You might also like

- Chapter 5 PPT (AIS - James Hall)Document10 pagesChapter 5 PPT (AIS - James Hall)Nur-aima Mortaba50% (2)

- The Expenditure Cycle Part I: Purchases and Cash Disbursements ProceduresDocument28 pagesThe Expenditure Cycle Part I: Purchases and Cash Disbursements ProceduresNicah AcojonNo ratings yet

- Chapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument7 pagesChapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresAstxilNo ratings yet

- Chapter 5Document5 pagesChapter 5Itsme ColladoNo ratings yet

- Accounting Information System: Expenditure CycleDocument11 pagesAccounting Information System: Expenditure CycleSophia Marie BesorioNo ratings yet

- Chapter 4Document29 pagesChapter 4Genanew AbebeNo ratings yet

- Chapter 5Document6 pagesChapter 5Jane LubangNo ratings yet

- Ais Chapter 5 ReviewerDocument9 pagesAis Chapter 5 ReviewerAngela Erish CastroNo ratings yet

- Chapter 5Document26 pagesChapter 5Pinky RoseNo ratings yet

- Module 05 - Accounting and Information SystemsDocument6 pagesModule 05 - Accounting and Information SystemsKaye BabadillaNo ratings yet

- PDF Chapter 5 The Expenditure Cycle Part I Summary - CompressDocument5 pagesPDF Chapter 5 The Expenditure Cycle Part I Summary - CompressCassiopeia Cashmere GodheidNo ratings yet

- Term Paper On PPPPPPPPPDocument17 pagesTerm Paper On PPPPPPPPPSharif KhanNo ratings yet

- Script AISDocument4 pagesScript AISbrennaNo ratings yet

- Sia - Uas - 2Document29 pagesSia - Uas - 2Cornelita Tesalonika R. K.No ratings yet

- Chapter 5 (Cando & Lascona)Document51 pagesChapter 5 (Cando & Lascona)brennaNo ratings yet

- Ch-4 Auditing Principles and Practices-IIDocument26 pagesCh-4 Auditing Principles and Practices-IIfiraolmosisabonkeNo ratings yet

- I Am Reign Gagalac: Hello!Document34 pagesI Am Reign Gagalac: Hello!Rundhille AndalloNo ratings yet

- Accounting Information SystemDocument21 pagesAccounting Information SystemSharif KhanNo ratings yet

- MODULE 05 EXPENDITURE CYCLE COMPUTER-BASED PURCHASES and CASH DISBURSEMENTS APPLICATIONSDocument8 pagesMODULE 05 EXPENDITURE CYCLE COMPUTER-BASED PURCHASES and CASH DISBURSEMENTS APPLICATIONSRed ReyesNo ratings yet

- The Expenditure Cycle: Purchasing To Cash Disbursements: Discussion QuestionsDocument5 pagesThe Expenditure Cycle: Purchasing To Cash Disbursements: Discussion QuestionsMayang SariNo ratings yet

- Chapter 17 - Audit of Acquisition and Payment CycleDocument8 pagesChapter 17 - Audit of Acquisition and Payment CycleRaymond GuillartesNo ratings yet

- Week 13 Exercise With AnswersDocument10 pagesWeek 13 Exercise With Answersmaria fernNo ratings yet

- Bsa201 CH05 QuizDocument3 pagesBsa201 CH05 QuizNicah AcojonNo ratings yet

- Accounting Information Systems, 6: Edition James A. HallDocument41 pagesAccounting Information Systems, 6: Edition James A. HallLaezelie SorianoNo ratings yet

- Accounting Information Systems, 6: Edition James A. HallDocument40 pagesAccounting Information Systems, 6: Edition James A. HallDianne NolascoNo ratings yet

- BP070 UcilDocument43 pagesBP070 UcilSrikanth PeriNo ratings yet

- Case Study - Bell StudioDocument19 pagesCase Study - Bell StudiosheetalsharmaNo ratings yet

- Jawaban SIDocument8 pagesJawaban SIfhadli kunNo ratings yet

- The Expenditure Cycle: I. Purchasing System A. Monitor Inventory Records (Warehouse)Document5 pagesThe Expenditure Cycle: I. Purchasing System A. Monitor Inventory Records (Warehouse)judel ArielNo ratings yet

- Chapter 5Document8 pagesChapter 5Christine Joy OriginalNo ratings yet

- Chapter 5 AIS PDFDocument4 pagesChapter 5 AIS PDFAnne Rose EncinaNo ratings yet

- Lesson H - 1 Ch10 Exp. Cycle Act. Tech.Document57 pagesLesson H - 1 Ch10 Exp. Cycle Act. Tech.Blacky PinkyNo ratings yet

- Ais Charter 5 ReviewerDocument9 pagesAis Charter 5 ReviewerAngela Erish CastroNo ratings yet

- The Expenditure Cycle: Part I: Purchases and Cash Disbursements ProceduresDocument24 pagesThe Expenditure Cycle: Part I: Purchases and Cash Disbursements ProceduresNAVISTA DITA FAIRUZINo ratings yet

- Chapter 5 Summary (The Expenditure Cycle Part I)Document11 pagesChapter 5 Summary (The Expenditure Cycle Part I)Janica GaynorNo ratings yet

- Expenditure CycleDocument31 pagesExpenditure CyclebernadetteNo ratings yet

- Chapter Test - Expenditure CycleDocument4 pagesChapter Test - Expenditure CycleFaith Reyna TanNo ratings yet

- P2P Report-1Document7 pagesP2P Report-1Keerthana KarthiNo ratings yet

- AIS Reviewer AIS Reviewer: Accountancy (The National Teachers College) Accountancy (The National Teachers College)Document13 pagesAIS Reviewer AIS Reviewer: Accountancy (The National Teachers College) Accountancy (The National Teachers College)Aldwin CalambaNo ratings yet

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocument39 pagesKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511No ratings yet

- Chapter FiveDocument58 pagesChapter Fivehasan jabrNo ratings yet

- Chapter 5 Expenditure Cycle Part 1Document33 pagesChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- Chapter 10 SummaryDocument12 pagesChapter 10 SummaryWendelyn TutorNo ratings yet

- Chapter 5 The Expenditure Cycle Part I SummaryDocument10 pagesChapter 5 The Expenditure Cycle Part I Summary0nionrings100% (2)

- EB - Romney - AIS13wm 405 440 31 36Document6 pagesEB - Romney - AIS13wm 405 440 31 36Mayang SariNo ratings yet

- Reviewer 5Document14 pagesReviewer 5Cyrene CruzNo ratings yet

- Ais VB2K242 23d2acc50701401 C12 N09Document12 pagesAis VB2K242 23d2acc50701401 C12 N09Quỳnh Vy ThúyNo ratings yet

- Lecture 9Document33 pagesLecture 9lawlokyiNo ratings yet

- Procurement Processes: EGS 5622 Enterprise Systems Integration Spring, 2018Document42 pagesProcurement Processes: EGS 5622 Enterprise Systems Integration Spring, 2018nbhaskar bhaskarNo ratings yet

- The Expenditure Cycle Part 1Document18 pagesThe Expenditure Cycle Part 1Herman BlomNo ratings yet

- PDFDocument22 pagesPDFJoy Dhemple LambacoNo ratings yet

- Flowchart RevenueDocument45 pagesFlowchart RevenueRezki PerdanaNo ratings yet

- Chapter 5-MCQDocument1 pageChapter 5-MCQHads LunaNo ratings yet

- 4 The Revenue CycleDocument23 pages4 The Revenue CycleWinoah HubaldeNo ratings yet

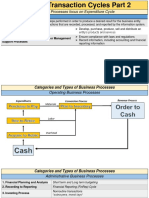

- AT 06-07 Transaction Cycles Part 2Document12 pagesAT 06-07 Transaction Cycles Part 2EeuhNo ratings yet

- Chap. 9 Cis Auditing The Revenue CycleDocument68 pagesChap. 9 Cis Auditing The Revenue CycleSergio, JesharelleNo ratings yet

- Audit II Unit IV-VDocument51 pagesAudit II Unit IV-VGena AlisuuNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Bookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingFrom EverandBookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingRating: 4 out of 5 stars4/5 (2)

- HBO - Module 2 Lesson 2Document7 pagesHBO - Module 2 Lesson 2Reviewers KoNo ratings yet

- International Business and Trade - Module 3Document6 pagesInternational Business and Trade - Module 3Reviewers KoNo ratings yet

- International Business and Trade - Module 2Document9 pagesInternational Business and Trade - Module 2Reviewers KoNo ratings yet

- HBO - Module 1 Lesson 2Document12 pagesHBO - Module 1 Lesson 2Reviewers KoNo ratings yet

- HBO - Module 1 Lesson 1Document10 pagesHBO - Module 1 Lesson 1Reviewers KoNo ratings yet

- International Business and Trade - Module 1Document7 pagesInternational Business and Trade - Module 1Reviewers KoNo ratings yet

- International Business and Trade - Module 1Document7 pagesInternational Business and Trade - Module 1Reviewers KoNo ratings yet

- GBERMIC - Code of Ethics For Professional Accountants Part ADocument5 pagesGBERMIC - Code of Ethics For Professional Accountants Part AReviewers KoNo ratings yet

- International Business and Trade - Module 2Document9 pagesInternational Business and Trade - Module 2Reviewers KoNo ratings yet

- International Business and Trade - Module 3Document6 pagesInternational Business and Trade - Module 3Reviewers KoNo ratings yet

- Introduction To Professional Values, Ethics, and Attitude Part 1Document2 pagesIntroduction To Professional Values, Ethics, and Attitude Part 1Reviewers KoNo ratings yet

- GBERMIC - Common Tools For Ethical Decision MakingDocument5 pagesGBERMIC - Common Tools For Ethical Decision MakingReviewers KoNo ratings yet

- GBERMIC - ChallengesDocument3 pagesGBERMIC - ChallengesReviewers KoNo ratings yet

- GBERMIC - Call To DevelopmentDocument2 pagesGBERMIC - Call To DevelopmentReviewers KoNo ratings yet

- AIS Chapter 4 Revenue CycleDocument8 pagesAIS Chapter 4 Revenue CycleReviewers KoNo ratings yet

- Chapter 5 - Self TestDocument2 pagesChapter 5 - Self TestReviewers KoNo ratings yet

- AIS Expenditure Cycle Self TestDocument2 pagesAIS Expenditure Cycle Self TestReviewers KoNo ratings yet

- Chapter 5 - Expenditure CycleDocument10 pagesChapter 5 - Expenditure CycleReviewers KoNo ratings yet

- Chapter 5 - Self TestDocument2 pagesChapter 5 - Self TestReviewers KoNo ratings yet

- Chapter 4 Self TestDocument3 pagesChapter 4 Self TestReviewers KoNo ratings yet

- AIS Chapter 4 Revenue CycleDocument8 pagesAIS Chapter 4 Revenue CycleReviewers KoNo ratings yet

- Chapter 4 Self TestDocument3 pagesChapter 4 Self TestReviewers KoNo ratings yet

- AIS Expenditure Cycle Self TestDocument2 pagesAIS Expenditure Cycle Self TestReviewers KoNo ratings yet

- New VLSIDocument2 pagesNew VLSIRanjit KumarNo ratings yet

- AFAR Problems PrelimDocument11 pagesAFAR Problems PrelimLian Garl100% (8)

- Germany's Three-Pillar Banking SystemDocument7 pagesGermany's Three-Pillar Banking Systemmladen_nbNo ratings yet

- E14r50p01 800 MhaDocument4 pagesE14r50p01 800 Mha'Theodora GeorgianaNo ratings yet

- LaMOT Rupture DiscsDocument20 pagesLaMOT Rupture Discshlrich99No ratings yet

- Wheel CylindersDocument2 pagesWheel Cylindersparahu ariefNo ratings yet

- Future Generation Computer SystemsDocument18 pagesFuture Generation Computer SystemsEkoNo ratings yet

- PFMEA Reference Card PDFDocument2 pagesPFMEA Reference Card PDFRajesh Yadav100% (5)

- CERES News Digest - Week 11, Vol.4, March 31-April 4Document6 pagesCERES News Digest - Week 11, Vol.4, March 31-April 4Center for Eurasian, Russian and East European StudiesNo ratings yet

- Lab 1Document8 pagesLab 1Нурболат ТаласбайNo ratings yet

- UntitledDocument6 pagesUntitledCoky IrcanNo ratings yet

- Firmware Upgrade To SP3 From SP2: 1. Download Necessary Drivers For The OMNIKEY 5427 CKDocument6 pagesFirmware Upgrade To SP3 From SP2: 1. Download Necessary Drivers For The OMNIKEY 5427 CKFilip Andru MorNo ratings yet

- CIVREV!!!!Document5 pagesCIVREV!!!!aypod100% (1)

- Suggested Answers Spring 2015 Examinations 1 of 8: Strategic Management Accounting - Semester-6Document8 pagesSuggested Answers Spring 2015 Examinations 1 of 8: Strategic Management Accounting - Semester-6Abdul BasitNo ratings yet

- Sparse ArrayDocument2 pagesSparse ArrayzulkoNo ratings yet

- CH 2 How LAN and WAN Communications WorkDocument60 pagesCH 2 How LAN and WAN Communications WorkBeans GaldsNo ratings yet

- LS Series Hand Crimping ToolsDocument4 pagesLS Series Hand Crimping ToolsbaolifengNo ratings yet

- LG+32LX330C Ga LG5CBDocument55 pagesLG+32LX330C Ga LG5CBjampcarlosNo ratings yet

- New York State - NclexDocument5 pagesNew York State - NclexBia KriaNo ratings yet

- KFF in OAF Page-GyanDocument4 pagesKFF in OAF Page-Gyangyan darpanNo ratings yet

- Analysis and Design of Foundation of ROB at LC-9 Between Naroda and Dabhoda Station On Ahmedabad-Himmatnagar RoadDocument10 pagesAnalysis and Design of Foundation of ROB at LC-9 Between Naroda and Dabhoda Station On Ahmedabad-Himmatnagar RoadmahakNo ratings yet

- Guglielmo 2000 DiapirosDocument14 pagesGuglielmo 2000 DiapirosJuan Carlos Caicedo AndradeNo ratings yet

- Surface News - 20130704 - Low Res PDFDocument9 pagesSurface News - 20130704 - Low Res PDFYoko GoldingNo ratings yet

- ReleaseNoteRSViewME 5 10 02Document12 pagesReleaseNoteRSViewME 5 10 02Jose Luis Chavez LunaNo ratings yet

- Phet Body Group 1 ScienceDocument42 pagesPhet Body Group 1 ScienceMebel Alicante GenodepanonNo ratings yet

- Psychological Attitude Towards SafetyDocument17 pagesPsychological Attitude Towards SafetyAMOL RASTOGI 19BCM0012No ratings yet

- PCU CalculationDocument2 pagesPCU CalculationMidhun Joseph0% (1)

- God Save The Queen Score PDFDocument3 pagesGod Save The Queen Score PDFDarion0% (2)

- Design of Accurate Steering Gear MechanismDocument12 pagesDesign of Accurate Steering Gear Mechanismtarik RymNo ratings yet

- HRM OmantelDocument8 pagesHRM OmantelSonia Braham100% (1)