You might also like

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Dethzaida AsebuqueNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Kate PaquizNo ratings yet

- Audit of Revenue and Receipts Cycle BA 123 Exercise Set 1: Problem 1: ABC COMPANY (Sales Cutoff Test)Document3 pagesAudit of Revenue and Receipts Cycle BA 123 Exercise Set 1: Problem 1: ABC COMPANY (Sales Cutoff Test)Becky GonzagaNo ratings yet

- 8506 - Installment SalesDocument4 pages8506 - Installment SalesAnonymous iNRMC4mgORNo ratings yet

- AP-200 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document5 pagesAP-200 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Fella GultianoNo ratings yet

- 8506 - Installment Sales - 113910598Document4 pages8506 - Installment Sales - 113910598Ryan CornistaNo ratings yet

- AccountingDocument6 pagesAccountingBlue HourNo ratings yet

- 2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFDocument25 pages2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFMae-shane SagayoNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- Practice Exercise 1.1Document4 pagesPractice Exercise 1.1leshz zynNo ratings yet

- AP Module 01 - Accounting Changes and ErrorsDocument10 pagesAP Module 01 - Accounting Changes and ErrorsjasfNo ratings yet

- Quiz 1. Special Revenue RecognitionDocument6 pagesQuiz 1. Special Revenue RecognitionApolinar Alvarez Jr.No ratings yet

- FSA Tutorial 1Document2 pagesFSA Tutorial 1KHOO TAT SHERN DEXTONNo ratings yet

- AP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document10 pagesAP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Bernadette Panican100% (1)

- May 2020 Error SHE Intangibles Liabilities LeasesDocument14 pagesMay 2020 Error SHE Intangibles Liabilities Leasesiraleigh17No ratings yet

- Chapter-2 Homework MisstatementsDocument4 pagesChapter-2 Homework MisstatementsKenneth Christian WilburNo ratings yet

- Exercises P Class2-2022Document9 pagesExercises P Class2-2022Angel MéndezNo ratings yet

- ReSA CPA Review Batch 41 Audit Problems Weeks 1-3Document4 pagesReSA CPA Review Batch 41 Audit Problems Weeks 1-3Angela AlejandroNo ratings yet

- Net income corrections for 2021Document1 pageNet income corrections for 2021Bella AyabNo ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- Error Correction - ExercisesDocument4 pagesError Correction - ExercisesDe Chavez May Ann M.No ratings yet

- ACT 205 Assignment - Spring 2019-20Document5 pagesACT 205 Assignment - Spring 2019-20Muhammad AhamdNo ratings yet

- Installment ExercisesDocument2 pagesInstallment ExercisesalyssaNo ratings yet

- The Big Picture: Brief ExercisesDocument13 pagesThe Big Picture: Brief ExercisesRacel Agonia0% (1)

- Installment Sales Gross Profit Calculation and Loss on RepossessionDocument2 pagesInstallment Sales Gross Profit Calculation and Loss on Repossessionelsana philipNo ratings yet

- Accruals & Deferrals Errors AuditDocument2 pagesAccruals & Deferrals Errors AuditHaidee Flavier SabidoNo ratings yet

- AP W1 Correction of ErrorsDocument4 pagesAP W1 Correction of ErrorsALYZA ANGELA ORNEDONo ratings yet

- Homework on Receivables and Notes ReceivableDocument4 pagesHomework on Receivables and Notes ReceivableJazehl Joy ValdezNo ratings yet

- Assignment No. 5 Hoba Franchising Joint ArrangementsDocument4 pagesAssignment No. 5 Hoba Franchising Joint ArrangementsJean TatsadoNo ratings yet

- Auditing Problems MidtermDocument20 pagesAuditing Problems MidtermjasfNo ratings yet

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- Nov 19 Q PDFDocument9 pagesNov 19 Q PDFTenywa SalimNo ratings yet

- Diamond Motors installment sales profits analysisDocument4 pagesDiamond Motors installment sales profits analysisGoal Digger Squad VlogNo ratings yet

- Acct 470 Pre Quiz Chapter 4,5,9-12Document28 pagesAcct 470 Pre Quiz Chapter 4,5,9-12karissa.jqasm.0No ratings yet

- Installment SalesDocument4 pagesInstallment Saleskat kaleNo ratings yet

- Answers - Module 2Document4 pagesAnswers - Module 2bhettyna noayNo ratings yet

- QUIZ Correction of ErrorsDocument7 pagesQUIZ Correction of ErrorsJanelleNo ratings yet

- Activity 1b - Current LiabilitiesDocument2 pagesActivity 1b - Current LiabilitiesUchayyaNo ratings yet

- FINALS QUIZ Fin3Document11 pagesFINALS QUIZ Fin3Erika Larinay100% (1)

- FINALS QUIZ Fin3Document11 pagesFINALS QUIZ Fin3Angela MartiresNo ratings yet

- 07 Installment SalesDocument1 page07 Installment SalesGem Yiel33% (3)

- Cambridge International AS & A Level: Accounting 9706/33Document12 pagesCambridge International AS & A Level: Accounting 9706/334ycvrzfjgfNo ratings yet

- Valuation of Firm GoodwillDocument7 pagesValuation of Firm GoodwillTanisha JainNo ratings yet

- Auditing Problem Assignment Lyeca JoieDocument12 pagesAuditing Problem Assignment Lyeca JoieEsse ValdezNo ratings yet

- Installment SalesDocument3 pagesInstallment SalesIryne Kim PalatanNo ratings yet

- November 2020 Professional Exams Financial Accounting ReportDocument20 pagesNovember 2020 Professional Exams Financial Accounting ReportMahediNo ratings yet

- Financial PlanDocument20 pagesFinancial Planzhijaescosio25No ratings yet

- Afar 2 - Installment SalesDocument1 pageAfar 2 - Installment SalesPanda ErarNo ratings yet

- Prae03 HoDocument3 pagesPrae03 HoDiane MagnayeNo ratings yet

- Cash and Accrual Basis - ExercisesDocument2 pagesCash and Accrual Basis - ExercisesTrisha Mae AlburoNo ratings yet

- Chapter 3 Receivables Exercises Answer Guide Summer AY2122 PDFDocument11 pagesChapter 3 Receivables Exercises Answer Guide Summer AY2122 PDFwavyastroNo ratings yet

- Installment Sales Multiple QuestionsDocument36 pagesInstallment Sales Multiple QuestionsTrixie CapisosNo ratings yet

- Instalment DISDocument4 pagesInstalment DISRenelyn David100% (1)

- Installment-Sales-Supplementary-Problems & NotesDocument3 pagesInstallment-Sales-Supplementary-Problems & NotesAlliah Mae ArbastoNo ratings yet

- ENT503M MidtermQuestionnaireDocument7 pagesENT503M MidtermQuestionnaireNevan NovaNo ratings yet

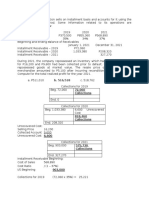

- B. 516,518 72,060 CollectionsDocument2 pagesB. 516,518 72,060 CollectionsMichelle Galapon LagunaNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- DividendsDocument3 pagesDividendsBecky GonzagaNo ratings yet

- BA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Document2 pagesBA 116 / 1 Semester, AY 2013-2014 Activity-Based Costing (ABC) Systems: Handout #7Becky GonzagaNo ratings yet

- 00 Quick Notes On Income TaxDocument11 pages00 Quick Notes On Income TaxBecky GonzagaNo ratings yet

- 00 Quick Notes On Income TaxDocument11 pages00 Quick Notes On Income TaxBecky GonzagaNo ratings yet

- University Job Fair 2023: Partnership ProposalDocument17 pagesUniversity Job Fair 2023: Partnership ProposalBecky GonzagaNo ratings yet

- Brandstorm 2023 Mission DocumentDocument23 pagesBrandstorm 2023 Mission DocumentBecky GonzagaNo ratings yet

- BA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Document51 pagesBA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Becky GonzagaNo ratings yet

- Audit of Inventories and Trade Payables BA 123 Exercise Set BDocument6 pagesAudit of Inventories and Trade Payables BA 123 Exercise Set BBecky GonzagaNo ratings yet

- Audit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Document10 pagesAudit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Becky GonzagaNo ratings yet

- 03.5 Correction On Problem 3Document6 pages03.5 Correction On Problem 3Becky GonzagaNo ratings yet

- BA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Document42 pagesBA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Becky GonzagaNo ratings yet

- 00 Quick Notes - Cash and Cash Equivalents PDFDocument6 pages00 Quick Notes - Cash and Cash Equivalents PDFBecky GonzagaNo ratings yet

- BA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Document146 pagesBA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Becky GonzagaNo ratings yet

- 00 Quick Notes - Revenue and Receipt Cycle PDFDocument5 pages00 Quick Notes - Revenue and Receipt Cycle PDFBecky GonzagaNo ratings yet

- DocxDocument5 pagesDocxBecky GonzagaNo ratings yet

- CSSC Donation Drive Helps Science StudentsDocument7 pagesCSSC Donation Drive Helps Science StudentsBecky GonzagaNo ratings yet

- Audit Expenditure and Disbursement CycleDocument4 pagesAudit Expenditure and Disbursement CycleBecky GonzagaNo ratings yet

- (Make/Buy, Drop/Continue, Special Order, Sell at Split-Off/process FurtherDocument17 pages(Make/Buy, Drop/Continue, Special Order, Sell at Split-Off/process FurtherBecky GonzagaNo ratings yet

- IAS 21: Effects of Foreign Exchange RatesDocument10 pagesIAS 21: Effects of Foreign Exchange RatesBecky GonzagaNo ratings yet

- Audit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Document10 pagesAudit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Becky GonzagaNo ratings yet

- 02a Creating - An - Investment - Policy - StatementDocument16 pages02a Creating - An - Investment - Policy - StatementBecky GonzagaNo ratings yet

- Exercises On Foreign Exchange Translation - Foreign To Functional (Questionnaire)Document3 pagesExercises On Foreign Exchange Translation - Foreign To Functional (Questionnaire)Becky GonzagaNo ratings yet

- CSupport 2.0 Partnership Letter For OrgsDocument4 pagesCSupport 2.0 Partnership Letter For OrgsBecky GonzagaNo ratings yet

- TechEx 2021 Partnership ProposalDocument9 pagesTechEx 2021 Partnership ProposalBecky GonzagaNo ratings yet

- Quiz Accounting For VHWO Ver. 7Document9 pagesQuiz Accounting For VHWO Ver. 7Becky GonzagaNo ratings yet

- Exercises On Foreign Exchange Translation - Functional To Presentation (Questionnaire)Document1 pageExercises On Foreign Exchange Translation - Functional To Presentation (Questionnaire)Becky GonzagaNo ratings yet

- Standard Costs and Variance AnalysisDocument14 pagesStandard Costs and Variance Analysisboen jayme0% (1)

- Forrest Oh VarianceDocument3 pagesForrest Oh VarianceBecky GonzagaNo ratings yet

- GLO Integrated Report 2019Document208 pagesGLO Integrated Report 2019Zervin LimNo ratings yet

- File 20230404153921Document66 pagesFile 20230404153921Sarah RostinNo ratings yet

- GX Global Powers of Luxury Goods 2023Document78 pagesGX Global Powers of Luxury Goods 2023xen101No ratings yet

- S&P 500 Index Etf: HorizonsDocument4 pagesS&P 500 Index Etf: HorizonsChrisNo ratings yet

- Emergency Response Plan Final NotesDocument6 pagesEmergency Response Plan Final Notesviren thakkarNo ratings yet

- B6 - Complete The Text and Reading ComprehensionDocument10 pagesB6 - Complete The Text and Reading ComprehensionAn NgoNo ratings yet

- Startup Checklist for Your BusinessDocument3 pagesStartup Checklist for Your BusinessAJAY SHINDENo ratings yet

- Creating Strategic Advantages for NespressoDocument14 pagesCreating Strategic Advantages for NespressoAnkitpandya23No ratings yet

- MCQ Monopolistic & Oligopolistic Competition PDFDocument5 pagesMCQ Monopolistic & Oligopolistic Competition PDFAJAY KUMAR SAHUNo ratings yet

- FM NumericalDocument3 pagesFM NumericalNitin KumarNo ratings yet

- RWDocument29 pagesRWPramod DhaigudeNo ratings yet

- Unit 6 7 Lesson Guide in Tourism Hospitality MarketingDocument36 pagesUnit 6 7 Lesson Guide in Tourism Hospitality MarketingSalvacion CalimpayNo ratings yet

- 1 - 20.09.2018 - Corriogendum 1aDocument1 page1 - 20.09.2018 - Corriogendum 1achtrpNo ratings yet

- Proforma Balance Sheet with Financing OptionsDocument6 pagesProforma Balance Sheet with Financing OptionsJohn Richard Bonilla100% (4)

- Aurobindo Pharma - Investor Presentation - INR - Sep 22 1Document30 pagesAurobindo Pharma - Investor Presentation - INR - Sep 22 1Hari KiranNo ratings yet

- Grade 10Document115 pagesGrade 10Manuelo Vangie100% (1)

- Nature and Elements of LeadershipDocument45 pagesNature and Elements of LeadershipMARIA SHIELA LEDESMANo ratings yet

- Case Analysis: Bain & Company's IT Practice: Problem StatementDocument1 pageCase Analysis: Bain & Company's IT Practice: Problem StatementVishal SairamNo ratings yet

- LetterDocument3 pagesLetterSandy MageshNo ratings yet

- Customs Valuation SystemDocument3 pagesCustoms Valuation SystemJehiel CastilloNo ratings yet

- Busines EthicsDocument8 pagesBusines EthicsjinkyNo ratings yet

- CRM in ICICIDocument17 pagesCRM in ICICIAkshay keerNo ratings yet

- Car Policy: Salient FeaturesDocument2 pagesCar Policy: Salient FeaturesZahid Shaikh100% (1)

- Clow IAPMC9 PPT 13Document46 pagesClow IAPMC9 PPT 13rana 123No ratings yet

- Solving Real-Life Problems Involving FunctionsDocument31 pagesSolving Real-Life Problems Involving FunctionsRenmel JosephNo ratings yet

- Department of Collegiate and Technical Education: Government Polytechnic, KarwarDocument41 pagesDepartment of Collegiate and Technical Education: Government Polytechnic, Karwarmisba shaikhNo ratings yet

- Problems at SKS ManufacturingDocument2 pagesProblems at SKS ManufacturingVanshGuptaNo ratings yet

- Term Sheet for Potential Equity Investment in TextcentricDocument6 pagesTerm Sheet for Potential Equity Investment in TextcentricRecklessgod100% (1)

- SamplingDocument16 pagesSamplingenam professorNo ratings yet

- SBI Seeks Insolvency of Western Refrigeration over GuaranteeDocument16 pagesSBI Seeks Insolvency of Western Refrigeration over Guaranteeveer vikramNo ratings yet

- HRM - Term Paper - Mohammad SujonDocument24 pagesHRM - Term Paper - Mohammad Sujonishapnil 63No ratings yet