and Portaankorva, P. 共1998兲. ‘‘Kaakkois-

98 –107. Suomen tiepiirin liikenteen telematiikkaselvitys.’’ 共Transport telemat-

Bristow, A. L., Pearman, A. D., and Shires, J. D. 共1997兲. ‘‘An assessment ics study of Southeastern road region兲, Finnra Rep. 42/1998.

of advanced transport telematics evaluation procedures.’’ Transport Kaakkois-Suomen tiepiiri 共Finnra Southeastern Region兲, Kouvola,

Rev., 17共3兲, 177–205. Finland.

Copeland, T. E., and Weston, J. F. 共1988兲. Financial theory and corporate Niskanen, E., Goebel, A., Pesonen, H., Roine, M. 共1998兲. ‘‘Liikenteen

policy, 3rd Ed., Addison-Wesley, Reading, Mass. hankearvioinnin kehittämistarpeet,’’ 共Development needs of project

Dixit, A. K., and Pindyck, R. S. 共1995兲. ‘‘The options approach to capital assessment in the transport sector兲, Publications of the Ministry of

investment.’’ Harvard Bus. Rev., 3, 105–115. Transport and Communications Finland 38/98, Ministry of Transport

Finnish Electronic Wholesalers Association 共1999兲. ‘‘Public statistics and Communications, Helsinki, Finland.

leaflets.’’ Helsinki, Finland. Perrett, K. E., and Stevens, A. 共1996兲. ‘‘Review of the potential benefits

Finnra 共1996兲. ‘‘Valtatien 6 parantaminen välillä Kärki—Mattila, of road transport telematics.’’ TRL Rep. 220, Transport Research

Lappeenranta. Tiesuunnitelmaselostus.’’ 共Enhancement of highway 6 Laboratory, England.

between Kärki and Mattila, Lappeenranta兲. Official public planning Saaty, T., and Kearns, K. 共1985兲. ‘‘Analytical planning. The organization

document, Kaakkois-Suomen tiepiiri 共Finnra Southeastern Region兲, of systems,’’ Pergamon, Tarrytown, N.Y.

Kouvola, Finland 共in Finnish兲. Sercu, P., and Uppal, R. 共1994兲. ‘‘International capital budgeting using

Finnra 共1998兲. ‘‘Kaakkois-Suomen tiepiirin toiminta-ja taloussuunitelma option pricing theory.’’ Managerial Finance, 20共8兲, 3–21.

1998 –2000.’’ 共Southeastern Region’s Operative and Financial Plan Stiglitz, J. E. 共1994兲. ‘‘Discount rates: The rate of discount for benefit-

for 1998 –2000兲. Official public planning document, Kaakkois- cost analysis and the theory of second best,’’ Cost-Benefit Analysis,

Suomen tiepiiri 共Finnra Southeastern Region兲, Kouvola, Finland 共in 2nd Ed., R. Layard and S. Glaister, eds., Cambridge Univ. Press, New

Finnish兲. York, 116 –159.

Hardison, M. F., and Mudge, R. R. 共1997兲. ‘‘National market analysis.’’ Ministry of Transport and Communications Finland 共1998兲. ‘‘Ministerial

Forecasting the Market Potential of ITS. A Joint EIA/ITS America working group of transport infrastructure.’’ Publications of the Minis-

Forecast Conf. of ITS Opportunities, Arlington, Va. try of Transport and Communications Finland 48/1998, Ministry of

Haynes, K., Arieira, C., Burhans, S., and Pandit, N. 共1995兲. ‘‘Fundamen- Transport and Communications, Helsinki, Finland.

tals of infrastructure financing with respect to ITS.’’ Build. Environ., Trigeorgis, L. 共1993兲. ‘‘The nature of option interactions and the valua-

21共4兲, 246 –254. tion of investments with multiple real options.’’ J. Financ. Quant.

Ingersoll, Jr., J. L., and Ross, S. A. 共1992兲. ‘‘Waiting to invest: Investment Anal., 28共1兲, 1–20.

and uncertainty.’’ J. Business, 65共1兲, 1–29. Zavergiu, R. 共1996兲. ‘‘Intelligent transportation systems—An approach to

Kemna, A. G. Z. 共1987兲. ‘‘Options in real and financial markets.’’ PhD benefit-cost studies.’’ Transport Canada Publication No. TP 12695E,

thesis, Erasmus Univ. of Rotterdam, Rotterdam, The Netherlands. Montréal.

Kulmala, R., et al. 共1998兲. ‘‘Liikennetelematiikkahankkeiden arviointio- Zhang, X., and Kompfner, P. 共1993兲. ‘‘Common guidelines for assess-

hjeet.’’ 共Guidelines for the evaluations of ITS projects兲. Publications ment of ATT pilots.’’ Commission of the European Communities,

of the Ministry of Transport and Communications 59/98, Ministry of CORD project V2056, Deliverable No. AC02—Part 6, ERTICO, Brus-

Transport and Communications, Helsinki, Finland. sels.

286 / JOURNAL OF TRANSPORTATION ENGINEERING / MAY/JUNE 2002

J. Transp. Eng. 2002.128:276-286.

You might also like

- Engineering Management (CH 2: Decision Making)Document2 pagesEngineering Management (CH 2: Decision Making)oddonekun100% (4)

- Impact Evaluation of Transport Interventions: A Review of the EvidenceFrom EverandImpact Evaluation of Transport Interventions: A Review of the EvidenceNo ratings yet

- 2017 - Assessment of E-Governance Projects (Gaps - Constructs)Document10 pages2017 - Assessment of E-Governance Projects (Gaps - Constructs)SheenjeeNo ratings yet

- Deployment of Contextual Mobile Payment System: A Prospective E-Service Based On Ictization Framework From Bangladesh PerspectiveDocument8 pagesDeployment of Contextual Mobile Payment System: A Prospective E-Service Based On Ictization Framework From Bangladesh PerspectiveRakibul Islam 221-14-458No ratings yet

- TD 18-10 Benefits and Costs of Automation For Bus Rapid Transit (BRT) WCAGDocument4 pagesTD 18-10 Benefits and Costs of Automation For Bus Rapid Transit (BRT) WCAGElya MuniraNo ratings yet

- Retraction: Retracted: Construction Project Cost Management and Control System Based On Big DataDocument8 pagesRetraction: Retracted: Construction Project Cost Management and Control System Based On Big DataNabilla Nur ZahwaNo ratings yet

- Stakeholder-Specific Data Acquisition and Urban Freight Policy Evaluation Evidence Implications and New SuggestionsDocument26 pagesStakeholder-Specific Data Acquisition and Urban Freight Policy Evaluation Evidence Implications and New SuggestionsManuel GutierrezNo ratings yet

- Best of Best of ORDocument12 pagesBest of Best of ORkebede desalegnNo ratings yet

- Digital Lending High Level System Architecture in Indonesia: August 2020Document7 pagesDigital Lending High Level System Architecture in Indonesia: August 2020mjNo ratings yet

- Improving Cost Estimates of Construction Projects UsingDocument5 pagesImproving Cost Estimates of Construction Projects UsingFigoNo ratings yet

- Bot Financial Model:taiwan High Speed Rail CaseDocument9 pagesBot Financial Model:taiwan High Speed Rail CasegalihyoedhaNo ratings yet

- Sustainability 12 09539Document14 pagesSustainability 12 09539Mahir MsawilNo ratings yet

- Innovative Mobility Master Plan Connecting Multimodal Systems With Smart TechnologiesDocument2 pagesInnovative Mobility Master Plan Connecting Multimodal Systems With Smart TechnologiesWulanNo ratings yet

- CIE - 2009 - Bahinipati - Horizontal Collaboration in Semiconductor Manufacturing Industry Supply Chain PDFDocument16 pagesCIE - 2009 - Bahinipati - Horizontal Collaboration in Semiconductor Manufacturing Industry Supply Chain PDFaserherNo ratings yet

- Value World - Fall 2009 (Draft 01) .Indd (10-14) PDFDocument5 pagesValue World - Fall 2009 (Draft 01) .Indd (10-14) PDFRegiNo ratings yet

- 1 s2.0 S0160791X22002020 MainDocument17 pages1 s2.0 S0160791X22002020 MainNabil FarhanNo ratings yet

- Application of Costing System in The Small and Medium Sized Enterprises SME in TurkeyDocument9 pagesApplication of Costing System in The Small and Medium Sized Enterprises SME in TurkeySantosh DeshpandeNo ratings yet

- Siemiatycki - 2008 - Managing Optimism Biases in The Delivery of LargeDocument6 pagesSiemiatycki - 2008 - Managing Optimism Biases in The Delivery of LargeSaad KhanNo ratings yet

- Infrastructure Consolidation Strategy WPDocument9 pagesInfrastructure Consolidation Strategy WPuserNameNo ratings yet

- Case Studies On Transport Policy: Giorgio Ambrosino, Brendan Finn, Saverio Gini, Lorenzo MussoneDocument10 pagesCase Studies On Transport Policy: Giorgio Ambrosino, Brendan Finn, Saverio Gini, Lorenzo MussoneRafael Lino dos SantosNo ratings yet

- ESG Maturity A Software Framework For The ChallengDocument18 pagesESG Maturity A Software Framework For The Challengsujaysarkar85No ratings yet

- Complexities of Cost Overrun in Construction ProjectsDocument4 pagesComplexities of Cost Overrun in Construction ProjectsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- GANNDocument6 pagesGANNRobert MaximilianNo ratings yet

- Airlines Remaining Relevant How To Retain Customer LoyaltyDocument57 pagesAirlines Remaining Relevant How To Retain Customer LoyaltyArman GargNo ratings yet

- Value Engineering (Ve) Application in Infrastructure Projects by Public-Private Partnerships (PPPS)Document9 pagesValue Engineering (Ve) Application in Infrastructure Projects by Public-Private Partnerships (PPPS)Guru VelmathiNo ratings yet

- MEGA White Paper - Application Portfolio ManagementDocument28 pagesMEGA White Paper - Application Portfolio ManagementIsmanto Semangoen100% (1)

- VE Case Studies (2023)Document59 pagesVE Case Studies (2023)Benyamin SadiraNo ratings yet

- iON Digital Assessment: Redefining The Future of Assessment ProcessDocument8 pagesiON Digital Assessment: Redefining The Future of Assessment ProcessPET BOTANY 2021No ratings yet

- V10n4a1 PDFDocument14 pagesV10n4a1 PDFkinecamposNo ratings yet

- Applying Benefit-Cost Analysis To Intelligent Transportation Systems (ITS) and The Australian ContextDocument14 pagesApplying Benefit-Cost Analysis To Intelligent Transportation Systems (ITS) and The Australian ContextIbnuFarhanKathinNo ratings yet

- A Survey of Cost Benefit Methodologies For Information SystemsDocument13 pagesA Survey of Cost Benefit Methodologies For Information SystemsAtahar HussainNo ratings yet

- Sciencedirect: Cost Drivers of Integrated Maintenance in High-Value SystemsDocument5 pagesSciencedirect: Cost Drivers of Integrated Maintenance in High-Value SystemsNadilla MursalimNo ratings yet

- Advanced Vehicle Telematics Analysis For Enhanced Safety and EfficiencyDocument8 pagesAdvanced Vehicle Telematics Analysis For Enhanced Safety and EfficiencybhelemukulNo ratings yet

- Research Article: Construction Project Cost Management and Control System Based On Big DataDocument7 pagesResearch Article: Construction Project Cost Management and Control System Based On Big DataMiguel NumanNo ratings yet

- A Construction Cost Estimation Framework Using DNN and Validation UnitDocument12 pagesA Construction Cost Estimation Framework Using DNN and Validation Unittivaga3618No ratings yet

- Intelligent Road Traffic Control System For TraffiDocument9 pagesIntelligent Road Traffic Control System For TraffiSimona NicoletaNo ratings yet

- Risk Analysis and Prediction of The Stock Market Using Machine Learning and NLPDocument6 pagesRisk Analysis and Prediction of The Stock Market Using Machine Learning and NLPAkash GuptaNo ratings yet

- An Artificial Neural Network Approach For Cost EstDocument15 pagesAn Artificial Neural Network Approach For Cost Est1190900011 NANDINI SHARMANo ratings yet

- Final Ysc Final Poster Format 04.01.24Document1 pageFinal Ysc Final Poster Format 04.01.24shreyanshsharma005No ratings yet

- Cha 2005Document13 pagesCha 2005Gian Fahmi PangestuNo ratings yet

- Risk Based Budgeting of Infrastructure ProjectsDocument10 pagesRisk Based Budgeting of Infrastructure ProjectsAshimolowo BabatundeNo ratings yet

- Applied Sciences: Smart Mobility and Aspects of Vehicle-to-Infrastructure: A Data ViewpointDocument18 pagesApplied Sciences: Smart Mobility and Aspects of Vehicle-to-Infrastructure: A Data ViewpointDániel TokodyNo ratings yet

- An Integrated Architecture For Future Car GenerationsDocument12 pagesAn Integrated Architecture For Future Car GenerationsnanytanarchNo ratings yet

- 01 Ieee Conference 2014 WebServiceTestiing Ce198Document9 pages01 Ieee Conference 2014 WebServiceTestiing Ce198Tehmina MehboobNo ratings yet

- Sustainability 16 00433Document20 pagesSustainability 16 00433Rogerio CesarNo ratings yet

- Cost Estimation and Prediction Using Android ApplicationDocument3 pagesCost Estimation and Prediction Using Android ApplicationMayhendra ESNo ratings yet

- Mehta2019Document5 pagesMehta2019Carlos BocanegraNo ratings yet

- EAC para La ConstrucionDocument11 pagesEAC para La ConstrucionPaulo César C SNo ratings yet

- Future Generation Computer Systems: Netsanet Haile Jörn AltmannDocument18 pagesFuture Generation Computer Systems: Netsanet Haile Jörn Altmannmjobs247No ratings yet

- Impact of Digital Payment Adoption On Indian Banking Sector EfficiencyDocument13 pagesImpact of Digital Payment Adoption On Indian Banking Sector EfficiencySuriya viratNo ratings yet

- Artificial Neural Network For Transportation Infrastructure Systems - Koorosh GharehbaghiDocument5 pagesArtificial Neural Network For Transportation Infrastructure Systems - Koorosh GharehbaghiAnonymous l6hBI1kzNo ratings yet

- Life Cycle Cost Analysis - Overview, How It Works, ApplicationsDocument1 pageLife Cycle Cost Analysis - Overview, How It Works, ApplicationsMigle BloomNo ratings yet

- Deterministic and Probabilistic Engineering CostDocument13 pagesDeterministic and Probabilistic Engineering CostEduardo MenaNo ratings yet

- 11) Lcc-Maret2014Document70 pages11) Lcc-Maret2014Oktavia RimandaNo ratings yet

- Cost Management of Large Construction PRDocument5 pagesCost Management of Large Construction PRMike MercNo ratings yet

- Applying Lean Construction Principles in Road Maintenance Planning and SchedulingDocument12 pagesApplying Lean Construction Principles in Road Maintenance Planning and Schedulingana majstNo ratings yet

- Bhangale 2016Document5 pagesBhangale 2016Gian Fahmi PangestuNo ratings yet

- Paper Gestion de Activos ElectricosDocument7 pagesPaper Gestion de Activos ElectricosAntonio Olmedo AvalosNo ratings yet

- Audit Role in Feasibility Studies and Conversions 2015Document5 pagesAudit Role in Feasibility Studies and Conversions 2015Roni YunisNo ratings yet

- Transportation Decision Making: Principles of Project Evaluation and ProgrammingFrom EverandTransportation Decision Making: Principles of Project Evaluation and ProgrammingNo ratings yet

- Research Framing & Justification Canvas PDFDocument1 pageResearch Framing & Justification Canvas PDFMarco BarretoNo ratings yet

- Graphs: CS 308 - Data StructuresDocument38 pagesGraphs: CS 308 - Data StructuresAmit RajNo ratings yet

- Experimental DesignsDocument23 pagesExperimental DesignsRika KartikaNo ratings yet

- Representation of Indonesian Revolution in Poem Rapat Mengganyang 7 Setan by H.R. BandaharoDocument13 pagesRepresentation of Indonesian Revolution in Poem Rapat Mengganyang 7 Setan by H.R. BandaharoSetyo Wahyu NugrohoNo ratings yet

- MGT604 Assessment 2B Brief - T3 2021Document7 pagesMGT604 Assessment 2B Brief - T3 2021Samir BhandariNo ratings yet

- Bso ExamDocument4 pagesBso ExamAssignments HelperNo ratings yet

- Current TrendDocument11 pagesCurrent TrendBrandi KaufmanNo ratings yet

- Thesis Proposal Tribhuvan UniversityDocument8 pagesThesis Proposal Tribhuvan Universitylisamoorewashington100% (2)

- BUS323 International Management: Unit Information and Learning GuideDocument31 pagesBUS323 International Management: Unit Information and Learning GuideDelishaNo ratings yet

- Gombich On MethodsDocument9 pagesGombich On MethodsJúlio MartinsNo ratings yet

- Ivanov Et Al (2008) - Some Practical Aspects of MASW Analysis and ProcessingDocument13 pagesIvanov Et Al (2008) - Some Practical Aspects of MASW Analysis and ProcessingramosmanoNo ratings yet

- A Level Biology Statistics Summary Test Formula Use Degrees of Freedom Accept/reject Null Hypothesis Extra InformationDocument12 pagesA Level Biology Statistics Summary Test Formula Use Degrees of Freedom Accept/reject Null Hypothesis Extra InformationmohammedNo ratings yet