You might also like

- PDF 718201235101PMKBLAnnualReport 18.07.2012Document120 pagesPDF 718201235101PMKBLAnnualReport 18.07.2012Keshav KalaniNo ratings yet

- By-Pallavi Malhotra Mba 2 YearDocument10 pagesBy-Pallavi Malhotra Mba 2 YearparulpalllaviNo ratings yet

- Havells India Limited Key Financials and Stock PerformanceDocument4 pagesHavells India Limited Key Financials and Stock PerformanceShivu BiradarNo ratings yet

- DocumentDocument34 pagesDocumentAngel JeniferNo ratings yet

- Company Profile: Hero Motocorp LimitedDocument25 pagesCompany Profile: Hero Motocorp LimitedjupinderNo ratings yet

- HUL Financial Analysis Reveals Decreasing Liquidity RatiosDocument19 pagesHUL Financial Analysis Reveals Decreasing Liquidity Ratiosspantdur100% (1)

- Corporate Social Responsibility (CSR) at Hindustan Uniliver Ltd. - A Case StudyDocument7 pagesCorporate Social Responsibility (CSR) at Hindustan Uniliver Ltd. - A Case StudyFalak ShaikhNo ratings yet

- Reliance Communications LTDDocument4 pagesReliance Communications LTDSahil JainNo ratings yet

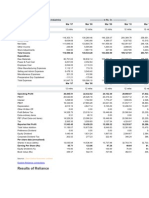

- Reliance Industries profit and loss analysisDocument10 pagesReliance Industries profit and loss analysisJack MartinNo ratings yet

- Annual Report 2015 LlyodsDocument139 pagesAnnual Report 2015 Llyodsratan203No ratings yet

- Corporate Social Responsibility (CSR) at Hindustan Uniliver Ltd. - A Case StudyDocument7 pagesCorporate Social Responsibility (CSR) at Hindustan Uniliver Ltd. - A Case StudyShalini VermaNo ratings yet

- 99 (Xi A) (Com) Shreue PatelDocument14 pages99 (Xi A) (Com) Shreue PatelChintan PatelNo ratings yet

- Voltamp Transformers Ltd. Was Initially Incorporated As Private Limited Company and Established in Year 1967 in Vadodara. Further, by SpecialDocument8 pagesVoltamp Transformers Ltd. Was Initially Incorporated As Private Limited Company and Established in Year 1967 in Vadodara. Further, by Specialreet gillNo ratings yet

- Bharti Airtel Financial AnalysisDocument10 pagesBharti Airtel Financial Analysismit024No ratings yet

- Marico Company AnalysisDocument12 pagesMarico Company AnalysisKshitij MaheshwaryNo ratings yet

- Havells Final ProjectDocument17 pagesHavells Final Projectsimran agarwalNo ratings yet

- FAC Project ReportDocument16 pagesFAC Project Reportmini nivalNo ratings yet

- Cotton Greaves FinalDocument34 pagesCotton Greaves FinalGautam KumarNo ratings yet

- Schneider Electric Infrastructure LTDDocument22 pagesSchneider Electric Infrastructure LTDShruti DasNo ratings yet

- NFL Annual Report 2011-2012Document108 pagesNFL Annual Report 2011-2012prabhjotbhangalNo ratings yet

- Arun Rawal PJ (2) 1Document78 pagesArun Rawal PJ (2) 1Arun rawalNo ratings yet

- ABB India Annual Report 2009Document74 pagesABB India Annual Report 2009Mohit DaftaryNo ratings yet

- Havells India Internship Report Analysis Electrical Company Marketing StrategyDocument70 pagesHavells India Internship Report Analysis Electrical Company Marketing StrategywasimkhanforyouNo ratings yet

- Sub: Accounting and Financial Management IVRCL and Infrastructure PVT LTD Submitted To: Dr. D.R.Patel By: Shaikh Adnan Cp1812Document15 pagesSub: Accounting and Financial Management IVRCL and Infrastructure PVT LTD Submitted To: Dr. D.R.Patel By: Shaikh Adnan Cp1812Adnan ShaikhNo ratings yet

- Omax Annual ReprtDocument78 pagesOmax Annual ReprtSalini RajamohanNo ratings yet

- 1: Industry Profile:-: 1.1 Air Conditioning Industry in IndiaDocument34 pages1: Industry Profile:-: 1.1 Air Conditioning Industry in IndiaShilpi Kumari100% (1)

- RIL Annual Report 2013Document228 pagesRIL Annual Report 2013Amar ItagiNo ratings yet

- CMA CIA 3Document23 pagesCMA CIA 3vaibhav1504.vsNo ratings yet

- Assignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailDocument9 pagesAssignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailSachin Kumar BassiNo ratings yet

- Training & Development at Havell's India LimitedDocument109 pagesTraining & Development at Havell's India LimitedPradeep Yadav100% (1)

- Acn 441Document11 pagesAcn 441Esraah AhmedNo ratings yet

- Edelweiss Financial Services LTDDocument7 pagesEdelweiss Financial Services LTDMukesh SharmaNo ratings yet

- The UB Group: Presentation ON Mcdowell & Company United Breweries LTDDocument30 pagesThe UB Group: Presentation ON Mcdowell & Company United Breweries LTDsonali_shigvanNo ratings yet

- BUY BUY BUY BUY: Exide Industries LTDDocument13 pagesBUY BUY BUY BUY: Exide Industries LTDcksharma68No ratings yet

- About The Company: MissionDocument6 pagesAbout The Company: MissionAakash BhutaniNo ratings yet

- 2010 Annual ReportDocument84 pages2010 Annual ReportnaveenNo ratings yet

- MBA Student's Marketing Project on LG Electronics Consumer Buying BehaviorDocument117 pagesMBA Student's Marketing Project on LG Electronics Consumer Buying BehaviorSandeep Kumar Daksha100% (1)

- Assignment Analysis of Financial Statements Company: HindalcoDocument7 pagesAssignment Analysis of Financial Statements Company: HindalcomayurgharatNo ratings yet

- Havells Project ShafeeqDocument33 pagesHavells Project ShafeeqnoufaNo ratings yet

- Here 2013-14Document180 pagesHere 2013-14AnneJacinthNo ratings yet

- Aditya Birla Draft 1Document5 pagesAditya Birla Draft 1Vishruth KhareNo ratings yet

- Food DPRDocument34 pagesFood DPRPallav ChhawanNo ratings yet

- Herbal GutkaDocument8 pagesHerbal GutkaKamlesh Rajput0% (1)

- Company ProfileDocument7 pagesCompany ProfileUmesh TyagiNo ratings yet

- Suprajit Engineering Limited - Annual Report 2010-11Document72 pagesSuprajit Engineering Limited - Annual Report 2010-11red cornerNo ratings yet

- Thermal Power ProjectDocument40 pagesThermal Power ProjectHinal GangarNo ratings yet

- Philips India LimitedDocument26 pagesPhilips India LimitedArun Kumar ArunNo ratings yet

- Financial Analysis of Havells India Ltd.Document55 pagesFinancial Analysis of Havells India Ltd.Bhuwan Gaur100% (3)

- ABB India Annual Report 2006Document70 pagesABB India Annual Report 2006Anupama VmNo ratings yet

- Content: SR No. Particulars Page NoDocument17 pagesContent: SR No. Particulars Page NoPiNak JogiaNo ratings yet

- Fa ProjectDocument16 pagesFa Projecttapas_kbNo ratings yet

- Indian Oil Corporation LimitedDocument40 pagesIndian Oil Corporation LimitedAnu Jindal100% (1)

- Videocon ProjectDocument58 pagesVideocon Projectmrinal_kakkar8215100% (2)

- From Products to Services: Insight and Experience from Companies Which Have Embraced the Service EconomyFrom EverandFrom Products to Services: Insight and Experience from Companies Which Have Embraced the Service EconomyRating: 4.5 out of 5 stars4.5/5 (2)

- IT-Driven Business Models: Global Case Studies in TransformationFrom EverandIT-Driven Business Models: Global Case Studies in TransformationNo ratings yet

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportFrom EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo ratings yet

- Capturing the Digital Economy—A Proposed Measurement Framework and Its Applications: A Special Supplement to Key Indicators for Asia and the Pacific 2021From EverandCapturing the Digital Economy—A Proposed Measurement Framework and Its Applications: A Special Supplement to Key Indicators for Asia and the Pacific 2021No ratings yet

- Andhra Allocation MattleDocument4 pagesAndhra Allocation MattleSubodh KumarNo ratings yet

- Personal InterviewDocument1 pagePersonal InterviewSubodh KumarNo ratings yet

- SubodhhDocument1 pageSubodhhSubodh KumarNo ratings yet

- Itc LimitedDocument15 pagesItc LimitedSubodh KumarNo ratings yet

- Steel Authority of India Limited Term PaperDocument53 pagesSteel Authority of India Limited Term PaperSubodh KumarNo ratings yet

- CAM RecoveryDocument26 pagesCAM RecoverySubramanian S (IN)No ratings yet

- Basic Bookkeeping Student ManualDocument37 pagesBasic Bookkeeping Student Manualcasscactus100% (1)

- Assignment Print View Lesson 6 PDFDocument8 pagesAssignment Print View Lesson 6 PDFnewonemadeNo ratings yet

- CH-2-Study Guide PDFDocument15 pagesCH-2-Study Guide PDFnirali17No ratings yet

- Financial Accounting Mock Exam Multiple Choice QuestionsDocument4 pagesFinancial Accounting Mock Exam Multiple Choice QuestionsGeeta LalwaniNo ratings yet

- 1 MW Solar Power Plant EPC Cost With Multi Crystalline ModulesDocument12 pages1 MW Solar Power Plant EPC Cost With Multi Crystalline ModulesWahid Rahman RahmaniNo ratings yet

- Business Plan For Computer ConsultingDocument20 pagesBusiness Plan For Computer ConsultingjohnNo ratings yet

- Chapter 6 - DepreciationDocument22 pagesChapter 6 - DepreciationUpendra ReddyNo ratings yet

- HOSP1860 4 AdjustingtheaccountsDocument6 pagesHOSP1860 4 AdjustingtheaccountsLule RamaNo ratings yet

- Coffee Distribution Business PlanDocument41 pagesCoffee Distribution Business Planalemayehu tameneNo ratings yet

- London Philatelist:: Old Lamps For FlewDocument28 pagesLondon Philatelist:: Old Lamps For FlewVIORELNo ratings yet

- Financial Aspect FinalDocument12 pagesFinancial Aspect Finalmelvanne tamboboyNo ratings yet

- COMPOUND FINANCIAL INSTRUMENTSDocument21 pagesCOMPOUND FINANCIAL INSTRUMENTSAga Mathew MayugaNo ratings yet

- Recent Advances in Cost Accounting and Cost SystemDocument6 pagesRecent Advances in Cost Accounting and Cost SystemDeepak ChandekarNo ratings yet

- Sol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Document10 pagesSol. Man. - Chapter 4 - Nca Held For Sale & Discontinued Opns.Crown Garcia50% (4)

- Reshmi BakeryDocument14 pagesReshmi BakeryAbhishek A PNo ratings yet

- AC 315 Exam 1 ReviewDocument18 pagesAC 315 Exam 1 Reviewkcreel2007No ratings yet

- Income Statement Case StudyDocument18 pagesIncome Statement Case StudyToto100% (1)

- ACCA - FA - 习题课 - 大题练习Document59 pagesACCA - FA - 习题课 - 大题练习mxw0717No ratings yet

- AC11 - Chaapter 7Document34 pagesAC11 - Chaapter 7anon_467190796100% (1)

- INCOME TAX ReviewDocument54 pagesINCOME TAX ReviewKeepy FamadorNo ratings yet

- Prepare Cost Sheet Any ProductDocument20 pagesPrepare Cost Sheet Any Productv adamNo ratings yet

- MinutesDocument8 pagesMinutesapi-238025861No ratings yet

- DBM Dof Dilg Joint Memorandum Circular No 2018 1 Dated July 12 2018Document10 pagesDBM Dof Dilg Joint Memorandum Circular No 2018 1 Dated July 12 2018barangay08 can-avidesamarNo ratings yet

- CAIIB-ABM-FORMULADocument3 pagesCAIIB-ABM-FORMULAVasimNo ratings yet

- ExerciseDocument5 pagesExerciseICS TEAMNo ratings yet

- Financial Planning and Forecasting Pro Forma Financial StatementsDocument22 pagesFinancial Planning and Forecasting Pro Forma Financial StatementsCOLONEL ZIKRIA0% (1)

- ABC Cash Flow StatementDocument1 pageABC Cash Flow StatementLps0625No ratings yet

- Assignment Classification Table: Topics Brief Exercises Exercises ProblemsDocument125 pagesAssignment Classification Table: Topics Brief Exercises Exercises ProblemsYang LeksNo ratings yet

- 1-Law Cover Print - Combine634642971062050292 PDFDocument274 pages1-Law Cover Print - Combine634642971062050292 PDFRaj Kunal100% (1)