You might also like

- Journal Entry BasicsDocument22 pagesJournal Entry BasicsSURBHI BATHAM Student, Jaipuria IndoreNo ratings yet

- Journal and subsidiary books explainedDocument16 pagesJournal and subsidiary books explainedTushar SainiNo ratings yet

- CBSE Class 11 Accounting-Recording of TransactionsDocument78 pagesCBSE Class 11 Accounting-Recording of TransactionsRudraksh PareyNo ratings yet

- Chap - 9 Book Keeping XI HALLDocument114 pagesChap - 9 Book Keeping XI HALLKirtee TiwariNo ratings yet

- 5) JournalDocument24 pages5) JournalRay ChNo ratings yet

- Answer: Book-Keeping Is Mainly Concerned With Record Keeping orDocument7 pagesAnswer: Book-Keeping Is Mainly Concerned With Record Keeping orRisha RoyNo ratings yet

- Block 1 ECO 02 Unit 1Document24 pagesBlock 1 ECO 02 Unit 1Akhilesh SinghNo ratings yet

- 2.2 - LedgerDocument3 pages2.2 - LedgerABHAYNo ratings yet

- 320 Accountancy Eng Lesson6Document17 pages320 Accountancy Eng Lesson6Hitesh MishraNo ratings yet

- Accounting and Financial ManagementDocument18 pagesAccounting and Financial ManagementRocky SinghNo ratings yet

- Journal EntriesDocument40 pagesJournal EntriesPai100% (4)

- Unit 1 Recording of Transactions Lesson-4 Journal StructureDocument23 pagesUnit 1 Recording of Transactions Lesson-4 Journal StructureAmit RawalNo ratings yet

- Accounts Journals TB P10Document22 pagesAccounts Journals TB P10varadu1963No ratings yet

- MBA Chp-7 - LedgerDocument11 pagesMBA Chp-7 - LedgerNitish rajNo ratings yet

- NCERT SolutionsDocument55 pagesNCERT SolutionsArif ShaikhNo ratings yet

- Ncert Solutions For Class 11 Accountancy Chapter 4 Recording of Transactions 2Document69 pagesNcert Solutions For Class 11 Accountancy Chapter 4 Recording of Transactions 2Prateek TodurNo ratings yet

- Books of Accounts RecordsDocument8 pagesBooks of Accounts RecordsMylene SantiagoNo ratings yet

- CH 10Document21 pagesCH 10Tushar SainiNo ratings yet

- 11 Class Journal EntriesDocument10 pages11 Class Journal EntriesAbhishek KaushikNo ratings yet

- Quarter 3 - Module 4: Books of AccountsDocument12 pagesQuarter 3 - Module 4: Books of AccountsKISHANo ratings yet

- Ledger Part 1Document25 pagesLedger Part 1manisha sarafNo ratings yet

- Journal, Ledger, Trial BalanceDocument12 pagesJournal, Ledger, Trial BalanceANJALI KUMARINo ratings yet

- Financial Accountancy Chapter 4 Notes PDFDocument55 pagesFinancial Accountancy Chapter 4 Notes PDFHarshavardhanNo ratings yet

- Books of Prime Entry / JournalDocument23 pagesBooks of Prime Entry / JournalSai TejaNo ratings yet

- Journal and LedgerDocument23 pagesJournal and Ledgerfarooq.haqiq2012No ratings yet

- MEFA - 4th UnitDocument24 pagesMEFA - 4th UnitP.V.S. VEERANJANEYULUNo ratings yet

- Fabm1 ch9Document8 pagesFabm1 ch9Crisson FermalinoNo ratings yet

- Unit 3 Ledger Posting and Trial Balance PDFDocument46 pagesUnit 3 Ledger Posting and Trial Balance PDFPankaj VishwakarmaNo ratings yet

- 3 Journal-TDocument1 page3 Journal-TanushkaNo ratings yet

- Accounting 1 Module 9 - The Books of Accounts - Journals Part 1Document19 pagesAccounting 1 Module 9 - The Books of Accounts - Journals Part 1Blanche MargateNo ratings yet

- Unit 3 Ledger Posting and Trial Balance Module - 1 M O D U L E - 1Document46 pagesUnit 3 Ledger Posting and Trial Balance Module - 1 M O D U L E - 1Ketan ThakkarNo ratings yet

- EBOOK6131f1fd1229c Unit 3 Ledger Posting and Trial Balance PDFDocument44 pagesEBOOK6131f1fd1229c Unit 3 Ledger Posting and Trial Balance PDFYaw Antwi-AddaeNo ratings yet

- Ledger Posting and Trial BalanceDocument28 pagesLedger Posting and Trial BalanceAbhijay AnoopNo ratings yet

- Ledger: Types, Importance and AdvantagesDocument3 pagesLedger: Types, Importance and AdvantagesNehaAgrawalNo ratings yet

- Simple Book KeepingDocument57 pagesSimple Book KeepinglagunzadjidNo ratings yet

- Journal or Day BookDocument42 pagesJournal or Day BookRaviSankar100% (1)

- Unit 2 - Module 2Document18 pagesUnit 2 - Module 2Sujata SarkarNo ratings yet

- Journal: What Is A Journal?Document14 pagesJournal: What Is A Journal?Sourabh Sabat100% (1)

- Journalizing TransactionsDocument38 pagesJournalizing TransactionsPratyush mishraNo ratings yet

- FAA questionsDocument8 pagesFAA questionssudeepverma007No ratings yet

- Books of Accounts: Journals and LedgersDocument11 pagesBooks of Accounts: Journals and LedgersRD Suarez83% (6)

- CH-2 Financial Accounting ConceptsDocument40 pagesCH-2 Financial Accounting Conceptsnemik007No ratings yet

- Unit 7Document16 pagesUnit 7Roma MunjalNo ratings yet

- ISR 111 - Chapter 7 MaterialsDocument9 pagesISR 111 - Chapter 7 MaterialsTrisha Nicole FajardoNo ratings yet

- Week 3.1 Books of Accounts 1Document7 pagesWeek 3.1 Books of Accounts 1sherynmanalo0No ratings yet

- Chapter 6 Books of AccountingDocument21 pagesChapter 6 Books of AccountingAina Charisse DizonNo ratings yet

- Management Accounting Chapter 2 DefinitionsDocument9 pagesManagement Accounting Chapter 2 DefinitionsRishi_Sachdev_6020No ratings yet

- UNIT 2 - FFA Study Material-DRJDocument54 pagesUNIT 2 - FFA Study Material-DRJTushar Singh SanuNo ratings yet

- Chapter 1Document8 pagesChapter 1Trisha SinghNo ratings yet

- Class 11 Account Solution For Session (2023-2024) Chapter-4 Recording of Transaction-IIDocument104 pagesClass 11 Account Solution For Session (2023-2024) Chapter-4 Recording of Transaction-IIsyed mohdNo ratings yet

- Ledger and posting explained in 40 charactersDocument19 pagesLedger and posting explained in 40 charactersSURBHI BATHAM Student, Jaipuria IndoreNo ratings yet

- Journal EntriesDocument12 pagesJournal Entriesg81596262No ratings yet

- Fundamentals of ABM Module 5Document14 pagesFundamentals of ABM Module 5Loriely De GuzmanNo ratings yet

- General Journal, The Most CommonDocument4 pagesGeneral Journal, The Most CommonShesharam ChouhanNo ratings yet

- Theory & Practical Question Journal Enteries 1Document17 pagesTheory & Practical Question Journal Enteries 1manimeraj506iNo ratings yet

- CH.2 Part IDocument35 pagesCH.2 Part IthomasNo ratings yet

- Entrepreneurship: Chart of Accounts/ JournalizingDocument8 pagesEntrepreneurship: Chart of Accounts/ JournalizingSeigfred SeverinoNo ratings yet

- 320 L - 2 Accounting Concepts PDFDocument15 pages320 L - 2 Accounting Concepts PDFpopushellyNo ratings yet

- Adjustment Entries I Unsolved 1 7Document2 pagesAdjustment Entries I Unsolved 1 7Erica SisgonNo ratings yet

- Bank Rekonsiliasi PDFDocument31 pagesBank Rekonsiliasi PDFSekar Ayu Kartika SariNo ratings yet

- Solved Example (1) - Bank Reconciliation Statement: Date Details Payments ($) Receipts ($) Balance ($)Document2 pagesSolved Example (1) - Bank Reconciliation Statement: Date Details Payments ($) Receipts ($) Balance ($)MATIULLAHNo ratings yet

- Accounting Conventions and Standards: Module - 1Document12 pagesAccounting Conventions and Standards: Module - 1MATIULLAHNo ratings yet

- Accounting - An Introduction: Module - 1Document22 pagesAccounting - An Introduction: Module - 1Karen Joy RevadonaNo ratings yet

- E-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedDocument2 pagesE-Ticket Receipt & Itinerary: 2021 Emirates. All Rights ReservedMATIULLAHNo ratings yet

- P2 Referral Package Check ListDocument1 pageP2 Referral Package Check ListMATIULLAHNo ratings yet

- Accounting For Business Transactions: Module - 1Document30 pagesAccounting For Business Transactions: Module - 1MATIULLAHNo ratings yet

- UsusuDocument1 pageUsusuMATIULLAHNo ratings yet

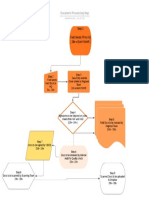

- Document Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)Document1 pageDocument Processing Map: Step 1 Field Sends FR To HQ (28 Each Month)MATIULLAHNo ratings yet

- Taxation Law For AFGHANISTANDocument1 pageTaxation Law For AFGHANISTANMATIULLAHNo ratings yet

- Reference Letter For Immigration 01Document1 pageReference Letter For Immigration 01MATIULLAHNo ratings yet

- SGB 2013 - 4amend.1 (Financial Regulations and Rules of The United Nations)Document13 pagesSGB 2013 - 4amend.1 (Financial Regulations and Rules of The United Nations)Muhammad Hafiz SalehNo ratings yet

- Supplemental Siv Chief of Mission ApplicationDocument1 pageSupplemental Siv Chief of Mission Applicationroberto perezNo ratings yet

- Detailed Project Proposal For: Earnesta Child and Youth Development ProjectDocument11 pagesDetailed Project Proposal For: Earnesta Child and Youth Development ProjectMATIULLAHNo ratings yet

- Itemized Budget - WAW 972 002 SOMDocument4 pagesItemized Budget - WAW 972 002 SOMMATIULLAHNo ratings yet

- Supplemental Siv Chief of Mission ApplicationDocument1 pageSupplemental Siv Chief of Mission Applicationroberto perezNo ratings yet

- GIZ-Afghanistan: A. Position Applied ForDocument3 pagesGIZ-Afghanistan: A. Position Applied ForMATIULLAHNo ratings yet

- WAW Audit Findings 113394 & 109111Document2 pagesWAW Audit Findings 113394 & 109111MATIULLAHNo ratings yet

- 2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07Document79 pages2007 Sida-UNDP Evaluation Revised Final Report - 9 August 07MATIULLAHNo ratings yet

- Waw Aide MemoireDocument5 pagesWaw Aide MemoireMATIULLAHNo ratings yet

- Template letter to MP for refugee English accessDocument1 pageTemplate letter to MP for refugee English accessMATIULLAHNo ratings yet

- Unaccompanied Asylum Seeking Children Statement of Evidence (SEF)Document43 pagesUnaccompanied Asylum Seeking Children Statement of Evidence (SEF)MATIULLAHNo ratings yet

- V - Audits and Compliance - FINAL - SEBDocument9 pagesV - Audits and Compliance - FINAL - SEBMATIULLAHNo ratings yet

- What Is Allowable - Eligible Cost Sharing - MIT Research Administration ServicesDocument4 pagesWhat Is Allowable - Eligible Cost Sharing - MIT Research Administration ServicesMATIULLAHNo ratings yet

- Asylum Declaration Writing Guide: WWW - Uscis.govDocument14 pagesAsylum Declaration Writing Guide: WWW - Uscis.govMATIULLAHNo ratings yet

- Va Co 2021 06 04 - Humanitarian - Access - OfficerDocument5 pagesVa Co 2021 06 04 - Humanitarian - Access - OfficerMATIULLAHNo ratings yet

- Types of Expenditures That Can Be Cost Shared - Office of Research and Sponsored Programs - University of Arkansas at Little RockDocument4 pagesTypes of Expenditures That Can Be Cost Shared - Office of Research and Sponsored Programs - University of Arkansas at Little RockMATIULLAHNo ratings yet

- FA and FFA Full Specimen Exam AnswersDocument10 pagesFA and FFA Full Specimen Exam Answersanees munirNo ratings yet

- Deposits Scheme'S Saving: Features & BenefitsDocument47 pagesDeposits Scheme'S Saving: Features & BenefitsKaranPatil100% (1)

- SBI Acc InsDocument11 pagesSBI Acc InsAnonymous UjEPpvYDNo ratings yet

- Acc548 Wk2 TeamDocument22 pagesAcc548 Wk2 TeamBri Mallon100% (1)

- ACTPACO Manalo Unit 7Document16 pagesACTPACO Manalo Unit 7Arbee LuNo ratings yet

- Business EnglishDocument35 pagesBusiness EnglishNicoleta SasNo ratings yet

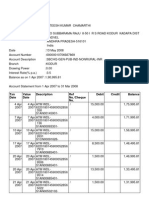

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesatishapexNo ratings yet

- Chart of Accounts Assets Liabilities Owner'S Equity Income ExpensesDocument2 pagesChart of Accounts Assets Liabilities Owner'S Equity Income ExpensesErika Bucao100% (1)

- Accounting language guides business decisionsDocument69 pagesAccounting language guides business decisionsConnor MillerNo ratings yet

- Audit ProbDocument36 pagesAudit ProbSheena BaylosisNo ratings yet

- History of Accounting Thought-1Document13 pagesHistory of Accounting Thought-1Valentino ArisNo ratings yet

- BASIC Book KeepingDocument79 pagesBASIC Book KeepingRicky BaldadoNo ratings yet

- Financial Asset at Amortized CostDocument20 pagesFinancial Asset at Amortized CostJudith Gabutero0% (1)

- Cost Quizlet 3Document13 pagesCost Quizlet 3agm25No ratings yet

- Financial Accounting Config S4HANADocument64 pagesFinancial Accounting Config S4HANAalegpontonNo ratings yet

- Acct 2021 CH 2 Completion of The WorksheetDocument20 pagesAcct 2021 CH 2 Completion of The WorksheetAlemu BelayNo ratings yet

- DGPS SurveyDocument21 pagesDGPS SurveyHitesh JangidNo ratings yet

- SAP ProjectDocument75 pagesSAP Projectansari nj100% (1)

- Fundamentals of Financial Accounting - CIMA Financial Management MagazineDocument5 pagesFundamentals of Financial Accounting - CIMA Financial Management MagazineLegogie Moses AnoghenaNo ratings yet

- Analysis of Pupil Performance: AccountsDocument49 pagesAnalysis of Pupil Performance: AccountsAJNo ratings yet

- Audit of LiabilitiesDocument6 pagesAudit of LiabilitiesandreamrieNo ratings yet

- EBS India GST Update 17-Jan-2017Document24 pagesEBS India GST Update 17-Jan-2017Hitesh TutejaNo ratings yet

- TLE Major Field GuideDocument17 pagesTLE Major Field GuideShella CortezNo ratings yet

- Foreign Exchange Operational Guidelines 2020 Department of Foreign Exchange and Reserve ManagementDocument31 pagesForeign Exchange Operational Guidelines 2020 Department of Foreign Exchange and Reserve ManagementLungten PhuentshoNo ratings yet

- DrillDocument10 pagesDrillgnim1520No ratings yet

- N. Title Location: List of Examples IFRS 15 Revenue From Contracts With CustomersDocument27 pagesN. Title Location: List of Examples IFRS 15 Revenue From Contracts With CustomersHồ Đan ThụcNo ratings yet

- EQP Salary LedgerDocument2 pagesEQP Salary Ledgerkarthikeyan PNo ratings yet

- Journal EntryDocument8 pagesJournal EntryAnklesh kumar GuptaNo ratings yet

- Internship Report Oninternship Report On UCB Imperial Savings Branding of United Commercial Bank LTD UCB Imperial Savings Branding of United Commercial Bank LTDDocument65 pagesInternship Report Oninternship Report On UCB Imperial Savings Branding of United Commercial Bank LTD UCB Imperial Savings Branding of United Commercial Bank LTDsatanic_soulNo ratings yet

- Study Resources: Earn Free AccessDocument17 pagesStudy Resources: Earn Free AccessTsegaye BojagoNo ratings yet