You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- Arrow - Dry Bulk Outlook - Apr-20Document22 pagesArrow - Dry Bulk Outlook - Apr-20Sahil FarazNo ratings yet

- Chaity Composite LTD: Goal For Customer Focus: Customar ClaimDocument1 pageChaity Composite LTD: Goal For Customer Focus: Customar ClaimMoklesur RahmanNo ratings yet

- India Real Estate: July - September 2020Document17 pagesIndia Real Estate: July - September 2020jitesh vachhaniNo ratings yet

- Arup Raha - Indonesia in A Covid-19 WorldDocument10 pagesArup Raha - Indonesia in A Covid-19 WorldMikesNo ratings yet

- BWR MicrofinanceReport FinalDocument13 pagesBWR MicrofinanceReport FinalHarsh KumarNo ratings yet

- Development Bank of Mongolia: Monthly Economic ReportDocument4 pagesDevelopment Bank of Mongolia: Monthly Economic ReportBiliguudei AmarsaikhanNo ratings yet

- BCG India Economic Monitor Dec 2020Document42 pagesBCG India Economic Monitor Dec 2020akashNo ratings yet

- Cement Sector - The Beginning of Long Term Recovery CycleDocument15 pagesCement Sector - The Beginning of Long Term Recovery CycleOnggo iMamNo ratings yet

- HIM2018Q2NPDocument6 pagesHIM2018Q2NPPuru SaxenaNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- Análisis de Entorno Jacpack (Inglés)Document12 pagesAnálisis de Entorno Jacpack (Inglés)jhonny moralesNo ratings yet

- Economic Impact of Covid-19 in The Philippines: Fact File 2020Document26 pagesEconomic Impact of Covid-19 in The Philippines: Fact File 2020Girlee Jhene CadeliñaNo ratings yet

- DBS China Dairy Industry Jun110217Document9 pagesDBS China Dairy Industry Jun110217Tony LeongNo ratings yet

- State of The Market Presentation - September 2022Document23 pagesState of The Market Presentation - September 2022Emmanuel Manex KubikwaNo ratings yet

- EmpsitDocument42 pagesEmpsitPrathamesh GhargeNo ratings yet

- Top 100 CompaniiDocument34 pagesTop 100 CompaniiDan MarianNo ratings yet

- HDFC Bank Research Presentation April 2020Document41 pagesHDFC Bank Research Presentation April 2020MohitNo ratings yet

- Growth and Investment: 25000 5000 6000 7000 New Cases (7 Day MA) Total Deaths (RHS)Document16 pagesGrowth and Investment: 25000 5000 6000 7000 New Cases (7 Day MA) Total Deaths (RHS)Rk SunnyNo ratings yet

- Popcorn (Savory Snacks) Market in India - Outlook To 2020: Market Size, Growth and Forecast AnalyticsDocument8 pagesPopcorn (Savory Snacks) Market in India - Outlook To 2020: Market Size, Growth and Forecast AnalyticspratyushNo ratings yet

- Earnings Update Q1FY22Document15 pagesEarnings Update Q1FY22sai mohanNo ratings yet

- Today's Market : Springfield Area Local Market Report, Third Quarter 2010Document7 pagesToday's Market : Springfield Area Local Market Report, Third Quarter 2010phatty34No ratings yet

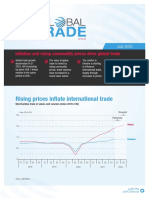

- GL Bal: Rising Prices Inflate International TradeDocument11 pagesGL Bal: Rising Prices Inflate International TradeBekele Guta GemeneNo ratings yet

- 2024-02 Monthly Housing Market OutlookDocument57 pages2024-02 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-10 Monthly Housing Market OutlookDocument57 pages2023-10 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- The Silver Economy in Latin America and The Caribbean Aging As An Opportunity For Innovation Entrepreneurship and InclusionDocument40 pagesThe Silver Economy in Latin America and The Caribbean Aging As An Opportunity For Innovation Entrepreneurship and InclusionFabiana SouzaNo ratings yet

- Latin America The Caribbean: Aging As An Opportunity For Innovation, Entrepreneurship, and InclusionDocument40 pagesLatin America The Caribbean: Aging As An Opportunity For Innovation, Entrepreneurship, and InclusionFabiana SouzaNo ratings yet

- Air Cargo Market Analysis: Air Cargo Volumes Reached An All-Time High in MarchDocument4 pagesAir Cargo Market Analysis: Air Cargo Volumes Reached An All-Time High in MarchJuan ArcilaNo ratings yet

- 2024-01 Monthly Housing Market OutlookDocument57 pages2024-01 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- US Banks Face Higher Unrealized Securities Losses Amid Rising RatesDocument8 pagesUS Banks Face Higher Unrealized Securities Losses Amid Rising RatesfsfefNo ratings yet

- 6.future PotentialsDocument5 pages6.future PotentialscesarNo ratings yet

- Assignment 2 CoronaDocument2 pagesAssignment 2 CoronasumeetkantkaulNo ratings yet

- 中国消费:新时代的开始(英)Document6 pages中国消费:新时代的开始(英)jessica.haiyan.zhengNo ratings yet

- 2023-06 Monthly Housing Market OutlookDocument57 pages2023-06 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Money Printing in 2020Document15 pagesMoney Printing in 2020Zerohedge100% (5)

- Cotton Outlook: United States Department of AgricultureDocument18 pagesCotton Outlook: United States Department of AgricultureNitin GuptaNo ratings yet

- Apparel and Footwear in Vietnam DatagraphicsDocument4 pagesApparel and Footwear in Vietnam DatagraphicsMy TranNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- EPCA Seminar - Introduction Megatrends Driving Petrochemical Demand October 2020Document16 pagesEPCA Seminar - Introduction Megatrends Driving Petrochemical Demand October 2020mostafa bagheriNo ratings yet

- Life Insurance: Growth Gradually ReboundingDocument9 pagesLife Insurance: Growth Gradually ReboundingwhitenagarNo ratings yet

- Capitalism Is FailingDocument17 pagesCapitalism Is FailingPacoNo ratings yet

- Covid-19 - The Route To A Planned and Predictable Aviation Industry RecoveryDocument22 pagesCovid-19 - The Route To A Planned and Predictable Aviation Industry RecoverySusheel Kumar SiramNo ratings yet

- LA Economic Vitals Dec Jan 2021Document5 pagesLA Economic Vitals Dec Jan 2021ChrisMNo ratings yet

- Indonesia Property Market Overview Recent Update in Transition Period 190920 01Document20 pagesIndonesia Property Market Overview Recent Update in Transition Period 190920 01rimuru samaNo ratings yet

- Review First Quarter 2022 1650676396Document6 pagesReview First Quarter 2022 1650676396myles zyblockNo ratings yet

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2024-03 Monthly Housing Market OutlookDocument57 pages2024-03 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- CareEdge Ratings Update On Tyre IndustryDocument5 pagesCareEdge Ratings Update On Tyre IndustryIshan GuptaNo ratings yet

- IT Services - Analyst Presentation - Sep15Document15 pagesIT Services - Analyst Presentation - Sep15Nimish NamaNo ratings yet

- Ncpi 20230821eDocument2 pagesNcpi 20230821eAdaderana OnlineNo ratings yet

- DKI's Economy: Navigating The Danger Zone: Fithra Faisal Hastiadi PH.D Executive Director of Next PolicyDocument46 pagesDKI's Economy: Navigating The Danger Zone: Fithra Faisal Hastiadi PH.D Executive Director of Next PolicyVesper 007No ratings yet

- Special Release: Philippine Statistics AuthorityDocument7 pagesSpecial Release: Philippine Statistics AuthorityYumie YamazukiNo ratings yet

- Ditcinf2021d2 enDocument8 pagesDitcinf2021d2 enseafishNo ratings yet

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Industry ReportDocument21 pagesIndustry ReportAman PriyadarshiNo ratings yet

- CRISIL Trade First Cut-Oct2020Document4 pagesCRISIL Trade First Cut-Oct2020KARTHIK PRASADNo ratings yet

- Banking: CHAPTER A: Brief About The Indian Banking SectorDocument63 pagesBanking: CHAPTER A: Brief About The Indian Banking SectorDevang ParabNo ratings yet

- Education Labour - Inequality in Ecuador - 2006 2016 - ENCDocument30 pagesEducation Labour - Inequality in Ecuador - 2006 2016 - ENCErnesto NietoNo ratings yet

- Classification Notes: Application of IRS Rules To Indian Coastal VesselsDocument14 pagesClassification Notes: Application of IRS Rules To Indian Coastal VesselsAmit OzaNo ratings yet

- Key Research Issues in Supply Chain & Logistics Management: 2030Document24 pagesKey Research Issues in Supply Chain & Logistics Management: 2030Amit Oza0% (1)

- Reducing International Shipping'S Carbon Intensity Through The Imo'S Eexi and CiiDocument6 pagesReducing International Shipping'S Carbon Intensity Through The Imo'S Eexi and CiiAmit OzaNo ratings yet

- 30-05-09 Proposal Caribbean Emergency Legislation Project Activity 201 2Document19 pages30-05-09 Proposal Caribbean Emergency Legislation Project Activity 201 2Amit OzaNo ratings yet

- Radio-Environmental Impacts of Phosphogypsum Disposed On A Coastal Area in Vasiliko, CyprusDocument7 pagesRadio-Environmental Impacts of Phosphogypsum Disposed On A Coastal Area in Vasiliko, CyprusMario WhoeverNo ratings yet

- John G Lake Biografc3ada Diarios de AvivamientosDocument37 pagesJohn G Lake Biografc3ada Diarios de AvivamientosEsteban De Vargas Cueter0% (2)

- Macintosh Developer's Guide To The Wacom TabletDocument29 pagesMacintosh Developer's Guide To The Wacom TabletnqrcNo ratings yet

- MCQ NetworkingDocument3 pagesMCQ NetworkingNamita SahuNo ratings yet

- Soil Mechanics and Foundations - (Chapter 10 Shear Strength of Soils) PDFDocument63 pagesSoil Mechanics and Foundations - (Chapter 10 Shear Strength of Soils) PDFFrancisco Reyes0% (1)

- Sessions 2, 3, 4, 5 - Inflation - National IncomeDocument110 pagesSessions 2, 3, 4, 5 - Inflation - National IncomeAbhay SahuNo ratings yet

- 03 - Cie - Cable Ties - (3.01 - 3.02)Document2 pages03 - Cie - Cable Ties - (3.01 - 3.02)ThilinaNo ratings yet

- 27 August To 02 SeptemberDocument16 pages27 August To 02 SeptemberpratidinNo ratings yet

- George Bernard Shaw by Chesterton, G. K. (Gilbert Keith), 1874-1936Document75 pagesGeorge Bernard Shaw by Chesterton, G. K. (Gilbert Keith), 1874-1936Gutenberg.orgNo ratings yet

- Mumbai 17022022Document23 pagesMumbai 17022022vivekNo ratings yet

- Model Solutions: Supplimentary Paper 1 - Set ADocument19 pagesModel Solutions: Supplimentary Paper 1 - Set ACARPE NOCTEMNo ratings yet

- Arlorio 05 Phenolic Antioxidantsin Cacao Hulls PhysiologyDocument6 pagesArlorio 05 Phenolic Antioxidantsin Cacao Hulls Physiologydjguevara1No ratings yet

- ArchitectureDocument268 pagesArchitectureAndrijaNo ratings yet

- ZXCTN Seamless MPLS (BGP LU) Principles and Applications - R1.1Document24 pagesZXCTN Seamless MPLS (BGP LU) Principles and Applications - R1.1kyi lwinNo ratings yet

- Pictorial Atlas of Botulinum Toxin Injection. Dosage Localization Application. (1) PDF PDFDocument2 pagesPictorial Atlas of Botulinum Toxin Injection. Dosage Localization Application. (1) PDF PDFTeng Lip Yuen50% (4)

- Angels Among UsDocument4 pagesAngels Among UsLanny CarpenterNo ratings yet

- 9709 s11 QP 62 PDFDocument4 pages9709 s11 QP 62 PDFSzeYee OonNo ratings yet

- Agency Theory EssayDocument2 pagesAgency Theory EssayAnggi KartikaNo ratings yet

- Tle 10 Agricrop Production Quarter 2 Week 8 Summative TestDocument5 pagesTle 10 Agricrop Production Quarter 2 Week 8 Summative TestRosalieMarCuyaNo ratings yet

- Transition TheoryDocument36 pagesTransition TheoryMatty Jolbitado100% (1)

- Self-Learning Home Task (SLHT) : KG Given To HelperDocument4 pagesSelf-Learning Home Task (SLHT) : KG Given To HelperCatherine AbabonNo ratings yet

- SOILMECHANICS Laboratory Manual 11 ExperimentsDocument58 pagesSOILMECHANICS Laboratory Manual 11 ExperimentsChristianNo ratings yet

- HS BreakdownDocument8 pagesHS BreakdownThane SnymanNo ratings yet

- The Horizons Limits and Taxonomies of OtDocument1 pageThe Horizons Limits and Taxonomies of Othalil başkanNo ratings yet

- The Heavenly VisionDocument3 pagesThe Heavenly VisionGuillermoRifoReyesNo ratings yet

- Ritual of LilithDocument0 pagesRitual of LilithDarely Sabbati100% (3)

- PGP Guidelines 2017Document27 pagesPGP Guidelines 2017vignesh__m0% (1)

- Review of LiteratureDocument18 pagesReview of LiteratureVimal VickyNo ratings yet

- Practical Research 1 LAS - Week 2Document1 pagePractical Research 1 LAS - Week 2Limar Geoff G. RosalesNo ratings yet

- Free PRM Handbook PDFDocument2 pagesFree PRM Handbook PDFRichard0% (1)