You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Exam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- 500 Question SetDocument72 pages500 Question SetSushant MaskeyNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- UntitledDocument72 pagesUntitledSushant MaskeyNo ratings yet

- IT ResultDocument1 pageIT ResultSushant MaskeyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Valn of CMN StockDocument18 pagesValn of CMN StockSushant Maskey0% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- MS Word: Marks AllocationDocument1 pageMS Word: Marks AllocationSushant MaskeyNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Exam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

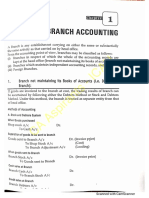

- Branch AccountingDocument51 pagesBranch AccountingSushant MaskeyNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Overheads PracticalDocument37 pagesOverheads PracticalSushant Maskey100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Risk Return Basics/Portfolio Management: Learning Objective of The ChapterDocument34 pagesRisk Return Basics/Portfolio Management: Learning Objective of The ChapterSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- CAPII Suggested Dec2015Document87 pagesCAPII Suggested Dec2015Sushant MaskeyNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- EDP Audit CIS Environment MeaningDocument7 pagesEDP Audit CIS Environment MeaningSushant MaskeyNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- URP Income Tax Part SolutionsDocument127 pagesURP Income Tax Part SolutionsSushant MaskeyNo ratings yet

- Budget & Budgetary ControlDocument15 pagesBudget & Budgetary ControlSushant MaskeyNo ratings yet

- NIOjid Akjc MDI9 L 5 Ulv I1617282937Document4 pagesNIOjid Akjc MDI9 L 5 Ulv I1617282937Sushant MaskeyNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Labour/Employee Cost: Classification of Labor CostDocument9 pagesLabour/Employee Cost: Classification of Labor CostSushant MaskeyNo ratings yet

- RD TReeqim RSFH XACz 0 W91617196460Document10 pagesRD TReeqim RSFH XACz 0 W91617196460Sushant MaskeyNo ratings yet

- Govt AuditingDocument12 pagesGovt AuditingSushant MaskeyNo ratings yet

- Join Us On Telegram: Https://t.me/caaspirantsican2Document14 pagesJoin Us On Telegram: Https://t.me/caaspirantsican2Sushant MaskeyNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant MaskeyNo ratings yet

- NON INTEGRATED TheoryDocument26 pagesNON INTEGRATED TheorySushant MaskeyNo ratings yet

- Join Us On Telegram: Https://t.me/caaspirantsican2Document15 pagesJoin Us On Telegram: Https://t.me/caaspirantsican2Sushant MaskeyNo ratings yet

- Cash ManagementDocument14 pagesCash ManagementSushant MaskeyNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- ESTIMATESDocument74 pagesESTIMATESAriane Joyze BronzalNo ratings yet

- Level 4 - Management Accounting Budgeting - Question BankDocument336 pagesLevel 4 - Management Accounting Budgeting - Question Banktrue100% (1)

- Chapter 4 - BudgetingDocument9 pagesChapter 4 - BudgetingVuong PhamNo ratings yet

- Estimation of BuildingDocument20 pagesEstimation of BuildingSaurav Gautam100% (1)

- Visvesvaraya Technological University: Assignment - 1Document12 pagesVisvesvaraya Technological University: Assignment - 1vinayNo ratings yet

- Oracle LCM Process FlowDocument3 pagesOracle LCM Process FlowMuhammad Faysal100% (1)

- Quizzer-Cost-Behavior - Docx Regression Analysis Least SquaresDocument1 pageQuizzer-Cost-Behavior - Docx Regression Analysis Least SquareslastjohnNo ratings yet

- Relevant Cost and Decision MakingDocument2 pagesRelevant Cost and Decision MakingInah SalcedoNo ratings yet

- Cost Accounting: Ex 5-5 Job Order Cost SheetDocument7 pagesCost Accounting: Ex 5-5 Job Order Cost Sheetatiq76No ratings yet

- Chapter 3 Part 2 - Costing and Budgetary ControlDocument23 pagesChapter 3 Part 2 - Costing and Budgetary ControlSuku Thomas SamuelNo ratings yet

- Flexible Budget ExampleDocument2 pagesFlexible Budget Examplebrenica_2000No ratings yet

- Difference Between Relevant Cost and Irrelevant CostDocument13 pagesDifference Between Relevant Cost and Irrelevant CostAmit SinghNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Managing RestructuringDocument140 pagesManaging RestructuringCollinson GrantNo ratings yet

- Management Accounting Questions Bank PDF FinalDocument18 pagesManagement Accounting Questions Bank PDF FinalSaba indian Food recipeNo ratings yet

- Financial Statements Analysis OF Companies (Non-Financial) Listed at Pakistan Stock ExchangeDocument463 pagesFinancial Statements Analysis OF Companies (Non-Financial) Listed at Pakistan Stock ExchangeMuhammad Asif YousafzaiNo ratings yet

- AssigmentDocument8 pagesAssigmentnonolashari0% (1)

- Variable Costing and Absorption CostingDocument15 pagesVariable Costing and Absorption CostingRomilCledoro100% (1)

- Assignment #1 ANSWER: LETTER A. 2,205Document5 pagesAssignment #1 ANSWER: LETTER A. 2,205hae1234100% (1)

- CH 10Document15 pagesCH 10JesseEwingNo ratings yet

- Management Accounting ReviewerDocument17 pagesManagement Accounting ReviewerAina Marie GullabNo ratings yet

- Management Advisory Services: Adamson UniversityDocument5 pagesManagement Advisory Services: Adamson UniversityziNo ratings yet

- BIAYA: Konsep, Klasifikasi Dan PerilakuDocument48 pagesBIAYA: Konsep, Klasifikasi Dan PerilakuAziz SugihartoNo ratings yet

- Cost Accounting StandardsDocument157 pagesCost Accounting StandardsMohit SankhalaNo ratings yet

- Dokumen - Tips - 12 Factory Overhead Planned Actual AppliedDocument13 pagesDokumen - Tips - 12 Factory Overhead Planned Actual AppliedDenny Kridex OmolonNo ratings yet

- Cost Accounting: T I C A PDocument4 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- 2015 Blue Orchid Business Plan Template Word OnlyDocument18 pages2015 Blue Orchid Business Plan Template Word OnlyPrince Horwolabi HifeoluwahNo ratings yet

- SamHoustonState Fy 2020Document79 pagesSamHoustonState Fy 2020Matt BrownNo ratings yet

- F5 - LCT-1Document6 pagesF5 - LCT-1Amna HussainNo ratings yet

- Product Costing and PricingDocument27 pagesProduct Costing and Pricingcarlito alvarezNo ratings yet

- Yes 3Document1 pageYes 3yes yesnoNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Excel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsFrom EverandExcel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsNo ratings yet

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)