You might also like

- Assignment On Installment SalesDocument12 pagesAssignment On Installment SalesTricia Nicole Dimaano100% (1)

- Installment-Sales-Supplementary-Problems & NotesDocument3 pagesInstallment-Sales-Supplementary-Problems & NotesAlliah Mae ArbastoNo ratings yet

- 8506 - Installment SalesDocument4 pages8506 - Installment SalesAnonymous iNRMC4mgORNo ratings yet

- 8506 - Installment Sales - 113910598Document4 pages8506 - Installment Sales - 113910598Ryan CornistaNo ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- Cpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesDocument15 pagesCpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesSophia PerezNo ratings yet

- FAR PreBoard (1) CPAR BATCH90Document18 pagesFAR PreBoard (1) CPAR BATCH90Bella ChoiNo ratings yet

- AccountingDocument6 pagesAccountingBlue HourNo ratings yet

- AP W1 Correction of ErrorsDocument4 pagesAP W1 Correction of ErrorsALYZA ANGELA ORNEDONo ratings yet

- AFAR 1.4 - Installment SalesDocument7 pagesAFAR 1.4 - Installment SalesKile Rien MonsadaNo ratings yet

- HW On ReceivablesDocument4 pagesHW On ReceivablesGian Carlo RamonesNo ratings yet

- Current LiabilitiesDocument9 pagesCurrent LiabilitiesErine ContranoNo ratings yet

- 11 17 AnswersDocument9 pages11 17 AnswersRizalito SisonNo ratings yet

- Afar 2 - Installment SalesDocument1 pageAfar 2 - Installment SalesPanda ErarNo ratings yet

- Installment ExercisesDocument2 pagesInstallment ExercisesalyssaNo ratings yet

- May 2020 Error SHE Intangibles Liabilities LeasesDocument14 pagesMay 2020 Error SHE Intangibles Liabilities Leasesiraleigh17No ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaJoyce Anne DugayNo ratings yet

- B. 516,518 72,060 CollectionsDocument2 pagesB. 516,518 72,060 CollectionsMichelle Galapon LagunaNo ratings yet

- Topic 2 Installment Sales Module Part 1Document5 pagesTopic 2 Installment Sales Module Part 1Maricel Ann BaccayNo ratings yet

- Installment Sales 1Document2 pagesInstallment Sales 1Jamie Ramos0% (1)

- AE 16 Prelims Problem SolvingDocument6 pagesAE 16 Prelims Problem SolvingJheally SeirNo ratings yet

- 02 FAR02 Accounting-for-ReceivablesDocument3 pages02 FAR02 Accounting-for-ReceivablesBea GarciaNo ratings yet

- Acc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ADocument6 pagesAcc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ARachel LuberiaNo ratings yet

- SCM Budget BSA2ADocument3 pagesSCM Budget BSA2AKaymark Lorenzo0% (2)

- Exercise LiabilitiesDocument2 pagesExercise LiabilitiesAlaine Milka GosycoNo ratings yet

- Homework 5 - Current Liabilities - RevisedDocument3 pagesHomework 5 - Current Liabilities - RevisedalvarezxpatriciaNo ratings yet

- Acctg 205B Prelim ExamDocument1 pageAcctg 205B Prelim ExamBella AyabNo ratings yet

- Errors - Discussion ProblemsDocument2 pagesErrors - Discussion ProblemsHaidee Flavier SabidoNo ratings yet

- 9009-Sale-or-Return-and-Installment-Sales HandoutsDocument2 pages9009-Sale-or-Return-and-Installment-Sales HandoutsAlliah Mae ArbastoNo ratings yet

- Deferred Income Tax Asset and LiabilityDocument4 pagesDeferred Income Tax Asset and Liabilityalcazar rtuNo ratings yet

- AUDITING-Adjusting Entries-Correction of ErrorsDocument10 pagesAUDITING-Adjusting Entries-Correction of ErrorsJamhel MarquezNo ratings yet

- Alom Ia FoDocument18 pagesAlom Ia FoLea Yvette SaladinoNo ratings yet

- Cash Accrual Practice SetDocument2 pagesCash Accrual Practice SetMa. Trixcy De VeraNo ratings yet

- Bac 2211 Cat&assignment Sep 2023Document5 pagesBac 2211 Cat&assignment Sep 2023toniruii98No ratings yet

- Practice Exercises For Confras Units 5 and 6 - Part 1Document3 pagesPractice Exercises For Confras Units 5 and 6 - Part 1xylynn myka cabanatanNo ratings yet

- Spectra NDocument5 pagesSpectra NRichelle Mea B. PeñaNo ratings yet

- Pup Auditofreceivable1 Bsa4 2Document6 pagesPup Auditofreceivable1 Bsa4 2Makoy BixenmanNo ratings yet

- Chapter 1 Liabilities ExercisesDocument3 pagesChapter 1 Liabilities ExercisesAwish FernNo ratings yet

- Special Trans Activity 2Document15 pagesSpecial Trans Activity 2Rachelle JoseNo ratings yet

- Practice Exercise 1.1Document4 pagesPractice Exercise 1.1leshz zynNo ratings yet

- AP 200 3 Change in Accounting Estimates Change in Accounting Policy and Correction of Errors StudentsDocument4 pagesAP 200 3 Change in Accounting Estimates Change in Accounting Policy and Correction of Errors StudentsMonica mangobaNo ratings yet

- FAR 03-19 Loans and Receivables DiscussionDocument20 pagesFAR 03-19 Loans and Receivables DiscussionHana Grace MamangunNo ratings yet

- Far-Single Entry PDFDocument7 pagesFar-Single Entry PDFJanica June FiscalNo ratings yet

- SbaDocument4 pagesSbaahyenn cabello100% (1)

- Auditing Problems MidtermDocument20 pagesAuditing Problems MidtermjasfNo ratings yet

- Chapter 3-4 Lab Problems 9.14.2021Document1 pageChapter 3-4 Lab Problems 9.14.2021Abdullah alhamaadNo ratings yet

- Audit of Inventories and Trade Payables BA 123 Exercise Set BDocument6 pagesAudit of Inventories and Trade Payables BA 123 Exercise Set BBecky GonzagaNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Kate PaquizNo ratings yet

- Numbers 36 and 37 (Installment Sales)Document2 pagesNumbers 36 and 37 (Installment Sales)elsana philipNo ratings yet

- Installment SalesDocument2 pagesInstallment SalesJULLIE CARMELLE H. CHATTONo ratings yet

- Activity 1b - Current LiabilitiesDocument2 pagesActivity 1b - Current LiabilitiesUchayyaNo ratings yet

- ACCTG 105 Midterm - Quiz No. 02 - Accounting Changes and Errors (Answers)Document2 pagesACCTG 105 Midterm - Quiz No. 02 - Accounting Changes and Errors (Answers)Lucas BantilingNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Dethzaida AsebuqueNo ratings yet

- 5.1 - AUDIT ON RECEIVABLES (Problems)Document10 pages5.1 - AUDIT ON RECEIVABLES (Problems)LorraineMartinNo ratings yet

- 02 Audit of Expenditure and Disbursements Cycle (Cont.)Document4 pages02 Audit of Expenditure and Disbursements Cycle (Cont.)Becky GonzagaNo ratings yet

- Accounting For Special TransactionDocument15 pagesAccounting For Special TransactionRichelle Mea B. PeñaNo ratings yet

- Assessment Current LiabilitiesDocument6 pagesAssessment Current LiabilitiesEdward Glenn BaguiNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Case 1: Control Account and Subsidiary Ledger ReconciliationDocument5 pagesCase 1: Control Account and Subsidiary Ledger Reconciliationkat kaleNo ratings yet

- Concept Map PCDocument4 pagesConcept Map PCkat kaleNo ratings yet

- Case 1: Balungao Company Engaged You To Examine Its Books and Records For TheDocument2 pagesCase 1: Balungao Company Engaged You To Examine Its Books and Records For Thekat kaleNo ratings yet

- Case 1: Audit of Accounts Receivable and Related AccountsDocument6 pagesCase 1: Audit of Accounts Receivable and Related Accountskat kaleNo ratings yet

- Concept Map ECDocument2 pagesConcept Map ECkat kaleNo ratings yet

- Home Office, Branch, and Agency AccountingDocument4 pagesHome Office, Branch, and Agency Accountingkat kaleNo ratings yet

- Stock Acquisition - Date of AcquisitionDocument2 pagesStock Acquisition - Date of Acquisitionkat kaleNo ratings yet

- Partnership Dissolution and LiquidationDocument4 pagesPartnership Dissolution and Liquidationkat kaleNo ratings yet

- Partnership Formation and OperationDocument4 pagesPartnership Formation and Operationkat kaleNo ratings yet

- Links To An External Site.Document1 pageLinks To An External Site.kat kaleNo ratings yet

- Construction ContractsDocument3 pagesConstruction Contractskat kaleNo ratings yet

- Intercompany TransactionsDocument1 pageIntercompany Transactionskat kaleNo ratings yet

- Corporate LiquidationDocument1 pageCorporate Liquidationkat kaleNo ratings yet

- Challenges Faced by Sales ManagerDocument29 pagesChallenges Faced by Sales ManagerniharikkaNo ratings yet

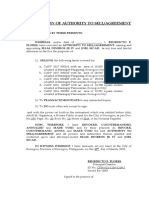

- Revocation of Authority To SellDocument2 pagesRevocation of Authority To SellCyril Oropesa67% (3)

- Dabur Final PPT EDITEDDocument21 pagesDabur Final PPT EDITEDAkshay GadkariNo ratings yet

- Chapter 15: Public RelationsDocument10 pagesChapter 15: Public RelationsAzizSafianNo ratings yet

- Freindenhaus Price QuotationDocument3 pagesFreindenhaus Price QuotationgerrymalgapoNo ratings yet

- International Marketing 2Document7 pagesInternational Marketing 2GunjanNo ratings yet

- Sales Representative Job ResponsibilitiesDocument6 pagesSales Representative Job ResponsibilitiesPopol Benavidez50% (2)

- RetailpricingDocument57 pagesRetailpricingNavpreet Singh RandhawaNo ratings yet

- Acc 305 PDFDocument147 pagesAcc 305 PDFgosaye desalegn100% (3)

- Forecasting The Revenues of The BusinessDocument2 pagesForecasting The Revenues of The Businessveronica relente100% (1)

- Contract For The Sale of GoodsDocument3 pagesContract For The Sale of Goodsdusan4No ratings yet

- Anatomy of Internet Marketing MixDocument5 pagesAnatomy of Internet Marketing MixmgambettaNo ratings yet

- Mi Lifestyle Marketing Pvt. LTDDocument4 pagesMi Lifestyle Marketing Pvt. LTDPrasanta Mondal100% (1)

- Collaborative Planning Forecasting & ReplenishmentDocument27 pagesCollaborative Planning Forecasting & ReplenishmentSandeep SasidharanNo ratings yet

- Good Qualities For BusinessmenDocument36 pagesGood Qualities For BusinessmenPradeepKumarNo ratings yet

- Strategy Formulation and ImplementationDocument26 pagesStrategy Formulation and ImplementationUrvashi Sharma100% (1)

- Strategic ManagementDocument33 pagesStrategic ManagementNaresh KuntiNo ratings yet

- W1 Tom IntroductionDocument61 pagesW1 Tom IntroductionFirmanNo ratings yet

- SD RRB DocumentDocument12 pagesSD RRB DocumentДмитрий Харланов100% (2)

- AL-Maur Company ProfileDocument10 pagesAL-Maur Company Profilegate2iraq100% (2)

- Zamora Realty and Development Corporation VsDocument3 pagesZamora Realty and Development Corporation VsKrizzle de la Peña0% (1)

- Risk and UncertaintyDocument14 pagesRisk and UncertaintySyed FaizanNo ratings yet

- Food AggregatorsDocument3 pagesFood AggregatorsAnany UpadhyayNo ratings yet

- Walgreen Company Rite Aid Corporation: G RoughDocument1 pageWalgreen Company Rite Aid Corporation: G Roughsaad bin sadaqat100% (1)

- Concept of BusinessDocument2 pagesConcept of BusinessHarishYadav100% (1)

- Business 2210 Case Analysis Report-FINALDocument34 pagesBusiness 2210 Case Analysis Report-FINALtamim707100% (3)

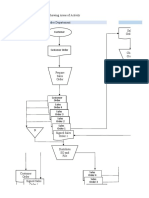

- Flowchart SIADocument5 pagesFlowchart SIAMarsa ArrahmanNo ratings yet

- Tourism in MoldovaDocument1 pageTourism in MoldovaDumitru PlamadealaNo ratings yet

- Bab 4 Barang Publik Hyman PDFDocument29 pagesBab 4 Barang Publik Hyman PDFBarang Hilang MalangNo ratings yet

- Pricing 9.12.17Document31 pagesPricing 9.12.17Kim AmuraoNo ratings yet