You might also like

- Chap 5-Pages-45-46,63-119Document59 pagesChap 5-Pages-45-46,63-119RITZ BROWNNo ratings yet

- Home Work Section Working CapitalDocument10 pagesHome Work Section Working CapitalSaloni AgrawalNo ratings yet

- Cash ManagementDocument14 pagesCash ManagementSushant MaskeyNo ratings yet

- Decemeber 2020 Examinations: Suggested Answers ToDocument41 pagesDecemeber 2020 Examinations: Suggested Answers ToDipen AdhikariNo ratings yet

- Financial Feasibility of Constructing Consultancy CentreDocument11 pagesFinancial Feasibility of Constructing Consultancy Centrenisarg_No ratings yet

- Chartered Accountancy Professional CAP-II TitleDocument104 pagesChartered Accountancy Professional CAP-II TitleBAZINGANo ratings yet

- Compiler CAP II Cost AccountingDocument187 pagesCompiler CAP II Cost AccountingEdtech NepalNo ratings yet

- Capital Structure and Leverages-ProblemsDocument7 pagesCapital Structure and Leverages-ProblemsUday GowdaNo ratings yet

- Accounting from Incomplete Records: Trading and Profit Loss StatementDocument21 pagesAccounting from Incomplete Records: Trading and Profit Loss StatementbinuNo ratings yet

- Working Capital QuestionsDocument10 pagesWorking Capital QuestionsVaishnavi VenkatesanNo ratings yet

- RISK and RETURN With SolutionsDocument33 pagesRISK and RETURN With Solutionschiaraferragni100% (2)

- Suggested Answer CAP II June 2018Document128 pagesSuggested Answer CAP II June 2018Pradeep Bhattarai67% (3)

- CA Inter Cost Important Questions For CA Nov'22Document93 pagesCA Inter Cost Important Questions For CA Nov'2202 Tapasvee ShahNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- Working Capital Management - NumericalsDocument9 pagesWorking Capital Management - NumericalsAnjali JainNo ratings yet

- Cost Acc Nov06Document27 pagesCost Acc Nov06api-3825774No ratings yet

- Branch Accounting Examination BankDocument71 pagesBranch Accounting Examination BankNicole TaylorNo ratings yet

- Solution On Estimation of Working CapitalDocument5 pagesSolution On Estimation of Working Capitaljeta_prakash100% (2)

- Bos 28432 CP 10Document45 pagesBos 28432 CP 10hiral dattaniNo ratings yet

- Cost & Finance RTP Nov 15Document41 pagesCost & Finance RTP Nov 15Aaquib ShahiNo ratings yet

- FFM Updated AnswersDocument79 pagesFFM Updated AnswersSrikrishnan SNo ratings yet

- Paper - 3: Cost and Management Accounting Questions Material CostDocument31 pagesPaper - 3: Cost and Management Accounting Questions Material CostMohammed Mustafa KampuNo ratings yet

- 1 Working CapitalDocument63 pages1 Working CapitalDeepika Mittal50% (2)

- Account Past Questions Compilation (2009june - 2020 Dec.)Document246 pagesAccount Past Questions Compilation (2009june - 2020 Dec.)Prashant Sagar Gautam100% (2)

- Q1Document31 pagesQ1Bhaskkar SinhaNo ratings yet

- Paper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Document56 pagesPaper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Basant OjhaNo ratings yet

- Over Heads Additional Sums PDFDocument40 pagesOver Heads Additional Sums PDFShiva AP100% (1)

- MEA AssignmentDocument13 pagesMEA Assignmentankit07777100% (1)

- Not For Profit OrganizationDocument69 pagesNot For Profit OrganizationDristi SaudNo ratings yet

- DEPARTMENTAL ACCOUNTSDocument17 pagesDEPARTMENTAL ACCOUNTSAyush AcharyaNo ratings yet

- Point of IndifferenceDocument3 pagesPoint of IndifferenceSandhyaNo ratings yet

- Ca Inter - Nov 2018 - Advanced Accounts - Suggested Answers PDFDocument28 pagesCa Inter - Nov 2018 - Advanced Accounts - Suggested Answers PDFHIMANSHU NNo ratings yet

- Revision Test Paper CAP II Dec 2017Document163 pagesRevision Test Paper CAP II Dec 2017Dipen AdhikariNo ratings yet

- Sdathn Ripsryd@r@ea@pis - Unit) : - SolutionDocument16 pagesSdathn Ripsryd@r@ea@pis - Unit) : - SolutionAnimesh VoraNo ratings yet

- 18 Chapter4 Unit 1 2 Hire Purchase and Instalment PaymentDocument17 pages18 Chapter4 Unit 1 2 Hire Purchase and Instalment Paymentnarasimha_gudiNo ratings yet

- Receivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearDocument6 pagesReceivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearJC Del MundoNo ratings yet

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant MaskeyNo ratings yet

- Financial AccountingDocument60 pagesFinancial AccountingSurajNo ratings yet

- Calculating operating, financial and combined leverageDocument4 pagesCalculating operating, financial and combined leveragek,hbibk,n0% (1)

- Problems From Unit - 5Document8 pagesProblems From Unit - 5jeganrajrajNo ratings yet

- Tough LekkaluDocument42 pagesTough Lekkaludeviprasad03No ratings yet

- Com203 - Final Accounts of Insurance CompaniesDocument23 pagesCom203 - Final Accounts of Insurance CompaniesSanaullah M SultanpurNo ratings yet

- Cost of Capital: Vivek College of CommerceDocument31 pagesCost of Capital: Vivek College of Commercekarthika kounderNo ratings yet

- Calculate Learning Curve CostsDocument8 pagesCalculate Learning Curve Costszoyashaikh20No ratings yet

- Chapter 8 Operating CostingDocument13 pagesChapter 8 Operating CostingDerrick LewisNo ratings yet

- 11 AmalgmationDocument38 pages11 AmalgmationPranaya Agrawal100% (1)

- Valuation of Securities - ASSIGNMENTDocument63 pagesValuation of Securities - ASSIGNMENTNaga Nagendra0% (2)

- Problems On Working CapDocument25 pagesProblems On Working Capamazing19inNo ratings yet

- Cost Sheet - Pages 16Document16 pagesCost Sheet - Pages 16omikron omNo ratings yet

- Cost of Capital-ProblemsDocument6 pagesCost of Capital-ProblemsUday GowdaNo ratings yet

- Ebit Eps AnalysisDocument2 pagesEbit Eps AnalysisUma N100% (1)

- Chapter # 6 Departmental AccountDocument36 pagesChapter # 6 Departmental AccountRooh Ullah KhanNo ratings yet

- Revision Test Paper: Cap-Ii: Advanced Accounting: QuestionsDocument158 pagesRevision Test Paper: Cap-Ii: Advanced Accounting: Questionsshankar k.c.No ratings yet

- Inventory Valuation-ProblemsDocument3 pagesInventory Valuation-ProblemsKaran100% (1)

- DepartmentalDocument17 pagesDepartmentalPapiya DeyNo ratings yet

- 3246accounting - CA IPCCDocument116 pages3246accounting - CA IPCCPrashant Pandey100% (1)

- Recivable ManagmentDocument26 pagesRecivable ManagmentAnkita MukherjeeNo ratings yet

- Sums On PortfolioDocument8 pagesSums On PortfolioPrantikNo ratings yet

- JWCh06 PDFDocument23 pagesJWCh06 PDF007featherNo ratings yet

- Risk, Return, and Valuation: by The Mcgraw-Hill Companies, Inc. Click Here For Terms of UseDocument3 pagesRisk, Return, and Valuation: by The Mcgraw-Hill Companies, Inc. Click Here For Terms of UseIndrani DasguptaNo ratings yet

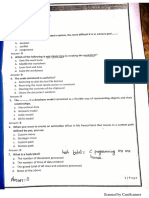

- MS Word: Marks AllocationDocument1 pageMS Word: Marks AllocationSushant MaskeyNo ratings yet

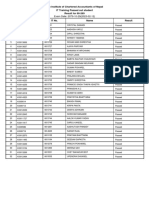

- Exam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-10-29 (2023-02-12) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

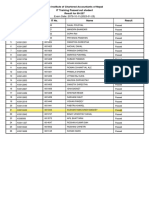

- Exam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalDocument1 pageExam Date: 2079-11-26 (2023-03-10) : IT Training Passed Out Student The Institute of Chartered Accountants of NepalSushant MaskeyNo ratings yet

- 500 Question SetDocument72 pages500 Question SetSushant MaskeyNo ratings yet

- CamScanner Document ScansDocument72 pagesCamScanner Document ScansSushant MaskeyNo ratings yet

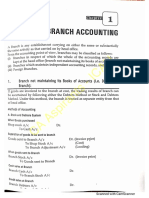

- Branch AccountingDocument51 pagesBranch AccountingSushant MaskeyNo ratings yet

- Budget Numerical PDFDocument5 pagesBudget Numerical PDFDilip BhusalNo ratings yet

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- IT ResultDocument1 pageIT ResultSushant MaskeyNo ratings yet

- Company ActDocument198 pagesCompany Actमेनसन लाखेमरूNo ratings yet

- Risk Return Basics/Portfolio Management: Learning Objective of The ChapterDocument34 pagesRisk Return Basics/Portfolio Management: Learning Objective of The ChapterSushant MaskeyNo ratings yet

- Common Stock Valuation MethodsDocument18 pagesCommon Stock Valuation MethodsSushant Maskey0% (1)

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- Leverage: Understanding Operating, Financial and Combined LeverageDocument15 pagesLeverage: Understanding Operating, Financial and Combined LeverageSushant MaskeyNo ratings yet

- Chapter 4: LeverageDocument15 pagesChapter 4: LeverageSushant MaskeyNo ratings yet

- 00 GC 7 G2 BPLXaal OX4 MSV 1617714838Document8 pages00 GC 7 G2 BPLXaal OX4 MSV 1617714838Sushant MaskeyNo ratings yet

- Common Stock Valuation MethodsDocument18 pagesCommon Stock Valuation MethodsSushant Maskey0% (1)

- Overheads PracticalDocument37 pagesOverheads PracticalSushant Maskey100% (1)

- Labour: (A) (B) (C) (D) (E)Document40 pagesLabour: (A) (B) (C) (D) (E)Sushant MaskeyNo ratings yet

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- EDP Audit CIS Environment MeaningDocument7 pagesEDP Audit CIS Environment MeaningSushant MaskeyNo ratings yet

- Z Ab I590 TIl 4 A3 o 6 O7 PYt 1617546492Document5 pagesZ Ab I590 TIl 4 A3 o 6 O7 PYt 1617546492Sushant MaskeyNo ratings yet

- URP Income Tax Part SolutionsDocument127 pagesURP Income Tax Part SolutionsSushant MaskeyNo ratings yet

- CAPII Suggested Dec2015Document87 pagesCAPII Suggested Dec2015Sushant MaskeyNo ratings yet

- Labour/Employee Cost: Classification of Labor CostDocument9 pagesLabour/Employee Cost: Classification of Labor CostSushant MaskeyNo ratings yet

- Overheads TheoryDocument11 pagesOverheads TheorySushant MaskeyNo ratings yet

- RD TReeqim RSFH XACz 0 W91617196460Document10 pagesRD TReeqim RSFH XACz 0 W91617196460Sushant MaskeyNo ratings yet

- NIOjid Akjc MDI9 L 5 Ulv I1617282937Document4 pagesNIOjid Akjc MDI9 L 5 Ulv I1617282937Sushant MaskeyNo ratings yet

- Financial Accounting - 1Document42 pagesFinancial Accounting - 1MajdiNo ratings yet

- Manual For SOA Exam MLC.: Chapter 5. Life Annuities. Section 5.4. N-Year Certain AnnuitiesDocument10 pagesManual For SOA Exam MLC.: Chapter 5. Life Annuities. Section 5.4. N-Year Certain AnnuitiesadelNo ratings yet

- Admission of Partner PDFDocument6 pagesAdmission of Partner PDFBHUMIKA JAINNo ratings yet

- Preqin - Corp Investor - IndiaDocument21 pagesPreqin - Corp Investor - Indiasavan anvekarNo ratings yet

- Final Project Report - Excel SheetDocument24 pagesFinal Project Report - Excel SheetrajeshNo ratings yet

- Joka Bulls CaseDocument2 pagesJoka Bulls Caseshivam kumarNo ratings yet

- LPP Formulation ProblemsDocument7 pagesLPP Formulation ProblemsRavindra BabuNo ratings yet

- East Coast Yacht's Expansion Plans-06!02!2008 v2Document3 pagesEast Coast Yacht's Expansion Plans-06!02!2008 v2percyNo ratings yet

- Feenstra Taylor Econ Capitulo 13Document60 pagesFeenstra Taylor Econ Capitulo 13João Carlos Silvério FerrazNo ratings yet

- Concept of DerivativesDocument7 pagesConcept of DerivativesveerabhadrayyaNo ratings yet

- Colgate Financial Model SolvedDocument33 pagesColgate Financial Model SolvedVvb SatyanarayanaNo ratings yet

- Portfolio Selection Theory ExplainedDocument3 pagesPortfolio Selection Theory ExplainedMufti AliNo ratings yet

- Corporation Accounting - DividendsDocument13 pagesCorporation Accounting - DividendsAlejandrea LalataNo ratings yet

- Level I Ethics Quiz 1Document9 pagesLevel I Ethics Quiz 1Mohammad Jubayer AhmedNo ratings yet

- Case Study:: Axis REITDocument9 pagesCase Study:: Axis REITAhmad Mustaqim SulaimanNo ratings yet

- Form A Application FormDocument6 pagesForm A Application FormBoinzb TNo ratings yet

- Forex QuizDocument20 pagesForex Quizgeetainderhanda4430No ratings yet

- Nyse Sap 2018Document190 pagesNyse Sap 2018Naveen KumarNo ratings yet

- Investment advice for client seeking retirement planningDocument16 pagesInvestment advice for client seeking retirement planningJaihindNo ratings yet

- Flowers Industries, Inc. (Abridged) : October 2008Document24 pagesFlowers Industries, Inc. (Abridged) : October 2008MJ SapiterNo ratings yet

- Karaoke Bar Business Case StudyDocument3 pagesKaraoke Bar Business Case StudyMark Louie Aguilar33% (3)

- FEDAI RulesDocument39 pagesFEDAI Rulesnaveen_ch522No ratings yet

- 04 Notes - The Net Present Value (NPV) PDFDocument7 pages04 Notes - The Net Present Value (NPV) PDFAlberto ElquetedejoNo ratings yet

- Undergraduate Story Templates for IBDocument4 pagesUndergraduate Story Templates for IBKerr limNo ratings yet

- Arbitrage Trading in Commodities-4Document2 pagesArbitrage Trading in Commodities-4James LiuNo ratings yet

- Debt Financing: Corporate Finance, 5E (Berk/Demarzo)Document4 pagesDebt Financing: Corporate Finance, 5E (Berk/Demarzo)Alexandre LNo ratings yet

- Towers Watson Tail Risk Management Strategies Oct2015Document14 pagesTowers Watson Tail Risk Management Strategies Oct2015Gennady NeymanNo ratings yet

- Calculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Document19 pagesCalculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Anil GowdaNo ratings yet

- The Sammons Associates Annual Heads of Equity Research SurveyDocument4 pagesThe Sammons Associates Annual Heads of Equity Research SurveytcawarrenNo ratings yet