You might also like

- 300 Crypto Map Matchcoins InfoDocument1 page300 Crypto Map Matchcoins Infoclawmvp100% (1)

- Littlehand Crochet Pirate DuckDocument20 pagesLittlehand Crochet Pirate Duckcabungcalmaryrose100% (2)

- Cryptocurrency Mining Hardware: Striving For EfficiencyDocument37 pagesCryptocurrency Mining Hardware: Striving For Efficiencysmshiva59No ratings yet

- MBODocument23 pagesMBOHarsimran KaurNo ratings yet

- Principles of Corporate Finance - AnswerDocument41 pagesPrinciples of Corporate Finance - Answernguyenhuyhuynh89No ratings yet

- NP727 Traveller English Amended 120821v2Document2 pagesNP727 Traveller English Amended 120821v2didinurieliaNo ratings yet

- Project Report On Fixed Deposit in Devgiri BankDocument78 pagesProject Report On Fixed Deposit in Devgiri BankKamlakar Avhad69% (16)

- CommScope ERA Product Update FEB2022Document23 pagesCommScope ERA Product Update FEB2022miche eeNo ratings yet

- Business PlanDocument16 pagesBusiness PlanMustafizur Rahman100% (1)

- Crypto Wallet PlatformDocument21 pagesCrypto Wallet PlatformJPAH FXNo ratings yet

- KDC-MHU Site Loa GagakDocument4 pagesKDC-MHU Site Loa GagakCholis CivilNo ratings yet

- Low Est Price Edito RS' Ratin G: Best ForDocument2 pagesLow Est Price Edito RS' Ratin G: Best ForMILACEL GAMIDONo ratings yet

- Xiaomi Pricelist CE & IOTDocument7 pagesXiaomi Pricelist CE & IOTdarma davasgaiumNo ratings yet

- Flashcart Comparison ChartDocument3 pagesFlashcart Comparison ChartTigerTail123No ratings yet

- Philips 49HFF8358Document84 pagesPhilips 49HFF8358equipotrabajofytNo ratings yet

- Cryptocurrencies Compatibility?: Permite Palabras Mnemotecnicas para Recordar SemillaDocument3 pagesCryptocurrencies Compatibility?: Permite Palabras Mnemotecnicas para Recordar SemillawdwwwwwNo ratings yet

- On Ground Infrastructure ReportDocument3 pagesOn Ground Infrastructure Reportkpraveen reddyNo ratings yet

- Peddi Indukuri Product Manager March 3rd, 2017: ©2017 Extreme Networks, Inc. All Rights ReservedDocument6 pagesPeddi Indukuri Product Manager March 3rd, 2017: ©2017 Extreme Networks, Inc. All Rights ReservedTomaNo ratings yet

- ATBU Staff Quarter Plot Subdivision-Mode2lDocument1 pageATBU Staff Quarter Plot Subdivision-Mode2lalica studioNo ratings yet

- Dor - 23 09 2022 - WQ1 223 - Idc 143 2Document1 pageDor - 23 09 2022 - WQ1 223 - Idc 143 2kareemNo ratings yet

- Comps UpworkDocument6 pagesComps UpworkSyed Umair NafeesNo ratings yet

- Budget Produksi: JudulDocument12 pagesBudget Produksi: JudulKei Hijrah FestNo ratings yet

- Planilla Rec-Doa 4 Al 10 MayoDocument399 pagesPlanilla Rec-Doa 4 Al 10 MayoJair CruzNo ratings yet

- Xcruiser 4K Models ComparisonDocument1 pageXcruiser 4K Models ComparisonAli YarahmadiNo ratings yet

- Hermione Granger The Witch Girl Crochet Pattern PDF Crochet EmbroideryDocument1 pageHermione Granger The Witch Girl Crochet Pattern PDF Crochet EmbroideryJackie Arrowsmith100% (2)

- Colombia Imp Detention DemurrageDocument1 pageColombia Imp Detention DemurrageAlvaro ValenciaNo ratings yet

- E1+Jitter+Wander+Data: TestingDocument8 pagesE1+Jitter+Wander+Data: TestingMohammad E AbbassianNo ratings yet

- Cardano (ADA) CryptoSlateDocument1 pageCardano (ADA) CryptoSlatePravin KharateNo ratings yet

- AV Over IP Solutions - enDocument32 pagesAV Over IP Solutions - enTim Tim GNo ratings yet

- Comparison IH Readers - OUS - ENDocument2 pagesComparison IH Readers - OUS - ENOo Kenx OoNo ratings yet

- Hadoop by Dr. Kamal GulatiDocument33 pagesHadoop by Dr. Kamal GulatiYash TiwariNo ratings yet

- TV - POP DISCLAIMER - R1Document1 pageTV - POP DISCLAIMER - R1h1 yb69No ratings yet

- Wireless Transmitter + Superregenerative Receiver Pair 315MHz - Dipmicro ElectronicsDocument4 pagesWireless Transmitter + Superregenerative Receiver Pair 315MHz - Dipmicro ElectronicsEarl GatesNo ratings yet

- OMMPR OnGroundInfrastructureReportDocument2 pagesOMMPR OnGroundInfrastructureReportkpraveen reddyNo ratings yet

- Electronics WorkshopDocument9 pagesElectronics WorkshoptanishqNo ratings yet

- Spec Compare DP20T and KemenkesDocument4 pagesSpec Compare DP20T and KemenkesRiyandNo ratings yet

- Managemen Gaji LaundryDocument62 pagesManagemen Gaji LaundryDodik LopmaNo ratings yet

- Poster Page of The Global TimesDocument1 pagePoster Page of The Global TimesmallikpankajNo ratings yet

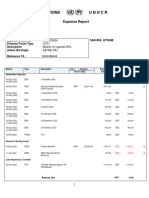

- Expense Report-SakuraDocument2 pagesExpense Report-Sakurazvikomborero manjalaNo ratings yet

- Company LogoDocument4 pagesCompany LogoKalakada HemanthNo ratings yet

- HDC-1801 Datasheet enDocument2 pagesHDC-1801 Datasheet enOscar MendozaNo ratings yet

- Nearians - Near 2021 Report v1Document29 pagesNearians - Near 2021 Report v1Homestay ParaNo ratings yet

- Apna Choice Hindi 225: Delhi / Haryana /uttar PradeshDocument98 pagesApna Choice Hindi 225: Delhi / Haryana /uttar PradeshVivekNo ratings yet

- Dungeons &: Do Not Disturb Registration Online - DND Activation - NDNC ..Document2 pagesDungeons &: Do Not Disturb Registration Online - DND Activation - NDNC ..Evubha GooDungarNo ratings yet

- Direct Sales Program Area 2 - ShareDocument34 pagesDirect Sales Program Area 2 - SharecepitelkomselNo ratings yet

- Planting and Harvesting Template SCDocument36 pagesPlanting and Harvesting Template SCriza cabugnaoNo ratings yet

- SanandDocument2 pagesSanandVishal UghrejiyaNo ratings yet

- Apartment Approach: Institutional Approach (Working Women Hostel, IT Industries Etc) Women EntrepreneurDocument1 pageApartment Approach: Institutional Approach (Working Women Hostel, IT Industries Etc) Women EntrepreneurVasanth KumarNo ratings yet

- Crypto Basics - Candidate Study Guide DecDocument1 pageCrypto Basics - Candidate Study Guide DecAllen LaiNo ratings yet

- ZEBRA DS3600 Vs IDH 7000Document2 pagesZEBRA DS3600 Vs IDH 7000Yogie NovriandiNo ratings yet

- Countries Allowed To Embark MSC CruisesDocument1 pageCountries Allowed To Embark MSC CruisesOxana CottaNo ratings yet

- Compairing DATADIODE - OPSWAT Data Diode Buying GuideDocument2 pagesCompairing DATADIODE - OPSWAT Data Diode Buying Guidebakhti.nasiri.avNo ratings yet

- Dor 19-11-2019 FH#5 Idc45 18Document1 pageDor 19-11-2019 FH#5 Idc45 18kareemNo ratings yet

- Spain DND ImportDocument1 pageSpain DND ImportyefryNo ratings yet

- Title Studio/Lab StatusDocument3 pagesTitle Studio/Lab StatusbuckNo ratings yet

- Ug2022 23Document2 pagesUg2022 23tmkoc2605No ratings yet

- Rubic PitchDeckDocument14 pagesRubic PitchDeckKoh Zhi HaoNo ratings yet

- IOS 4217 Currency CodesDocument12 pagesIOS 4217 Currency Codestemporal11No ratings yet

- DPO Hathway DigitalDocument27 pagesDPO Hathway DigitalSuresh KumarNo ratings yet

- Dahua DH-IPC-SHFW71921-ZAS 2MPDocument3 pagesDahua DH-IPC-SHFW71921-ZAS 2MPJUANSOLUSINDONo ratings yet

- XAT Compendium Part 5Document5 pagesXAT Compendium Part 518131A04E9 PATNAYAKUNI KIRANNo ratings yet

- Catálogo 2016 LiteDocument32 pagesCatálogo 2016 LiteMEP ComunicacionesNo ratings yet

- IP Solutions For All Application NeedsDocument12 pagesIP Solutions For All Application Needsqcmqpdmc evdgxpxrNo ratings yet

- Analyzing and Interpreting Financial Statements: Learning Objectives - Coverage by QuestionDocument37 pagesAnalyzing and Interpreting Financial Statements: Learning Objectives - Coverage by QuestionpoollookNo ratings yet

- Software Sector Report 1.16.2018Document24 pagesSoftware Sector Report 1.16.2018in_daHouseNo ratings yet

- F 2016114034 P 1Document147 pagesF 2016114034 P 1scribd167No ratings yet

- FIN 354 Ca2Document13 pagesFIN 354 Ca2Jashim AhammedNo ratings yet

- Leases: IAS 17: IFRS PrimerDocument39 pagesLeases: IAS 17: IFRS PrimersadorzonNo ratings yet

- Motaal Analysis TheoryDocument5 pagesMotaal Analysis TheoryKrishnamohan VaddadiNo ratings yet

- Heart Attack Prevention TipsDocument1 pageHeart Attack Prevention TipsMLastTryNo ratings yet

- Internship ReportDocument36 pagesInternship ReportMd.Ashraful Islam RiyadNo ratings yet

- IEA Report 3rd AprilDocument39 pagesIEA Report 3rd AprilnarnoliaNo ratings yet

- Record The Following Transactions On Page 2 of The Journal:: InstructionsDocument3 pagesRecord The Following Transactions On Page 2 of The Journal:: InstructionsItsF2bleAP 37100% (1)

- R36 The Arbitrage-Free Valuation Framework Q Bank PDFDocument9 pagesR36 The Arbitrage-Free Valuation Framework Q Bank PDFZidane Khan100% (1)

- Lobj19 - 0000047 CR 19 PT Q PDFDocument8 pagesLobj19 - 0000047 CR 19 PT Q PDFqqqNo ratings yet

- Baroda BNP Paribas Flexi Cap Fund Leaflet - EnglishDocument2 pagesBaroda BNP Paribas Flexi Cap Fund Leaflet - EnglishMohd Faraz TariqNo ratings yet

- PF Admin Charges Reduced To 0.5% From 1 June 2018 and EDLI Admin Charges Waived by EPFO - CA ClubDocument4 pagesPF Admin Charges Reduced To 0.5% From 1 June 2018 and EDLI Admin Charges Waived by EPFO - CA ClubNISHA SONARNo ratings yet

- 162 001Document1 page162 001Christian Mark AbarquezNo ratings yet

- Fintech Report StudyDocument2 pagesFintech Report StudyAishwaryaNo ratings yet

- Bank Reserves and Bank DepositsDocument2 pagesBank Reserves and Bank DepositsH-Sam PatoliNo ratings yet

- Accounting LalaDocument2 pagesAccounting LalaPaw PaladanNo ratings yet

- Group 1nov 2009Document73 pagesGroup 1nov 2009dc9510No ratings yet

- Aptitudes:: Period April 16, 2017 To Till DateDocument4 pagesAptitudes:: Period April 16, 2017 To Till DateRaka AnjumNo ratings yet

- Fiscal Policy Paper FY 2020/21: Government of JamaicaDocument112 pagesFiscal Policy Paper FY 2020/21: Government of JamaicaMecheal ThomasNo ratings yet

- Construction Equipment Management: Part Three 3Document18 pagesConstruction Equipment Management: Part Three 3jaradatNo ratings yet

- Kriti Industries 2019 PDFDocument132 pagesKriti Industries 2019 PDFPuneet367No ratings yet

- MuniGuideDocument69 pagesMuniGuidePioneer Institute50% (2)

- Axpo Solutions Annual Report 2021 2022Document132 pagesAxpo Solutions Annual Report 2021 2022VioletaNo ratings yet

- Economy 4 NewbiesDocument441 pagesEconomy 4 NewbiesSahil KapoorNo ratings yet