You might also like

- FAR Vol 2 Chapter 16 18Document14 pagesFAR Vol 2 Chapter 16 18Allen Fey De Jesus100% (1)

- Accounting For Income Tax SeatworkDocument3 pagesAccounting For Income Tax SeatworkKenneth TorresNo ratings yet

- Audit of Non-current Liabilities ProblemsDocument2 pagesAudit of Non-current Liabilities ProblemsbangtansonyeondaNo ratings yet

- Accounting For Taxes 6Document7 pagesAccounting For Taxes 6charlene kate bunaoNo ratings yet

- CHAPTER-22-DEFERRED-TAX-ASSET-AND-LIABILITYDocument8 pagesCHAPTER-22-DEFERRED-TAX-ASSET-AND-LIABILITYCheesca Macabanti - 12 Euclid-Digital ModularNo ratings yet

- Net income corrections for 2021Document1 pageNet income corrections for 2021Bella AyabNo ratings yet

- Accounting for Income Taxes QuizDocument3 pagesAccounting for Income Taxes QuizAngelica manaois100% (2)

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument171 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionRengeline LucasNo ratings yet

- AccountingDocument6 pagesAccountingBlue HourNo ratings yet

- Income Taxes Batch 4 (Repaired)Document10 pagesIncome Taxes Batch 4 (Repaired)Lealyn Martin BaculoNo ratings yet

- IAS 12 Income Tax AccountingDocument6 pagesIAS 12 Income Tax AccountingAnn Christine C. Chua100% (2)

- Chapter 18Document12 pagesChapter 18ks1043210No ratings yet

- Assignment 4Document2 pagesAssignment 4Nate LoNo ratings yet

- May 2020 Error SHE Intangibles Liabilities LeasesDocument14 pagesMay 2020 Error SHE Intangibles Liabilities Leasesiraleigh17No ratings yet

- Assignment No. 5 Hoba Franchising Joint ArrangementsDocument4 pagesAssignment No. 5 Hoba Franchising Joint ArrangementsJean TatsadoNo ratings yet

- W5 - AS2 - Deferred TaxesDocument2 pagesW5 - AS2 - Deferred TaxesJere Mae MarananNo ratings yet

- AUDITING-Adjusting Entries-Correction of ErrorsDocument10 pagesAUDITING-Adjusting Entries-Correction of ErrorsJamhel MarquezNo ratings yet

- Installment SalesDocument4 pagesInstallment Saleskat kaleNo ratings yet

- Acct 470 Pre Quiz Chapter 4,5,9-12Document28 pagesAcct 470 Pre Quiz Chapter 4,5,9-12karissa.jqasm.0No ratings yet

- FAR05 - Accounting For Income and Deferred TaxesDocument4 pagesFAR05 - Accounting For Income and Deferred TaxesDisguised owlNo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Income Tax Expense and Deferred Tax Asset & Liability CalculationsDocument3 pagesIncome Tax Expense and Deferred Tax Asset & Liability Calculationskrisha millo0% (1)

- MSU-CBA Accounting for Income TaxDocument7 pagesMSU-CBA Accounting for Income TaxJayr BV100% (1)

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Kate PaquizNo ratings yet

- Classroom Exercise - Unit 1-1Document2 pagesClassroom Exercise - Unit 1-1Hannah Jane ToribioNo ratings yet

- Chap. 19Document75 pagesChap. 19Nguyễn Lê ThủyNo ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- HW On ReceivablesDocument4 pagesHW On ReceivablesGian Carlo RamonesNo ratings yet

- Audit of Special Liabilities 1Document4 pagesAudit of Special Liabilities 1kimnicoledelacruz05No ratings yet

- Accounting For Income Tax QuizDocument5 pagesAccounting For Income Tax QuizTorico BryanNo ratings yet

- Illustrative Examples - Accounting For Income TaxDocument3 pagesIllustrative Examples - Accounting For Income Taxr3rvpaudit.nfjpia2324supaccNo ratings yet

- Far-Single Entry PDFDocument7 pagesFar-Single Entry PDFJanica June FiscalNo ratings yet

- AP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document4 pagesAP-100 (Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Dethzaida AsebuqueNo ratings yet

- Exercises P Class2-2022Document9 pagesExercises P Class2-2022Angel MéndezNo ratings yet

- Problem Quiz On IntermediateDocument3 pagesProblem Quiz On IntermediateReginald ValenciaNo ratings yet

- QUIZ Correction of ErrorsDocument7 pagesQUIZ Correction of ErrorsJanelleNo ratings yet

- Week 6 - ch19Document55 pagesWeek 6 - ch19bafsvideo4No ratings yet

- Additional Input FlyByU AGDocument2 pagesAdditional Input FlyByU AGChiara AnindaNo ratings yet

- Calculate Income Tax Expense and Deferred TaxDocument10 pagesCalculate Income Tax Expense and Deferred Taxlana del reyNo ratings yet

- UntitledDocument4 pagesUntitledgigi meiNo ratings yet

- FAR PreBoard (1) CPAR BATCH90Document18 pagesFAR PreBoard (1) CPAR BATCH90Bella ChoiNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument9 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionJay-L TanNo ratings yet

- Practice exercises accrual cash basis single entryDocument3 pagesPractice exercises accrual cash basis single entryxylynn myka cabanatanNo ratings yet

- CPA Review School Philippines Financial Accounting Preboard ExamDocument14 pagesCPA Review School Philippines Financial Accounting Preboard Examomer 2 gerdNo ratings yet

- Philippine School of Business Administration Financial Accounting and Reporting Problems Final ExamDocument11 pagesPhilippine School of Business Administration Financial Accounting and Reporting Problems Final ExamNicole Aragon0% (1)

- Cpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesDocument15 pagesCpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesSophia PerezNo ratings yet

- Accounting For Taxes Employee BenefitsDocument6 pagesAccounting For Taxes Employee BenefitsBess Tuico MasanqueNo ratings yet

- (EN) Problem Mojakoe AK1Document11 pages(EN) Problem Mojakoe AK1gebbyNo ratings yet

- Homework 5 - Current Liabilities - RevisedDocument3 pagesHomework 5 - Current Liabilities - RevisedalvarezxpatriciaNo ratings yet

- Domondon Acctg 3 Prelim ExamDocument3 pagesDomondon Acctg 3 Prelim ExamPrince Anton DomondonNo ratings yet

- Principles of Taxation Key ConceptsDocument2 pagesPrinciples of Taxation Key ConceptsSharif MahmudNo ratings yet

- Error Correction - ExercisesDocument4 pagesError Correction - ExercisesDe Chavez May Ann M.No ratings yet

- Audit of Long-Term LiabilitiesDocument3 pagesAudit of Long-Term LiabilitiesJhaybie San BuenaventuraNo ratings yet

- Income Taxes (Module 8)Document8 pagesIncome Taxes (Module 8)Paulo Emmanuel SantosNo ratings yet

- Reviewer FinalsDocument23 pagesReviewer FinalsMark AloysiusNo ratings yet

- 5.1 - AUDIT ON RECEIVABLES (Problems)Document10 pages5.1 - AUDIT ON RECEIVABLES (Problems)LorraineMartinNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- The Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesFrom EverandThe Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesNo ratings yet

- Finance LeaseDocument1 pageFinance Leasealcazar rtuNo ratings yet

- Legal TheoriesDocument3 pagesLegal Theoriesalcazar rtuNo ratings yet

- GR No. 122653Document1 pageGR No. 122653alcazar rtuNo ratings yet

- Agricultural Extension Test AnswersDocument13 pagesAgricultural Extension Test Answersalcazar rtuNo ratings yet

- Nil ExamDocument2 pagesNil Examalcazar rtuNo ratings yet

- Labour ExamDocument1 pageLabour Examalcazar rtuNo ratings yet

- Labour QuizDocument1 pageLabour Quizalcazar rtuNo ratings yet

- Cayetano vs. MonsodDocument2 pagesCayetano vs. Monsodalcazar rtuNo ratings yet

- Analysis of Equity Transactions and Share Capital CalculationsDocument3 pagesAnalysis of Equity Transactions and Share Capital Calculationsalcazar rtuNo ratings yet

- Ulep vs. Legal ClinicDocument3 pagesUlep vs. Legal Clinicalcazar rtuNo ratings yet

- Cipriano Vs Comelec Case DigestDocument4 pagesCipriano Vs Comelec Case Digestalcazar rtuNo ratings yet

- Legal PhilosophersDocument6 pagesLegal Philosophersalcazar rtuNo ratings yet

- GR No. 85519Document2 pagesGR No. 85519alcazar rtuNo ratings yet

- Cruz VS MinaDocument2 pagesCruz VS Minaalcazar rtuNo ratings yet

- MERCADO VsDocument3 pagesMERCADO Vsalcazar rtuNo ratings yet

- Assignment 2Document4 pagesAssignment 2alcazar rtuNo ratings yet

- Lonzanida Vs COMELECDocument1 pageLonzanida Vs COMELECalcazar rtuNo ratings yet

- In Re ArgosinoDocument2 pagesIn Re ArgosinodinvNo ratings yet

- BASIC ACCOUNTING-Controlling Accounts Quiz No. 2Document2 pagesBASIC ACCOUNTING-Controlling Accounts Quiz No. 2alcazar rtuNo ratings yet

- Labor Midterm Digest CasesDocument43 pagesLabor Midterm Digest Casesalcazar rtuNo ratings yet

- Alawi VS AlauyaDocument1 pageAlawi VS Alauyaalcazar rtuNo ratings yet

- TAXATION - INTRODUCTION ExeDocument2 pagesTAXATION - INTRODUCTION Exealcazar rtuNo ratings yet

- TAXATION PRINCIPLES QUIZDocument8 pagesTAXATION PRINCIPLES QUIZalcazar rtuNo ratings yet

- BASIC ACCOUNTING-Controlling Accounts Lec. 3Document1 pageBASIC ACCOUNTING-Controlling Accounts Lec. 3alcazar rtuNo ratings yet

- TAXATION - INTRODUCTION ExeDocument2 pagesTAXATION - INTRODUCTION Exealcazar rtuNo ratings yet

- Accounting For Warranties and PremiumsDocument8 pagesAccounting For Warranties and Premiumsalcazar rtuNo ratings yet

- BASIC ACCOUNTING-Controlling Accounts ExeDocument1 pageBASIC ACCOUNTING-Controlling Accounts Exealcazar rtuNo ratings yet

- TAXATION PRINCIPLES QUIZDocument8 pagesTAXATION PRINCIPLES QUIZalcazar rtuNo ratings yet

- Classification of DebtsDocument7 pagesClassification of Debtsalcazar rtuNo ratings yet

- Global Recession and RecoveryDocument54 pagesGlobal Recession and RecoveryPaven RajNo ratings yet

- A Reformulation: Intel CorporationDocument15 pagesA Reformulation: Intel Corporationmnhasan150No ratings yet

- Islamic Modes of Car FinancingDocument4 pagesIslamic Modes of Car FinancingMajid Shahzaad KharralNo ratings yet

- Strides Arcolab Limited's Dividend Pay-Out Decision - Final2Document21 pagesStrides Arcolab Limited's Dividend Pay-Out Decision - Final2Lucas Tai100% (1)

- Fundamental Analysis On Max Life InsuranceDocument16 pagesFundamental Analysis On Max Life InsuranceSimon StilerNo ratings yet

- Optional Riders Provide Critical Illness and Disability CoverageDocument2 pagesOptional Riders Provide Critical Illness and Disability Coverageemaraty khNo ratings yet

- ProblemsDocument368 pagesProblemsAnne EstrellaNo ratings yet

- Shareholders' Equity: PROBLEM 1: Prepare Journal Entries To Record Each of The FollowingDocument14 pagesShareholders' Equity: PROBLEM 1: Prepare Journal Entries To Record Each of The FollowingAccounting LayfNo ratings yet

- Liquidation Process ExplainedDocument7 pagesLiquidation Process ExplainedAhmad KhanNo ratings yet

- Iligan Institute of Technology: Mindanao State University Iligan CityDocument4 pagesIligan Institute of Technology: Mindanao State University Iligan Citylairah.mananNo ratings yet

- Rekening Koran Agustus 2023Document2 pagesRekening Koran Agustus 2023Ade AlfianNo ratings yet

- Trial Balance Ud Mudah HasilDocument1 pageTrial Balance Ud Mudah HasilSani SausanNo ratings yet

- Policybazaar: Indian Institute of Management RaipurDocument7 pagesPolicybazaar: Indian Institute of Management RaipurKaran SardaNo ratings yet

- Ca Rohit Chola: ProfileDocument2 pagesCa Rohit Chola: ProfileThe Cultural CommitteeNo ratings yet

- Virtual CFO Services for StartupsDocument15 pagesVirtual CFO Services for StartupsKarun GuptaNo ratings yet

- Chapter 1Document20 pagesChapter 1Adam MilakaraNo ratings yet

- Lesson 2 - Activity FSA2Document4 pagesLesson 2 - Activity FSA2jeffrey galanzaNo ratings yet

- NFJPIA - Mockboard 2011 - MAS PDFDocument7 pagesNFJPIA - Mockboard 2011 - MAS PDFAbigail Faye RoxasNo ratings yet

- 7110 w15 Ms 22 PDFDocument9 pages7110 w15 Ms 22 PDFRachel RAMSAMYNo ratings yet

- Saudi Airlines Catering EnglishDocument174 pagesSaudi Airlines Catering EnglishUltimo GuerreroNo ratings yet

- Accounting Cycle HacksDocument14 pagesAccounting Cycle HacksAnonymous mnAAXLkYQCNo ratings yet

- PRTC 1stPB - 05.22 Sol FARDocument7 pagesPRTC 1stPB - 05.22 Sol FARCiatto SpotifyNo ratings yet

- Bill of Exchange MaybankDocument3 pagesBill of Exchange MaybankBuayaz GamingNo ratings yet

- Partnership Formation GuideDocument5 pagesPartnership Formation GuideABCNo ratings yet

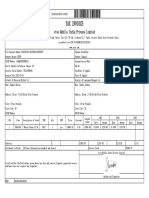

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- Lululemon Financial AnalysisDocument14 pagesLululemon Financial Analysismrsammy100% (1)

- Material 20191017125124 Indonesian Mortality Table IV v20191017Document15 pagesMaterial 20191017125124 Indonesian Mortality Table IV v20191017Alank KurniawanNo ratings yet

- A Study On Compariion of Online With Offline Trading in CommoditiesDocument56 pagesA Study On Compariion of Online With Offline Trading in CommoditiesN.MUTHUKUMARAN100% (1)

- Chapter 2 The Accounting EquationDocument15 pagesChapter 2 The Accounting EquationDahlia Fernandez Bt Mohd Farid FernandezNo ratings yet

- Access To Finance For Smes: World Bank, Ghana OfficeDocument11 pagesAccess To Finance For Smes: World Bank, Ghana OfficeReddahi BrahimNo ratings yet