You might also like

- RISK MGMT 321Document80 pagesRISK MGMT 321Yehualashet MekonninNo ratings yet

- Risk Chapter 1Document12 pagesRisk Chapter 1N ENo ratings yet

- RISK Management and InsuranceDocument10 pagesRISK Management and InsuranceWonde Biru100% (1)

- Concepts of Risk and InsuranceDocument20 pagesConcepts of Risk and Insurancetanvi murumkarNo ratings yet

- Risk Management and Insurance (DRMC)Document123 pagesRisk Management and Insurance (DRMC)Kass amenesheNo ratings yet

- Risk Cha 1Document16 pagesRisk Cha 1Abreham AwokeNo ratings yet

- Chapter 1Document20 pagesChapter 1habtamuNo ratings yet

- Risk and InsuranceDocument29 pagesRisk and InsuranceFaheemNo ratings yet

- Risk Management HandoutDocument114 pagesRisk Management HandoutGebrewahd HagosNo ratings yet

- Chapter One (1) 1. Risk and Related TopicsDocument61 pagesChapter One (1) 1. Risk and Related TopicsBeka AsraNo ratings yet

- CHAPTER 1-Introduction To RiskDocument8 pagesCHAPTER 1-Introduction To RiskgozaloiNo ratings yet

- Chapter ObjectivesDocument19 pagesChapter Objectivesborena extensionNo ratings yet

- Risk AllDocument108 pagesRisk AllGabi MamushetNo ratings yet

- Risk Management and Insurance HandoutDocument99 pagesRisk Management and Insurance HandoutGregg AaronNo ratings yet

- Chapter One (1) 1. Risk and Related TopicsDocument12 pagesChapter One (1) 1. Risk and Related TopicssolomonaauNo ratings yet

- CHAPTER 1 Risk and Related Topics NewDocument10 pagesCHAPTER 1 Risk and Related Topics NewbikilahussenNo ratings yet

- Risk Management PDFDocument146 pagesRisk Management PDFFikre FekaduNo ratings yet

- Risk Management EssentialsDocument71 pagesRisk Management Essentials0913314630No ratings yet

- Risk and Related Topics Chapter OneDocument14 pagesRisk and Related Topics Chapter OneAbel HailuNo ratings yet

- LC Risk MGT CH 1Document7 pagesLC Risk MGT CH 1newaybeyene5No ratings yet

- Risk Chap 1 & 2 From MKTG DPRTDocument20 pagesRisk Chap 1 & 2 From MKTG DPRTnewaybeyene5No ratings yet

- Chapter One 2Document12 pagesChapter One 2Tahir DestaNo ratings yet

- Risk Management and Insurance Chapter 1-1Document10 pagesRisk Management and Insurance Chapter 1-1bayrashowNo ratings yet

- Lesson 1: Basic Concepts of Risk Management: Week 1Document73 pagesLesson 1: Basic Concepts of Risk Management: Week 1Anna DerNo ratings yet

- Risk Management Chapter OneDocument9 pagesRisk Management Chapter Onekirubel legeseNo ratings yet

- Introduction to Understanding RiskDocument33 pagesIntroduction to Understanding RiskShuvro RahmanNo ratings yet

- Rish Ch@oneDocument9 pagesRish Ch@oneibrahim JimaleNo ratings yet

- Risk and Uncertainty in InsuranceDocument8 pagesRisk and Uncertainty in InsuranceEbsa AdemeNo ratings yet

- Risk Chap 1-3Document33 pagesRisk Chap 1-3Tilahun GirmaNo ratings yet

- Principles of InsurenceDocument257 pagesPrinciples of InsurenceKomal PanditNo ratings yet

- Risk &insuranceDocument138 pagesRisk &insurancesabit hussenNo ratings yet

- Risk Chapter 1-4 - 1Document56 pagesRisk Chapter 1-4 - 1YonasBirhanuNo ratings yet

- 2023 BWIA 121 ReaderDocument293 pages2023 BWIA 121 ReaderIrfaan CassimNo ratings yet

- Introduction To Risk Management Chapter One Basic Concepts of RiskDocument32 pagesIntroduction To Risk Management Chapter One Basic Concepts of RiskYehualashet MekonninNo ratings yet

- Risk Concepts ChapterDocument77 pagesRisk Concepts ChapterYosef Ketema100% (1)

- Risk Management and InsuranceDocument121 pagesRisk Management and Insurancekidus Berhanu100% (1)

- CH 1 Risk - Related 1Document8 pagesCH 1 Risk - Related 1yeabsira semuNo ratings yet

- Chapter One The Nature of RiskDocument11 pagesChapter One The Nature of RiskGregg AaronNo ratings yet

- RISK MGT CHAP-IDocument37 pagesRISK MGT CHAP-Inatiman090909No ratings yet

- Risk management assignmentDocument9 pagesRisk management assignmentAsteway MesfinNo ratings yet

- Chapter Five - ResponsibilitesDocument43 pagesChapter Five - ResponsibilitesStar branchNo ratings yet

- Ramins 1&2Document24 pagesRamins 1&2bayisabirhanu567No ratings yet

- Report Bosh - Copy (Acsaran and Absara)Document5 pagesReport Bosh - Copy (Acsaran and Absara)Al-Qudcy AbsaraNo ratings yet

- Group 1 - Introductory ConceptsDocument5 pagesGroup 1 - Introductory ConceptsAl-Qudcy AbsaraNo ratings yet

- Risk Chapter-1Document8 pagesRisk Chapter-1damenaga35No ratings yet

- Concept of riskDocument12 pagesConcept of riskJer RyNo ratings yet

- Definitions of Risk: Topic 1. Risk and Risk ManagementDocument14 pagesDefinitions of Risk: Topic 1. Risk and Risk ManagementLNo ratings yet

- WM Insurance Set 1 Risk Mangement ProcessDocument17 pagesWM Insurance Set 1 Risk Mangement ProcessRohit GhaiNo ratings yet

- Differentiate between hazard, risk, and safetyDocument2 pagesDifferentiate between hazard, risk, and safetyirishkate matugasNo ratings yet

- Insu 3 Risk ManagementDocument10 pagesInsu 3 Risk ManagementMd Fahim Muntasir HeavenNo ratings yet

- Chapter I RiskDocument14 pagesChapter I RiskCanaanNo ratings yet

- Risk and Insurance Chapter OverviewDocument16 pagesRisk and Insurance Chapter Overviewmufarowashe marechaNo ratings yet

- Ch1 - Risk and Its TreatmentDocument16 pagesCh1 - Risk and Its TreatmentghaidaNo ratings yet

- Principles of InsuranceDocument35 pagesPrinciples of Insuranceckchetankhatri967No ratings yet

- Differentiating pure, speculative, personal, property and liability risksDocument5 pagesDifferentiating pure, speculative, personal, property and liability risksDereje BelayNo ratings yet

- 3 Engineers Responsibility For SafetyDocument4 pages3 Engineers Responsibility For SafetyGOKILA VARTHINI MNo ratings yet

- Lecture 1 Insurance RiskDocument43 pagesLecture 1 Insurance RiskKazi SaifulNo ratings yet

- Risk Management G InsuranceDocument160 pagesRisk Management G InsurancePrasanta Ghosh100% (1)

- RiskDocument10 pagesRiskAmuliya VSNo ratings yet

- Assessment of Costing and Pricing SystemDocument53 pagesAssessment of Costing and Pricing SystemCanaan100% (3)

- Introducing Liberalism in International Relations TheoryDocument4 pagesIntroducing Liberalism in International Relations TheoryCanaanNo ratings yet

- Insurnance Chapter Iii-Insurance: An Overview: 3.1. The Nature and Functions of InsuranceDocument29 pagesInsurnance Chapter Iii-Insurance: An Overview: 3.1. The Nature and Functions of InsuranceCanaanNo ratings yet

- Chapter I RiskDocument14 pagesChapter I RiskCanaanNo ratings yet

- Chapter-II Risk Management ProcessDocument44 pagesChapter-II Risk Management ProcessCanaanNo ratings yet

- Insurnance Chapter Iii-Insurance: An Overview: 3.1. The Nature and Functions of InsuranceDocument29 pagesInsurnance Chapter Iii-Insurance: An Overview: 3.1. The Nature and Functions of InsuranceCanaanNo ratings yet

- Chapter I RiskDocument14 pagesChapter I RiskCanaanNo ratings yet

- Chapter-II Risk Management ProcessDocument44 pagesChapter-II Risk Management ProcessCanaanNo ratings yet

- Chapter One Risk and Related ConceptsDocument15 pagesChapter One Risk and Related ConceptsCanaanNo ratings yet

- Corporate Governance in Financing and Banking in BangladeshDocument22 pagesCorporate Governance in Financing and Banking in BangladeshAsrafia Mim 1813026630No ratings yet

- Philip Capital (Objective To Conclusion)Document20 pagesPhilip Capital (Objective To Conclusion)Shubhani PandeyNo ratings yet

- Ar 2011Document410 pagesAr 2011Dennis AngNo ratings yet

- 3c Orange County CaseDocument19 pages3c Orange County Caseannabellekd123No ratings yet

- Corporate Financial Accounting 14th Edition Warren Solutions ManualDocument14 pagesCorporate Financial Accounting 14th Edition Warren Solutions ManualRobertMurphyjgwo100% (59)

- Top Glove Financial AssignmentDocument23 pagesTop Glove Financial Assignmentnigina2lips100% (1)

- Candlestick Patterns PDF Free Guide DownloadDocument11 pagesCandlestick Patterns PDF Free Guide DownloadGreg Mavhunga88% (8)

- Taxes: Corporate: Sec. S OcDocument2 pagesTaxes: Corporate: Sec. S OcAnonymous JqimV1ENo ratings yet

- Accounting Top 50 QuestionsDocument152 pagesAccounting Top 50 QuestionsDeep Mehta0% (1)

- The influence of capital structure on firm valueDocument51 pagesThe influence of capital structure on firm valueDevikaNo ratings yet

- Capitaltwo RISHABHDocument36 pagesCapitaltwo RISHABHSaloni SharmaNo ratings yet

- Financial Statement Analysis 2Document21 pagesFinancial Statement Analysis 2San Juan EzthieNo ratings yet

- Economics 9732/01: Pioneer Junior College, Singapore Preliminary Examinations 2014 Higher 2Document8 pagesEconomics 9732/01: Pioneer Junior College, Singapore Preliminary Examinations 2014 Higher 2Yvette LimNo ratings yet

- BPI UITF Client Suitability Assessment FormDocument6 pagesBPI UITF Client Suitability Assessment FormNorman PeñaNo ratings yet

- Internal ReconstructionDocument5 pagesInternal ReconstructionJoshua StarkNo ratings yet

- MoneyDocument3 pagesMoneyKrrish WaliaNo ratings yet

- Monetary Policy Notes PDFDocument18 pagesMonetary Policy Notes PDFOptimistic Khan50% (2)

- Quick Check-Chapter 6: Skechers Famous FootwearDocument2 pagesQuick Check-Chapter 6: Skechers Famous FootwearJannette Treviño RamosNo ratings yet

- Vietnam's Exchange Rate Regime Transition Since 1999Document12 pagesVietnam's Exchange Rate Regime Transition Since 1999wikileaks30No ratings yet

- Notes On Final Accounts & Journal& Ledger ProblemDocument17 pagesNotes On Final Accounts & Journal& Ledger ProblemSaiVenkatNo ratings yet

- How Much Money Do You Need to Be a Successful Day TraderDocument3 pagesHow Much Money Do You Need to Be a Successful Day TraderChukwuebuka Okechukwu (KingNebx)No ratings yet

- Investment Banking Deal ProcessDocument25 pagesInvestment Banking Deal Processdkgrinder100% (1)

- Chapter FiveDocument14 pagesChapter Fivemubarek oumerNo ratings yet

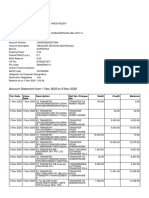

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyNo ratings yet

- Chapter 12, Problem 1COMP: (To Record Issuance of 4,000 Preferred Shares in Excess of Par)Document1 pageChapter 12, Problem 1COMP: (To Record Issuance of 4,000 Preferred Shares in Excess of Par)Varun SharmaNo ratings yet

- Partnership profit sharing ratiosDocument2 pagesPartnership profit sharing ratiosm v r rNo ratings yet

- Problems Chapter 11Document29 pagesProblems Chapter 11Incia100% (1)

- Planet Starbucks Case AnalysisDocument3 pagesPlanet Starbucks Case AnalysisJugraj Dharni50% (2)

- 66107bos53355fold p8Document19 pages66107bos53355fold p8sam kapoorNo ratings yet

- PARTNERSHIPDocument84 pagesPARTNERSHIPJohn Rey LabasanNo ratings yet