You might also like

- Deed of Conditional Sale of Motor VehicleDocument2 pagesDeed of Conditional Sale of Motor VehicleMark Lester Lee Aure92% (60)

- Criminal Procedure Notes Based On RianoDocument19 pagesCriminal Procedure Notes Based On RianoMark Lester Lee Aure80% (10)

- Basic Skills in Construction Full BookDocument146 pagesBasic Skills in Construction Full Bookgeorgeowen100% (1)

- Exxon Contract Appointment LetterDocument7 pagesExxon Contract Appointment LetterDavid BoyerNo ratings yet

- Utilizing LGPMS InformationDocument13 pagesUtilizing LGPMS InformationRonz RoganNo ratings yet

- Construction of Bataan Government Center-Cum-Business Hub Starts - BusinessMirrorDocument2 pagesConstruction of Bataan Government Center-Cum-Business Hub Starts - BusinessMirrorErika RafaelNo ratings yet

- SAMPLE Letter of Intent 1.11.11Document1 pageSAMPLE Letter of Intent 1.11.11batambintanNo ratings yet

- BOOK I - Sovereignty and General AdministrationDocument9 pagesBOOK I - Sovereignty and General AdministrationRosa GamaroNo ratings yet

- Human Resource Review Work Program: Audit ObjectivesDocument7 pagesHuman Resource Review Work Program: Audit ObjectivesCyrose TaguinodNo ratings yet

- 2021 MPDC Final Accomplishment ReportDocument7 pages2021 MPDC Final Accomplishment ReportCristine Viernes Gaspar Batay-anNo ratings yet

- 5 MPDC Citizens Charter 2022Document6 pages5 MPDC Citizens Charter 2022Brod LanNo ratings yet

- PhilippinesGPRAProcurementObserversGuide2014 PDFDocument55 pagesPhilippinesGPRAProcurementObserversGuide2014 PDFCeslhee AngelesNo ratings yet

- Do - 061 - s1999 DPWH and Lgu Cost Sharing ProgramDocument17 pagesDo - 061 - s1999 DPWH and Lgu Cost Sharing ProgramrubydelacruzNo ratings yet

- Rule Vii - Invitation To Bid1Document13 pagesRule Vii - Invitation To Bid1GLYCE JOIE PLAZANo ratings yet

- BPLS Reformguide Promoting Local BPLS Reform in The PhilsDocument58 pagesBPLS Reformguide Promoting Local BPLS Reform in The PhilsErnstjr Montes100% (1)

- 04 14 2023 Public Private Partnerships in The PhilippinesDocument32 pages04 14 2023 Public Private Partnerships in The PhilippinesJediann BungagNo ratings yet

- Policy Memorandum WordDocument3 pagesPolicy Memorandum WordMawar PutihNo ratings yet

- Case Digest: The Disbursement Acceleration Program (DAP) FactsDocument2 pagesCase Digest: The Disbursement Acceleration Program (DAP) FactsyssaNo ratings yet

- Coa M2013-007 PDFDocument8 pagesCoa M2013-007 PDFGie Bernal CamachoNo ratings yet

- COA RulesDocument22 pagesCOA RulesNoraiza Mae Keith TalbinNo ratings yet

- What Is Project Execution?Document5 pagesWhat Is Project Execution?Russell EndoyNo ratings yet

- Cawad VS Abad Et Al, GR 207145, Juky 28, 2015Document27 pagesCawad VS Abad Et Al, GR 207145, Juky 28, 2015GmaeNo ratings yet

- DBM BudgetDocument85 pagesDBM BudgetGab Pogi100% (1)

- The Rules On Mediation: Legal BasisDocument22 pagesThe Rules On Mediation: Legal BasislambajosepgNo ratings yet

- 1991 LGC - Ra 7160Document257 pages1991 LGC - Ra 7160Lyrech NillerNo ratings yet

- Module 2 Accounting For Budgetary Accounts PDFDocument30 pagesModule 2 Accounting For Budgetary Accounts PDFcha11No ratings yet

- Updates On Local GovernanceDocument60 pagesUpdates On Local GovernanceTriov AntNo ratings yet

- Mandatory and Optional Positions, CSC Rules On Hiring and Selection and CompensationDocument61 pagesMandatory and Optional Positions, CSC Rules On Hiring and Selection and CompensationJojo ArcillasNo ratings yet

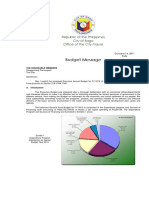

- Budget Message: Republic of The Philippines City of Bago Office of The City MayorDocument3 pagesBudget Message: Republic of The Philippines City of Bago Office of The City MayorAl SimbajonNo ratings yet

- The PARC StoryDocument59 pagesThe PARC StoryRio AlmenaNo ratings yet

- 01-Anda2015 Audit ReportDocument92 pages01-Anda2015 Audit ReportoabeljeanmoniqueNo ratings yet

- RA 9184 Rule 1to7Document86 pagesRA 9184 Rule 1to7Earl Justin Enrique0% (1)

- Migrant Workers Act RA 10022 and 9422 Amending 8042Document49 pagesMigrant Workers Act RA 10022 and 9422 Amending 8042adrianmdelacruzNo ratings yet

- Quantitative Strategic Planning Matrix (QSPM)Document4 pagesQuantitative Strategic Planning Matrix (QSPM)Ghurdiv ChandNo ratings yet

- Cases For COnsti CompilationDocument33 pagesCases For COnsti CompilationAchilles Neil EbronNo ratings yet

- FAQs For LGUs BudgetingDocument2 pagesFAQs For LGUs BudgetingSheryl Balualua Mape-SalvatierraNo ratings yet

- Theory & Practice of Public Administration: The Modern Civil ServiceDocument10 pagesTheory & Practice of Public Administration: The Modern Civil ServiceRokzxc GamingNo ratings yet

- Republic of Commonwealth Avenue, Quezon City, Philippines: Commission OnDocument25 pagesRepublic of Commonwealth Avenue, Quezon City, Philippines: Commission OnMariaRizzaMontalboGuizzaganNo ratings yet

- Coa M2014-009 PDFDocument34 pagesCoa M2014-009 PDFAlvin ComilaNo ratings yet

- LGU NGAS Chapter 1 and 2Document24 pagesLGU NGAS Chapter 1 and 2Lail PDNo ratings yet

- Feasibility Study NRW - PhilipinesDocument24 pagesFeasibility Study NRW - PhilipinesengkjNo ratings yet

- LGC - Ra 7160Document207 pagesLGC - Ra 7160Rah-rah Tabotabo ÜNo ratings yet

- M1 - Sources of ObligationsDocument5 pagesM1 - Sources of ObligationsAdrienne Nicole MercadoNo ratings yet

- Disposal of Real PropertyDocument24 pagesDisposal of Real Propertypogiman_01100% (1)

- Remedial Law - CRIM PRO (Pros. Centeno)Document61 pagesRemedial Law - CRIM PRO (Pros. Centeno)Eisley Sarzadilla-GarciaNo ratings yet

- Deed of Donation-TamarDocument2 pagesDeed of Donation-TamarJomidy MidtanggalNo ratings yet

- Do - 137 - s1999 Guidelines On Moa For LguDocument23 pagesDo - 137 - s1999 Guidelines On Moa For LgurubydelacruzNo ratings yet

- Budget Basics For UP Students by Leonor M. BrionesDocument9 pagesBudget Basics For UP Students by Leonor M. BrionesSteve B. SalongaNo ratings yet

- Accounting For Budgetary AccountsDocument10 pagesAccounting For Budgetary AccountsIsah Ma. Zenaida Felisilda100% (1)

- Project Administration ManualDocument31 pagesProject Administration ManualZeuss MohamedNo ratings yet

- Job Seekers Employment Guide Training Manual - ColoredDocument34 pagesJob Seekers Employment Guide Training Manual - ColoredFrancis RayNo ratings yet

- GPPB Circular No. 02-2012 PDFDocument2 pagesGPPB Circular No. 02-2012 PDFLuckyTTinioNo ratings yet

- Concept of Funds-Dr. Loida M. CancinoDocument81 pagesConcept of Funds-Dr. Loida M. CancinoAricirtap Abenoja JoyceNo ratings yet

- Competitive Bidding Procedure - Procurement of Goods & InfraDocument50 pagesCompetitive Bidding Procedure - Procurement of Goods & InfraBryan MendozaNo ratings yet

- Budgeting and FinancingDocument12 pagesBudgeting and FinancingMondrei TVNo ratings yet

- BIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsDocument1 pageBIR Form 2550M - Monthly Value-Added Tax Declaration Guidelines and InstructionsdreaNo ratings yet

- E GovernanceDocument3 pagesE Governanceshubhi1996No ratings yet

- Joint Circular CSC-DBM No. 01, S. 2016 - Rules and Regulations On The Grant of Step Increments To Elective Officials Based On Length of ServiceDocument6 pagesJoint Circular CSC-DBM No. 01, S. 2016 - Rules and Regulations On The Grant of Step Increments To Elective Officials Based On Length of ServiceMarjoriz Tan IgnacioNo ratings yet

- RA 9184 - 5th EditionDocument108 pagesRA 9184 - 5th EditionJoseph Teejay LeeNo ratings yet

- Kida vs. SenateDocument11 pagesKida vs. SenateCassandra LaysonNo ratings yet

- PM Ra 11032 Written Report by John Carlo CapawaDocument16 pagesPM Ra 11032 Written Report by John Carlo CapawaJohn Carlo JoCapNo ratings yet

- Unlocking Innovation for Development: Action Update: What worked and what didn't for ADB's first innovation regional technical assistance projectFrom EverandUnlocking Innovation for Development: Action Update: What worked and what didn't for ADB's first innovation regional technical assistance projectNo ratings yet

- Brantford 2011 Financial ReportsDocument168 pagesBrantford 2011 Financial ReportsHugo RodriguesNo ratings yet

- Resource Mobilisation of LSGBsDocument31 pagesResource Mobilisation of LSGBsShaimon Joseph0% (1)

- Review of Utilization of ENR Revenues and Application of Media StrategiesDocument160 pagesReview of Utilization of ENR Revenues and Application of Media StrategiesMark Lester Lee AureNo ratings yet

- De La Puerta v. Court of Appeals, G.R. No. 77867, February 6, 1990, 181 SCRA 861, 869Document3 pagesDe La Puerta v. Court of Appeals, G.R. No. 77867, February 6, 1990, 181 SCRA 861, 869Mark Lester Lee AureNo ratings yet

- SB 44 - LacsonDocument25 pagesSB 44 - LacsonMark Lester Lee AureNo ratings yet

- PILA Case Digest MTDocument27 pagesPILA Case Digest MTMark Lester Lee Aure100% (1)

- Silverio Vs SilverioDocument6 pagesSilverio Vs SilverioMark Lester Lee AureNo ratings yet

- La Bugal BlaanDocument21 pagesLa Bugal BlaanMark Lester Lee AureNo ratings yet

- LTD Digest FinalsDocument24 pagesLTD Digest FinalsMark Lester Lee Aure100% (1)

- Del Mar Vs PagcorDocument15 pagesDel Mar Vs PagcorMark Lester Lee AureNo ratings yet

- People Vs de CastroDocument5 pagesPeople Vs de CastroMark Lester Lee AureNo ratings yet

- 1 - Prudential Guarantee and Assurance Inc Vs Trans-Asia Shipping Lines Inc 491 SCRA 411 GR 151890, 151991 June 20, 2006Document11 pages1 - Prudential Guarantee and Assurance Inc Vs Trans-Asia Shipping Lines Inc 491 SCRA 411 GR 151890, 151991 June 20, 2006Mark Lester Lee AureNo ratings yet

- CrimPro Bar Q&ADocument15 pagesCrimPro Bar Q&AMark Lester Lee AureNo ratings yet

- Vinuya Vs Executive SecretaryDocument4 pagesVinuya Vs Executive SecretaryMark Lester Lee AureNo ratings yet

- PILA2 - in Re Arturo GarciaDocument1 pagePILA2 - in Re Arturo GarciaMark Lester Lee AureNo ratings yet

- 5 - Beltran Vs PeopleDocument7 pages5 - Beltran Vs PeopleMark Lester Lee AureNo ratings yet

- PILA3 - Sison Vs Board of AccountancyDocument3 pagesPILA3 - Sison Vs Board of AccountancyMark Lester Lee AureNo ratings yet

- 9 - People Vs AbalosDocument3 pages9 - People Vs AbalosMark Lester Lee AureNo ratings yet

- 10 - People Vs UmaliDocument7 pages10 - People Vs UmaliMark Lester Lee AureNo ratings yet

- Auditing 2 - Chapter FiveDocument10 pagesAuditing 2 - Chapter Fivehabtamu tadesseNo ratings yet

- Weebly Adult LiteracyDocument12 pagesWeebly Adult Literacyapi-547116548No ratings yet

- Vicarious Liability Is One of The Most Important Part of Torts Which Is Basically Concerned With Holding The Master Responsible For The Wrongful Acts of The Servant Done in The Course of EmploymentDocument3 pagesVicarious Liability Is One of The Most Important Part of Torts Which Is Basically Concerned With Holding The Master Responsible For The Wrongful Acts of The Servant Done in The Course of EmploymentBrijbhan Singh RajawatNo ratings yet

- Business Studies Assignment - Netflix Group Gamma-F Pestel Analysis Political FactorsDocument6 pagesBusiness Studies Assignment - Netflix Group Gamma-F Pestel Analysis Political FactorsRadhika VekariaNo ratings yet

- Pay GoDocument213 pagesPay GodeepusvvpNo ratings yet

- University of Technology, Jamaica Faculty of Law Discrimination LawDocument22 pagesUniversity of Technology, Jamaica Faculty of Law Discrimination LawPersephone WestNo ratings yet

- Curriculum Vitae: PO Box 952, Charlton City, MA 01508 (774) 230-3459Document3 pagesCurriculum Vitae: PO Box 952, Charlton City, MA 01508 (774) 230-3459ds_srinivasNo ratings yet

- Child Labor PowerpointDocument18 pagesChild Labor Powerpointapi-123809048No ratings yet

- Introduction To ManagemetDocument38 pagesIntroduction To ManagemetKhalid WariaNo ratings yet

- Special Challenges in Career Management - PPT 12Document33 pagesSpecial Challenges in Career Management - PPT 12ERMIYAS TARIKUNo ratings yet

- 1980 F007 Motivating Through Total Reward RBSDocument5 pages1980 F007 Motivating Through Total Reward RBSChetan SahgalNo ratings yet

- Workers Compensation Florida Case Ramos-V-sedgwick-complaintDocument26 pagesWorkers Compensation Florida Case Ramos-V-sedgwick-complaintbmiller6863No ratings yet

- Administración de Recursos HumanosDocument345 pagesAdministración de Recursos Humanosmanuela zuiga100% (1)

- Transformation of Human Resource Management Practices in India After The Liberalization - A Case of Tata MotorsDocument4 pagesTransformation of Human Resource Management Practices in India After The Liberalization - A Case of Tata MotorsAyushi kashyapNo ratings yet

- Aug - 23 Salary SlipDocument1 pageAug - 23 Salary SlipBack-End MarketingNo ratings yet

- Corporate Social ResponsibilityDocument8 pagesCorporate Social ResponsibilityGauchoJuniorNo ratings yet

- 4 Jcom 04 2016 0026Document23 pages4 Jcom 04 2016 0026Pitrayanti KambaNo ratings yet

- HIGA LOA - Other Than Managerial - FINAL - July 14Document25 pagesHIGA LOA - Other Than Managerial - FINAL - July 14Yejira KionNo ratings yet

- Administrative Disciplinary Rules On Sexual Harassment Cases (CSC Resolution 01-0940)Document3 pagesAdministrative Disciplinary Rules On Sexual Harassment Cases (CSC Resolution 01-0940)Jerome AzarconNo ratings yet

- P 4 (1 05) PSI Plant Safety Inspection (35) Jul.2012Document35 pagesP 4 (1 05) PSI Plant Safety Inspection (35) Jul.2012Vaibhav Vithoba Naik100% (9)

- Component of Social Casework 3.) Place AgencyDocument20 pagesComponent of Social Casework 3.) Place AgencyJanna Monica YapNo ratings yet

- Rolce Royce HR PoliciesDocument3 pagesRolce Royce HR PoliciesNikul Maheshwari0% (1)

- Do You Redress The Grievances of Employee's WifeDocument6 pagesDo You Redress The Grievances of Employee's WifeMani Vardhan0% (2)

- Overheads - CW - Sums - Part 2Document8 pagesOverheads - CW - Sums - Part 2kushgarg627No ratings yet

- Resume For Internship With No Work ExperienceDocument6 pagesResume For Internship With No Work Experienceafjwftijfbwmen100% (1)

- Vinoya Vs NLRCDocument2 pagesVinoya Vs NLRCHeidi100% (1)

- Tennis Action PlanDocument31 pagesTennis Action PlanKhalid FadliNo ratings yet