You might also like

- Leveraging on India: Best Practices Related to Manufacturing, Engineering, and ItFrom EverandLeveraging on India: Best Practices Related to Manufacturing, Engineering, and ItNo ratings yet

- Sigachi Q4FY22 Earnings Presentation Highlights Revenue Growth of 40%, PAT of Rs. 116 MnDocument16 pagesSigachi Q4FY22 Earnings Presentation Highlights Revenue Growth of 40%, PAT of Rs. 116 Mnknowme73No ratings yet

- 34bc670e-508d-4c44-87e6-b22c777b2d9dDocument21 pages34bc670e-508d-4c44-87e6-b22c777b2d9dHimanshu GuptaNo ratings yet

- Synopsis: MIC Electronics (MIC)Document21 pagesSynopsis: MIC Electronics (MIC)suru27No ratings yet

- Digitizing IndiaDocument64 pagesDigitizing IndiaAhmed MuneebNo ratings yet

- Company Flyer - VedantaDocument1 pageCompany Flyer - VedantaShrey RanaNo ratings yet

- 201909161805annual Report 2018-19Document248 pages201909161805annual Report 2018-19NILESH SHETENo ratings yet

- Phillip Capita On EMS Industry The Story of Local ManufacturingDocument141 pagesPhillip Capita On EMS Industry The Story of Local ManufacturingChirag ShahNo ratings yet

- Minda Corporation Ltd - Leading Automotive Component ManufacturerDocument14 pagesMinda Corporation Ltd - Leading Automotive Component ManufacturerSrini VasanNo ratings yet

- AnnualReport2022 23Document190 pagesAnnualReport2022 23purushothaman.sNo ratings yet

- Inox India Ltd. IPO Product NoteDocument3 pagesInox India Ltd. IPO Product NoteamansardarNo ratings yet

- UNO MINDA Group Enters Into Joint Venture Agreement With Katolec Corporation, Japan (Company Update)Document5 pagesUNO MINDA Group Enters Into Joint Venture Agreement With Katolec Corporation, Japan (Company Update)Shyam SunderNo ratings yet

- 82 - Amber ReportDocument5 pages82 - Amber ReportSaloniPatilNo ratings yet

- April 2022Document43 pagesApril 2022Indraneel MahantiNo ratings yet

- CM20220429 5abae 1adc1Document116 pagesCM20220429 5abae 1adc1Liora Vanessa DopacioNo ratings yet

- DNL FactsheetDocument5 pagesDNL FactsheetAmit KatriyaNo ratings yet

- Portfolio Management ReportDocument7 pagesPortfolio Management ReportAniruddh Singh ThakurNo ratings yet

- Competitive Environment of Computer Hardware IndustryDocument4 pagesCompetitive Environment of Computer Hardware IndustryYogesh YadavNo ratings yet

- Transcript Earnings Call Maruti Suzuki Q2 FY 23Document13 pagesTranscript Earnings Call Maruti Suzuki Q2 FY 23ElaineNo ratings yet

- Mosp Project Samsung India Electronics Pvt. LTDDocument15 pagesMosp Project Samsung India Electronics Pvt. LTDIntekhab AslamNo ratings yet

- Instrument Transformers Global LeadershipDocument12 pagesInstrument Transformers Global Leadershipganesh_d2k6100% (1)

- Consumer Durables ReportDocument9 pagesConsumer Durables ReportAzhaguraj VelumaniNo ratings yet

- PrintablesDocument5 pagesPrintablesKeshav KhetanNo ratings yet

- Rudrali Hitech - IM - 2020 - Unlocked - 1Document47 pagesRudrali Hitech - IM - 2020 - Unlocked - 1Rudrali HitechNo ratings yet

- Syngene 3Document44 pagesSyngene 3Puneet KapoorNo ratings yet

- Make in India PresentationDocument24 pagesMake in India PresentationShivam chauhnNo ratings yet

- Avantel Initial (HDFC)Document12 pagesAvantel Initial (HDFC)beza manojNo ratings yet

- Ar17 18 PDFDocument236 pagesAr17 18 PDFRohith ReddyNo ratings yet

- Nirlon Limited Updates Investor Presentation for Nine Months Ended December 2021Document28 pagesNirlon Limited Updates Investor Presentation for Nine Months Ended December 2021Bethany CaseyNo ratings yet

- Annual Report 2022Document366 pagesAnnual Report 2022Sagar chNo ratings yet

- Kiri Q4FY20 EarmingsDocument28 pagesKiri Q4FY20 EarmingsSwamiNo ratings yet

- United Drilling Tools LTD Visit NoteDocument12 pagesUnited Drilling Tools LTD Visit Noteharsh agarwalNo ratings yet

- Championing Change in The Indian Ace Industry Online Version v1Document32 pagesChampioning Change in The Indian Ace Industry Online Version v1irfanjamie1981No ratings yet

- Daikin Global Overview & India OperationsDocument27 pagesDaikin Global Overview & India OperationsIsha AggarwalNo ratings yet

- Dixon Technologies Q1 FY23 Earnings Call Summary - Revenue up 53% YoYDocument16 pagesDixon Technologies Q1 FY23 Earnings Call Summary - Revenue up 53% YoYPuneet kumarNo ratings yet

- SRTG Investor Presentation August 2023Document24 pagesSRTG Investor Presentation August 2023pokeyuNo ratings yet

- Analysis of Hindalco's working capital managementDocument18 pagesAnalysis of Hindalco's working capital managementAbhishek RaiNo ratings yet

- DTI 2021 Priority PAPsDocument70 pagesDTI 2021 Priority PAPsVictoria SalazarNo ratings yet

- 2021 Year of IPODocument61 pages2021 Year of IPOvijay saiNo ratings yet

- Grapite India PresentationDocument27 pagesGrapite India PresentationBhaskar DasguptaNo ratings yet

- Project Report On DixonDocument49 pagesProject Report On Dixon955762720067% (3)

- REIMAGINING TODAY FOR A BETTER TOMORROWDocument264 pagesREIMAGINING TODAY FOR A BETTER TOMORROWSavy DhillonNo ratings yet

- CIA-1 (Financial Management) ReportDocument14 pagesCIA-1 (Financial Management) Reportabhishek anandNo ratings yet

- Hindalco Investor Day 2022 PresentationDocument56 pagesHindalco Investor Day 2022 PresentationNarasimha Sai SangapuNo ratings yet

- Smartlink Annual Report 2015-16-25june2016 1Document84 pagesSmartlink Annual Report 2015-16-25june2016 1Siddharth ShekharNo ratings yet

- Cisco Market Analysis and Company OverviewDocument19 pagesCisco Market Analysis and Company Overviewsujith krishnaNo ratings yet

- GIM2012 Simple HandoutDocument3 pagesGIM2012 Simple HandoutRamesh BabuNo ratings yet

- SJS Q1fy24Document28 pagesSJS Q1fy24Akash PhogatNo ratings yet

- Siemens Industry Inspire Q4 NewsletterDocument6 pagesSiemens Industry Inspire Q4 NewslettershaileshwinsNo ratings yet

- Sarthak Metals Ltd.Document21 pagesSarthak Metals Ltd.saggttjsNo ratings yet

- TATA - Business StrategyDocument29 pagesTATA - Business StrategyMadhusudan Partani67% (12)

- Thanush projectDocument48 pagesThanush projectdhanushmrNo ratings yet

- High-Value ManufacturingDocument19 pagesHigh-Value ManufacturingPriyansh KhandelwalNo ratings yet

- Project Source: Funding ProposalDocument29 pagesProject Source: Funding Proposalheena23No ratings yet

- ITC Subsidiary 2023Document510 pagesITC Subsidiary 2023Akhil Mahi KaramchetiNo ratings yet

- Project of Entrepreneurship: Business Plan of A Start-UpDocument60 pagesProject of Entrepreneurship: Business Plan of A Start-UpMuhammad SaadNo ratings yet

- Dayananda Sagar Academy of Technology & Management, Udayapura Department of Management StudiesDocument11 pagesDayananda Sagar Academy of Technology & Management, Udayapura Department of Management StudiesSRIRAMA VKNo ratings yet

- HS 全球 投资策略 智能建筑:进一步投资以推动有机增长和并购 2020.3 90页Document92 pagesHS 全球 投资策略 智能建筑:进一步投资以推动有机增长和并购 2020.3 90页benNo ratings yet

- Annual Report 23Document364 pagesAnnual Report 23Sourav GhoshNo ratings yet

- Odisha Semiconductor PolicyDocument6 pagesOdisha Semiconductor Policydebasis_orkutNo ratings yet

- CRISIL AgrochemDocument2 pagesCRISIL AgrochemSandyNo ratings yet

- INFLOW CHEMICAL Company ProfileDocument19 pagesINFLOW CHEMICAL Company ProfileSandyNo ratings yet

- Vardhman Textiles LimitedDocument3 pagesVardhman Textiles LimitedSandyNo ratings yet

- 6 Finance RulesDocument8 pages6 Finance RulesSandyNo ratings yet

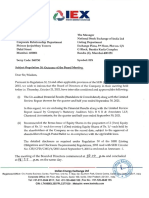

- IEX BOARD APPROVES BONUS ISSUEDocument16 pagesIEX BOARD APPROVES BONUS ISSUESandyNo ratings yet

- Affle Stock PricingDocument8 pagesAffle Stock PricingSandyNo ratings yet

- Bodal ChemicalsDocument1 pageBodal ChemicalsSandyNo ratings yet

- EdgeReport AFFLE CaseStudyDocument36 pagesEdgeReport AFFLE CaseStudySandyNo ratings yet

- BCG Q2FY22 ResultsDocument12 pagesBCG Q2FY22 ResultsSandyNo ratings yet

- 1645093193orna Brochure 151121Document28 pages1645093193orna Brochure 151121SandyNo ratings yet

- How Income Tax Department Tracks Your Income DetailsDocument2 pagesHow Income Tax Department Tracks Your Income DetailsSandyNo ratings yet

- 412-Economics Tools For Evalvating Shyam&SalimDocument12 pages412-Economics Tools For Evalvating Shyam&SalimSandyNo ratings yet

- PPPA22Document3 pagesPPPA22SandyNo ratings yet

- PLC AutomationDocument1 pagePLC AutomationSandyNo ratings yet

- COEP Building AutomationDocument1 pageCOEP Building AutomationSandyNo ratings yet

- Post Graduate Diploma in Industrial Automation (PGDIA) NewDocument4 pagesPost Graduate Diploma in Industrial Automation (PGDIA) NewSandyNo ratings yet

- QCI TrainingsDocument2 pagesQCI TrainingsSandyNo ratings yet

- JK Lakshmi Cement: Low Risk Buy. RS Positive Stock. Seen Buying From Last Accumulation ZoneDocument1 pageJK Lakshmi Cement: Low Risk Buy. RS Positive Stock. Seen Buying From Last Accumulation ZoneSandyNo ratings yet

- Management Resiko & Peluang PDFDocument39 pagesManagement Resiko & Peluang PDFzia.ulhaqNo ratings yet

- 22 Stage Analysis BioconDocument1 page22 Stage Analysis BioconSandyNo ratings yet

- BASF: RS Positive Stock. Ascending TriangleDocument1 pageBASF: RS Positive Stock. Ascending TriangleSandyNo ratings yet

- Tata Motors: RS Positive Stock. Price & Ratio Are Interestingly PoisedDocument2 pagesTata Motors: RS Positive Stock. Price & Ratio Are Interestingly PoisedSandyNo ratings yet

- Company Name: Shivalik Bimetal Controls LTDDocument4 pagesCompany Name: Shivalik Bimetal Controls LTDSandyNo ratings yet

- MetropolishDocument1 pageMetropolishSandyNo ratings yet

- Understanding PPFAS Mutual Fund's Investment Approach and ProcessDocument17 pagesUnderstanding PPFAS Mutual Fund's Investment Approach and ProcessSandyNo ratings yet

- Dividend Study of Nifty CompaniesDocument7 pagesDividend Study of Nifty CompaniesCraft DealNo ratings yet

- Audit QP - 1Document18 pagesAudit QP - 1sanket karwaNo ratings yet

- MF Scheme Performance MetricsDocument12 pagesMF Scheme Performance MetricsKiran VidhaniNo ratings yet

- CV PM Om 04 06 2019Document6 pagesCV PM Om 04 06 2019soumya19800000000No ratings yet

- 2021-2022 FRC Business PlanDocument4 pages2021-2022 FRC Business PlanAngel DuranNo ratings yet

- Patterson 1999Document18 pagesPatterson 1999Teodora Maria DeseagaNo ratings yet

- 095 Priyanka TejwaniDocument19 pages095 Priyanka TejwaniNitin BasoyaNo ratings yet

- Gantt Chart: Plant Pals Operations and Training Plan (Name)Document5 pagesGantt Chart: Plant Pals Operations and Training Plan (Name)brasilrulesNo ratings yet

- MATH4512 - Fundamentals of Mathematical Finance HomeworkDocument5 pagesMATH4512 - Fundamentals of Mathematical Finance HomeworkAnonymous pPeyKBmYNo ratings yet

- 126-Article Text-390-1-10-20230115Document16 pages126-Article Text-390-1-10-20230115Wayamis PutraNo ratings yet

- JP Morgan Industrials ConferenceDocument19 pagesJP Morgan Industrials ConferenceJames BrianNo ratings yet

- A. UNIQLO ProductDocument10 pagesA. UNIQLO ProductHải Đoànnn100% (1)

- Marketing Plan Restoran: October 2015Document29 pagesMarketing Plan Restoran: October 2015Ricky ImandaNo ratings yet

- ToolsDocument52 pagesToolsLisa Marie CaballeroNo ratings yet

- Name: Date: Score:: ActivityDocument1 pageName: Date: Score:: ActivityAllyza RenoballesNo ratings yet

- Tilahun EsmaelDocument46 pagesTilahun EsmaelFasika WorkuNo ratings yet

- N-LC-01 Bank of America v. CADocument2 pagesN-LC-01 Bank of America v. CAKobe Lawrence VeneracionNo ratings yet

- © Standard Legal Network Instructions - Page 1Document25 pages© Standard Legal Network Instructions - Page 1Thomson ValliyakalayilNo ratings yet

- Tvs Motor Company LimitedDocument10 pagesTvs Motor Company LimitedFakrudeen Ali Ahamed PNo ratings yet

- Entrepreneurship Risk TakingDocument3 pagesEntrepreneurship Risk TakingTAPAN HALDERNo ratings yet

- FA of SPDocument8 pagesFA of SPShivangi AggarwalNo ratings yet

- Paying BankerDocument5 pagesPaying BankerPrajwalNo ratings yet

- PejanDocument5 pagesPejanjolmarie llantoNo ratings yet

- Seminar Brochure Ceo YtlDocument2 pagesSeminar Brochure Ceo YtlChun Fai ChoNo ratings yet

- Project B Pact 315Document9 pagesProject B Pact 315ALYSSA PERALTANo ratings yet

- ABITRIA Online Assignment Chapter 11 and 12 1Document1 pageABITRIA Online Assignment Chapter 11 and 12 1Ian LamayoNo ratings yet

- HWAWELLTEX 2021-2022 Annual PDFDocument146 pagesHWAWELLTEX 2021-2022 Annual PDFCAL ResearchNo ratings yet

- Constitution of IndiaDocument7 pagesConstitution of IndiaRITIKANo ratings yet

- Theory Questions 5 PDF FreeDocument5 pagesTheory Questions 5 PDF FreeSamsung AccountNo ratings yet

- Fire Insurance Claim - HomeworkDocument18 pagesFire Insurance Claim - Homeworknikhilcoke7No ratings yet